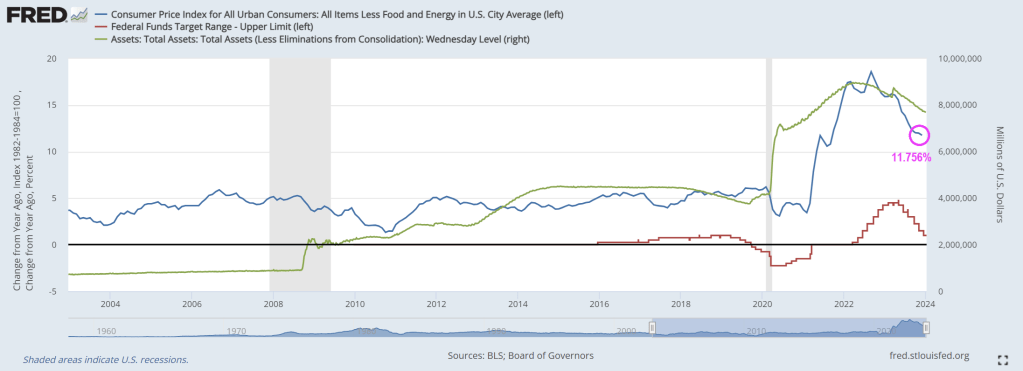

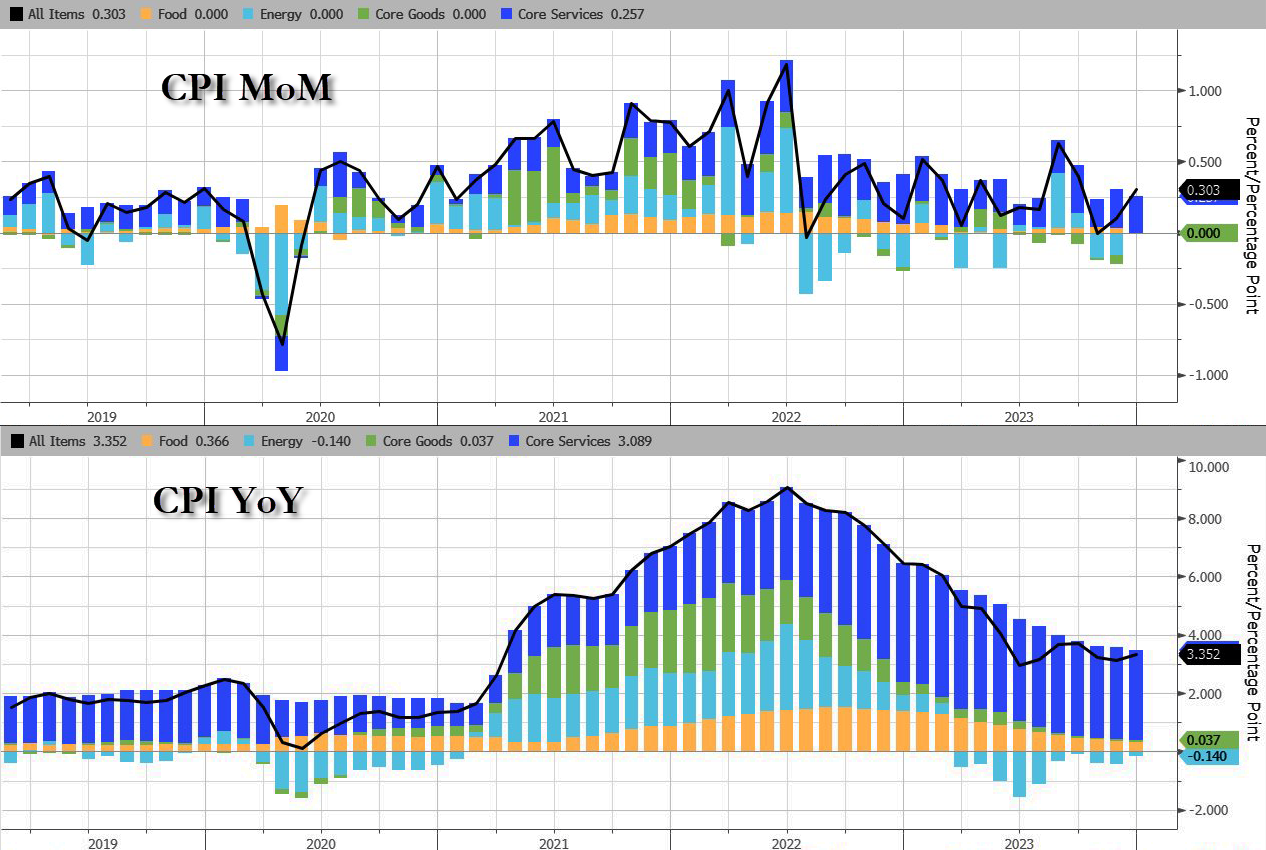

Although core inflation declined in December (CPI all items less food and energy), it is still hot, hot, hot at 4% Year-over-year (YoY). This raises the following question: Is The Fed tightening too much? Aka, yet another Fed policy error?? Since The Fed target rate is 5.50% and core inflation is now 4%?

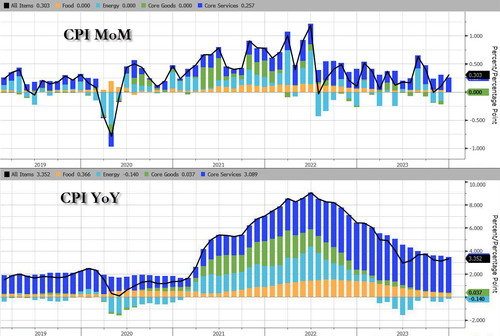

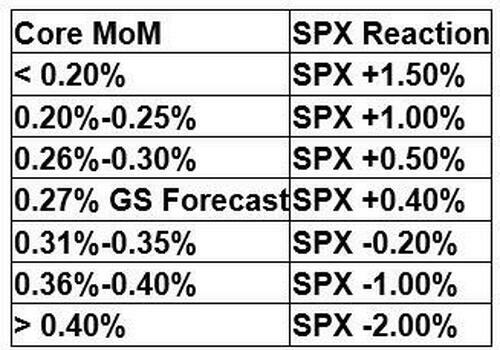

Headline Consumer Price Inflation printed hotter than expected in December, +0.3% MoM vs +0.2% exp and +0.1% prior, pushing the YoY headline CPI up to +3.4% (from +3.1% prior and hotter than the +3.2% exp)…

Source: Bloomberg

Services (Shelter mostly) costs re-accelerated and energy deflation stalled in December…

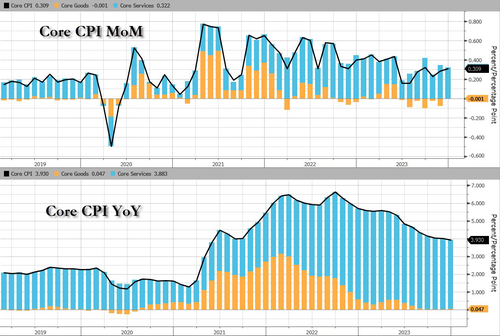

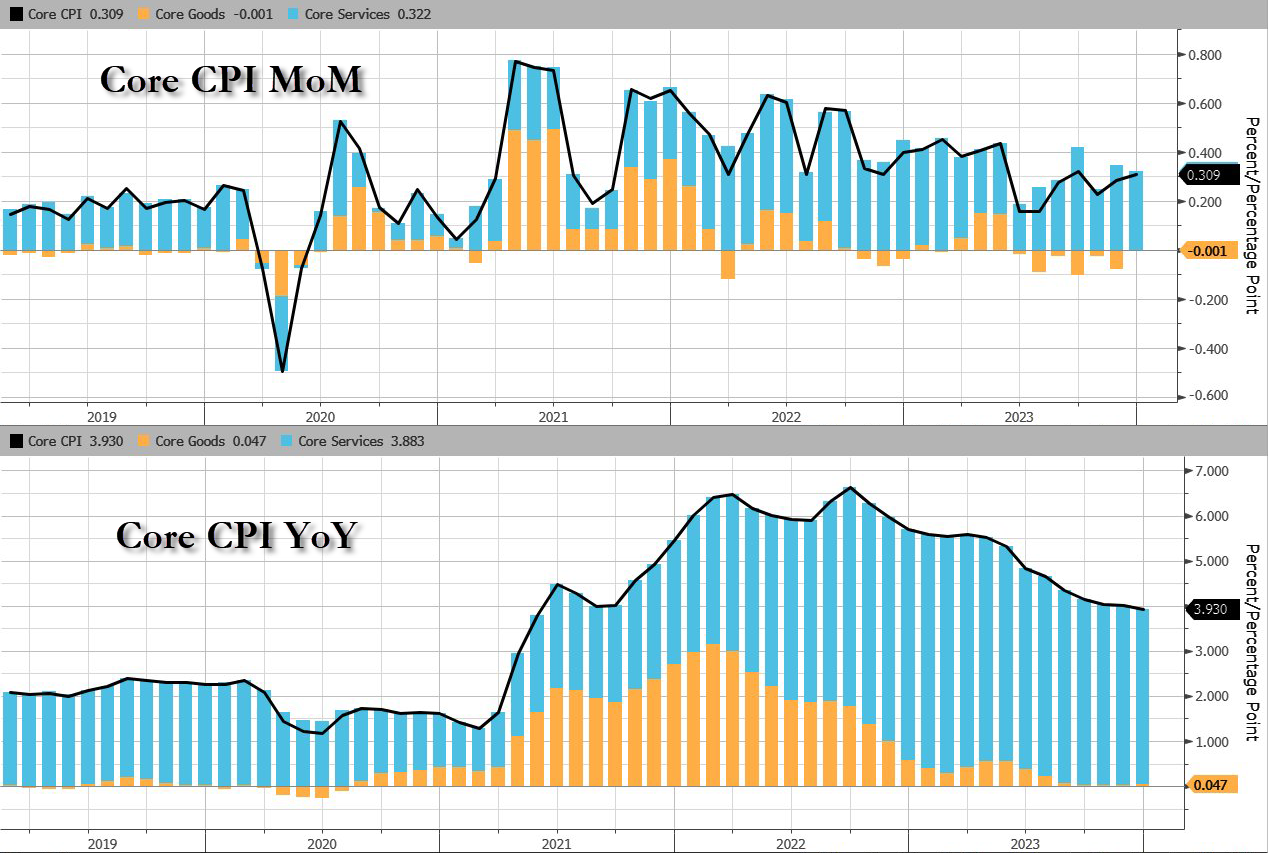

On the brighter side, core CPI according to the BLS rose 0.3% MoM as expected, dropping the YoY change below 4.00% for the first time since May 2021…

Source: Bloomberg

Goods deflation has stalled as the used cars and trucks index rose 0.5 percent over the month, after rising 1.6 percent in November.

