The Hollies said it best: Stop, stop, stop. FIAT Money Printing that is.

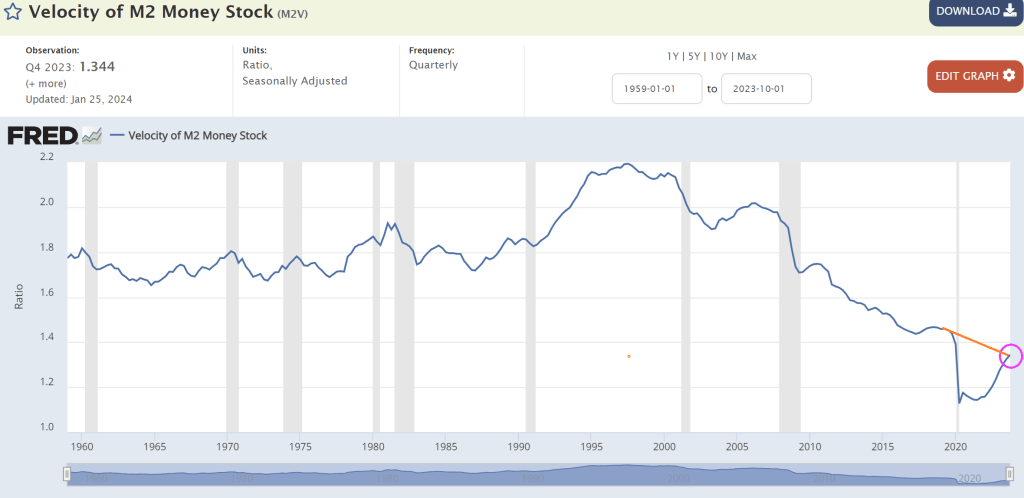

Typically, we look at M2 Money Velocity (GDP/M2) as a measure of how much the economy grows by expanding the money supply.

M2 Money Velocity is currently at 1.344, and still below where we were under Trump prior to Covid. After Powell printing palooza after Covid, M2 Money Velocity collapsed and is slowly rising, but remains low by historic standards.

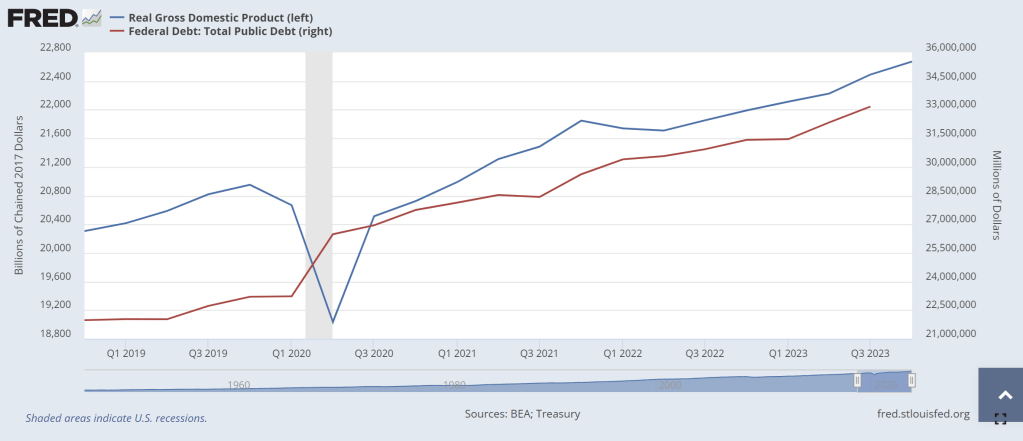

Perhaps a more interest velocity is DEBT velocity (GDP/DEBT). Under Biden’s Reign of Error, Federal debt has increased by $6,539,359 million while real GDP has increased by only $1,948.731 billion (or roughly $2 trillion in GDP growth after $6.54 trillion in debt). Or a DEBT velocity of 0.3. Yikes! No wonder China is bailing on US debt!

This chart makes debt issuance look better than it really is. Again, the DEBT VELOCITY of 0.3 is terrible meaning that for every $1 of Federal debt, we get 30 cents in Real GDP under Biden. One of my macroeconomics textbooks stated that debt growth is fine as long as real GDP growth rises faster than debt growth. Apparently, Treasury Secretary Janet Yellen didn’t read that textbook! Real GDP has grown by 9.43% under Biden while Federal debt has grown by … gulp .. 24%.

Yes, the US is borrowing like the proverbial drunken sailor while they “invest” in green energy, wars in Ukraine and the Middle East, and massive social welfare programs (like the old breads and circuses from the dying Roman Empire). When watching the media’s obsession with Taylor Swift and Chief’s Tight End Travis Kelce at The Super Bowl, it reminded me of “Breads and Circuses” as our nation is collapsing like a dying star. (That is why I Iike Gold, Silver and Bitcoin!)

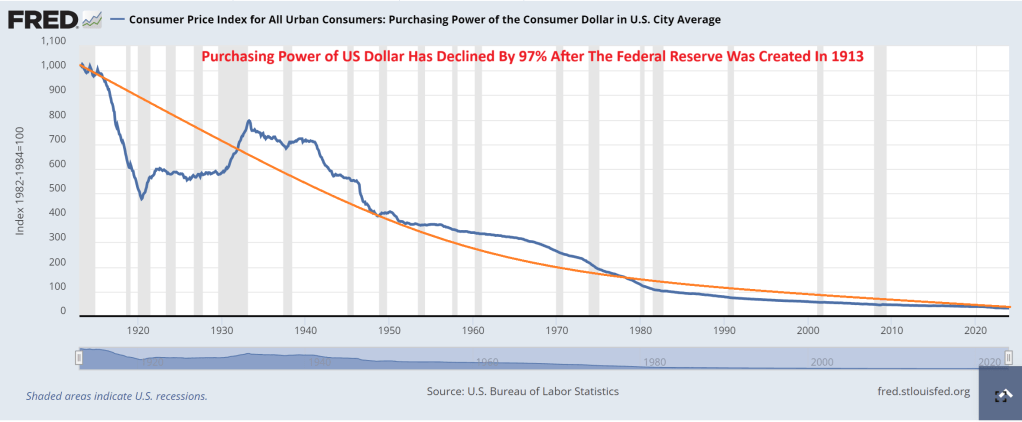

What about The Federal Reserve? It was created in 1913 after signed into existence by President Woodrow Wilson. Since The Fed’s inception, consumer purchasing power has declined by 97%.

