Agency mortgage-backed securities (MBS) prices started to degrade as The Federal Reserve started to try to combat inflation caused by Biden’s energy policies and rampant Federal spending. That is, under June when the implied Fed O/N rate (red line) cooled and the 30-year mortgage rate (blue line) has come down a little.

In terms of duration risk, the FNCL 3% MBS duration has risen with anticipated Fed tightening.

So, further Fed tightening will result in greater MBS losses AND rising duration risk.

The US housing market is simply unaffordable for millions of Americans. To illustrate the problem, here is a chart of the Case-Shiller National home price index less CPI YoY graphed against Average Hourly Wages less CPI YoY.

The gap between the REAL national home price index YoY and REAL US average hourly earnings YoY is near the largest since 1988. Inflation is making matters far worse since REAL average hourly earnings growth continues to decline.

The only thing positive to say is that REAL home price growth YoY is lower now than at the peak of the 2005 home price bubble that burst catastrophically.

Another “positive” is that the REAL 30-year mortgage rate has fallen to -3.23%. At the peak of the house price bubble in June 2005, the REAL 30-year mortgage rate was +2.58%. THAT is one big difference between the pre-2008 recession and today’s impending recession.

Today’s jobs report was … strange. While the US economy added more jobs than expected, we also saw labor force participation contract and real wage growth decline again.

The reaction in the bond market? US Treasury 10-year yields exploded by +14 basis points. As I used to tell my fixed-income students, any basis point jump or decline of 10 basis points or more is a BIG DEAL.

The implied target rate for The Fed (based on Fed Funds Futures) is now lower for the Jan 1, 2024 FOMC meeting (3.025%) than it is for the Sept 21, 2022 FOMC meeting (3.034%).

Mortgage rates? They will go up as The Fed removes its Brawndo, the economy mutilator.

The media is thrilled with today’s jobs report showing a sizzling 528k jobs added to the US economy. And with that, the media is cheering that recession fears are shrinking.

But hold on a second.

First, while 528k jobs were added in July (great news!), REAL average hourly earnings growth YoY fell to -3.8173. Why? Because the rate of inflation is greater than nominal average hourly earnings YoY of 5.2%. That is BAD.

This charts shows that inflation-adjusted (or real) wage growth is the worst in recorded history.

And the “sizzling” jobs report isn’t feeling any love in the bond market where the US Treasury yield curve (10Y-2Y) deepened its inversion to -37.593 basis points, a drop of -1.331 BPS. Note that the 10Y-2Y curve falls below 0% just prior to every recession.

Labor force participation actually fell to 62.1% from 62.2% in June.

I am assuming that The Fed will misread the jobs report and argue for LESS COWBELL.

We are seeing a slowing of the US economy. For example, the JOLTs (job openings) numbers are out for June and they are down -5.5% from May. And from April to May, JOLTs declined -3.2% MoM. That is a clear slowing trend.

And on the housing front, the CoreLogic HPI Forecast indicates that home prices will increase on a month-over-month basis by 0.6% from June 2022 to July 2022 and on a year-over-year basis by 4.3% from June 2022 to June 2023. But rose +18.3% YoY in June. Also a clear cooling trend.

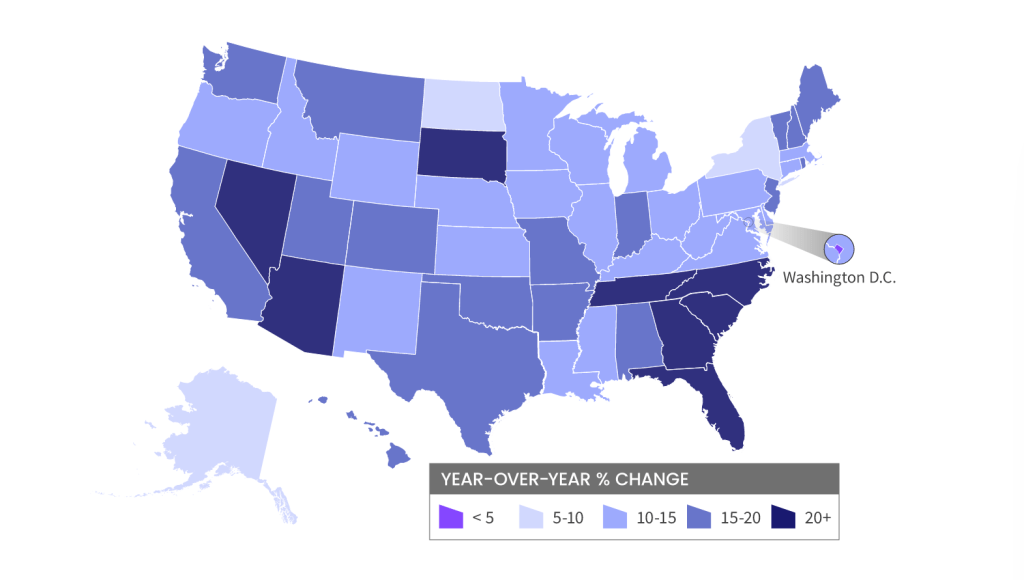

And its “Escape From Blue States” (perhaps a new Kurt Russell movie), with home prices rising fastest in red states (primarily The South). And contiguous migration from California to Nevada and Arizona.