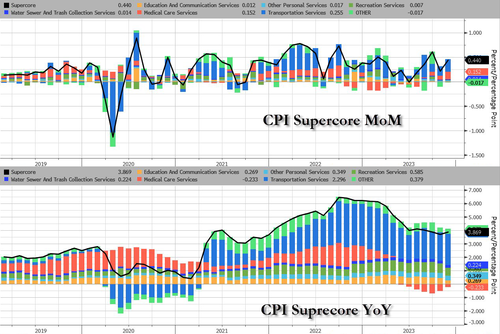

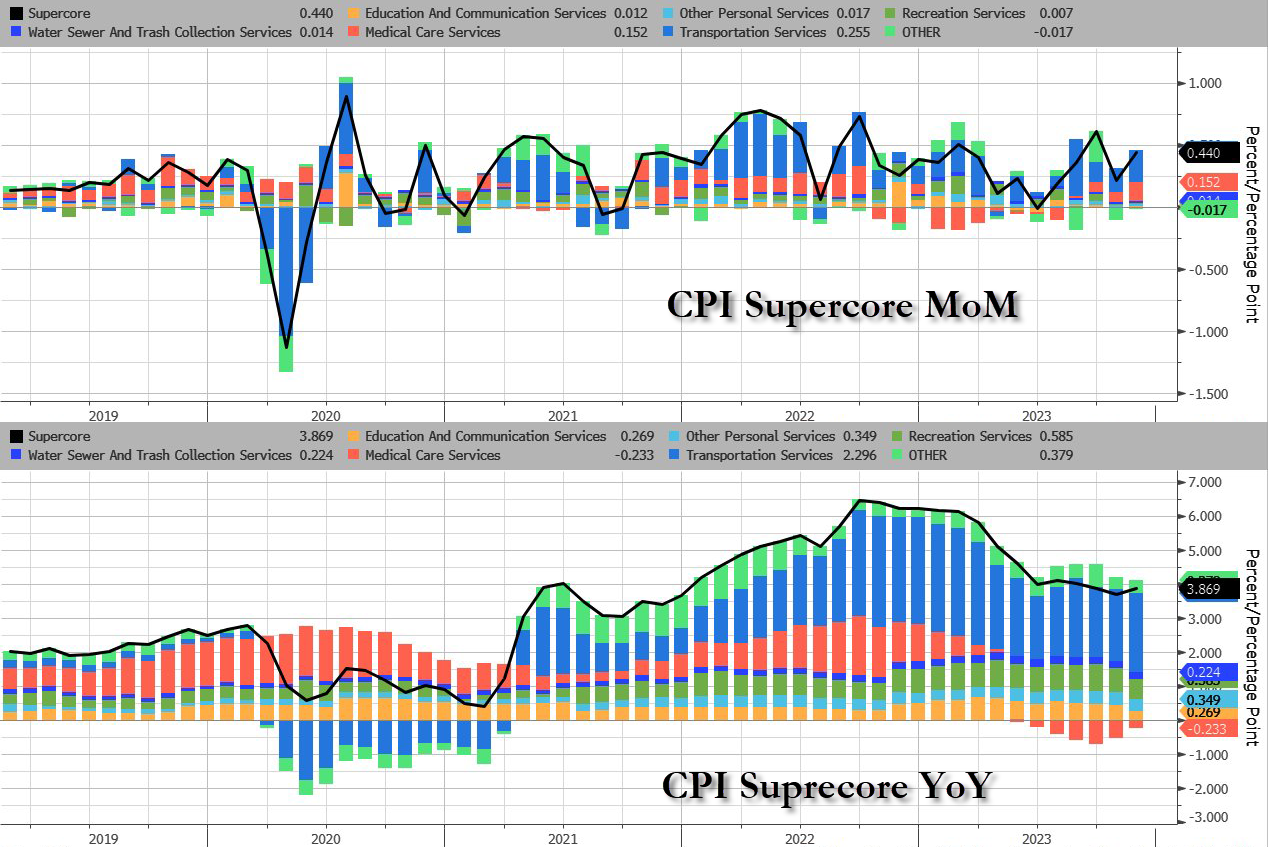

More problematically for The Fed (and the rate-cut ‘hypers’), is the fact that Core CPI Services Ex-Shelter (SuperCore) rose 0.4% MoM, upticking the YoY rise to +4.09%…

Source: Bloomberg

This is a category that Fed Chair Jerome Powell and other policymakers have highlighted as a focus.

All the subsectors of SuperCore rose MoM with the shelter index increased 6.2 percent over the last year, accounting for over two thirds of the total increase in the all items less food and energy index.

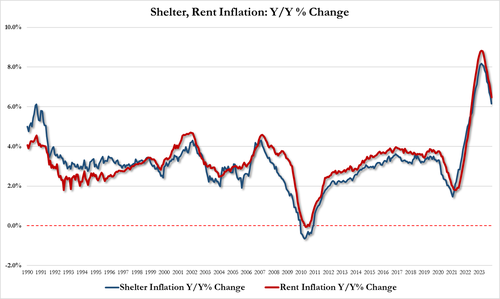

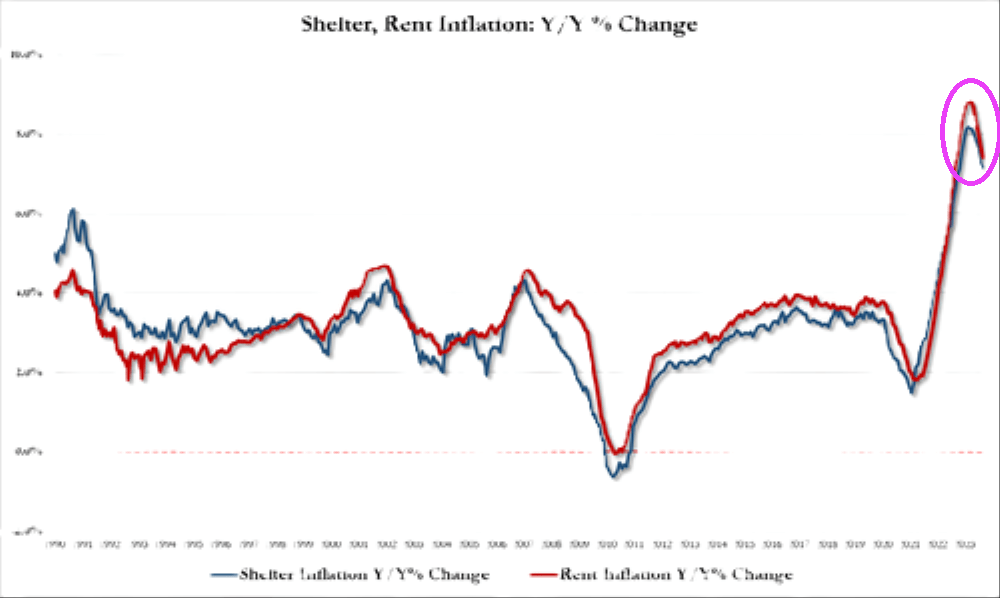

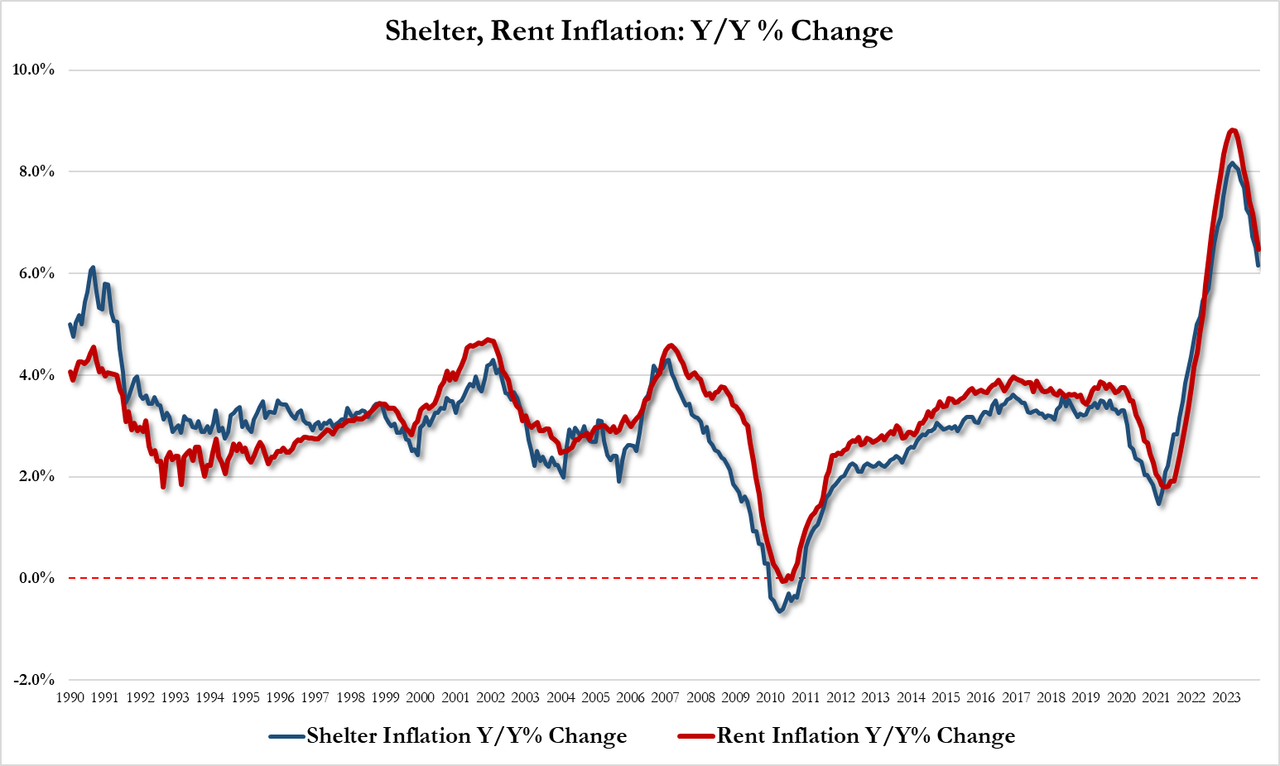

But shelter inflation is slowing (slowly):

Shelter inflation was up 6.15% YoY in Dec, down from 6.51% in Nov and the lowest since July 2022

Rent inflation was up 6.47% YoY in Dec, down from 6.87% in Nov and the lowest since July 2022

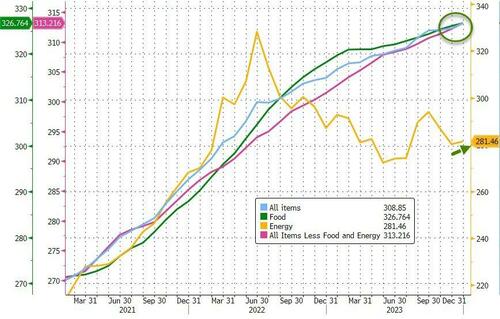

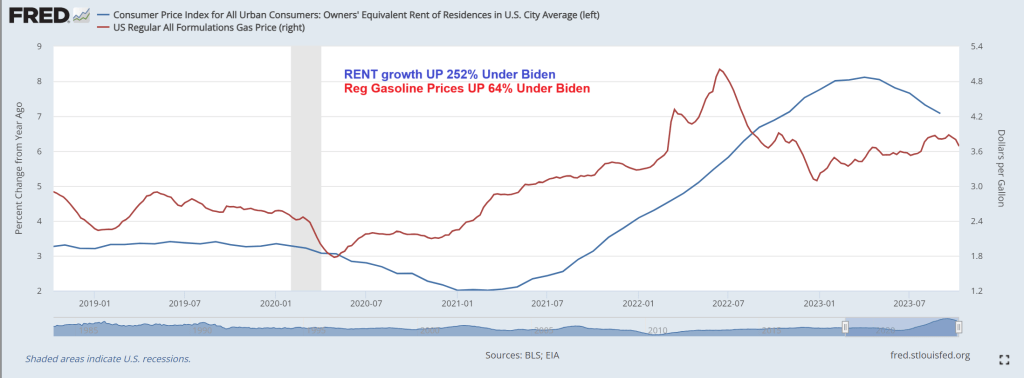

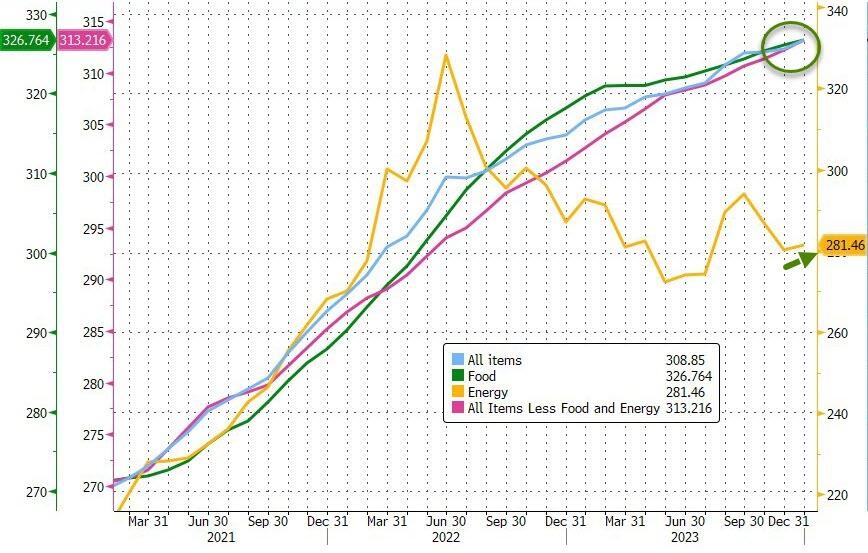

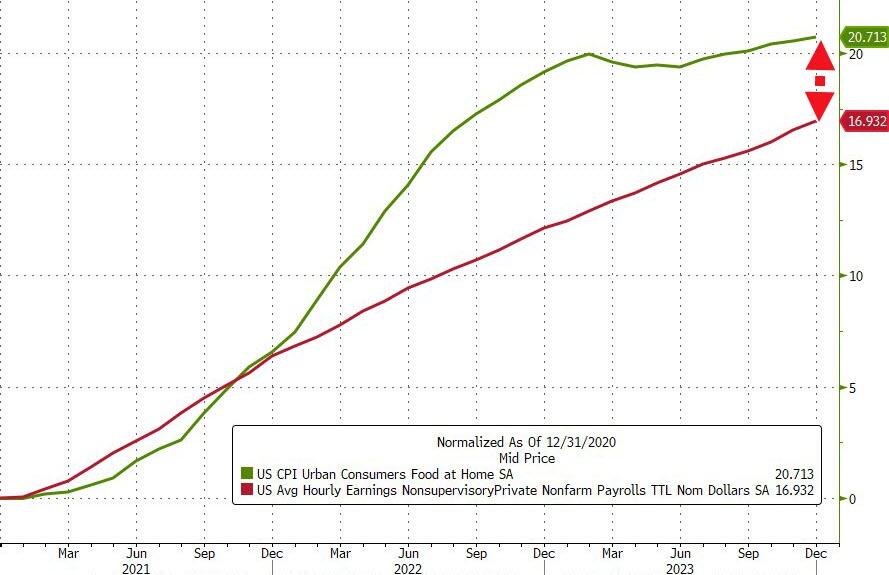

And the next time someone from the Biden administration says ‘inflation is down’ in an attempt to gaslight the public into believing ‘prices are down’ – show them this chart…

Headline costs at record highs

Core costs are record highs

Food costs at record highs

Fuel costs on the rise again

Source: Bloomberg

Four of the six major grocery store food group indexes increased over the month.

