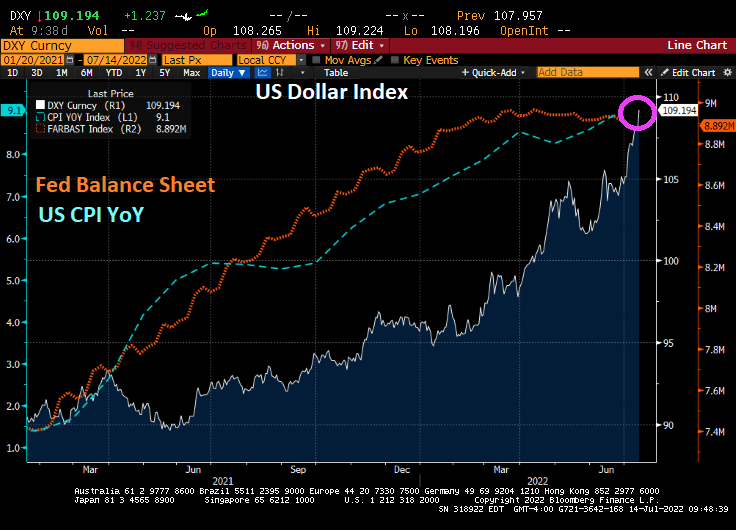

Bear in mind that a strong dollar is a two-edged sword. The US Dollar Index has risen 16% year-over-year, presenting a big hurdle for US firms with business overseas.

That strength of the greenback will rise until the Fed makes a dovish policy pivot.

And that pivot is forecast to occur at the Feb ’23 FOMC meeting.