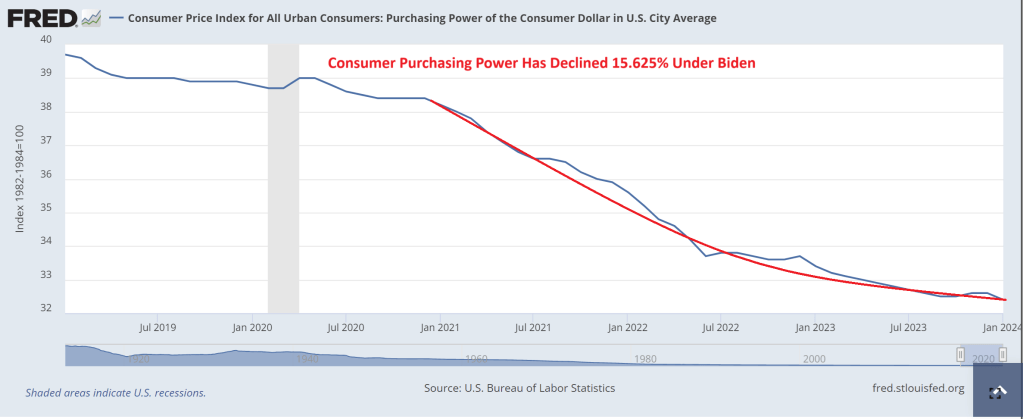

And under Biden, inflation has been so bad that consumer purchasing power is down 16%.

In summary, The Federal Reserve has been printing like crazy (I would say Batshit Crazy, but I actually think bats are adorable). And Treasury (under former Fed Chair Janet Yellen) has been borrowing like crazy too. While politicians claim the economy is in great shape, it is really because The Fed is printing wildly, Yellen is borrowing wildly, and much of US GDP is not due to the private sector, but Federal government spending … to the donor class. This is NOT a sustainable and will eventually crash into a ravine.

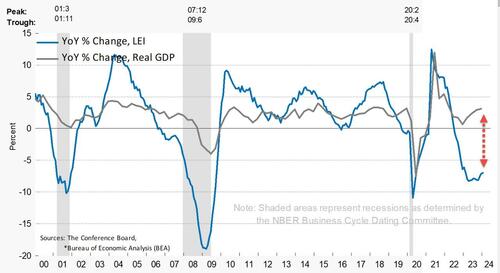

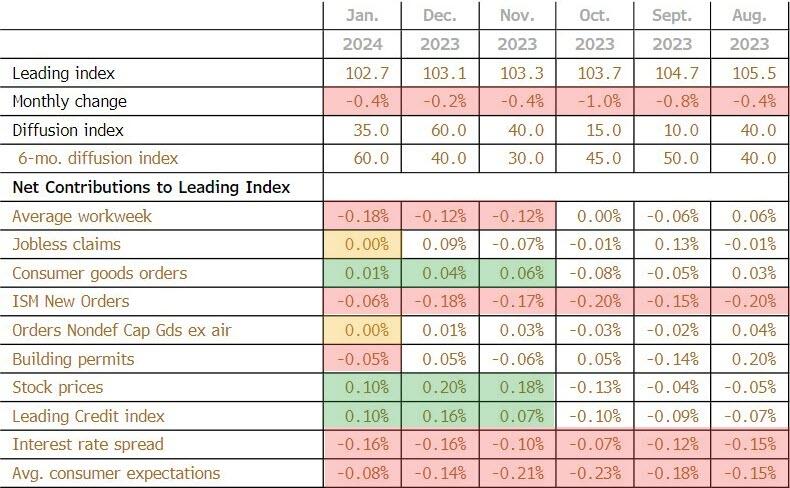

The biggest positive contributor to the leading index was stock prices (again)at +0.10

The biggest negative contributor was average workweek at -0.18

This is the 22nd straight MoM decline in the LEI (and 23rd month of 25) – equaling the longest streak of declines since ‘Lehman’ (22 straight months of declines from June 2007 to April 2008)

“While the declining LEI continues to signal headwinds to economic activity, for the first time in the past two years, six out of its ten components were positive contributors over the past six-month period (ending in January 2024).

As a result, the leading index currently does not signal recession ahead.

While no longer forecasting a recession in 2024, we do expect real GDP growth to slow to near zero percent over Q2 and Q3.”

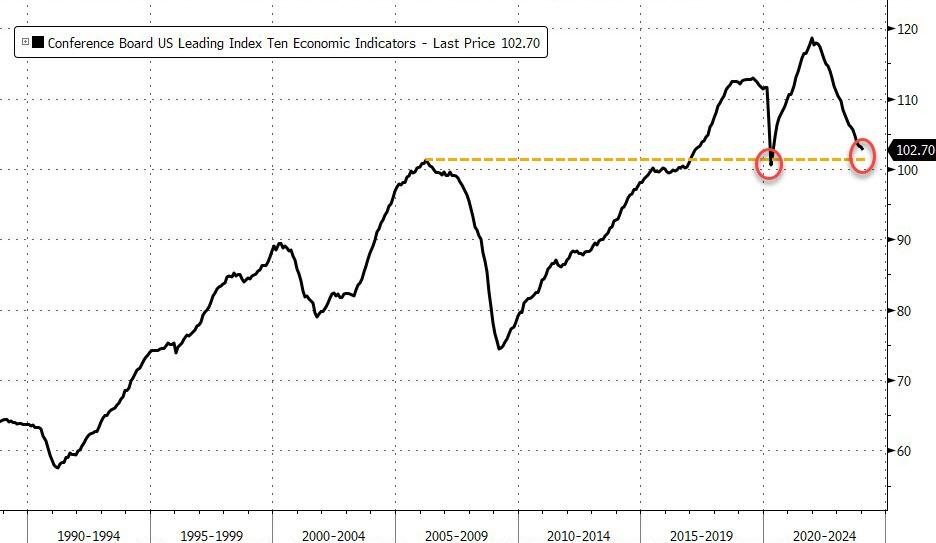

While the Conference Board seems optimistic, we are struggling to see any signs of hope! tumbling back below the peak in March 2006…

And on a year-over-year basis, the LEI is down 7.0% (down YoY for 19 straight months) – still close to its biggest YoY drop since 2008 (Lehman) outside of the COVID lockdown-enforced collapse (but starting to inflect)…

