So, the Biden Administration made a horrible error by guaranteeing deposits at Silicon Valley Bank for deposits over $250,000. Essentially, Biden bailed out big tech that kept their deposits at SVB.

But what triggered the run on SVB and other banks? Simple. Biden and Congress spent like drunken sailors with Covid and The Federal Reserve went nuts printing money. Viola! We got inflation. But with inflation came The Fed’s attempt to get inflation back to its 2% target (difficult since Biden/Congress refuse to return spending to pre-Covid levels). But as interest rates rise, duration (weighted average life of MBS) rose dramatically meaning that risk increased. But banks like SVP ignored the risk, or didn’t hedge, or were spending time worrying about non-bank related issues.

So, what happened? Banks are holding Treasuries and MBS (orange line) that are getting clobbered with rate hikes (yellow line).

Talk about volatility. Today, the 2-year Treasury yield is up over 20 basis points as bond volatility hits levels last seen in 2008, just prior to the subprime credit crisis.

So, Biden’s bailout of SVP depositors stopped the deposit run for the moment. But if The Fed keeps hiking rates, banks are going to be hurting worse and worse. They could rebalance their portfolios and/or hedge. But with Uncle Spam (Biden) at the helm, bailouts are always on the table.

Mortgage applications increased 6.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 3, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 6.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 9 percent compared with the previous week. The Refinance Index increased 9 percent from the previous week and was 76 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 7 percent from one week earlier. The unadjusted Purchase Index increased 9 percent compared with the previous week and was 42 percent lower than the same week one year ago.

Today, we saw mortgage rates climb further to 7.11% as the US Treasury yield curve (10Y-2Y) descends into Mortgage Mordor as The Fed continues to tighten.

What a mess in Washington DC. While House Republicans are at lagerheads with Senate Democrats and Resident Biden over Federal spending cuts, the price of insuring against a debt default just rose to 76.75.

How bad it that? Put it this way. Millions are fleeing Mexico and Guatemala and coming to the US. But Mexico has a lower cost of insuring against a debt default than the USA. And Guatemala is almost as expensive as the USA.

It will all be over soon, according to CDS prices.

Not really a surprise, but January’s personal spending numbers came in hot at 1.8% MoM. Also, Personal Consumption Expenditures PRICE index (aka, inflation) rose to 5.4% YoY.

Here comes The Fed! The 2-year Treasury yield rose 10 basis points this morning.

The first headline I saw when I turned on Bloomberg.com was “DOJ Officials Find More Classified Documents at President Biden’s Home.” This is an improvement! So far, the task has been handled by Biden’s private attorneys who don’t have proper security clearance; at least the Justice Department is finally getting involved!

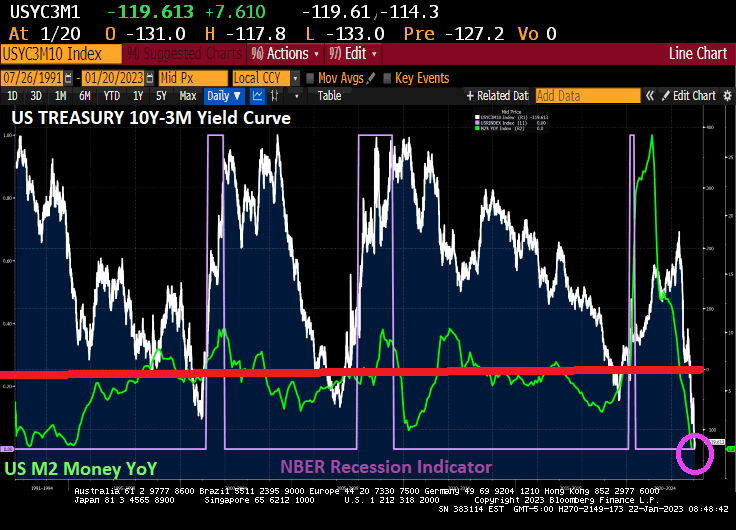

But back to the US yield curve. It is now the most inverted in 30+ years as M2 Money growth stalls. Inverted yield curves have preceded recessions in the past.

But as China reopens and Europe is experiencing a warmer winter than expected (meaning that Europe has sufficient natural gas reserves) and US inflation cooling,

we are seeing market-implied odds of a recession falling in January.

I am still betting on a recession in the second half of 2023.

Liz Ann Sonders, Chief Investment Strategist, Charles Schwab & Co, wrote today “Collapse in shipping rates continues to look unreal … cost to ship 40-foot container from Shanghai to Los Angeles has fallen by 83% from peak, by far largest drop on record (bringing level to lowest since June 2020)”

Yes, Liz Ann, shipping costs from Shanghai to Los Angeles are plunging. But why?

Federal Reserve and Federal government stimultypo has wound down. M2 Money YoY growth is the lowest since 2010 and no, it isn’t the result of Mayor Pete’s magical skills at clearing the logjam at Los Angeles ports. It is the slowing of Federal stimulus (or stimulypto).

Here is Liz Ann Sonders tweet.

Let’s see if 1) The Fed continues to hike and 2) will House Republicans halt the insane spending, particularly since the start of Covid in 2020.

The Federal Reserve’s DOTS PLOT shows where each Fed official’s projection for the central bank’s key short-term interest rate is headed. As of the September 21, 2022 Fed Open Market Committee (FOMC) meeting, the prediction of future Fed target rates is decidedly DOWNWARD SLOPING.

The Fed hawks, those that want to tighten monetary policy, are Bowman, Waller, Kashkari, Mester and George. The Fed doves (or those who are neutral) are Biden recent appointees Barr, Cook, Jefferson, Logan, Collins. Note that Brainard and Bostic are the only technical doves.