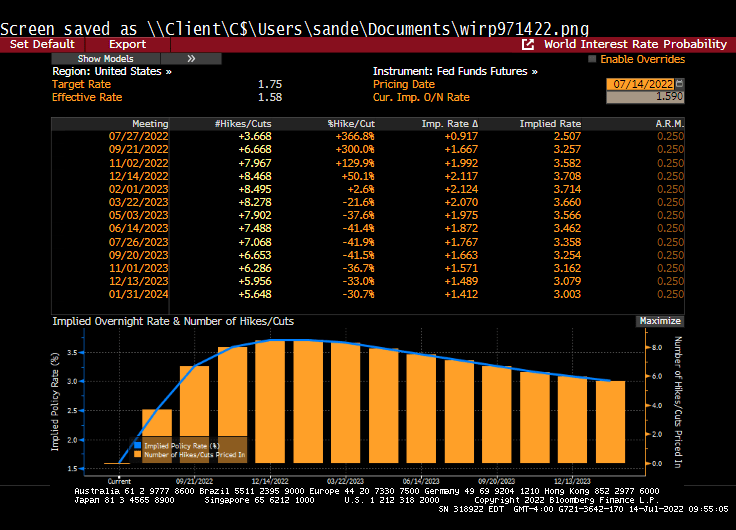

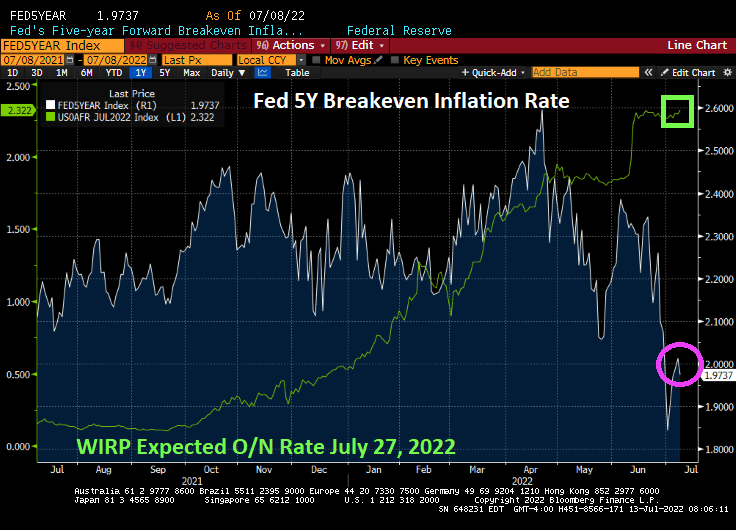

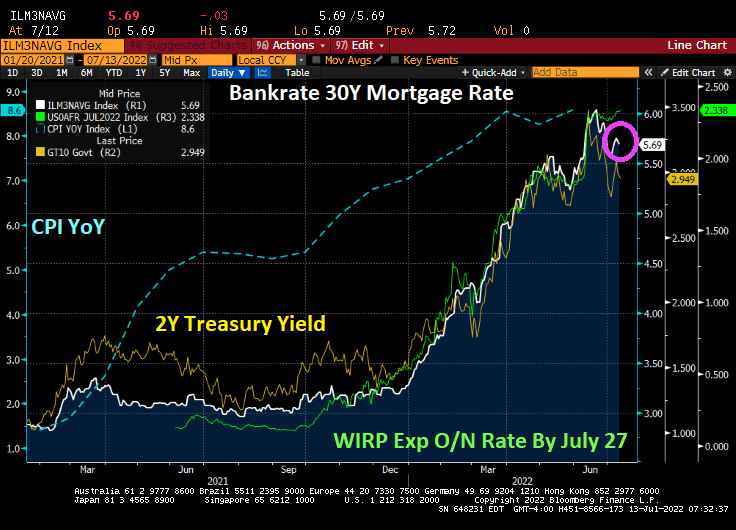

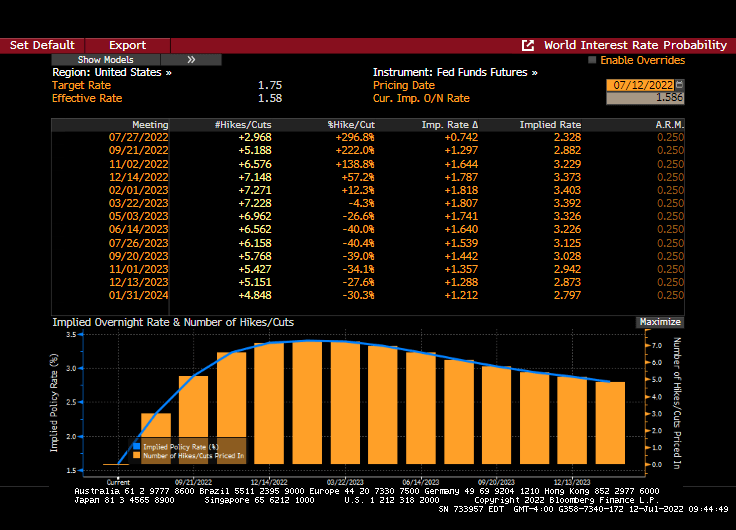

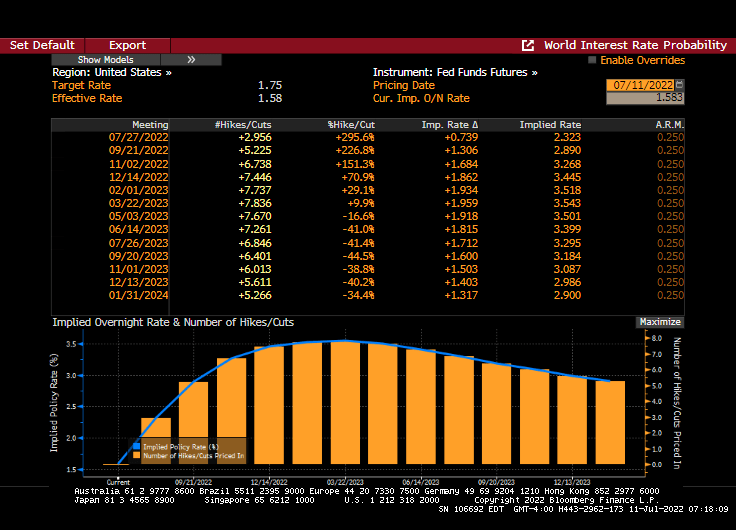

Here we go loop de loop! Traders are pricing in a 75 basis point rate increase at the July FOMC meeting despite collapsing Fed 5-year inflation breakeven rates.

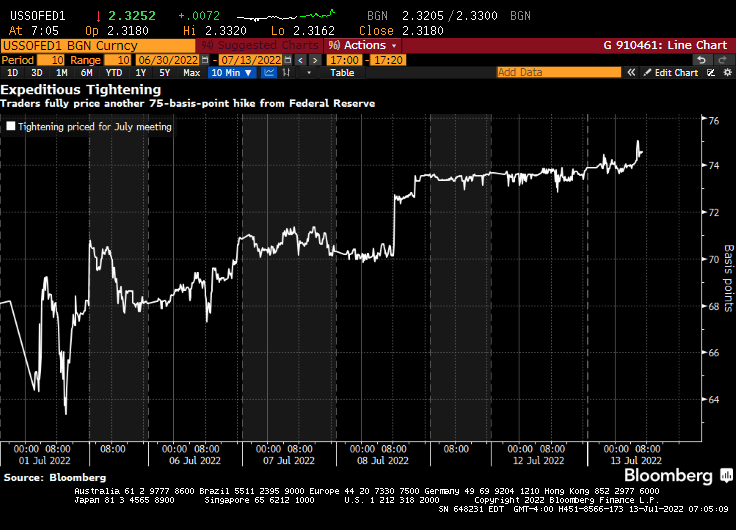

Money markets are betting on a three quarter-percentage point hike by Federal Reserve officials later this month, wagering the US will need to ramp up the pace of monetary tightening to tame inflation.