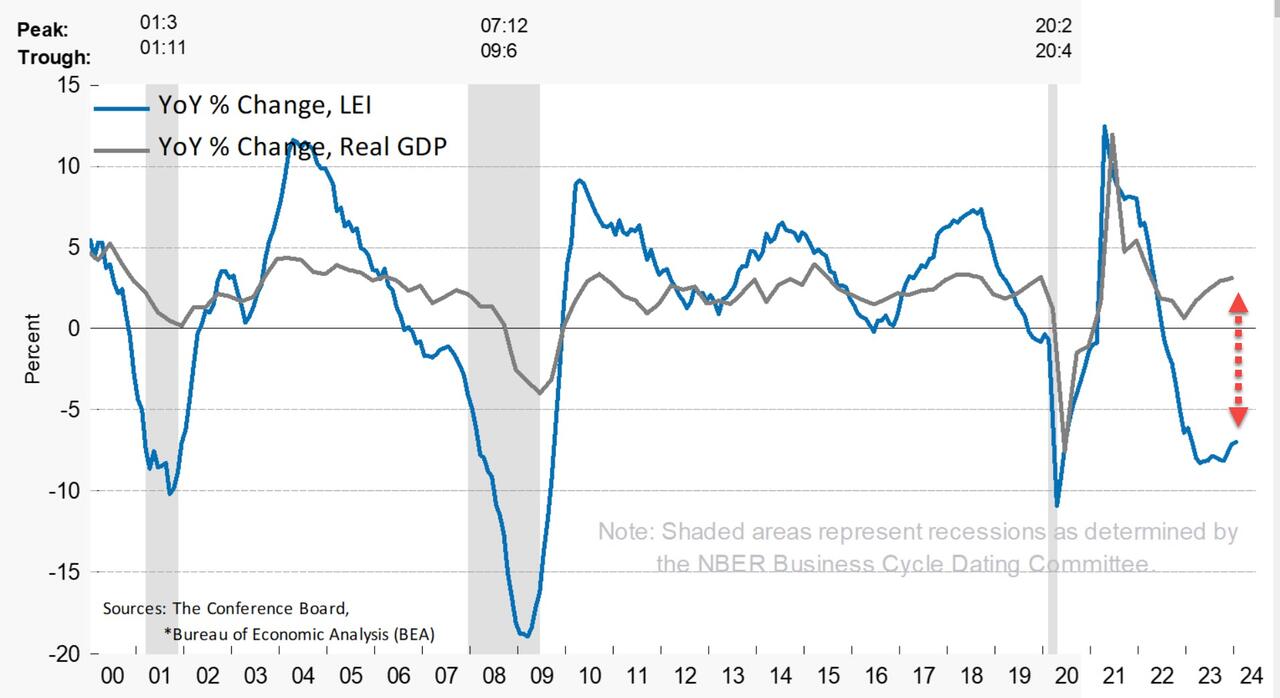

The annual growth rate of the LEI remains deeply negative and decoupled from Real GDP…..

Finally, the massive easing of financial conditions in the last few months suggests a turn in LEI is imminent…

And hence the ‘soft landing’ mission is accomplished… so no need for rate-cuts? (Except for the banking crisis that looms in March).

The cumulative number of jobs reported each month was 1,255,000 less than previously thought, with new seasonal and census data affecting total employment estimates, according to data from the BLS calculated by the Daily Caller News Foundation. The huge downward revisions are in spite of a 115,000 upward revision in December, the only month that saw an upward revision to the employment level in 2023.

The biggest revision was for March, which was revised down by a total of 266,000 jobs, followed by January at 234,000 and April at 205,000, according to the BLS. The lowest downward revision was in November, with only 2,000, followed by 11,000 in October.

“Revisions are a normal part of the reporting process, but large changes, or adjustments that consistently move in the same direction, are not normal,” E.J. Antoni, a research fellow at the Heritage Foundation’s Grover M. Hermann Center for the Federal Budget, told the Daily Caller News Foundation. “Instead, they’re indicative of something problematic with the BLS’ methodology. That can happen when market conditions change drastically enough to be outside of the assumptions used in their models.”

The revisions are due in part to an overestimate of the number of jobs in the U.S. economy in January 2023 at 155,007,000 instead of the revised 154,773,000, according to the BLS. The job level increased to a revised 157,347,000 by December, totaling an increase of 2,340,000 positions in the year.

The most recent jobs report in February also released an adjustment to the total jobs level, lowering March by 266,000 positions, according to the BLS. The jobs totals were also adjusted to recent census data, throwing off past estimates.

Recent years have not seen the same high downward revisions as 2023, with 2022 only seeing negative revisions in five months, equating to a downward revision of 66,000 for the year. March was the only month that was revised down in 2021, with the total number for the year being revised up by nearly 2 million as the country recovered from the COVID-19 pandemic.

Growth in government positions has bolstered recent job numbers, adding a total of 601,000 jobs to the U.S. economy in the past 12 months. The gains have led to an all-time record for government positions at 23,091,000, outdoing a surge in hiring from the 2010 census collections.

“When the economy was rapidly deteriorating at the onset of the Great Recession, the BLS repeatedly and consistently overestimated job levels, which then had to be revised down,” Antoni told the DCNF. “The worsening economic conditions fell outside of the assumptions used by the BLS statisticians, so the estimates became inaccurate. There could be similar problems today due to fallout from the government-imposed recession in 2020 because the labor market still hasn’t recovered.”

Remember the massive bank bailout of “subprime” mortgage securities back that resulted in the Dodd-Frank banking legislation of 2010? Yes know, where they promised NO MORE BANK BAILOUTS EVER??? Particularly if Disease X is unleashed and we start shutting down economies and schools again. Will we see ANOTHER bank bailout??

Cantor Fitzgerald CEO Howard Lutnick spoke with Fox Business host Maria Bartiromo on the sidelines at the World Economic Forum in Davos, Switzerland, last week. He offered a bleak outlook on the commercial real estate sector, warning a “very ugly” two years is ahead.

“Coming due in the next two and a half years at these higher rates – you’re not going to get proceeds, meaning when you have a $120 million loan on a building, and someone says I’ll give you 90 million at a much higher rate – than it throws the keys back to the lenders – and there’s going to be a lot of them that are going to get wiped out,” Lutnick told Bartiromo.

“I think $700 billion could default … The lenders are going to have to do things with them. They’re going to be selling. It’s going to be a generational change in real estate coming at the end of 2024 and all of 2025. We will be talking about real estate being just a massive change,” Lutnick said.

