According to the BLS, US core inflation is 6.3% and headline inflation is 8.3% YoY. But everything I consume seems to be going up at a much faster rate?

Under Biden, regular gasoline price is UP 55%, CRB Foodstuffs UP 47%, rents UP 12.5% YoY and electricity is UP 957%.

And as The Fed continues to signal monetary tightening, the spread between 30Y FNCL Par Coupon and the 10-year Treasury yield keeps growing.

In case you watched the Buffalo Bills play the Miami Dolphins yesterday, you may remember this punt by the Dolphins. It almost perfectly represents what The Federal Reserve and Biden Administration are doing to the American middle class and low-wage workers.

And I thought the Washington Commanders QB Carson Wentz getting sacked nine times in a game against his former team was bad!

We start the week with another chapter of “The Worst Bond Bubble Burst Since 1949.” This time its the US Treasury 10yr-2yr yield curve inverted to its lowest level since 2000.

Then across the pond, the UK sovereign yield curve is also inverted. But this curve is only inverted to 2008 levels of The Great Recession. The UK 2-year sovereign yield is up over 50 basis points this morning.

Then we have the US Dollar Swaps curve (green line), steeply UPWARD sloping until 6 months, then declining. The same goes for the US Treasury Actives curve (blue line), except that is it steeply upward sloping out to 1 year then begins declining.

And then we have the Bankrate 30-year mortgage rate rising to 6.59%, up 129% since Biden was sworn-in as President.

Also declining since Powell unleashed his monetary Panzers on the economy and financial markets are 1) agency MBS and 2) S&P 500 index.

The stock market’s value is down $7.6 trillion since Biden took office.

When I saw Carson Wentz of the Washington Commanders getting sacked 9 times, I thought maybe Prince Harry was playing instead. Or maybe Meghan Markle.

Price Harry is on the left, Commanders QB Carson Wentz is on the right.

Pension funds hold large positions in US Treasuries and Agency Mortgage-backed Securities (MBS). As does America’s central bank, The Federal Reserve. All are suffering losses as The Fed fights inflation.

(Bloomberg) — Week by week, the bond-market crash just keeps getting worse and there’s no clear end in sight.

With central banks worldwide aggressively ratcheting up interest rates in the face of stubbornly high inflation, prices (created by The Fed, Biden’s Green Energy Follicies and reckless Federal spending) are tumbling as traders race to catch up. And with that has come a grim parade of superlatives on how bad it has become.

On Friday, the UK’s five-year bonds tumbled by the most since at least 1992 after the government rolled out a massive tax-cut plan that may only strengthen the Bank of England’s hand. Two-year US Treasuries are in the middle of the the longest losing streak since at least 1976, dropping for 12 straight days. Worldwide, Bank of America Corp. strategists said government bond markets are on course for the worst year since 1949, when Europe was rebuilding from the ruins of World War Two.

The escalating losses reflect how far the Federal Reserve and other central banks have shifted away from the monetary policies of the pandemic, when they held rates near zero to keep their economies going. The reversal has exerted a major drag on everything from stock prices to oil as investors brace for an economic slowdown.

And as The Fed tries to combat stubborn inflation (caused by The Fed, Biden’s Green Energy folly and reckless Federal spending), you can see the US government security liquidity is worsening.

At least inflation has produced one “positive.” REAL mortgage rates are NEGATIVE since Freddie Mac’s 30-year mortgage rate less headline inflation is currently -2.975%.

Then we have Agency MBS (example, FNCL 3% MBS) plunging like a paralyzed falcon as duration risk increases with Fed rate tightening.

Fed Funds Futures data points to tightening until May ’23, then a reversal of rate hikes.

First, let’s look at the S&P 500 index since August 24, 2020 (white line) and compare that to just before The Great Recession 04/15/06 – 05/17/08. They look pretty similar.

Second, let’s look at returns on long-term US Treasuries (10yr+, white line) and US mortgage-backed securities (gold line) since The Fed undertook “Operation Crush Inflation!” (green line).

I saw The President’s press secretary fielding questions about the declining stock returns and impending recession. She responded “But the labor market is strong!” Well, Ms. Karine Jean-Pierre, I am sure President’s Biden economic advisor Jared Bernstein told you unemployment was at a very low level just prior to 1) The Great Recession and 2) The Great Covid-shutdown Recession). So, claiming that the US employment market is strong economy ignores that unemployment will surge if the economy slows … which is what The Fed is trying to do.