The Fed Funds Futures market is pricing in rate hikes until the March 2023 FOMC meetings. After all, Prince Imhotep (aka, Minneapolis Fed’s Neel Kashkari) is screaming for more rate hikes to fight inflation … caused by 1) loose monetary policies since late 2008 and 2) insane Federal government spending.

Let’s see if “Mr. Freeze” (aka, Jerome Powell) relents on Fed rate increases before the March 2023 FOMC meeting.

US inflation, based on June’s Personal Consumption Expenditures (PCE) deflator, rose to its highest level since 1982. The PCE Deflator YoY rose to 6.8% while the core PCE deflator (less food and energy, the two things more households care about) rose to 4.8% YoY in June.

In order to fight inflation, The Federal Reserve is going to have to raise their target rate to … 17.78% based on 6.80% PCE deflator YoY. We are currently at 2.50%.

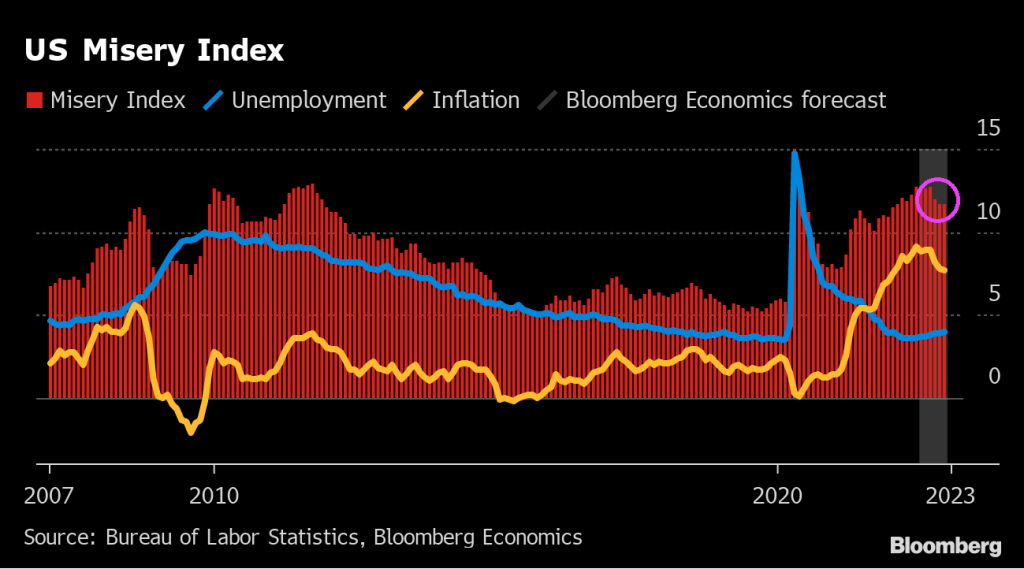

The US Misery Index remains elevated.

Based on the PCE Deflator YoY and U-3 unemployment, the misery index remains elevated compared to before Covid and The Fed’s/Federal government hyper-stimulypto to counter the Covid economic shutdowns. We never fully recovered.

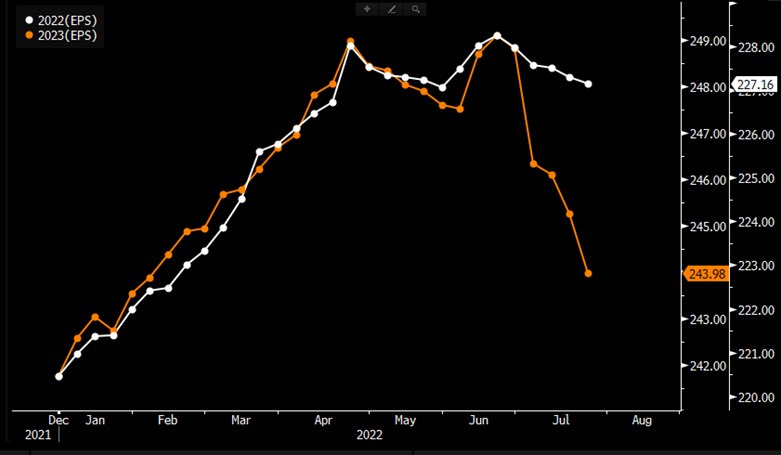

S&P 500 2023 EPS expectations falling off a cliff (orange line).

My former colleague at Deutsche Bank, Joe Carson, said recently that the US economy is not in a recession, but corporate profits are in a recession. While I cling to the traditional definition of recession (two consecutive quarters of negative real GDP growth), there is another component of the US economy that is in recession: consumer sentiment.

The University of Michigan Consumer Sentiment Index rose slightly in the latest release, but remains depressed at 51.5. University of Michigan Buying Conditions for House also rose to 47.0, also a depressed reading.

While unemployment remains low, the price of gasoline is crushing the wallets of American households helping to cause a recession in consumer sentiment.

Biden feebly attempts to explain why 2 consecutive quarters of negative real GDP growth (better known as contraction) is NOT a recession.

You must be logged in to post a comment.