He warned: “I think it’s going to be a very, very ugly market in owning real estate over the next, you know, 18 months, two years.”

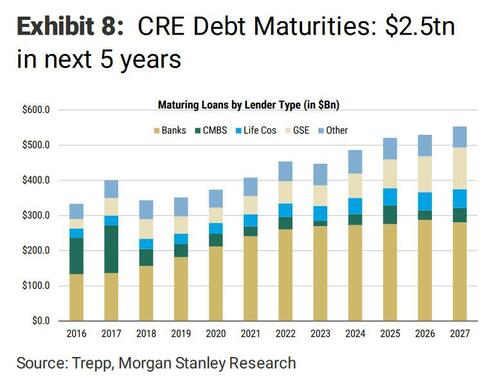

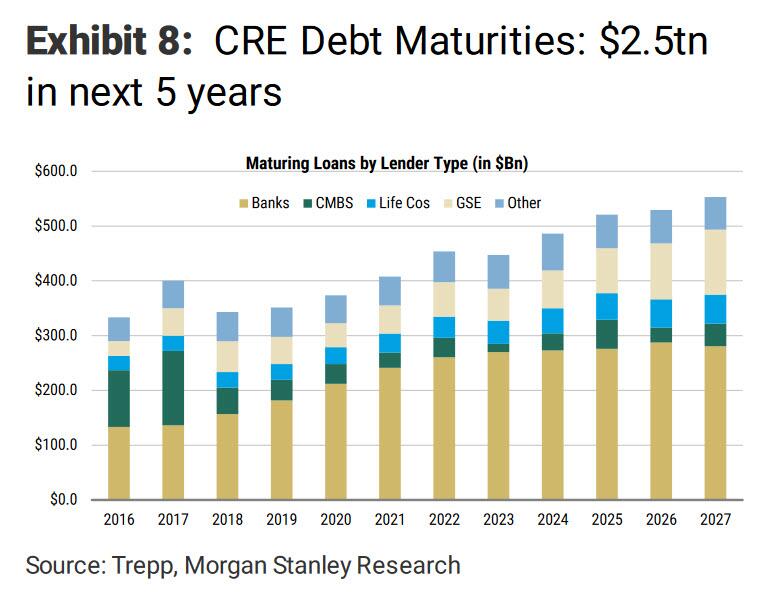

Lutnick noted that loan sales are set to become a major business opportunity with the upcoming maturity of CRE mortgages. He highlighted that an estimated trillion dollars of CRE debt is coming due over the next 2.5 years.

Shortly after the regional bank implosion in March 2023, Morgan Stanley penned a note to clients about a $2.5 trillion wall of CRE debt coming due over five years.

A recent survey of Terminal users by Bloomberg’s Markets Live found most respondents believe the office tower market needs a deeper correction before a rebound materializes.

Lutnick pointed out, “Real estate equity, REITS, are going to be in trouble … a lot of them are going to be wiped out, so many defaults, I think.”

Bloomberg office REITs have been plunging since early 2022 when the Federal Reserve embarked on the most aggressive interest rate hiking cycle in a generation to tame inflation.

“Commercial real estate is experiencing a meaningful repricing as cap rates correlate to long-term to interest rates,” Morgan Stanley told clients in a recent report, adding, “Patience is required while refinancing to higher debt costs gradually triggers valuation adjustments.”

Lutnick’s not the only one with a dismal outlook on CRE.

In a recent interview, Scott Rechler, Chairman and CEO of RXR Realty, told Goldman’s Allison Nathan that the CRE downturn is still in the early innings.

Its beginning to smell like Fed spirit! As the 2024 Presidential election rapidly approaches, The Fed will be pressured into lower interest rates to haul Biden’s befuddled and corrupt ass across the finish line. Or his replacement, Greasy Gavin Newsom. (Leaving an oil slick in his wake).

Lowering the mortgage rate will benefit the real estate market, which is currently been “Biden’d.” Due to inflation and The Fed’s mission to crush inflation.

High mortgage rates that approached 8% earlier this month continue to hammer builder confidence, but recent economic data suggest housing conditions may improve in the coming months.

Builder confidence in the market for newly built single-family homes in November fell six points to 34 in November, according to the National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI) released today. This is the fourth consecutive monthly drop in builder confidence, as sentiment levels have declined 22 points since July and are at their lowest level since December 2022. Also of note, nearly the entire HMI data for November was collected before the latest Consumer Price Index was released and showed that inflation is moderating.

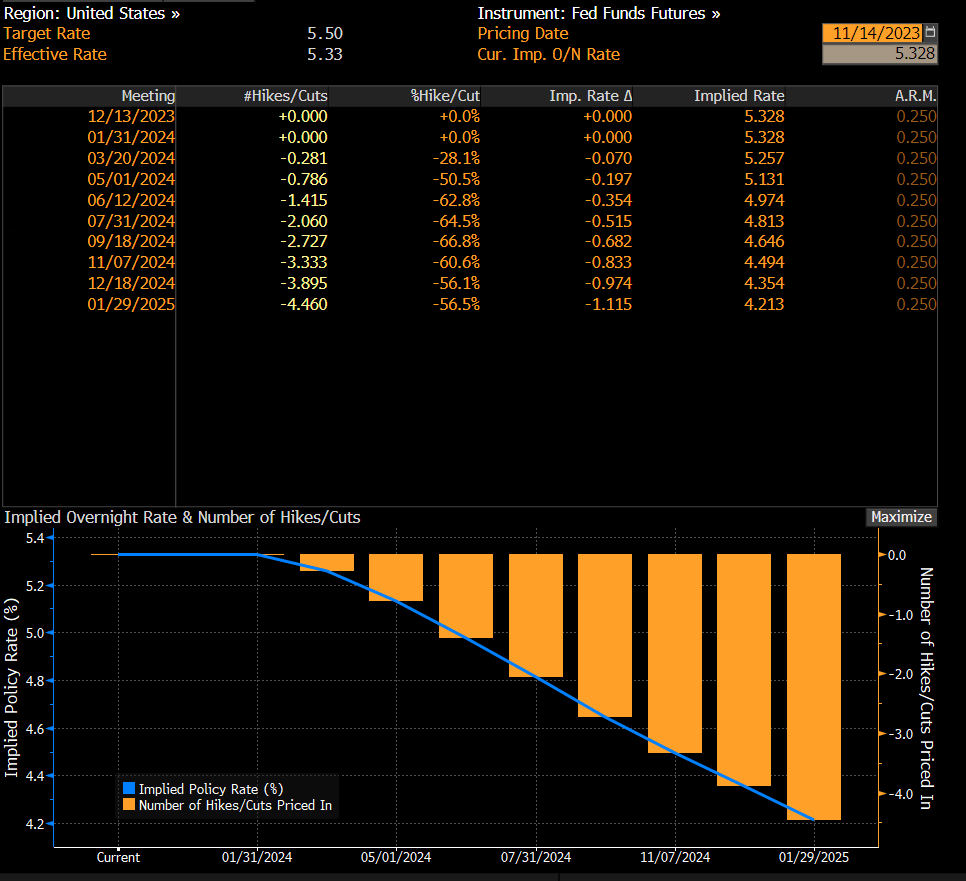

Mortgage rates will likely decline in 2024 as The Fed reverses its inflation-crushing policy for Presidential election interference.