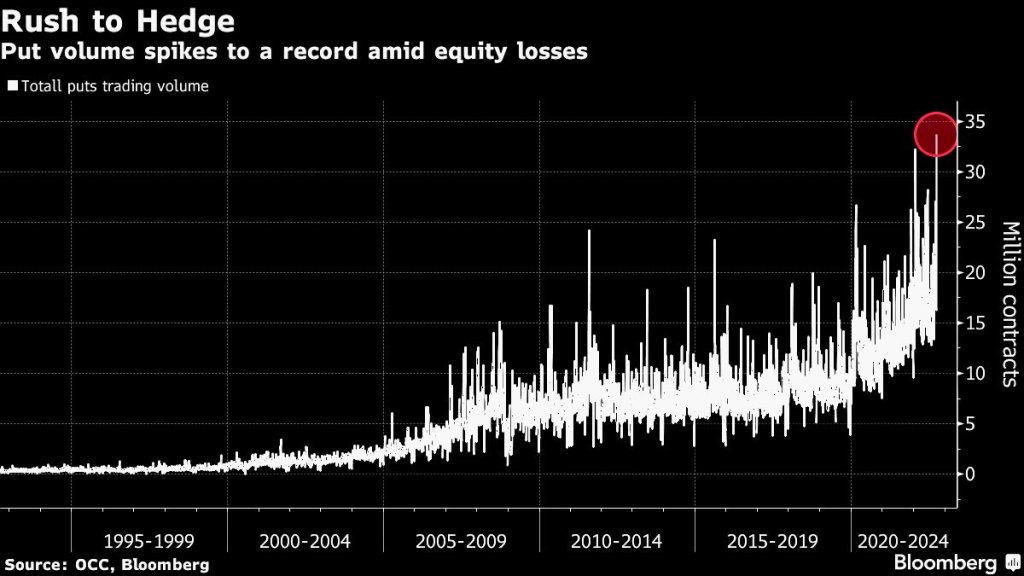

There is a rush to hedge the downside with The Fed tightening the monetary noose.

As The Federal Reserve battles inflation (caused by excessive monetary stimulus since 2008), Biden’s green energy policies and excess Federal government spending), we can see that the US Treasury 10yr-2yr yield curve has inverted to -54.4 basis points, the lowest since 1982 after Fed Chair Paul Volcker’s war on inflation.

The US Treasury 10yr-2yr yield curve typically inverts (or goes below zero) several months prior to a recession and is most inverted since 1982.

Fed Funds futures data points to the target rate rising to 4.613% by the May ’23 FOMC meeting … then declining.

Since this is rather miserable news for the economy, I will now play my favorite Bruce Springsteen tune, Sherry Darling.

At least the Dow Jones mini-me futures are up this morning.

The US Dollar/Euro cross currency is rising with Fed tightening.

As expected, The Federal Reserve raise their target rate by 75 basis points today. While that sounds like an inflation (blue line)-crushing rate hike, look at the slowly shrinking Fed Balance Sheet (gold line).

Of course, the risk of a recession (dark blue line) is on the increase.

Given the increasing likelihood of a recession, The FOMC’s Dots Project shows The Fed’s target rate increasing to 4.625% in 2023, then gradually declining to 2.5% in the long run.

Fed Funds Futures data points to a peak in May 2023.

Well, The Federal Reserve is doing what they wanted … crushing the housing market as they fight inflation.

Today we get our first glimpse of the carnage in the housing market from August. With mortgage rates having soared and homebuilder sentiment tumbling (and permits plunging), it should be no surprise that existing home sales were expected to fall for the 7th straight month (-2.3% MoM vs -5.9% MoM in July).

Somewhat surprisingly, existing home sales ‘only’ fell 0.4% MoM in August (from a revised 5.7% MoM drop in July), but that is still 7 consecutive drops. This left existing home sales down 19.87% YoY.

Look at existing home sales YoY as M2 Money Yoy crashes.

Median prices YoY for existing home sales plunged to 7.63% while inventory for sale (yellow line) remains depressed.