The index for meats, poultry, fish, and eggs rose 0.5 percent in December, led by an 8.9-percent increase in the index for eggs.

The index for food away from home rose 5.2 percent over the last year.

The index for limited service meals rose 5.9 percent over the last 12 months, and the index for full service meals rose 4.5 percent over the same period.

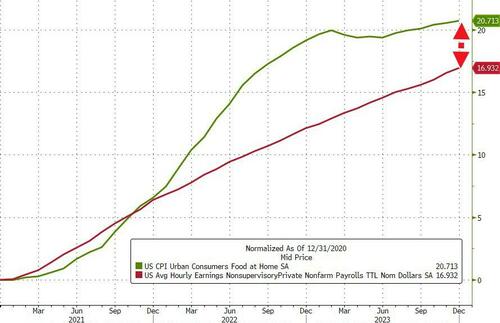

The White House was quick to note that real hourly earnings was positive in December (+0.8% YoY) but that number is the aggregate of ALL American workers.

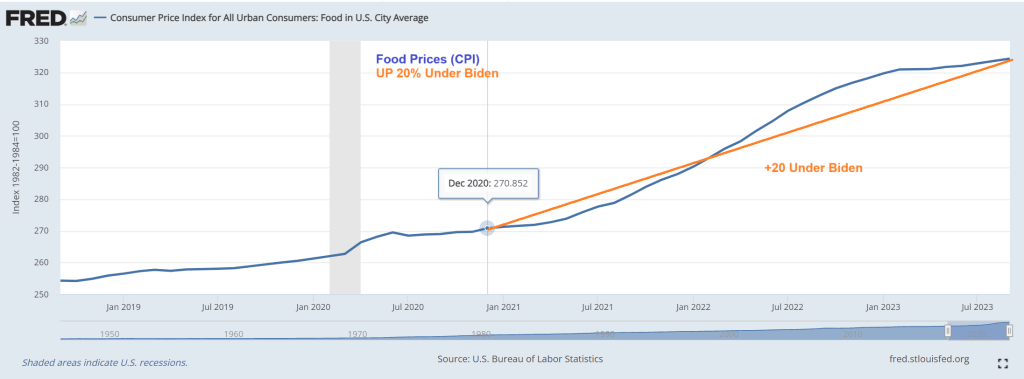

If we drill down to the ‘average joe’ – production and non-supervisory jobs – their wages are up 17% since Biden was elected… The only problem is, the cost of food since then has surged almost 21%…

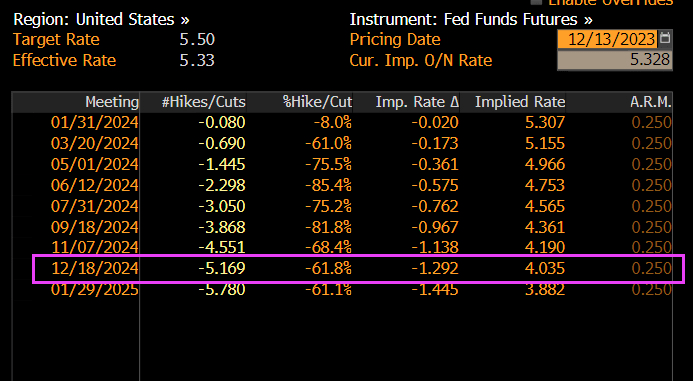

Is this a pause before the re-plunge? M2 thinks so…

So what happens next?

Not so much Goldilocks perfection.

Powell is in a real pickle now – does the Fed begin shrinking QT in March (which it has to if it is terminating BTFP and Reverse Repo is drained) without starting rate cuts.

Like the spaghetti western “The Good, The Bad And The Ugly,” Bidenomics has had similar effects on financing. Some good, some bad and a lot of uglies.

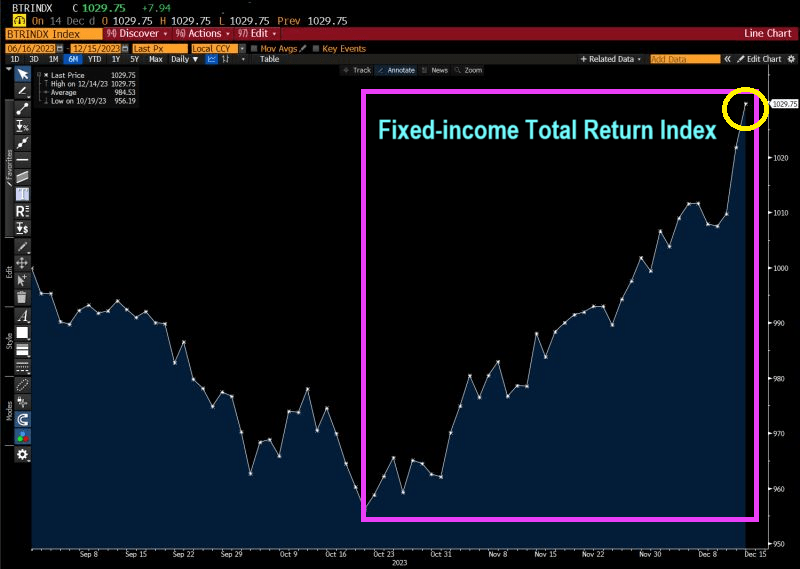

The good! For investors like pension funds the own US Treasuries, inflation has led The Federal Reserve to raise interest rates. This is good for investors holding short-term debt. The Bianco Fixed Income Total Return Index is soaring!!

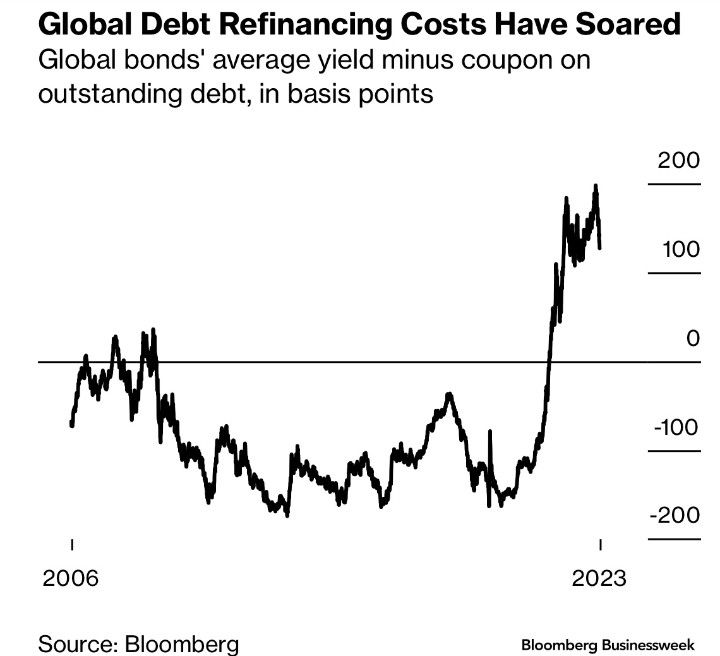

The Bad: Well, the flip-side of the same coin is that debt refinancing costs have soared.