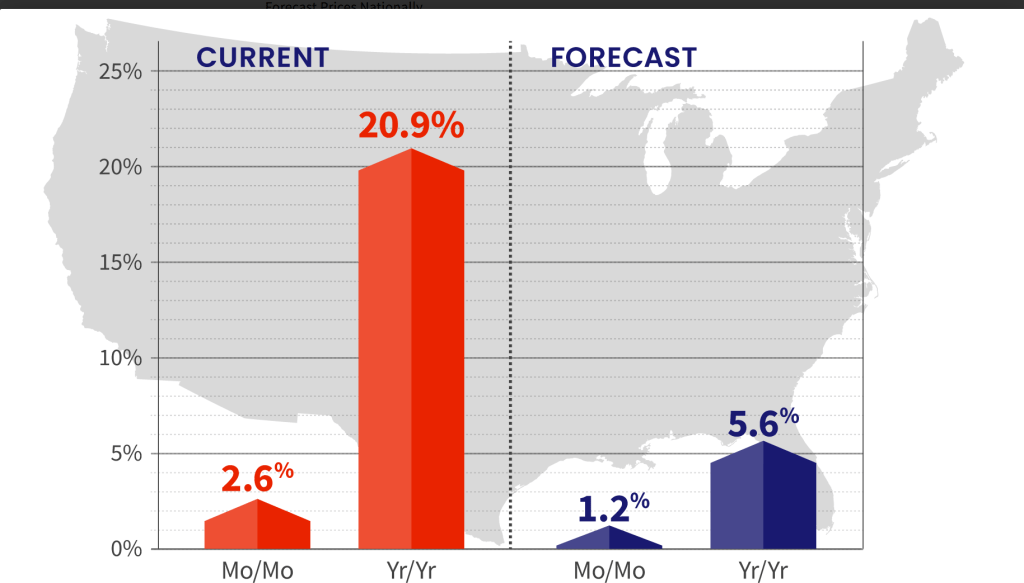

The repricing comes ahead of a key inflation report due Wednesday. The headline figure for June is set to accelerate to 8.8% year over year, the highest since 1981.

Bankrate’s 30Y mortgage rate fell slightly ahead of today’s inflation report with the expectation of The Fed hiking their target rate by 75 basis points to 2.338% at the July 27th Fed Open Market Committee meeting.

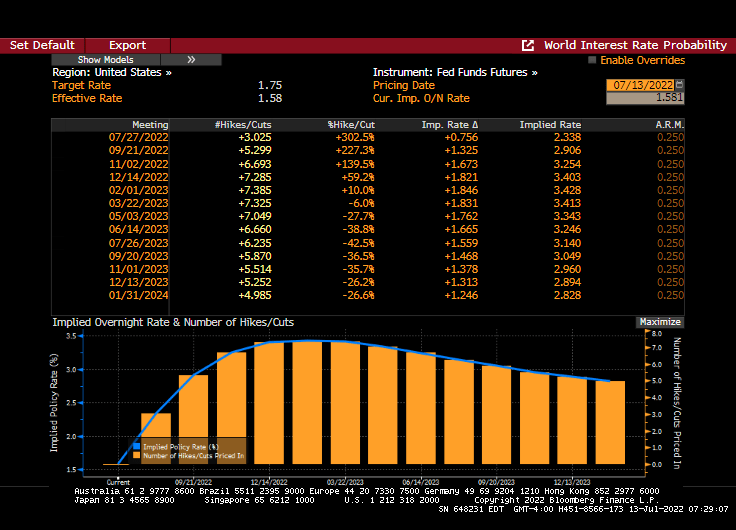

Trader expectations from Fed Funds Futures data:

Last night I watched “The Shallows” on Peacock TV. I thought from the title that it was going to be a biography of The Federal Reserve, but it was a film about a surfer being attacked by a shark.