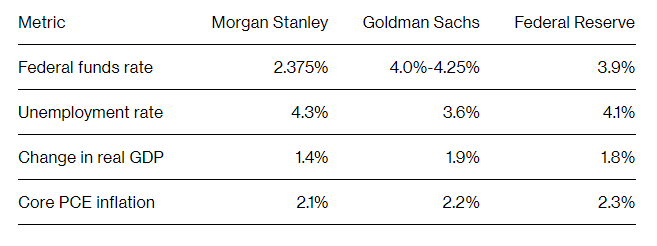

And Morgan Stanley forecasts the Fed Funds Rate to plunge to 2.375%.

Joe Biden is 80 and not exactly the most energetic President that can inspire confidence.

Maybe the economy needs Viagra.

I really wish Biden would stop babbling about “his” approach to economic growth, a Chinese Communist approach of top down economic management.

Under Biden, Americans have seen a 17.6% price hike and a 3% pay cut. Inflation has averaged 5.9% — more than double the level of inflation under any of the last four presidents.

After listening in horror to Joe Biden’s press conference after his summit with China’s Xi, I had to ask the following question: what does Joe Biden has in common with Georgia Tech? Answer? They are both rambling wrecks. Biden made a horrendous foreign policy blunder by calling Xi a “dictator” and almost blew it by nearly spillling the beans on our foreign policy negotiations with Israel. SecState Blinken had to intervene. We are represented by Winken (Harris), Blinken and Nod (Biden, who usually looks asleep or confused).

But back to the horrors of a slowing economy.

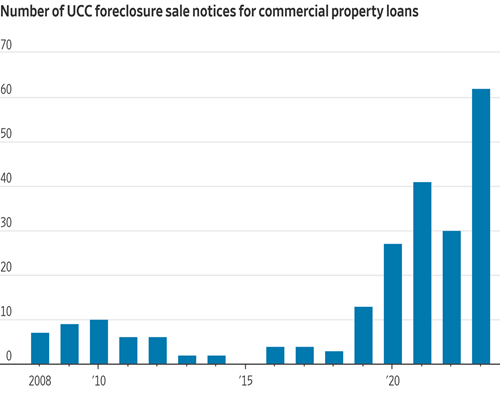

As the US economy slows down (like Biden himself), we are seeing further cracks in the real estate market. Foreclosure sale notices for commercial property loans are exploding.

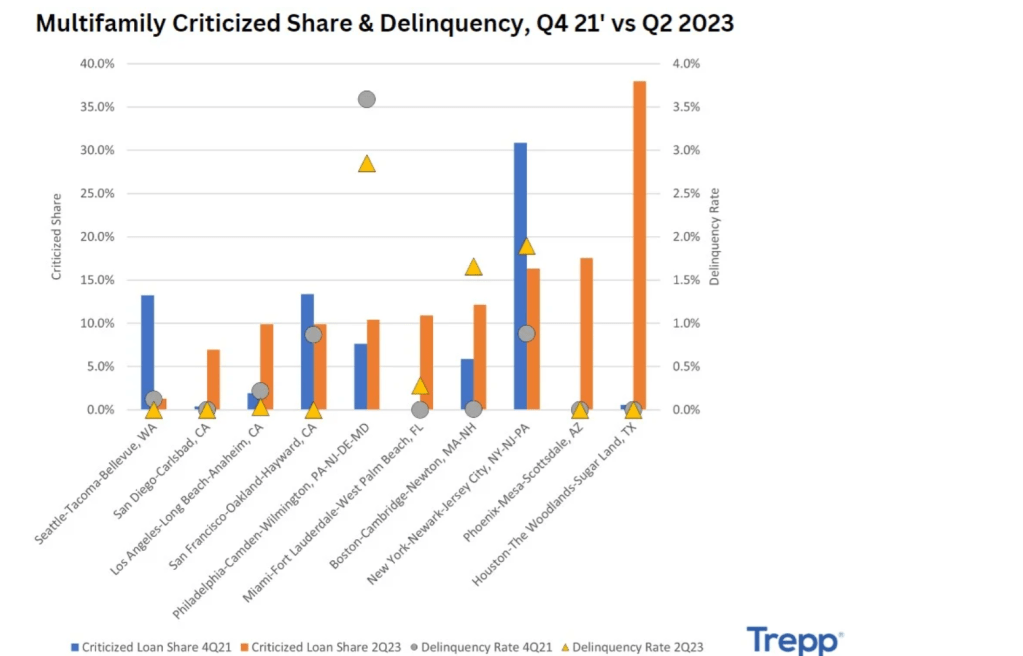

And depending on the MSA, multifamily delinquencies are booming, like in Houston, Texas, New York City and Phoenix AZ.

Then we have this headline: “Not Just Office Towers – Commercial Real Estate Sales Crater Throughout Los Angeles.” It’s difficult to find big commercial real estate deals of any kind in Los Angeles. A new report from NAI Capital reveals how severe and universal the decline in activity is throughout the region this year amid collapsing values, higher interest rates, and a new tax on property sales above $5 million.

Yes, I know, California’s real estate woes are mostly the fault of their politicians like Governor Gavin (Gruesome) Newsom. The same guy who ordered San Francisco’s homeless population to be moved creating a new Potemkin Village. But rising interest rates are the fault of excessive spending by Congress and the Biden Administration.

The primary reason for Moody’s downgrade of US credit? The absolutely insane ramp-up of Federal spending starting with the Covid outbreak in early 2020. And the subsequent economic shutdowns and the closure of public schools. But even as Covid faded to diminished status, Bidem demanded an increase in Federal spending. Well, Biden’s war (Ukraine) which looks like spending in perpetutity.