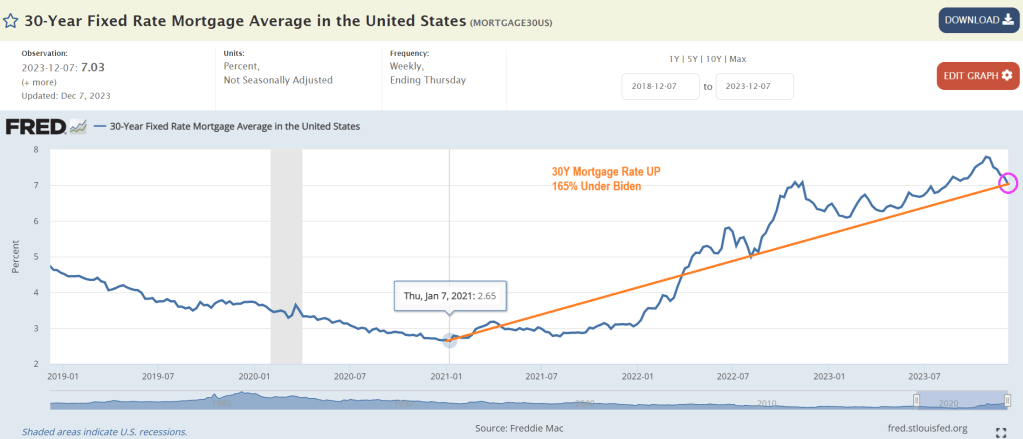

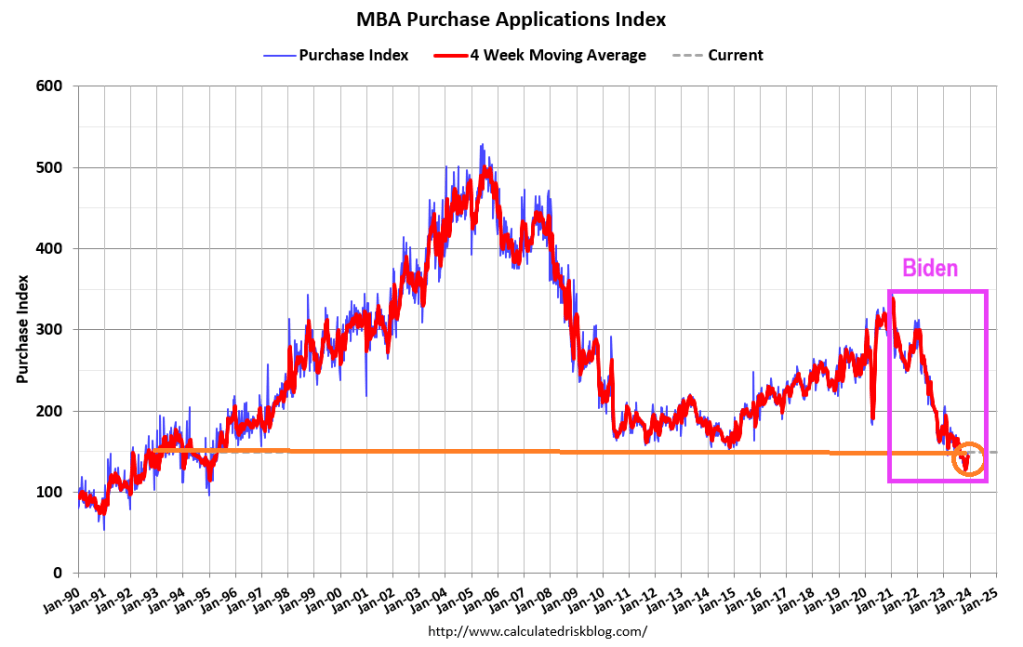

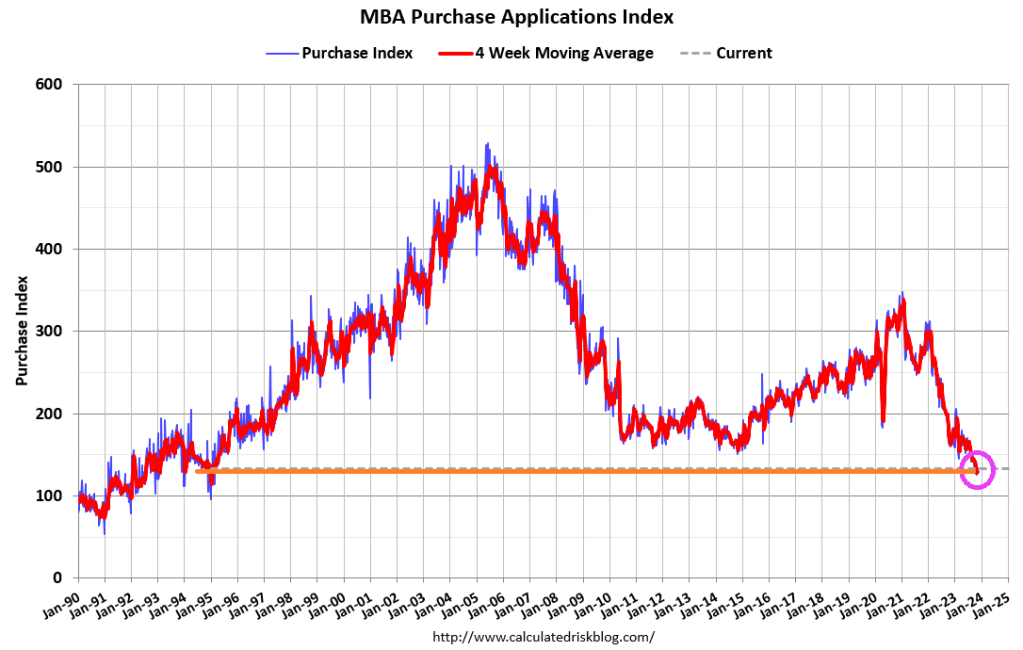

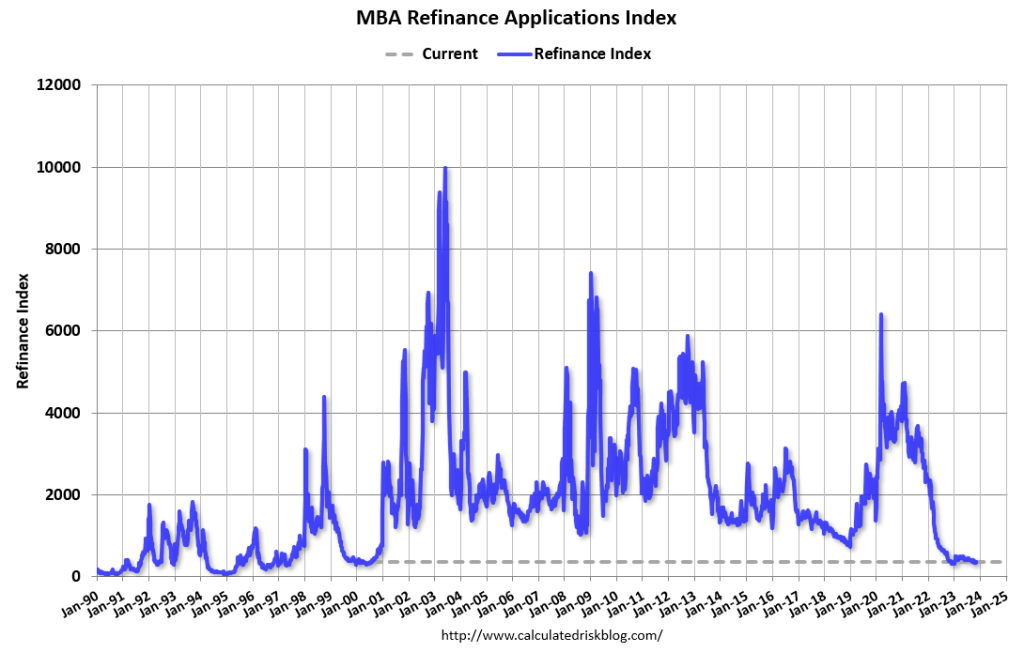

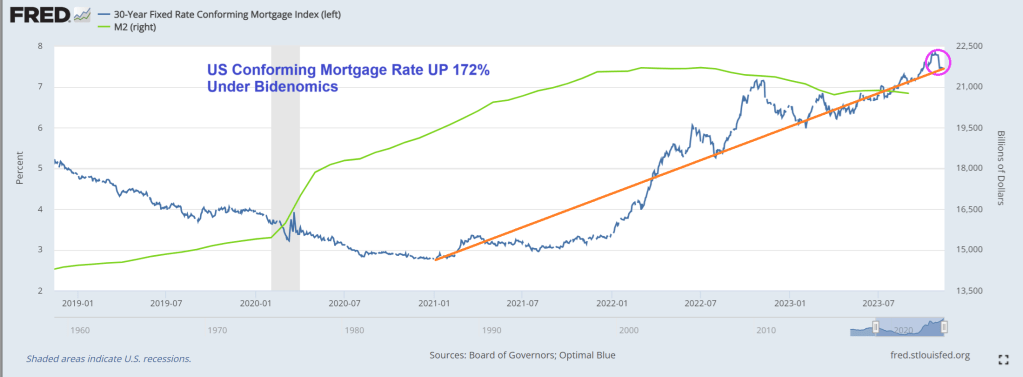

The Ugly. There are many contenders for losers under Bidenomics and current Fed (garbled) policies. But I choose … mortgage demand collapse with rising home prices and rising mortgage rates. Mortgage rates are up 165% under Biden.

And mortgage demand (applications) have been crushed.

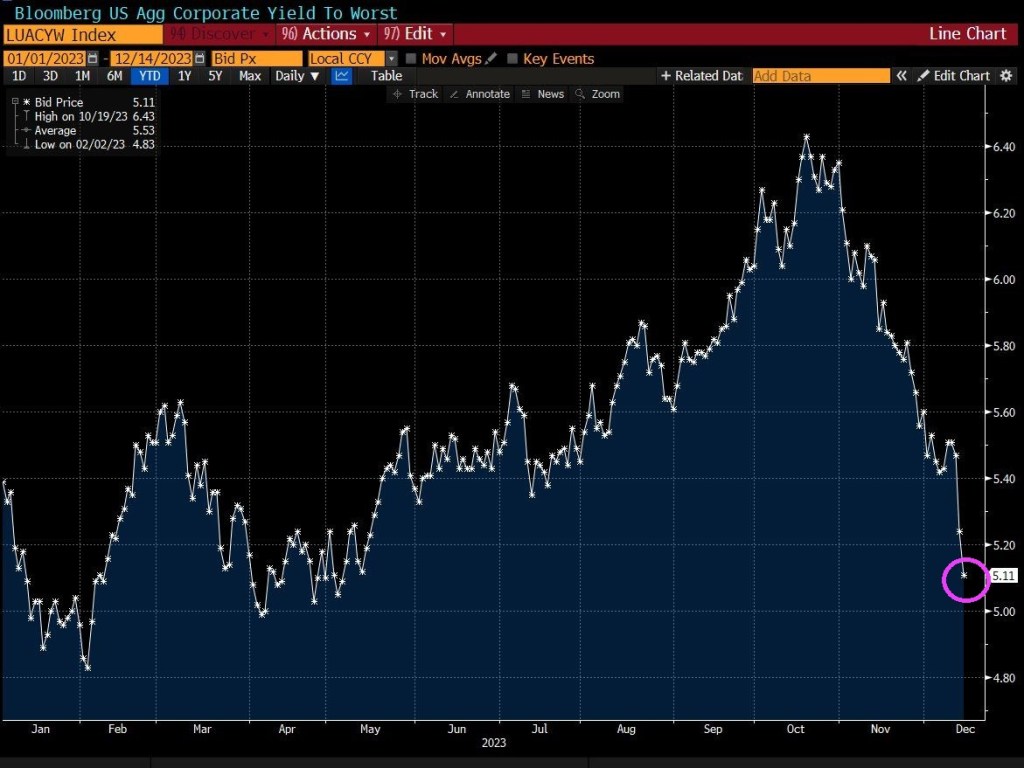

Also on the ugly side, global aggregate corporate yields have collapsed.

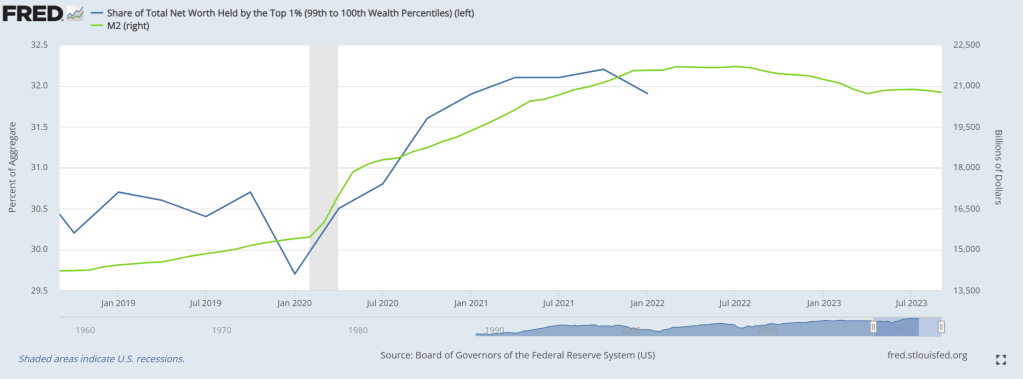

So, there have been winners with Bidenomics (the top 1%), and lots of losers.

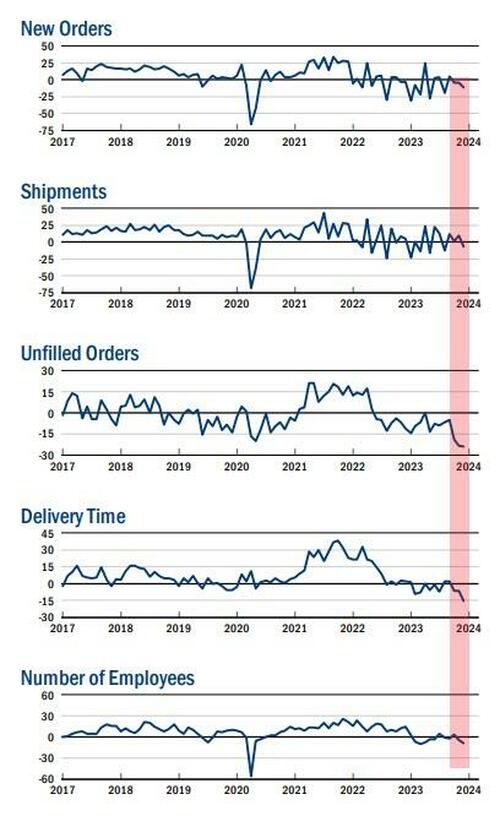

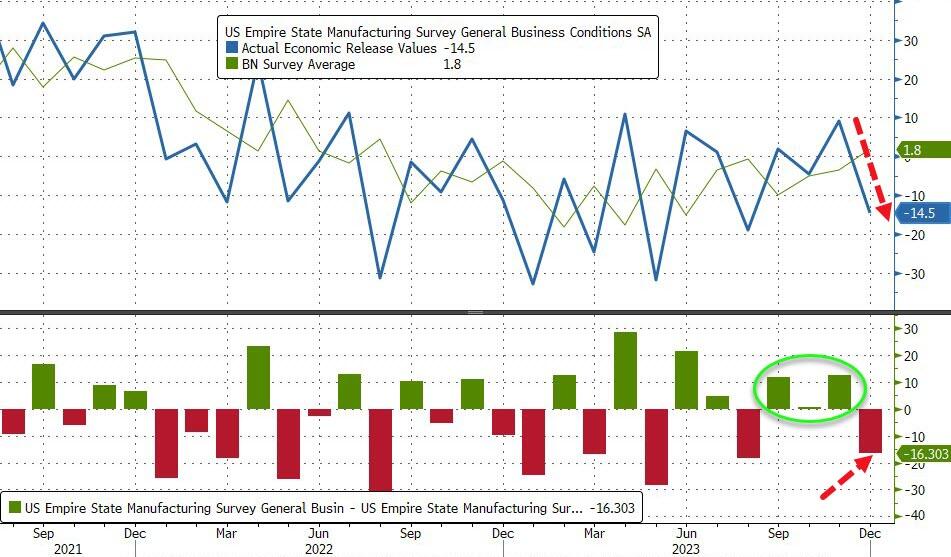

The drop takes the measure from ‘expansion’ at 7-month-highs to ‘contraction’ at 4-month-lows…

Source: Bloomberg

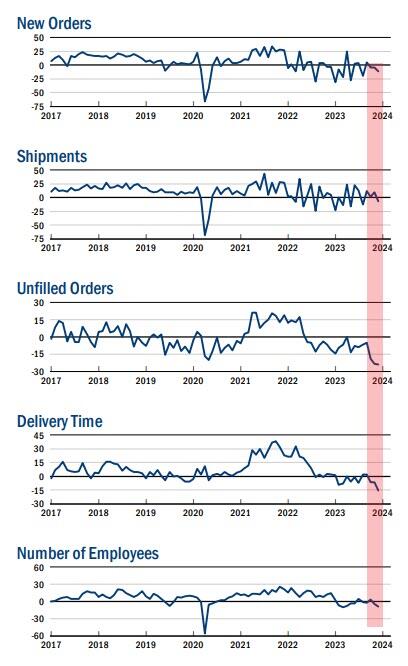

The new orders fell six points to -11.3, pointing to a decline in orders for a third consecutive month, and the shipments index fell sixteen points to -6.4, indicating that shipments fell.

The unfilled orders index held steady at -24.0, a sign that unfilled orders continued to fall significantly.

After rising into positive territory last month, the inventories index retreated fourteen points to -5.2, suggesting that inventories moved lower.

The delivery times index dropped ten points to -15.6, its lowest reading in several years, a sign that delivery times shortened.

The index for number of employees fell four points to -8.4, its lowest level in several months, pointing to a modest decline in employment levels.

On the bright side, the prices paid index moved down six points to 16.7, suggesting an ongoing moderation in input price increases, while the prices received index held steady at 11.5, a sign that selling price increases remained modest.

Is this the start of ‘soft’ data’s reversion to ‘hard’ reality?