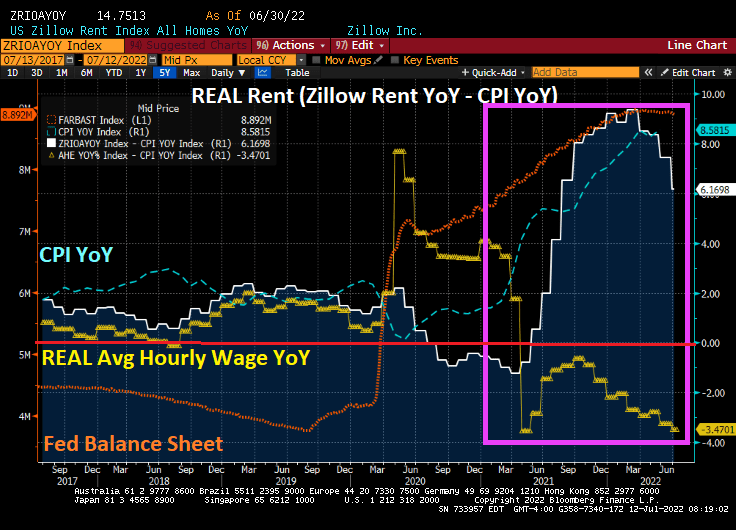

We are all aware that inflation is soaring, since the Covid outbreak in 2020 and the massive overaction by The Federal Reserve and Federal government in terms of stimulus spending and economic lockdowns.

Things were “normal” before Covid in that REAL housing rent (white line) and REAL average hourly earnings YoY (yellow line) moved together. But after Covid shutdowns and Federal stimulus “relief” (orange line), we see that inflation (blue line) took off along with the growth in housing rent. The problem, of course, is that REAL average hourly earnings YoY has been declining. I call this “The Great Divide in housing affordability”.

The question, of course, is whether The Federal Reserve will continue their “war on inflation” with a 75 basis point rate increase.

Inflation is at its fastest pace in 40 years, and is expected to increase even higher in tomorrow’s inflation report.

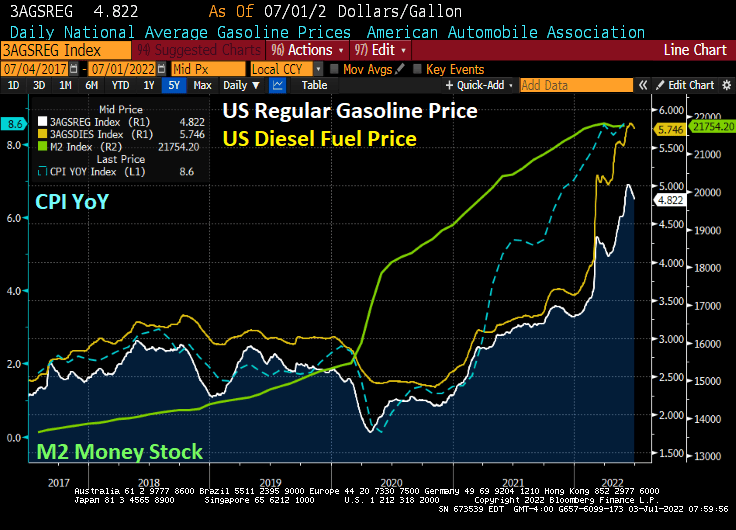

Gasoline prices have been dropping recently, but remain above $4.50 per gallon (regular gas price was $2.40 per gallon on Biden’s inauguration day. And no, it wasn’t the Biden Administration selling nearly 1 million barrels of crude oil from the strategic petroleum reserve to the Chinese government-owned Sinopec that Biden’s son Hunter is an investor (so, The Big Guy aka Joe Biden gets a 10% piece of the action). It is a slowing global economy that is helping to lower gasoline prices.