Of course, Biden/Congress love to spend money, but raising personal taxes to pay for it is political suicide. A private sector firm would cut spending to balance its budget, government simply doubles down on spending. Never let a crisis go to waste!

And The Federal deficit keeps on growing under Biden/Yellen’s economic reign of error.

After a disastrous 30Y bond auction this week, a collapse in Treasury market liquidity, and an accelerating rise in the market’s perception of the United States’ credit risk, Moody’s has just cut its outlook on US credit ratings to negative from stable.

Source: Bloomberg

The key driver of the outlook change to negative is Moody’s assessment that the downside risks to the US’ fiscal strength have increased and may no longer be fully offset by the sovereign’s unique credit strengths.

In the context of higher interest rates, without effective fiscal policy measures to reduce government spending or increase revenues, Moody’s expects that the US’ fiscal deficits will remain very large, significantly weakening debt affordability.

Continued political polarization within US Congress raises the risk that successive governments will not be able to reach consensus on a fiscal plan to slow the decline in debt affordability.

Moody’s does affirm the Aaa rating:

The affirmation of the Aaa ratings reflects Moody’s view that the US’ formidable credit strengths continue to preserve the sovereign’s credit profile.

First, Moody’s expects the US to retain its exceptional economic strength. Further positive growth surprises over the medium term could at least slow the deterioration in debt affordability.

Second, the US’ institutional and governance strength is also very high, supported in particular by monetary and macroeconomic policy effectiveness. While the adjustment of the US economy and financial sector to higher-for-longer interest rates is underway, policymakers have facilitated the transition through transparent and effective policy.

Finally, the unique and central roles of the US dollar and Treasury bond market in the global financial system provide extraordinary funding capacity and significantly reduce the risk of a sudden spiraling of funding costs, which is particularly relevant in the context of high debt levels and weakening debt affordability.

The US’ long-term local- and foreign-currency country ceilings remain unchanged at Aaa. The Aaa local-currency ceiling reflects a small government footprint in the economy, relatively predictable and reliable institutions, very low external imbalances and moderate political risks, all of which reduce the risks posed to non-government issuers by government actions or shocks that would commonly affect the government and the private sector. The foreign-currency ceiling at Aaa reflects the country’s strong policy effectiveness and open capital account which reduce transfer and convertibility risks to minimal levels.

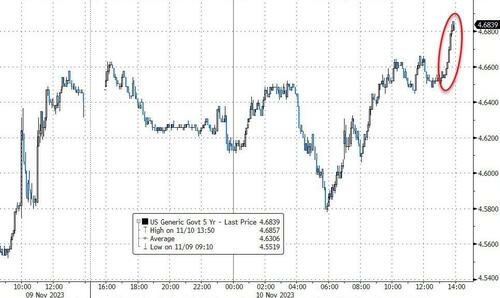

The market – late on a Friday – pushed yields on the 2Y and 5Y Treasyr notes to fresh new highs for the day…

Full Rationale:

ABSENT POLICY ACTION, FISCAL STRENGTH WILL DECLINE

The sharp rise in US Treasury bond yields this year has increased pre-existing pressure on US debt affordability. In the absence of policy action, Moody’s expects the US’ debt affordability to decline further, steadily and significantly, to very weak levels compared to other highly-rated sovereigns, which may offset the sovereign’s credit strengths.

Past increases in interest rates by the Federal Reserve will continue to drive the US government’s interest bill higher over the next few years. Meanwhile, although the government’s revenue base will rise in line with the economy as a whole, in the absence of specific policy action, this will occur at a much slower pace than the rise in interest payments. Moody’s expects federal interest payments relative to revenue and GDP to rise to around 26% and 4.5% by 2033, respectively, from 9.7% and 1.9% in 2022. These projections factor in Moody’s expectation of higher-for-longer interest rates, with the average annual 10-year Treasury yield peaking at around 4.5% in 2024 and ultimately settling at around 4% over the medium term. The debt affordability forecasts also take into account Moody’s expectations that, absent significant policy changes, the federal government will continue to run wide fiscal deficits of around 6% of GDP near term and to around 8% by 2033, the widening being driven by higher interest payments and aging-related entitlement spending.

By comparison, deficits averaged around 3.5% of GDP from 2015-2019. Such deficits will raise the US federal government’s debt burden to around 120% of GDP by 2033 from 96% in 2022. In turn, a higher debt burden will inflate the interest bill.

For a reserve currency country like the US, debt affordability – more than the debt burden – determines fiscal strength. As a result, in the absence of measures that limit the size of fiscal deficits, fiscal strength will increasingly weigh on the US’ credit profile.

FISCAL RISKS ARE EXACERBATED BY ENTRENCHED POLITICAL POLARIZATION UNDERSCORING RISING POLITICAL RISK

At a time of weakening fiscal strength, there is an increased risk that political divisions could further constrain the effectiveness of policymaking by preventing policy action that would slow the deterioration in debt affordability. These risks underscore rising political risk to the US’ fiscal position and overall sovereign credit profile.

Recently, multiple events have illustrated the depth of political divisions in the US: renewed debt limit brinkmanship, the first ouster of a House Speaker in US history, prolonged inability of Congress to select a new House Speaker, and increased threats of another partial government shutdown due to Congress’ inability to agree on budgetary appropriations. In Moody’s view, such political polarization is likely to continue. As a result, building political consensus around a comprehensive, credible multi-year plan to arrest and reverse widening fiscal deficits through measures that would increase government revenue or reform entitlement spending appears extremely difficult.

While the US’ Aaa rating takes into account relative weaknesses with regards to the quality of the country’s legislative and executive institutions and fiscal policy effectiveness compared to other Aaa-rated sovereigns, there is a risk that these weaknesses take greater credit relevance because the deteriorating debt affordability trend would call for a more significant and effective fiscal policy response.

In particular, the US’ lack of an institutional focus on medium-term fiscal planning, either through legislated fiscal rules aimed at improving the fiscal balance or general bipartisan consensus on the need for fiscal consolidation, is fundamentally different from what is seen in most other Aaa-rated peers such as in Government of Germany (Aaa stable) and Government of Canada (Aaa stable). Meanwhile, the more short-term focus of US fiscal policymaking, along with limited fiscal flexibility – because a very large portion of nondiscretionary budgetary spending is on mandatory entitlement programs and debt service (around 75% of total outlays), exacerbates already fractious bipartisan politics around a relatively disjointed and disruptive budget process. As annual debt service costs continue to rise, fiscal flexibility will diminish even further.