The Fed – with its six rate-cuts – better hope so.

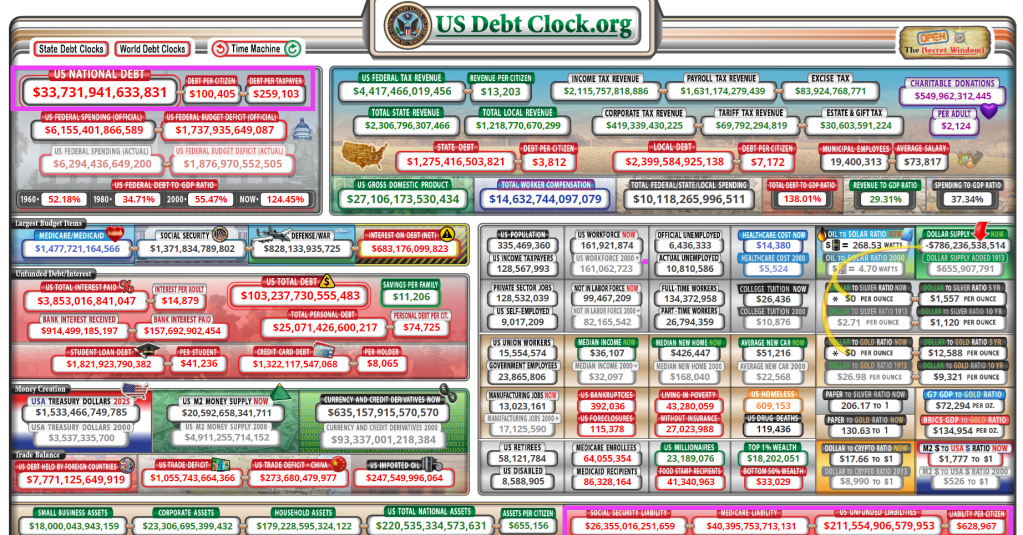

In fact, Congress and the Biden (mis) Administration are spending like the proverbial drunk sailors in port. US national debt is up to $33.7 TRILLION. That transates to $259,103 per taxpayer. With US debt to GDP of 138%!

Now, HERE IS THE REAL BAD NEWS! Unfunded promises that politicians made to Americans (Social Security, Medicare, Medicaid, etc.) now stands at $211.6 TRILLION. That equates to $629,000 per citizen. Maybe that should be the deal at the southern border: all immigrants must pay $629,000 for admission!

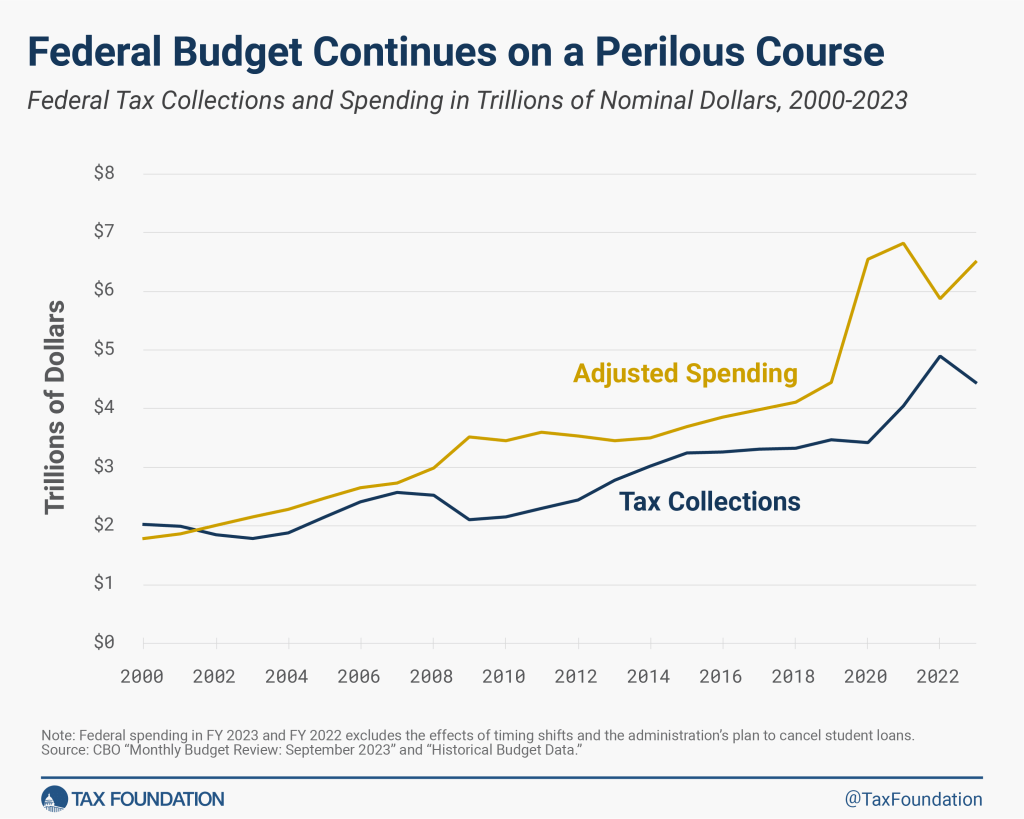

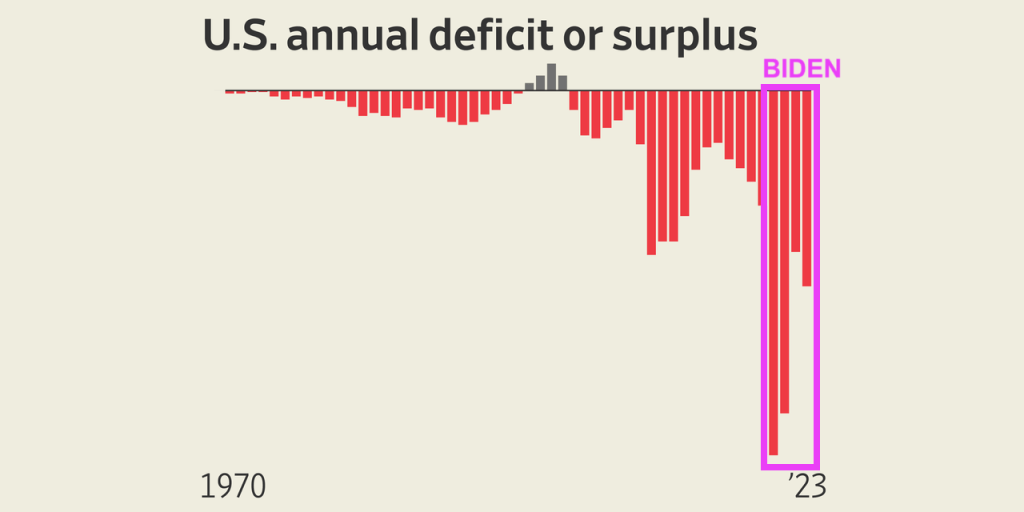

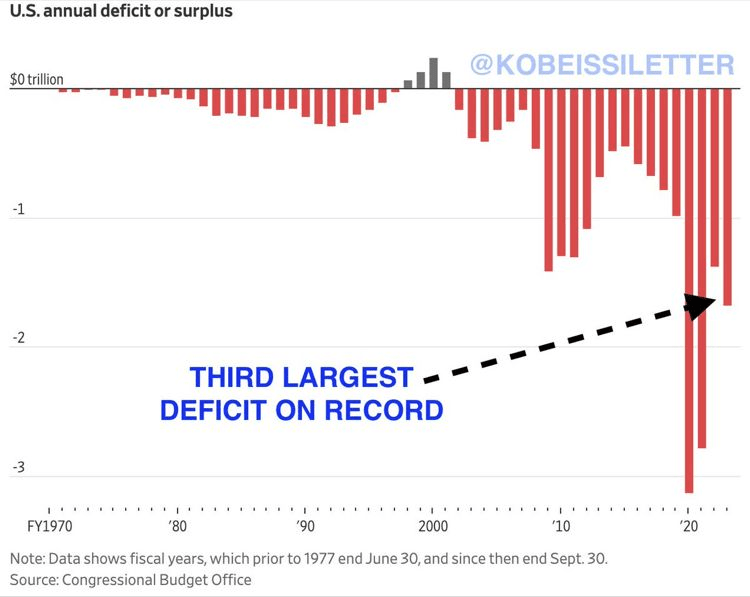

And the Federal budget deficit keeps on getting worse.

The budget deficits under Biden/Yellen have been the worst in history. So much for Biden whispering “Bidenomics is working!”

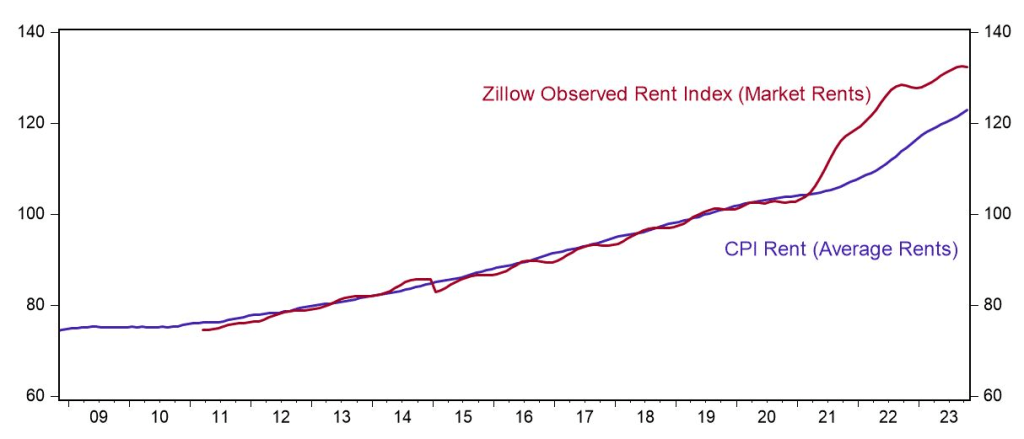

Rents in the US remain unaffordable to many.

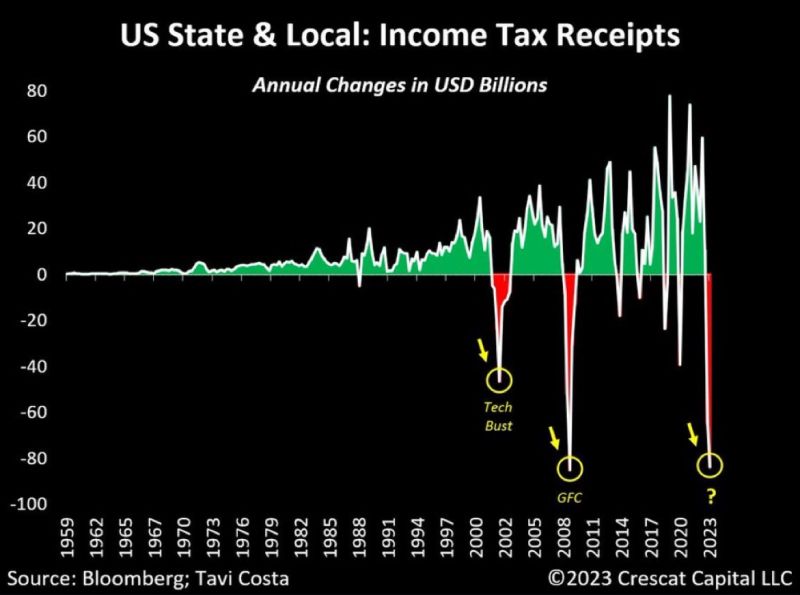

And Yellen, our nation’s financial consigliari, hasn’t said much about the dire decline in income tax receipts.

