As The Federal Reserve continues to withdraw its massive Covid-related monetary stimulus, US mortgage applications continue to fall to the lowest level since 1997.

Mortgage applications decreased 1.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 21, 2022.

The Refinance Index increased 0.1 percent from the previous week and was 86 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 42 percent lower than the same week one year ago.

Under Biden, we have seen (orange line) a significant decline in mortgage purchase applications (peak 2021 to this week). Mortgage rates are the highest since 2001 (wait for it!)

The Federal Reserve’s DOTS PLOT shows where each Fed official’s projection for the central bank’s key short-term interest rate is headed. As of the September 21, 2022 Fed Open Market Committee (FOMC) meeting, the prediction of future Fed target rates is decidedly DOWNWARD SLOPING.

The Fed hawks, those that want to tighten monetary policy, are Bowman, Waller, Kashkari, Mester and George. The Fed doves (or those who are neutral) are Biden recent appointees Barr, Cook, Jefferson, Logan, Collins. Note that Brainard and Bostic are the only technical doves.

I call the hawks at The Fed “The Blackhawks” since their mission of fighting inflation may lead to a recession. And Bowman, Mester and George are Lady Blackhawks.

25 days later. A real-life horror created by The Federal government.

Yes, according to the US Department of Energy, the US has only 25 days of diesel supply left.

The diesel crunch comes just weeks ahead of the midterm elections and has the potential to drive up prices for consumers who already view inflation and the economy as a top voting issue. Retail prices have been steadily climbing for more than two weeks. At $5.324 a gallon, they’re 50% higher than this time last year, according to AAA data.

Notably, National Economic Council Director Brian Deese recently commented on the emerging crisis. Deese said diesel inventories are “unacceptably low” and added that “all options are on the table.”

Yesh, diesel fuels prices are surging again as diesel inventory is shockingly low.

At least the US gets to live out a horror story created by The Federal government because failed Presidential candidate Al “The Snore” Gore and a teenage Swedish girl (Greta Thunberg) told Biden and Democrats to hate fossil fuels.

How dare you … drive inflation through the roof because of your green energy lunacy.

Things are getting interesting in DC, to say the least. The US is 100% likely to face a recession in the next 12 months while The Federal Reserve is on its crusade to fight inflation caused by … The Federal Reserve, Biden’s green energy shenanigans and massive, irresponsible Federal spending that even Former Obama economist Lawrence Summers warned would cause inflation. So what will The Fed do? Lower rates and expand their assets purchases to fight the impending recession OR keep tightening to fight Bidenflation? But where we are now is that the fixed-income market could be in big, big trouble.

For months, traders, academics, and other analysts have fretted that the $23.7 trillion Treasuries market might be the source of the next financial crisis. Then last week, U.S. Treasury Secretary Janet Yellen acknowledged concerns about a potential breakdown in the trading of government debt and expressed worry about “a loss of adequate liquidity in the market.” Now, strategists at BofA Securities have identified a list of reasons why U.S. government bonds are exposed to the risk of “large scale forced selling or an external surprise” at a time when the bond market is in need of a reliable group of big buyers.

“We believe the UST market is fragile and potentially one shock away from functioning challenges” arising from either “large scale forced selling or an external surprise,” said BofA strategists Mark Cabana, Ralph Axel and Adarsh Sinha. “A UST breakdown is not our base case, but it is a building tail risk.”

In a note released Thursday, they said “we are unsure where this forced selling might come from,” though they have some ideas. The analysts said they see risks that could arise from mutual-fund outflows, the unwinding of positions held by hedge funds, and the deleveraging of risk-parity strategies that were put in place to help investors diversify risk across assets.

In addition, the events which could surprise bond investors include acute year-end funding stresses; a Democratic sweep of the midterm elections, which is not currently a consensus expectation; and even a shift in the Bank of Japan’s yield curve control policy, according to the BofA strategists.

The BOJ’s yield curve control policy, aimed at keeping the 10-year yield on the country’s government bonds at around zero, is being pushed to a breaking point.

Well. Bidenflation certainly isn’t helping, but Statist Economist and Cheerleader Janet Yellen can’t bring herself to blame green energy policies, rampant Federal spending or irresponsible Federal Reserve policies for the crisis.

You will note the differences between today and the financial crisis of 2008-2009. The financial crisis gave us a massive surge in government securities liquidity thanks to then Fed Chair Ben Bernanke imitating Japan’s Central Bank and buying US government securities. Fast forward to today and the liquidity index hasn’t budged much since 2010 (except for a little blip around the Covid Fed intervention of early 2020), but we are now seeing near 40-year highs in inflation and a barely declining Fed balance sheet. And M2 Money YoY (mostly commercial bank deposits) are crashing.