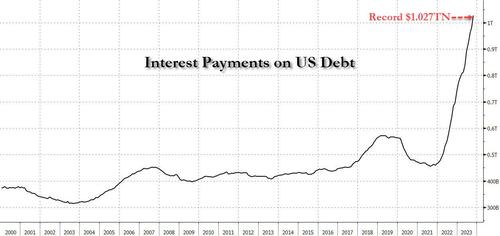

Remember, annual interest payments of the $33.8 TRILLION debt load is now over $1 TRILLION. Yes. rampant Federal spending begat inflation which begat Fed rate hikes.

Let’s start with personal savings as a percentage of disposable income. It has been in the red (meaning very low) under Billions Biden.

And The Fed is really in the red under Biden’s inflation rattling spending with losses leading to a surge in remittances.

And then we have the growth in the Federal deficit as a % of GDP in the red.

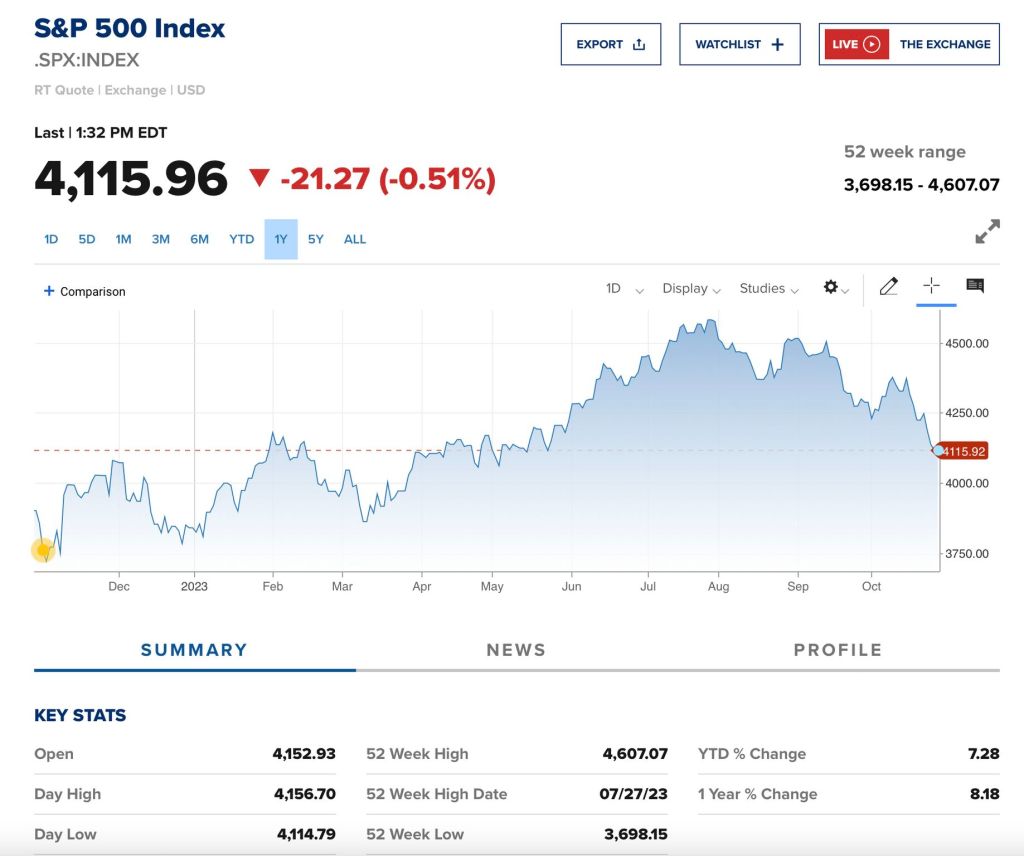

And the S&P 500 is in the red since August.

Even Biden’s pro-censorship buddies in the tech world are in the red since July.

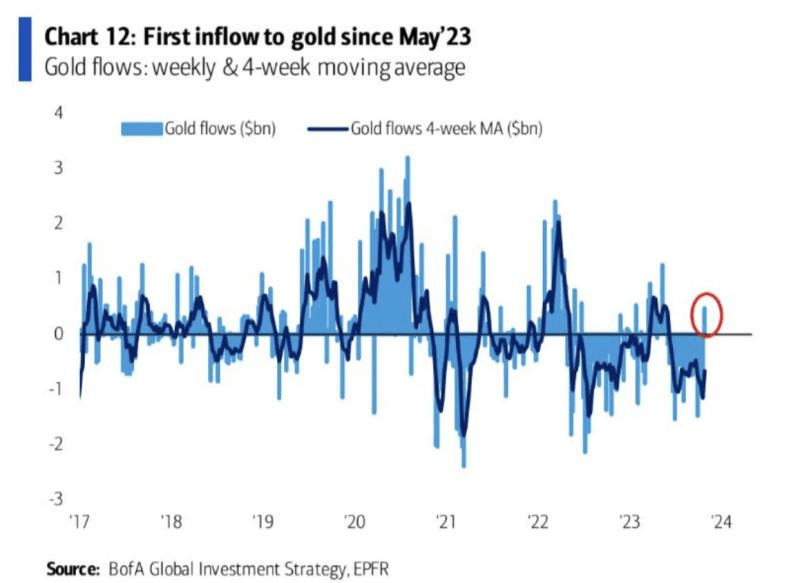

On the black side of the ledge, Bitcoin (along with gold) are through the roof.

The first inflow to golf since May ’23.

But at least Bidenomics has helped the donor class get wealthier and has helped the lessers get part-time jobs.

Yes, Bidenomics is a highway to hell for the 99%. But a stairway to heaven for the donor class and 1%. And the donor class (and defense/banking/tech/drug industries) have Biden under their thumbs.

My foolish US Senator Sherrod “The Mad Marxist” Brown claimed that he hasn’t noticed illegal immigrants.

Of course, Senator Brown could travel with Biden to the border to witness military age men crossing the border under Biden/Mayorkis “:Operation US Chaos.”

We are Livin’ la vida Biden as Biden continues to push illegal immigration and working with Communist dictators like Venezuela’s Nicolas Maduro and NOT expand US energy production.