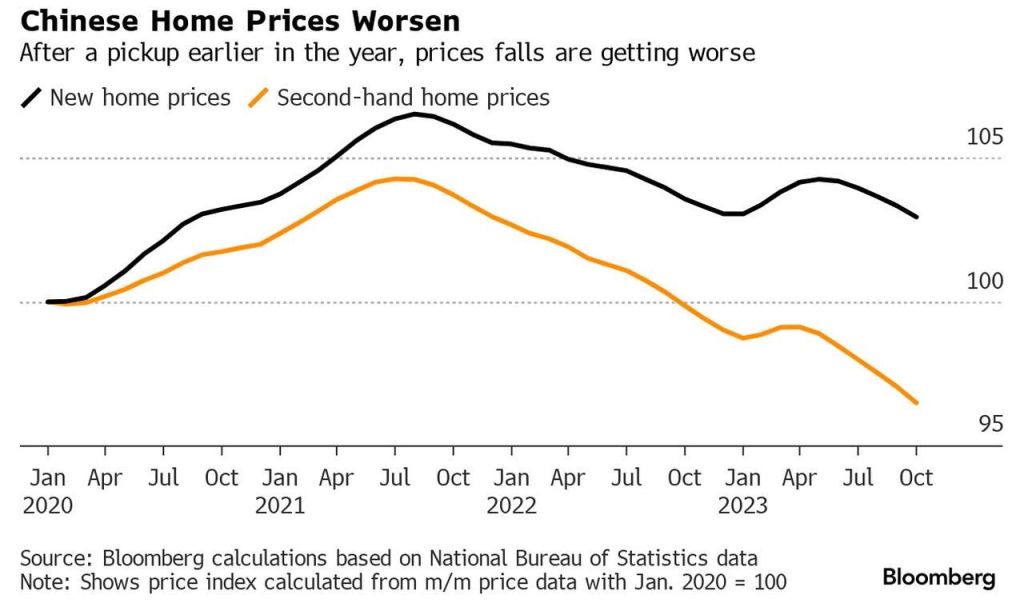

But Biden’s favorite country China, a classic top-down command economy like Biden and Yellen love,

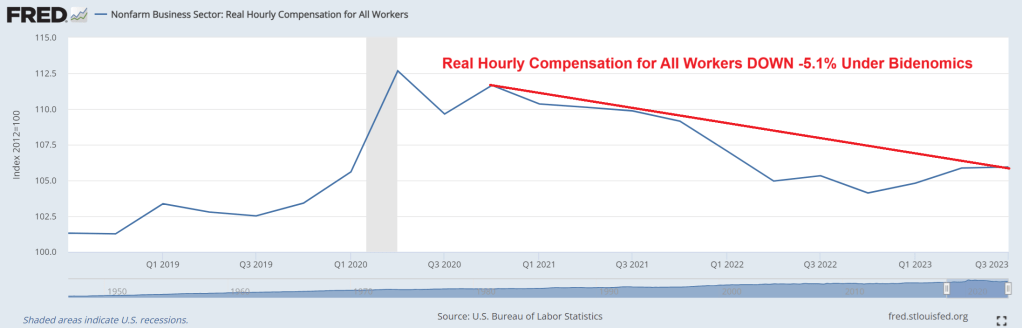

On Sunday, President Joe Biden tweeted, “Right now, real wages for the average American worker is higher than it was before the pandemic, with lower wage workers seeing the largest gains. That’s Bidenomics.” That’s right, Joe! Except real hourly compensation has DECLINED by -5.1% under Biden.

Biden says he wants 4 more years to finish the job. Like killing off the mortgage market completely, Joe?

Mortgage applications increased 2.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 10, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 2.8 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 0.4 percent compared with the previous week. The seasonally adjusted Purchase Index increased 3 percent from one week earlier. The unadjusted Purchase Index decreased 0.3 percent compared with the previous week and was12 percent lower than the same week one year ago.

The Refinance Index increased 2 percent from the previous week and was 7 percent higher than the same week one year ago.

Of course, mortgage rates have been declining slightly over the past few weeks, but remain up 172% under Biden.

At least the stock market is booming after the inflation report signalled that The Fed is likely done with rate hikes.

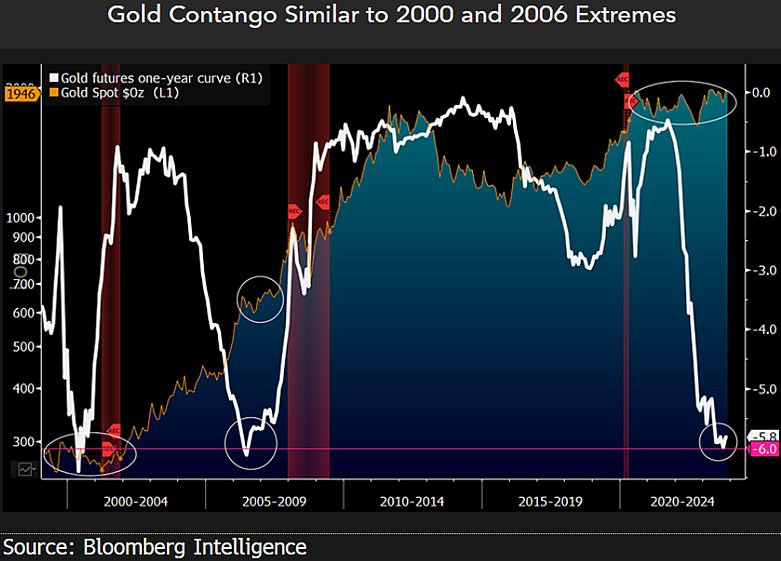

On the gold front, we are seeing evidence of contango.

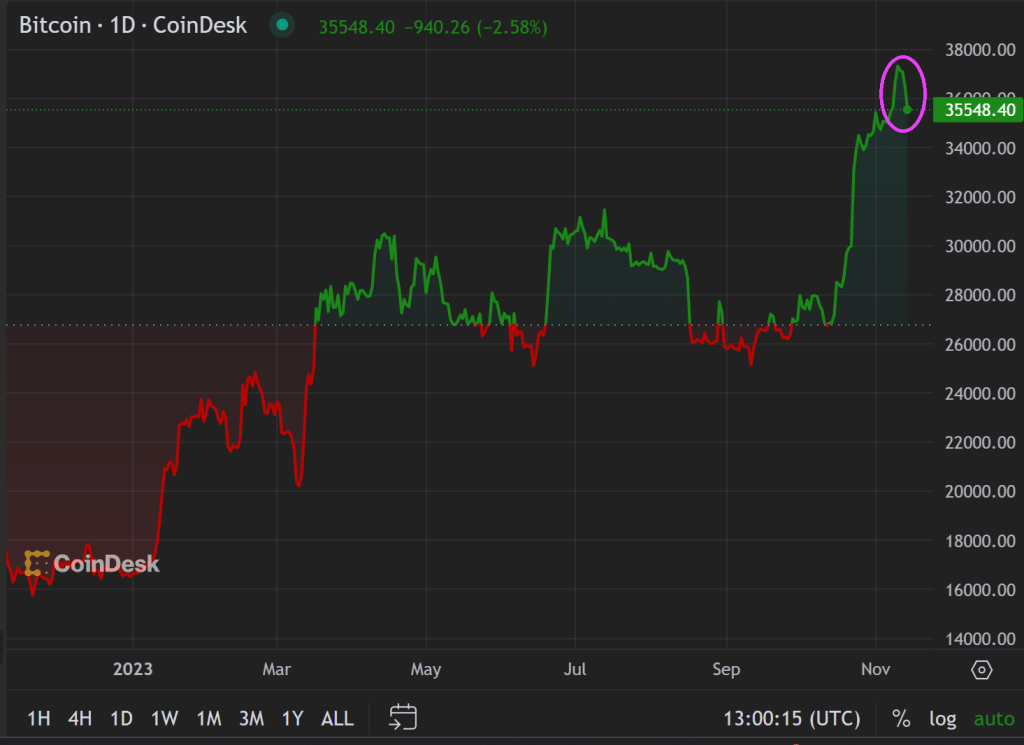

Bitcoin? Down a wee bit after a staggering rise in price over the past year.

Here is China’s Xi meeting with Biden’s likely replacement, “Greasy Gavin” Newsom and Newsom’s likely Treasury Secretary, Janet “Too Low For Too Long” Yellen. Newsom, Yellen and Xi all want havoc in America.

Republicans elected Mike Johnson from Louisiana as House Speaker, then were surprised when Johnson agreed with big spending Senators McConnell and Schumer on Biden’s mega spendathon. Also, several Republicans voted with Democrats NOT to impeach Cuba Pete (Mayorkas) for allowing 8 million illegals to cross the southern border. Bottom line: the Biden Administration and Congress are closely held subsidiaries of the elite 1% and US large corporations. The middle class be damned! But we will get fooled again in every election.

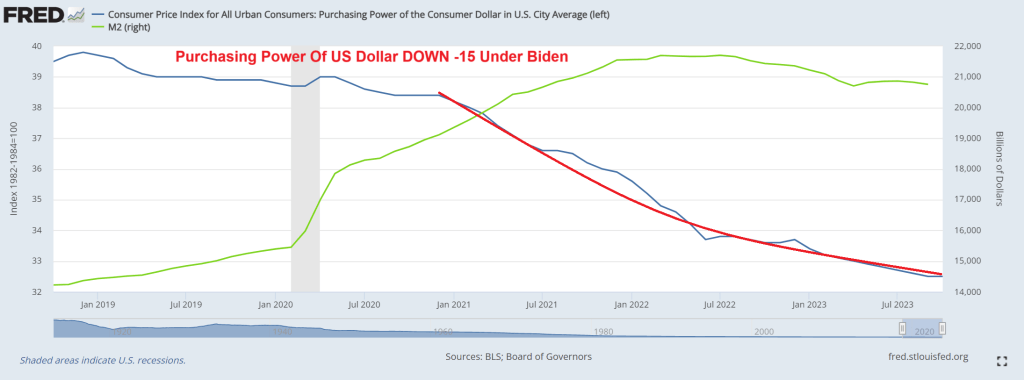

Since Biden’s inaugration in January 2021, the purchasing power of the US dollar is down a staggering -15%.

Yes, under control of large corporations and the 1%, the economy is an economic wasteland. But the 1% are doing great under Bidenomics! With The Fed’s help of course.

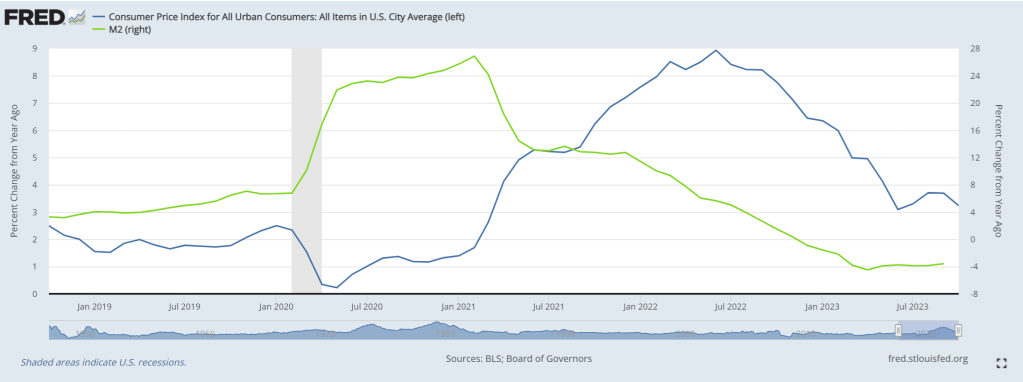

Here is a chart of core inflation relative to M2 Money printing. Easy way to cool inflation … stop printing money!

Here is China’s Xi and America’s “China Joe” Biden.

Seriously, Biden has always been known as being stupid and corrupt. Now he has dementia. A PERFECT President for the 1% in their war against the middle class. Biden is the penultimate “useful idiot” with an emphasis on idiot.

First, food prices are up 20% since December 2020. Talk about destruction of middle class wealth!

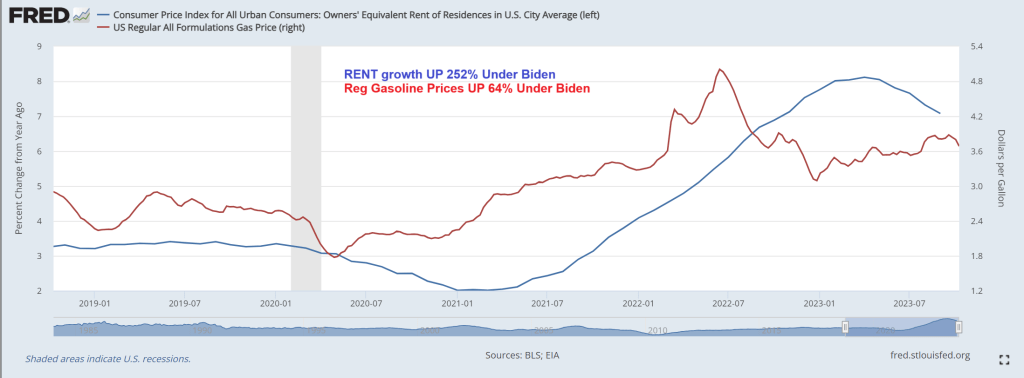

That is in addition to gasoline prices are up 64% under Biden while rent growth is up 252%. Well, Biden waived through millions of illegal immigrants and rent had to rise. Biden and Washington DC’s broken borders is Livin’ La Vida Loco.