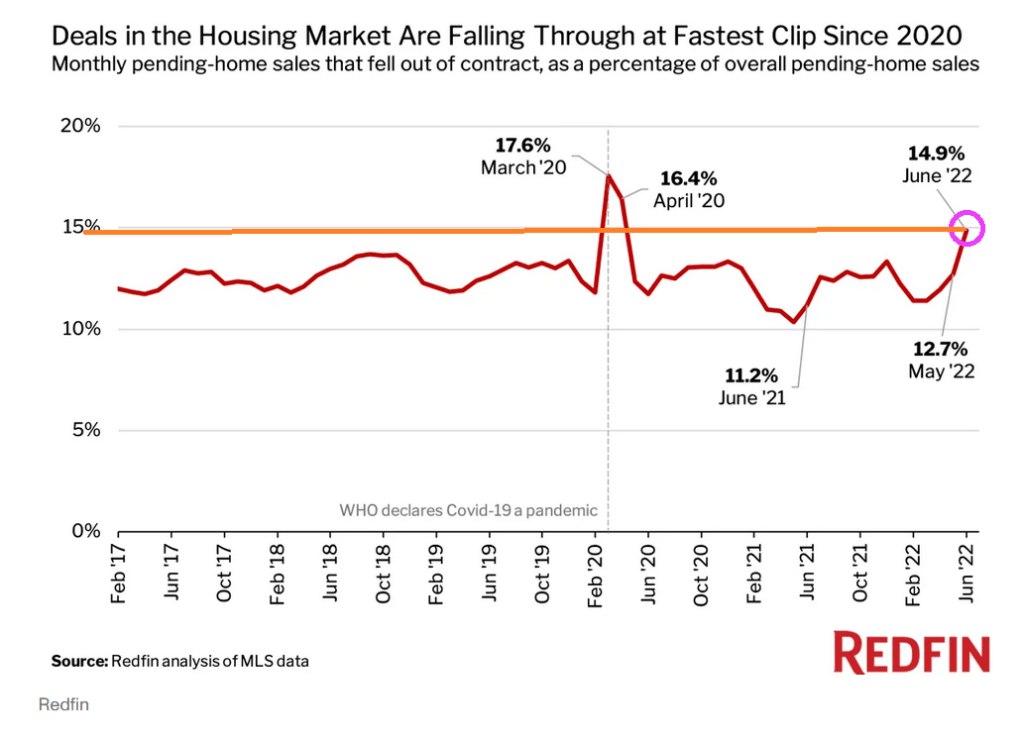

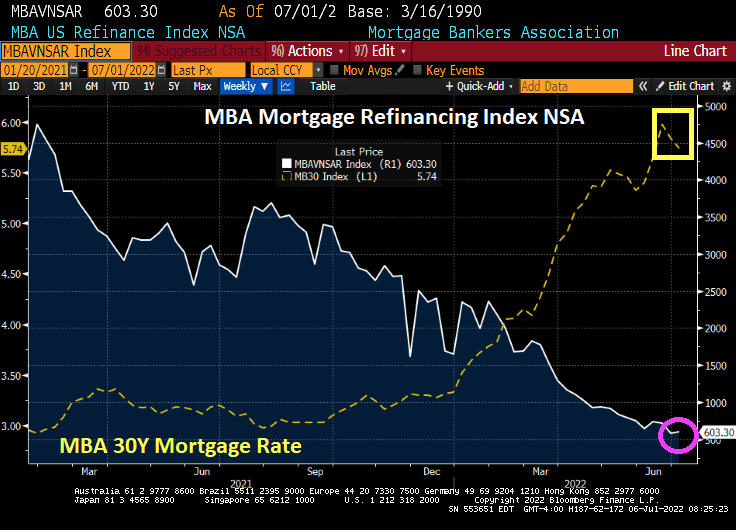

With rising mortgage rates, we are seeing a surge in pending home sales cancellations.

Atlanta Fed’s Raphael Bostic thinks that the US economy is so strong that it can easily handle a 75 basis point increase at the next FOMC meeting. Fortunately, he is not a voting member.