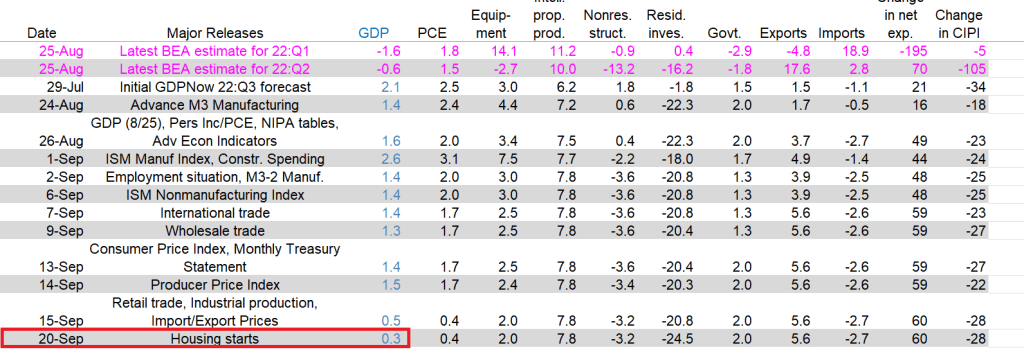

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2022 is 0.3 percent on September 20, down from 0.5 percent on September 15. After this morning’s housing starts report from the US Census Bureau, the nowcast of third-quarter residential investment growth decreased from -20.8 percent to -24.5 percent.

The culprit? US Housing starts!

We knew from this morning that housing starts declined -0.01% YoY as The Fed’s Stimulypto wears off.

Even Obama’s economic advisor, Larry Summers, is wondering why Biden won’t allow pipelines to be build to reduce energy prices and reduce inflation.

Having said that, US mortgage rates are now the highest since 2008 and continue to rise with the expectation of more Fed rate hikes this year. Even core inflation is on the rise motivating The Fed to do more tightening since they aren’t receiving any help from Biden on energy or Congress in terms of massive spending of our money.

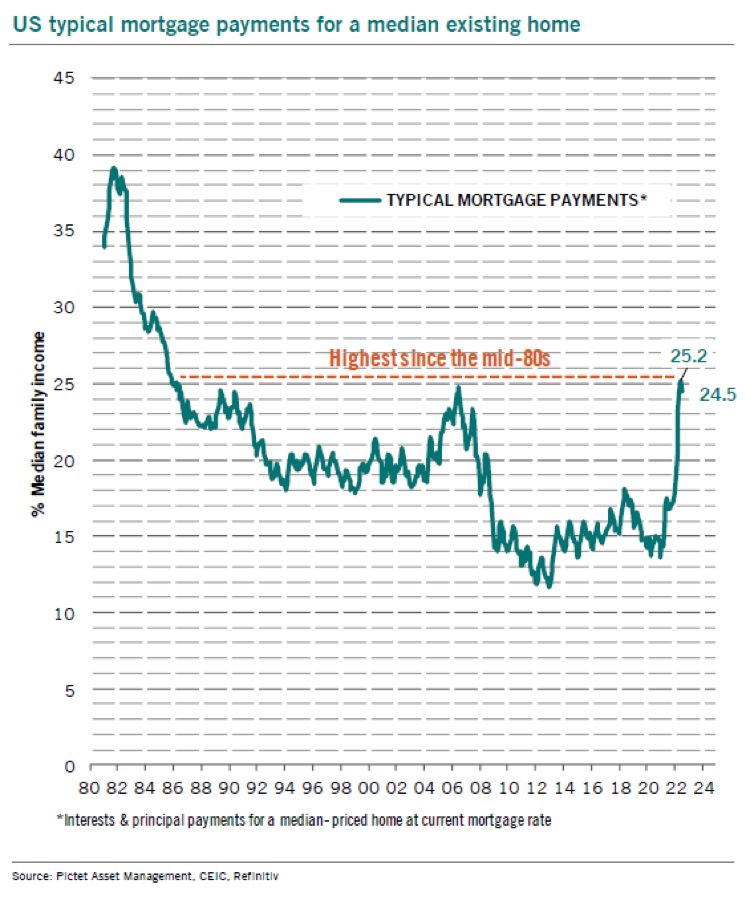

Mortgage payments for a median existing home in the US is back to the mid-1980s.

Data from Fed Funds futures implies that The Fed will raise their target rate to 4.50% by March 2023, then slowly lower rates.

Futures are down with the prospect of a 75 basis point bump in rates tomorrow. The Dow Jone Mini is down -167 points.

You must be logged in to post a comment.