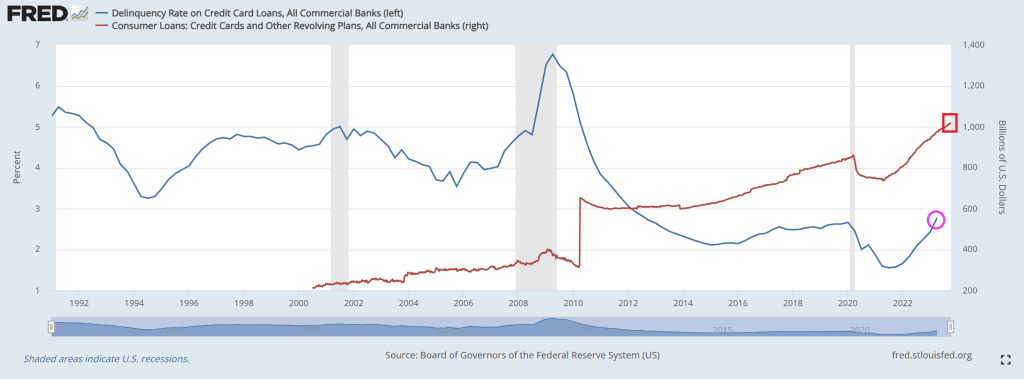

To cope with inflation (that Paul Krugman claims is over but the last inflation report showed that the tinders of inflation are hard to extinguish), consumers have turned to credit cards to survive. In fact, credit cards have expanded 38% since April 2021 despite rapidly rising interest rates. And credit card delinquency rates are rising and are now above Covid-era economic shutdown levels.

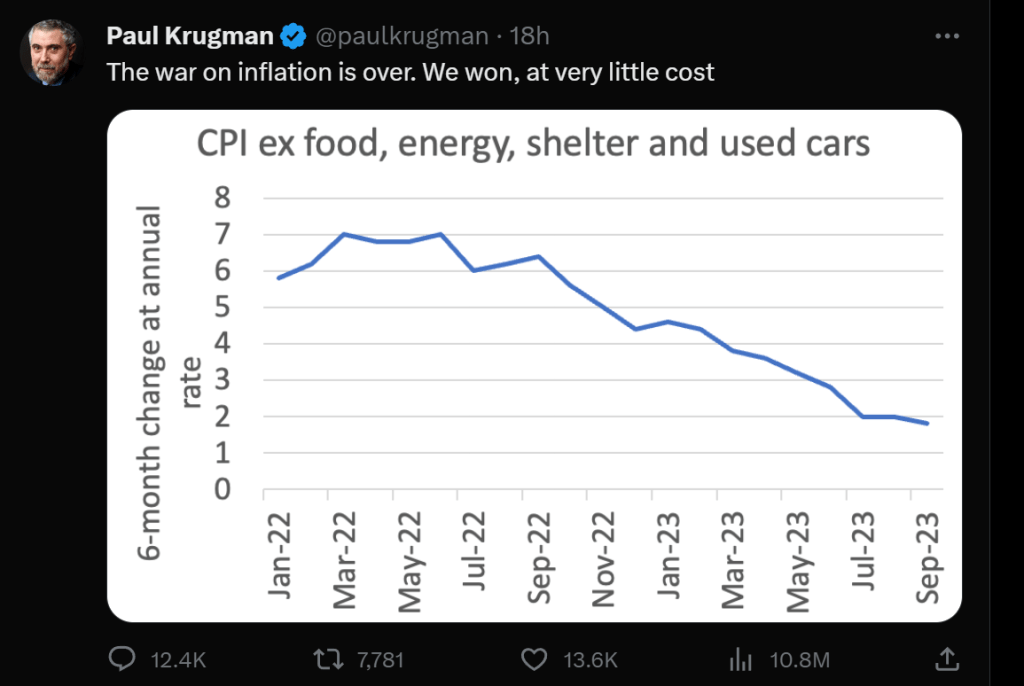

Paul Krugman, Nobel Laureate in economics and media celebrity, made a terrible claim yesterday when he pronounced that “The war on inflation is over. We won, at very little cost.” Krugman’s proclamation was trumpeted by The View’s Joy Behar Joy who claimed that everything is going great in the country! The economy is “booming” and people are having an “easier time” putting bread on the table. Huh? Easier than a month ago maybe, but not easier since 2021 under Bidenomics.

Hmm. Suppose that during World War II the Germans had stopped after they invaded and captured Paris on June 14, 1940. The war could have been over, but France was lost to Germany amidst thousands of dead and loss of property. That is not a victory, but a crushing defeat.

Just like my Paris example, Krugman’s claim the war on inflation is over and we won AT VERY LITTLE COST was grossly misleading and a big kerplunk (thud). Why? For one, the average American family is $7,400 POOR than in January 2021 when Biden became President. So, it looks like we know the cost of inflation and it was steep, not “very little cost.” Well, very little cost to elitist millionaires like Krugman.

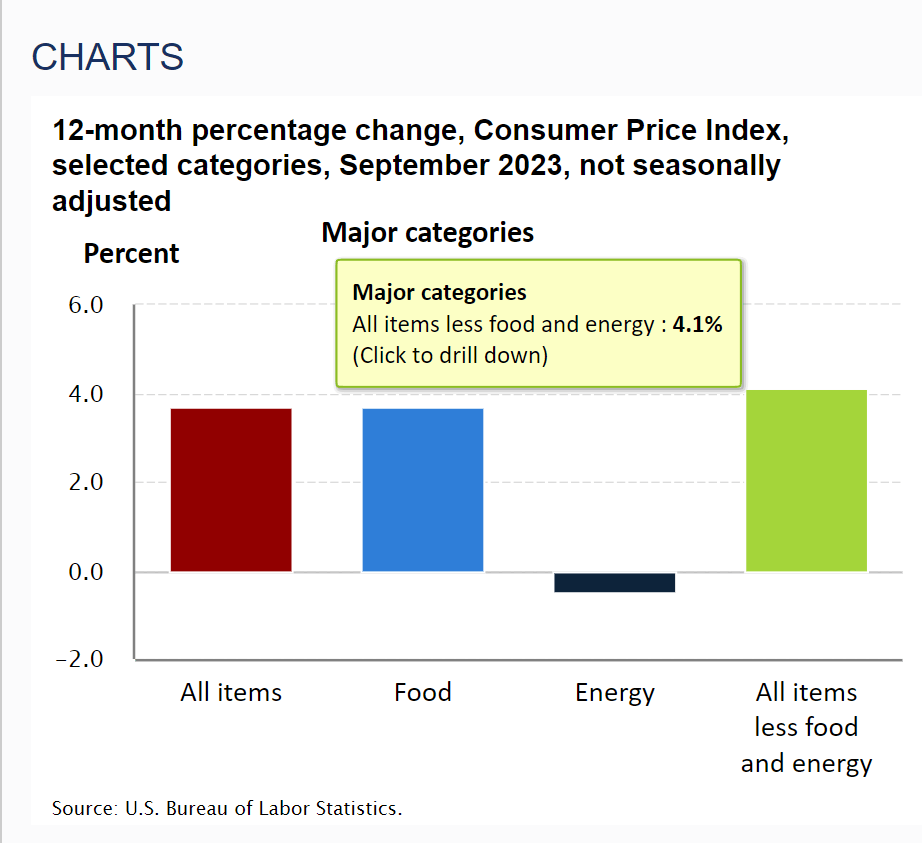

Krugman loves the recent inflation report from the BLS. Specifically, the 12-month change in the Consumer Price Index Less Food And Energy for September was 4.1%. Krugman focuses on the recent 6-month change being less than 2%. In Krugman’s mind, this is victory … core inflation has been tamed and inflation is at The Fed’s target rate of 2%.

But before Krugman pops the champagne cap on the 1959 Dom Perignon for $42,350 (while the rest of us are drinking E&J Gallo’s Thunderbird), bear in mind that he is referring to the RATE OF GROWTH in prices, not the highly elevated levels of prices. Victory against inflation would be if prices returned to December 2020 levels.

I pointed out yesterday that “real” wages contracted 0.1% YoY (after 3 months positive) in September. It is important to note that real wage growth was negative from 2021 until 3 months ago, but has gone negative yet again. Victory??

Krugman prefers core inflation, removing food, housing and energy. You know, the three things most Americans actually care about. Take shelter (or rent of residence) where rent is growing at a sizzling 7.1% YoY.

Under Biden and Congress’ reckless spending splurges (and inane Federal energy policies), regular gasoline prices are up 64%. Growth in rent of residence has grown 252%! So, Professor Krugman, Americans are far worse off than before Biden was President.

If prices return to December 2020 (or pre-Covid levels), I will declare a victory. But for right now, symbollically, the German army is occupying France and Paris with horrible suffering for the French people. In other words, Americans are still far worse off under Biden even though inflation is finally slowing.ew

Speaking of France and World War II, maybe we should consider Joe Biden as today’s Pierre Laval, leader of Vichy France since Biden seems more concerned with pleasing Klaus Schwab and The World Economic Forum than America’s middle class and low wage worker (like Laval was concerned with that German leader Adolf Hitler thought).

Former Fed Chair Janet Yellen, notorious for leaving rates too low for too long (TLTL) and then suddely raising them after Donald Trump was elected President, wants rates lower again for much longer. Make rates great again (MRGA?).

YELLEN SAYS DEBT SERVICE COSTS WILL BE 1% OF GDP FOR THE NEXT DECADE. – Reuters

Her statement implies that the economy will be strong and the government will run budget surpluses, or interest rates will be near zero for the next ten years.

Instead of guessing what she is pondering, we do some math and arrive at the only possible answer.

The Government Can’t Afford Today’s Interest Rates

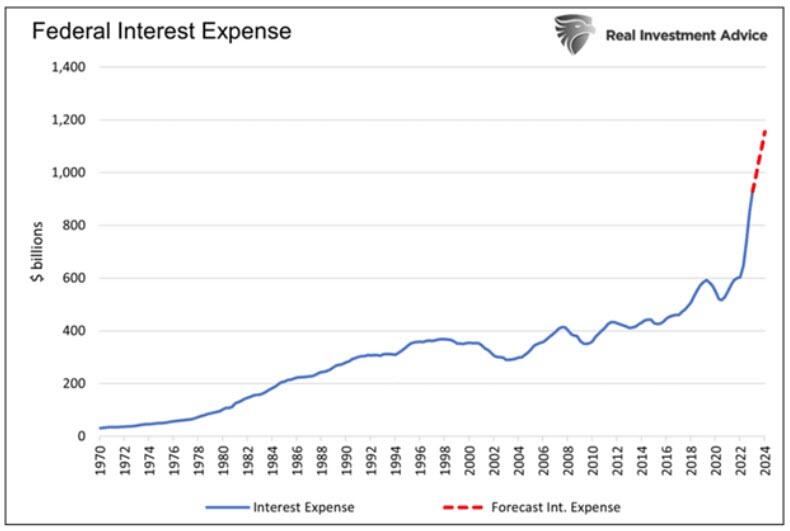

Before walking through various scenarios to figure out what Yellen may be implying, it’s helpful to provide background on what drives her mindset. In our article The Government Can’t Afford Higher For Longer, Much Longer, we shared the following graph and commentary:

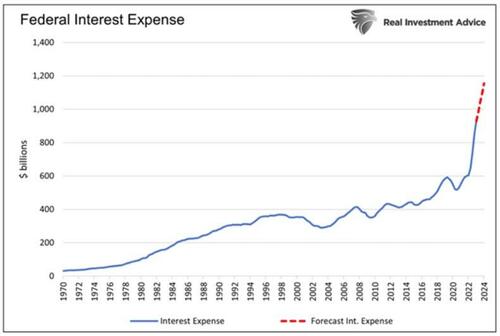

Total federal interest expenses should rise by approximately $226 billion over the next twelve months to over $1.15 trillion. For context, from the second quarter of 2010 to the end of 2021, when interest rates were near zero, the interest expense rose by $240 billion in aggregate. More stunningly, the interest expense has increased more in the last three years than in the fifty years prior.

The graph above is just the tip of the fiscal iceberg. Every month, lower-interest-rate debt matures and will be replaced with higher-cost debt.

Higher interest rates are an additional funding burden for the federal government. Janet Yellen surely understands the damaging situation and grasps that higher interest rates are not feasible given current debt levels.

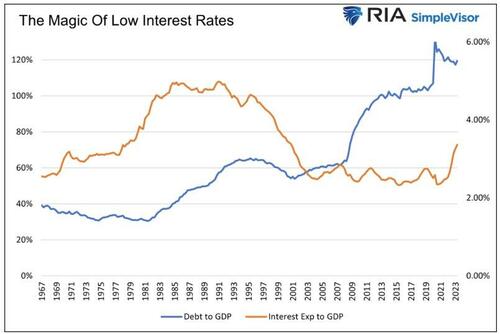

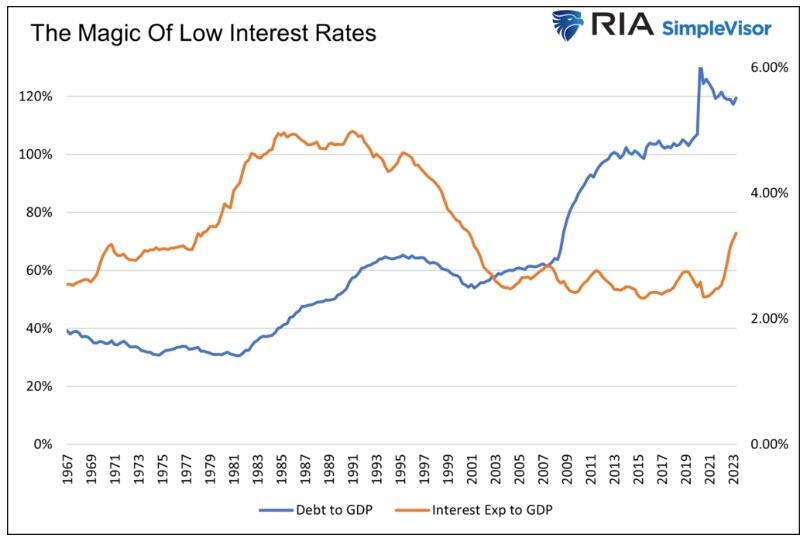

Low-Interest Rates Make Debt Manageable

The government’s debt-to-GDP ratio has climbed three-fold since 1966. Yet, until very recently, the ratio of the federal interest expense to GDP was at its lowest level since 1966.