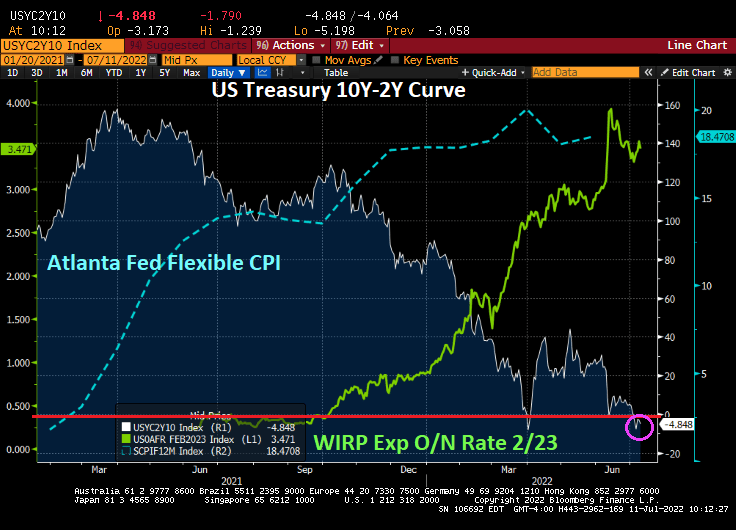

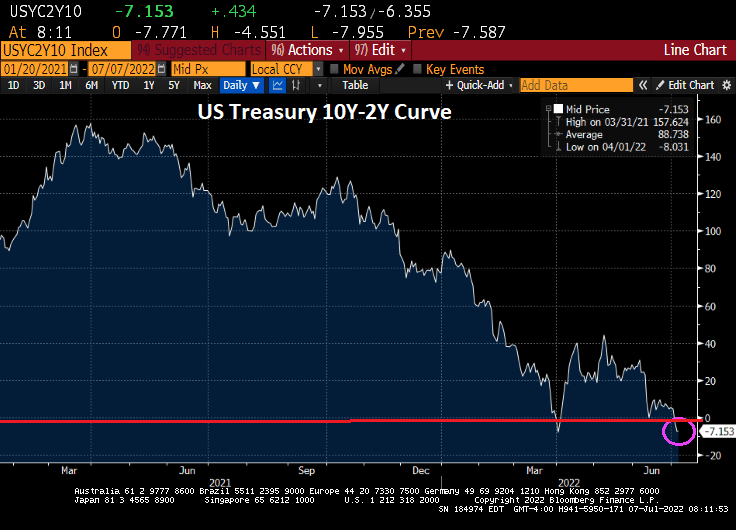

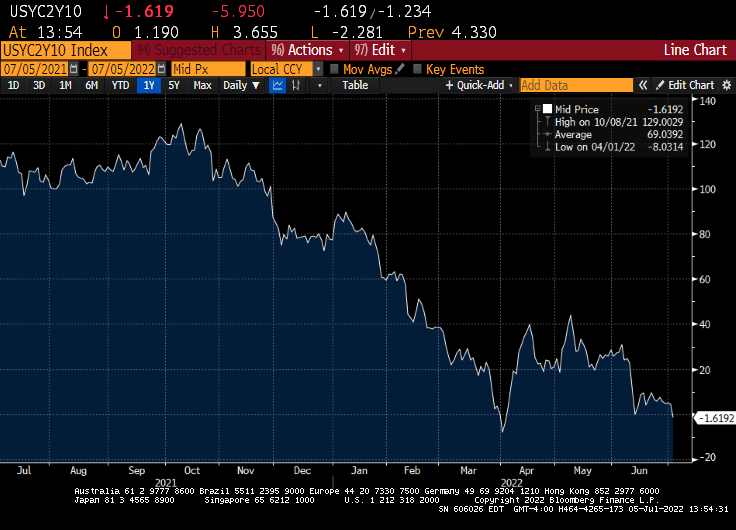

The US Treasury 10Y-2Y yield curve steepened after Biden’s inauguration as President, a sign of economic optimism. Then reality began to dawn when inflation began to surge (blue line). Then The Fed stepped in to combat inflation by signaling an increase in their target rate (green line). The result? The 10Y-2Y Treasury curve is inverted at -4.85 BPS, generally an indicator of an impending recession.

But never fear! The Feral Reserve is expected to reverse its rate increases by March 2023.

So, it looks like The Fed will be returning to its “low rider” rate policies in early 2023.

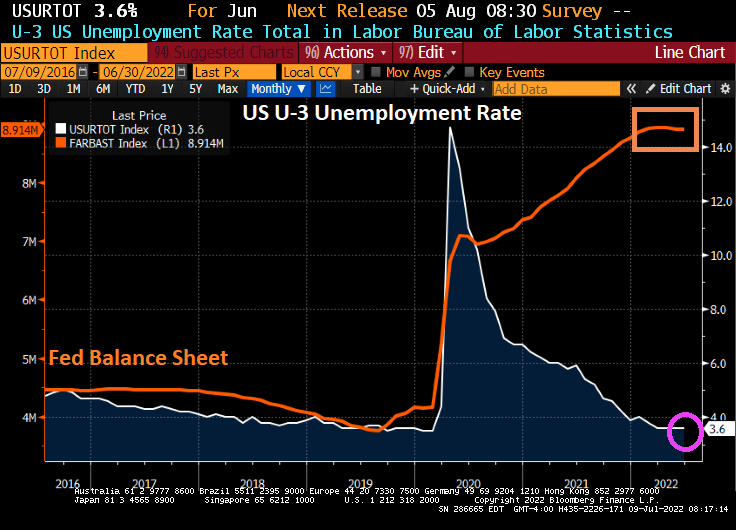

Take the US U-3 unemployment rate. The Biden Administration is proud of the unemployment rate of 3.6%. But if you look at the chart of unemployment relative to The Fed’s balance sheet expansion due to Covid lockdowns, there is still almost $9 trillion of Fed stimulus outstanding.

Of course, the lockdowns were pure economy killers, so opening the economies again led to the unemployment rate falling to 3.6% which is still higher than before the Covid outbreak. But The Federal Reserve has been painfully slow at shrinking its balance sheet, leaving almost $9 trillion in monetary stimulus outstanding.