The Consumer Financial Protection Bureau (CFPB) and the Department of Justice (DOJ) released a joint statement telling financial institutions that while it is not illegal to consider a person’s immigration status in the decision on whether to lend money, an overreliance on it could run afoul of the law, according to the statement. The statement implicates the Equal Credit Opportunity Act (ECOA), which makes it illegal to discriminate on the basis of race, color, religion, national origin, sex and more in considering a person’s credit application as the mechanism, even though the law does not list citizenship status as a protected attribute.

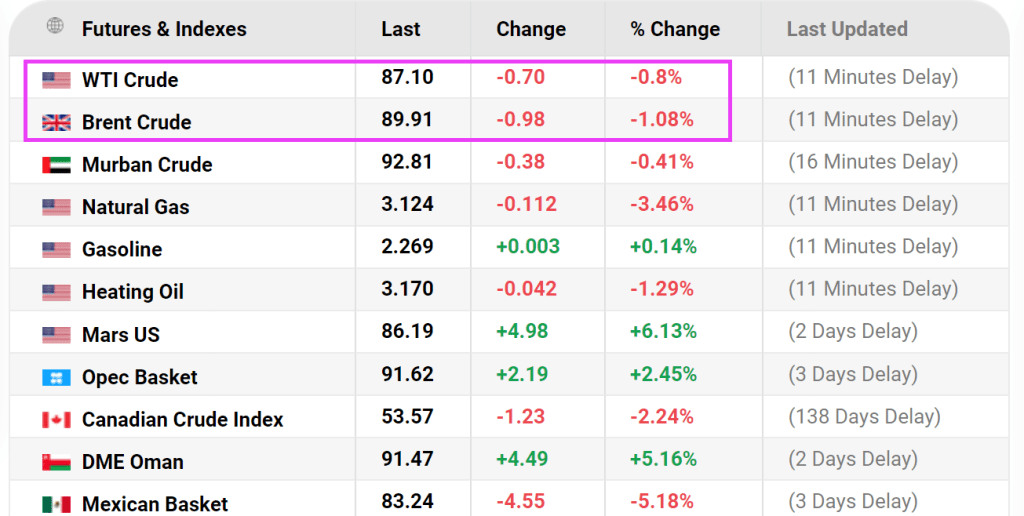

The result? WTI Crude is down almost -1% today and Brent Crude is down over -1%.

The sad part of Biden’s deal with brutal Marxist dictator Nicolas Maduro requires Venezuela to allow another candidate to run against Maduro in the next Presidential election. What? Biden and Democrats are working hard to eliminate Donald Trump from running for President in 2024, but want Venezuela to have competition??

So, Biden is sticking to his anti-US energy production stance while supporting a brutal Marxist dictator AND forcing banks to lend to illegal immigrants.

Joe Biden and brutal Marxist dictator Nicolas Maduro.

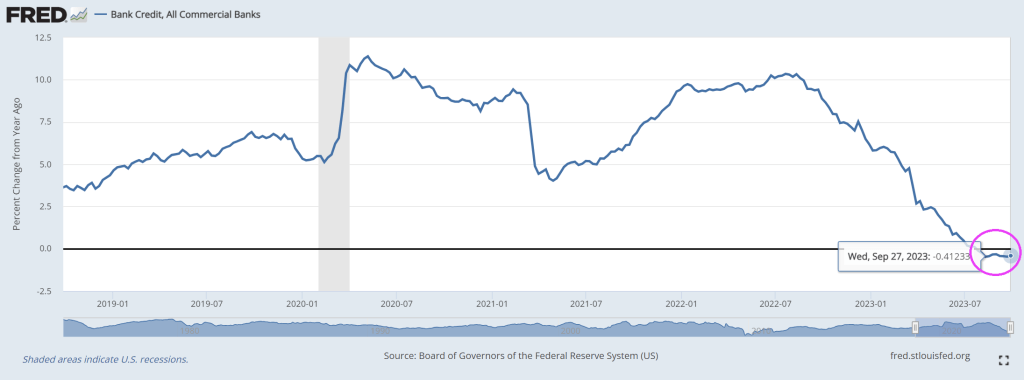

Bidenomics is failing catestropically. Example? As interest rates rise to fight Biden’s Federal spending splurges, bank credit growth slowed to -0.41% YoY for the 10th straight week of negative credit growth.

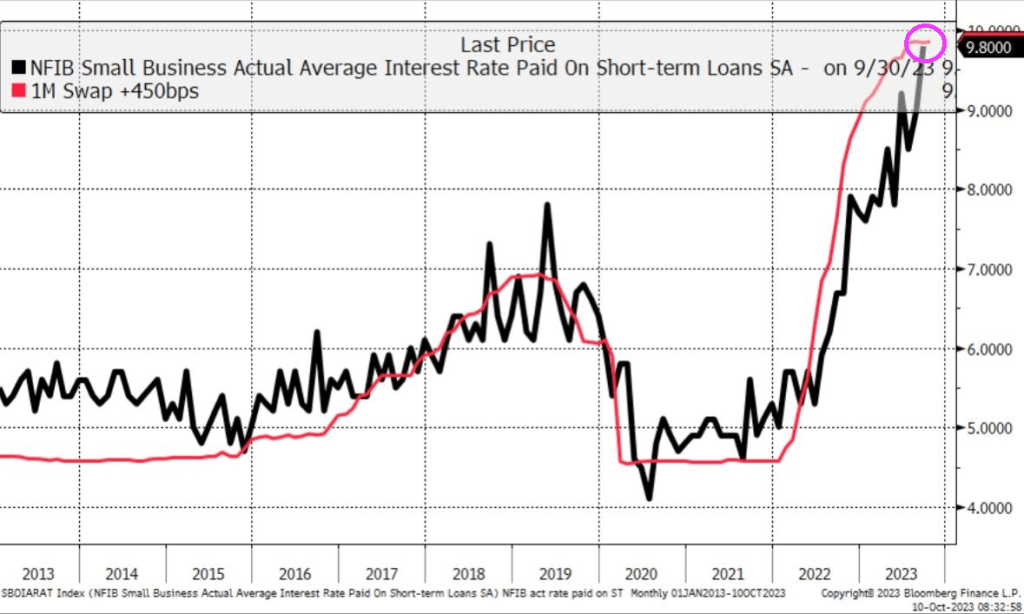

While interest paid on short-term loans almost 10%!!

“Jimmy, watch me tank the economy even worse than you did!”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.