I am guessing that The Fed will pivot given that stock futures are way up for Monday. The Dow Jones mini is up 770 points and the S&P 500 mini is up 88.75 points.

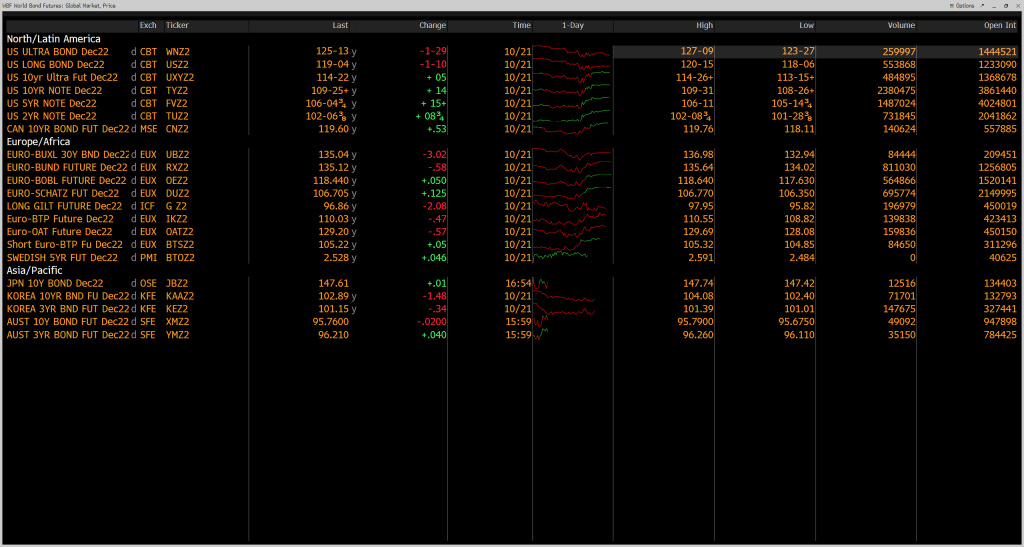

Bond market futures (specifically the US Ultra Bond) is down for Monday, meaning yields will be climbing.

I remember giving a speech at The Brookings Institute in Washington DC. Talk about stranger in a strange land. One person who I was debating got frustrated and said “You are such a … Republican!!!” As if that was the worst slur he could throw at me.

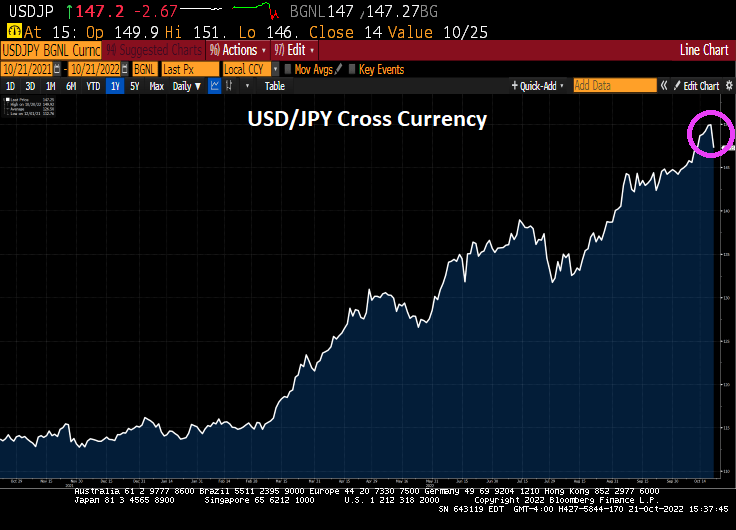

Wall Street saw another day of stunning reversals, with stocks rallying after a Treasury selloff sputtered. The yen jumped as Japan intervened again to prop up the currency.

After many twists and turns, the S&P 500 pushed solidly into the green and headed for its best week since June as 10-year yields fell from the highest since 2007.

Probably because The Fed is likely to pivot with impending recession. The Dow is up 774 points this Friday. And today was a huge option expiration day!!

And the 10-year Treasury yield fell -2.2 basis points.

Here is the result of Japan’s intervention.

But today’s numbers were largely monthly stock index option expiration.

Why did it fall upon Powell to be the wielder of the Fed tightening scimitar? Why didn’t Yellen? Because “Good Girls Don’t.” But Powell did.

Have a nice weekend. I will be rooting for Ohio State to annihilate the Iowa Hawkeyes at noon on Saturday.

Bloomberg’s recession probability over next 12 months is … 100%.