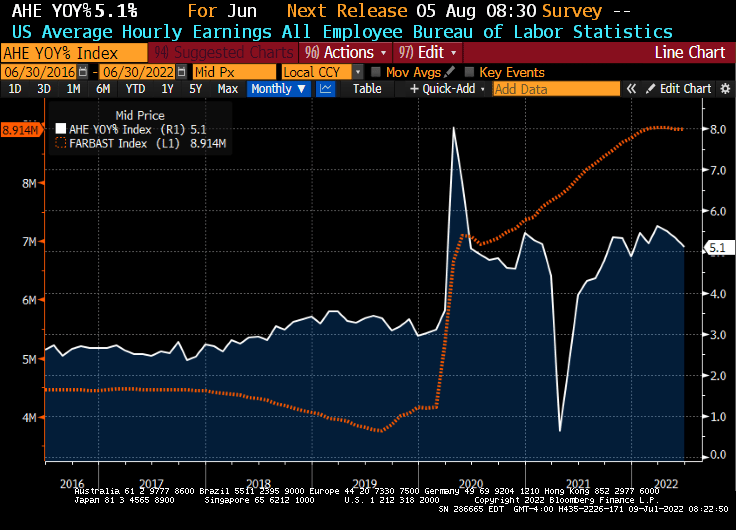

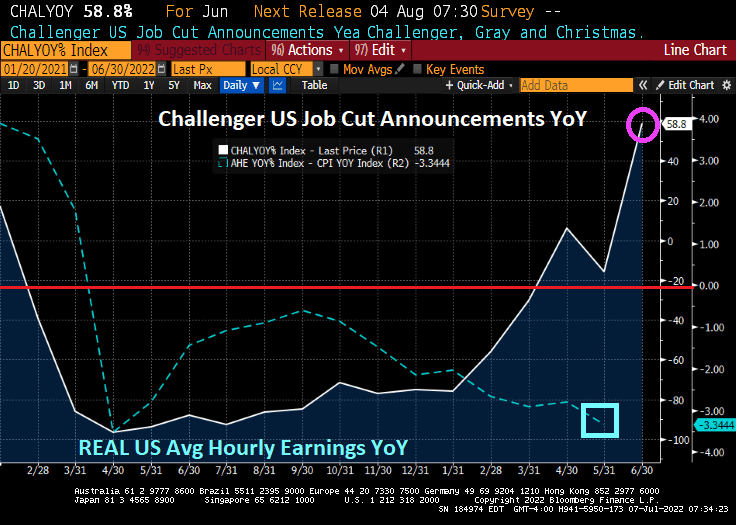

Take average hourly earnings growth. The media is all smiles as US wage growth declined to 5.1%, much higher than pre-Covid.

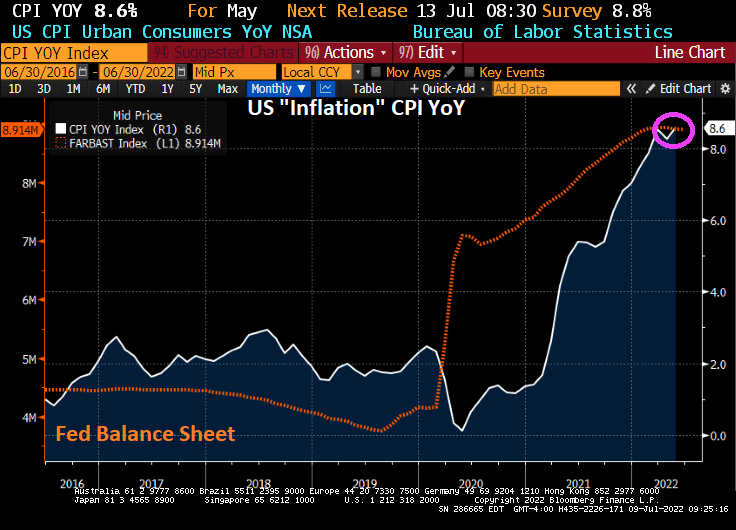

Then we have inflation, at 40-years highs thanks to massive Fed stimulus (and Federal spending).