While the amount of debt rose sharply, its cost was offset by rapidly falling interest rates. As a result, higher debt levels were very manageable.

If $1 trillion of debt with a 4% coupon matures, and the Treasury replaces it with $2 trillion at a 2% coupon, the interest expense doesn’t change despite doubling the debt. While a simplified example, that is essentially what has occurred for the last 30 years.

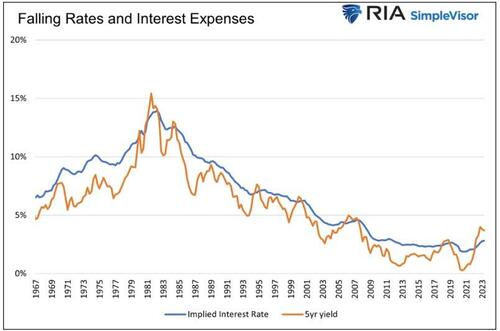

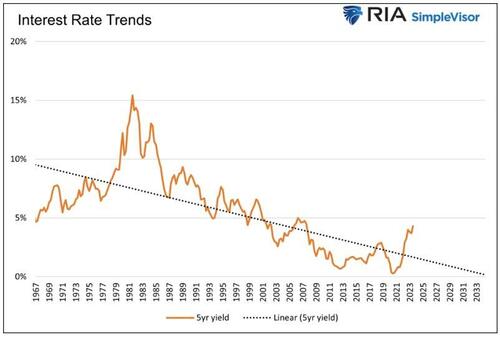

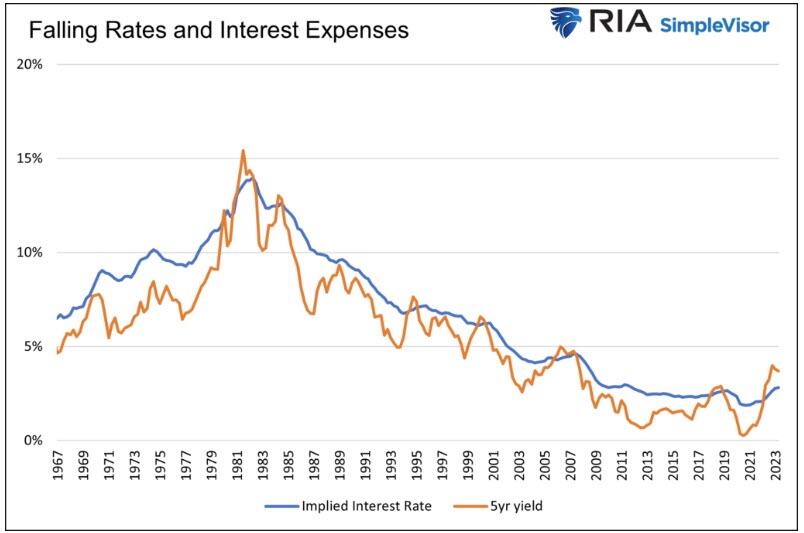

The following graph compares the 5-year U.S. Treasury note and the implied cost of funding the government’s debt.

In time, as lower interest rate debt is replaced with higher interest rate debt, the benefits of lower rates work in reverse.

“Debt Service Costs At 1%” – Is It Possible?

We return to Janet Yellen’s message and discuss why she is likely correct.

Balanced Budgets and Unicorns

In the five years leading up to the pandemic, nominal GDP grew at 5.03% annually. Let’s optimistically assume growth continues at 5% consistently for the next ten years. Now, let’s tack on an even bolder presumption: the government balances its budget every year for the next ten years. Thus, the amount of outstanding debt will remain constant. For context, in the last 57 years, there has only been one year in which the amount of debt has not increased.

In such a far-fetched scenario, the debt-to-GDP ratio would drop considerably to 70%. However, interest costs would equal 2% of GDP. Such is much better than the current 3.36% but double Janet Yellen’s 1% objective.

Budget surpluses for the next ten years would lower interest expenses even more and possibly get the interest expense to GDP ratio to 1%. However, the odds of a unicorn spraying rainbows across the sky and the government running a surplus are the same: zero percent.

Consequently, we exclude surpluses as a viable way to reduce the interest expense to a more manageable level.

Budget Deficits And The Magic Of Low-Interest Rates

Balanced budgets or surpluses are unrealistic, given the political and fiscal trends. Further, the economy relies heavily on government spending. While fiscal prudence would be good in the long run, the short-run effect would be a recession.

Instead of using pipe dreams as scenarios, let’s get realistic. The more likely, albeit still optimistic, scenario involves the debt and GDP growing at the same rate. Let’s also assume interest rates remain at current levels. In this exercise, we assume an average borrowing cost of 4.75%, which is a little below the current weighted average funding cost for the government. Under this “realistic” picture, interest expense would climb to 5.6% of GDP.

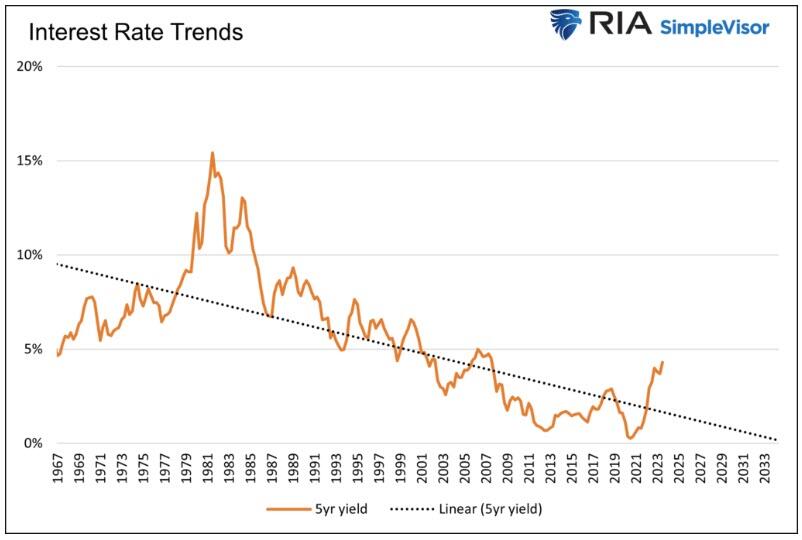

The only logical variable in the equation that can make Janet Yellen correct is the future interest rate.

To arrive at Yellen’s 1% figure, assuming debt grows at the rate of GDP, interest rates must be much lower.

In time, a weighted average interest rate of 0.85% would put the nation’s interest expense at 1% of GDP.

When Janet Yellen tells us the debt cost to GDP ratio will be 1% over the next ten years, she is really saying interest rates will be below 1% for the next ten years.

Therefore, Janet Yellen must believe that the recent spike in inflation and yields is an anomaly. If the pre-pandemic economic and interest rate trends resume, she will be correct.

Summary

Part of Janet Yellen’s job is to exude confidence to its investors. In this case, it means telling the public that the current jump in interest expenses will not last. While she would probably prefer to be straightforward and say interest rates will be much lower, she must also be sympathetic to the Fed’s job of getting inflation down. Therefore, to walk the party line, she must speak in code, so to speak.

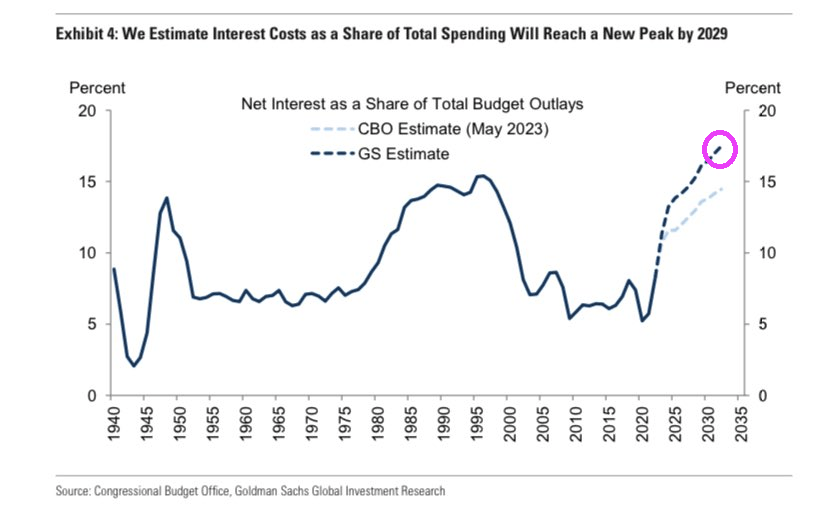

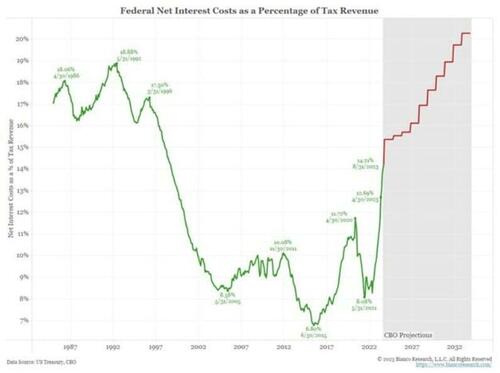

Whether you agree with Yellen’s projection or not, the following CBO graph projecting interest costs as a percentage of tax revenues, courtesy of Bianco Research, highlights that the government has no choice but lower for longer interest rates. The current level of interest rates will bankrupt the nation.

This makes sense. Two global elitists who look down with disdain and want to reprogram MAGA voters. Can we reprogram the MRGA types into letting rates float to market.

Like President Biden enjoying a barbeque at The White House with a live band (probably NOT Justin Moore singing “Small Town USA”) while Hamas declared war on Israel and Americans are being held hostage with the promise of public executions of hostages livestreamed. Nothing that “Empathy Joe” does ever surprises me anymore, but I am surprise that various Federal Reserve Presidents will speak today while Hamas terrorizes Israeli and US citizens.

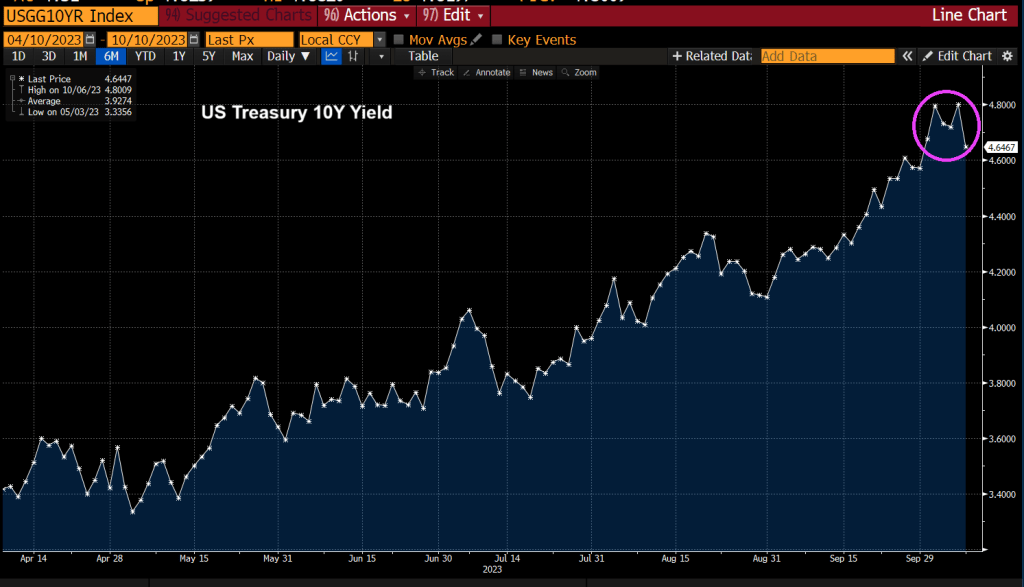

It could be that investors think that Talking Heads at The Fed will claim that Fed rate increases are over. Then again, the Iran/Hamas terror campaign against Israel is spookking markets, driving up oil and gold prices and driving up “flight to safety” in US Treasuries.

President Biden called on Americans in Israel to book a commercial flight home, even though Israel has cancelled all flights. Does Old Joe even read the news??

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.