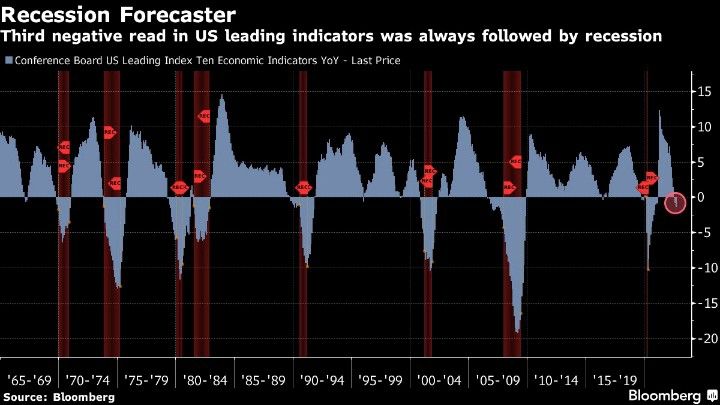

And how about the Conference Board’s Leading index of 10 economic indicators YoY? Third negative read ALWAYS followed by recession.

The Federal Reserve may be forced to pivot. This may be one reason why the Dow is up 565 points today (+1.86%) as recession and pain become ever more likely.

Look at commercial banks deposits. Wonder why liquidity is drying up?

One of my friends on Wall Street wrote my yesterday claiming “The 10-year Treasury yield is set to crash. Brace for impact!” Then I logged into Bloomberg this AM and saw the 10-year Treasury yield up almost 10 basis points (although it is down -2 BPS at 10:20am). Did markets not read his comments?? Maybe they did!

Well, The Fed is doing the Tighten Up. That is, The Fed is FINALLY removing their excessive monetary stimulus left over from the Bernanke Blowout (2008 adopting Japan’s print ’till you drop model).

But as The Fed removes their monetary stimulus (rate increases), we are seeing negative effects in the housing market. I call this chart “The X Factor.”

The US Treasury 10-year yield is up to 4.3% this morning, a far cry from 1.804% when Biden was crowned as President on January 20, 2021. The 30-year mortgage rate is up from 3.67% on Coronation Day to 7.32% yesterday, an increase of … 100% (that is, the 30-year mortgage rate has doubled under Biden). At the same time, Existing Home Sales YoY have gone from -2.41% in January 2021 to -23.79% in September 2022. THAT is a HUGE decline!

University of Michigan’s consumer sentiment for housing for 77 in January 2021 to 39 in November 2022. That is a -49% decline in consumer confidence. Also a big decline.

But going back to my pal’s email, he also said that The Fed is unwinding its balance sheet at a dangerously rapid rate (orange line). Relative to just increasing it, I would agree with him. But The Fed’s balance sheet is barely declining to my eyes. The troubling thing for housing is that inflation is so hot that REAL average hourly earnings YoY (yellow line) has fallen from +0.24% growth YoY on January 25, 2021 to a horrific -2.80% YoY rate in September 2022.

Bill’s point to me is that lending is still hot (at least commercial and industrial lending or C&I) while The Fed’s balance sheet remains in force (green line).

The Fed has a lot more work to do if they want to cool the commercial lending market. They have successfully slowed down the residential mortgage market.

Today’s existing home sales were … gruesome. While EHS month-over-month were down only -1.5%, on a year-over-year basis EHS was down a staggering -23.79%.

If you look at the declining growth rate of M2 Money (green line) and rising mortgage rates (yellow line), we can see why the housing market is struggling.

How about median price? That dropped to 8.07% YoY as inventory for sale remains lower than before Covid and Covid stimulypto.

US 30-year mortgage rates rose to 7.20% yesterday, the highest rate since 2000. Why?

Core inflation is rising and its the highest since 1992. Diesel prices, the all-important fuel for the transportation industry, is rising again after a brief respite and is near the all-time high.

But will mortgage rates continue to rise? That depends on The Federal Reserve. Will they continue to try to combat inflation (largely caused by … The Federal Reserve and voracious Federal spending under Biden/Pelosi/Schumer (The Three Amigos).

As of today, investors in Fed Funds Futures are pointing to a peak of Fed tightening in May 2023, then a slow decline in rates.

While this is The Fed Funds rate, it is likely that mortgage rates will continue to rise to May 2023 then level out at 9%-9.25%.

I really miss teaching college students. An example of a test question I gave was the first chart: who was The President when all hell broke loose (pink box)? 1) Joe Biden, 2) Donald Trump or 3) Millard Fillmore?

The answer, of course, is Joe Biden.

Doesn’t Millard Fillmore, the 13th President of the United States, look like actor Alec Baldwin after too many cheeseburgers and chocolate milkshakes at In-N-Out Burger?

Bear in mind that the are numerous wildcards in play, like the Russia/Ukraine war and the probability the China will invade Taiwan in the near future.

You must be logged in to post a comment.