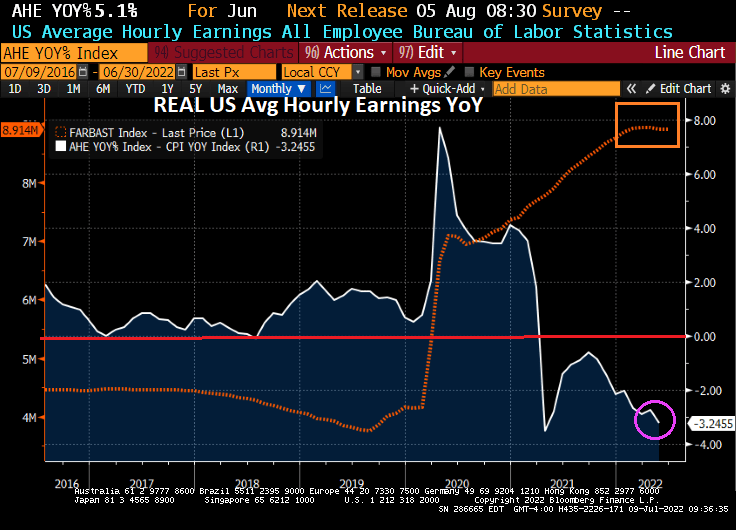

And if we deduct inflation from average hourly wage growth, we see REAL wage growth declining at a -3.25% YoY clip.

Lastly, we have the US Dollar. Nothing has been the same since the financial crisis of 2008 and the entrance of The Federal Reserve distorting the economy and prices. Not to mention the US Dollar.

The Fed leaving its monetary stimulus out in force for so long is a major policy error. So what happens when The Fed actually gets serious about withdrawing the monetary stimulus (likely after the midterm elections)?

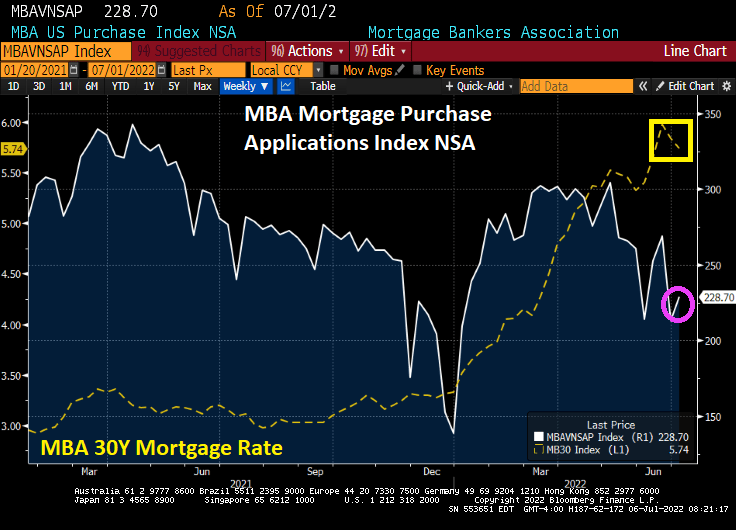

Well, this is one way to get inflation under control … crash the economy. And inflation fears growing, we are seeing mortgage rates declining and mortgage applications increasing.

Mortgage applications decreased 5.4 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 1, 2022. This week’s results include a holiday adjustment to account for early closings the Friday before Independence Day.

The seasonally adjusted Purchase Index decreased 4 percent from one week earlier. The unadjusted Purchase Index increased 7 percent compared with the previous week and was 17 percent lower than the same week one year ago.

The Refinance Index decreased 8 percent from the previous week and was 78 percent lower than the same week one year ago.

Hey, I thought Mayor Pete Buttigieg, the US Transportation Secretary, was supposed to unclog the supply-chain crisis! Instead, we get heartaches on heartaches as diesel prices rise 118% under Biden AND now the bottle-necks may get a lot worse.

A US Supreme Court decision that could force California’s 70,000 truck owner-operators to stop driving is set to create another choke point in already-stressed West Coast logistics networks, a truckers’ organization said.

“Gasoline has been poured on the fire that is our ongoing supply-chain crisis,” the California Trucking Association said in a statement following the Supreme Court’s decision to deny a judicial review of a decision of a lower court, a process known as certiorari.

“In addition to the direct impact on California’s 70,000 owner-operators who have seven days to cease long-standing independent businesses, the impact of taking tens of thousands of truck drivers off the road will have devastating repercussions on an already fragile supply chain, increasing costs and worsening runaway inflation,” the CTA said.

The association asked the Supreme Court for a review of a case challenging California’s Assembly Bill 5, a law that sets out three tests to determine whether a worker is an employee entitled to job benefits or an independent contractor who isn’t. The trucking industry relies on contractors, and has fought to be exempt from state regulations for years because of federal law.

With few exceptions, the relationship between independent truckers and their carriers, brokers and shippers will be governed by the tests.

As if US consumers aren’t getting crushed by rising prices already. In response to the Covid outbreak, The Fed slammed its foot on the money accelerator along with Federal government stimulus. Throw in Biden’s anti-drilling executive orders, and we have a nightmare.

Consumer confidence is already crumbling under inflation and rising energy prices.

You must be logged in to post a comment.