I call the hawks at The Fed “The Blackhawks” since their mission of fighting inflation may lead to a recession. And Bowman, Mester and George are Lady Blackhawks.

Things are getting interesting in DC, to say the least. The US is 100% likely to face a recession in the next 12 months while The Federal Reserve is on its crusade to fight inflation caused by … The Federal Reserve, Biden’s green energy shenanigans and massive, irresponsible Federal spending that even Former Obama economist Lawrence Summers warned would cause inflation. So what will The Fed do? Lower rates and expand their assets purchases to fight the impending recession OR keep tightening to fight Bidenflation? But where we are now is that the fixed-income market could be in big, big trouble.

For months, traders, academics, and other analysts have fretted that the $23.7 trillion Treasuries market might be the source of the next financial crisis. Then last week, U.S. Treasury Secretary Janet Yellen acknowledged concerns about a potential breakdown in the trading of government debt and expressed worry about “a loss of adequate liquidity in the market.” Now, strategists at BofA Securities have identified a list of reasons why U.S. government bonds are exposed to the risk of “large scale forced selling or an external surprise” at a time when the bond market is in need of a reliable group of big buyers.

“We believe the UST market is fragile and potentially one shock away from functioning challenges” arising from either “large scale forced selling or an external surprise,” said BofA strategists Mark Cabana, Ralph Axel and Adarsh Sinha. “A UST breakdown is not our base case, but it is a building tail risk.”

In a note released Thursday, they said “we are unsure where this forced selling might come from,” though they have some ideas. The analysts said they see risks that could arise from mutual-fund outflows, the unwinding of positions held by hedge funds, and the deleveraging of risk-parity strategies that were put in place to help investors diversify risk across assets.

In addition, the events which could surprise bond investors include acute year-end funding stresses; a Democratic sweep of the midterm elections, which is not currently a consensus expectation; and even a shift in the Bank of Japan’s yield curve control policy, according to the BofA strategists.

The BOJ’s yield curve control policy, aimed at keeping the 10-year yield on the country’s government bonds at around zero, is being pushed to a breaking point.

Well. Bidenflation certainly isn’t helping, but Statist Economist and Cheerleader Janet Yellen can’t bring herself to blame green energy policies, rampant Federal spending or irresponsible Federal Reserve policies for the crisis.

You will note the differences between today and the financial crisis of 2008-2009. The financial crisis gave us a massive surge in government securities liquidity thanks to then Fed Chair Ben Bernanke imitating Japan’s Central Bank and buying US government securities. Fast forward to today and the liquidity index hasn’t budged much since 2010 (except for a little blip around the Covid Fed intervention of early 2020), but we are now seeing near 40-year highs in inflation and a barely declining Fed balance sheet. And M2 Money YoY (mostly commercial bank deposits) are crashing.

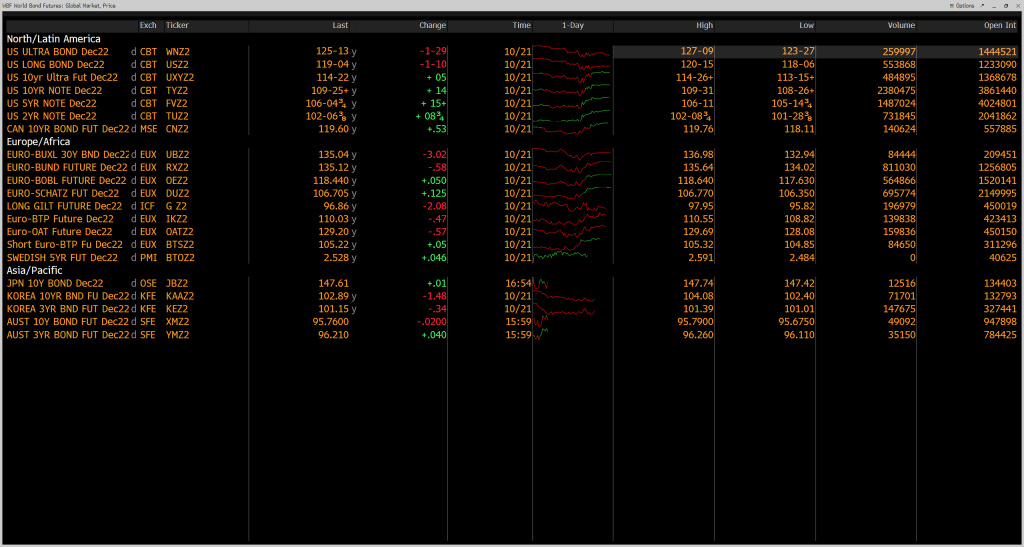

I am guessing that The Fed will pivot given that stock futures are way up for Monday. The Dow Jones mini is up 770 points and the S&P 500 mini is up 88.75 points.

Bond market futures (specifically the US Ultra Bond) is down for Monday, meaning yields will be climbing.

I remember giving a speech at The Brookings Institute in Washington DC. Talk about stranger in a strange land. One person who I was debating got frustrated and said “You are such a … Republican!!!” As if that was the worst slur he could throw at me.

US core inflation keeps rising and diesel fuel, the life line of the economy, is rising again and is UP 107% under Biden. And the inventory of diesel fuel is DOWN -35.2%.

Speaking of the end of the world, NAHB foot traffic has collapsed.

To begin with, headline inflation remains high at 8.2% YoY while CORE inflation (headline less food and energy) rose to 6.6% YoY.

Meanwhile, REAL average weekly earnings growth YoY further declined to -3.8% YoY.

On the bond front, the Bank of America ICE bond volatility index rose to Great Recession/banking crisis levels (also achieved during the Covid government shutdowns).

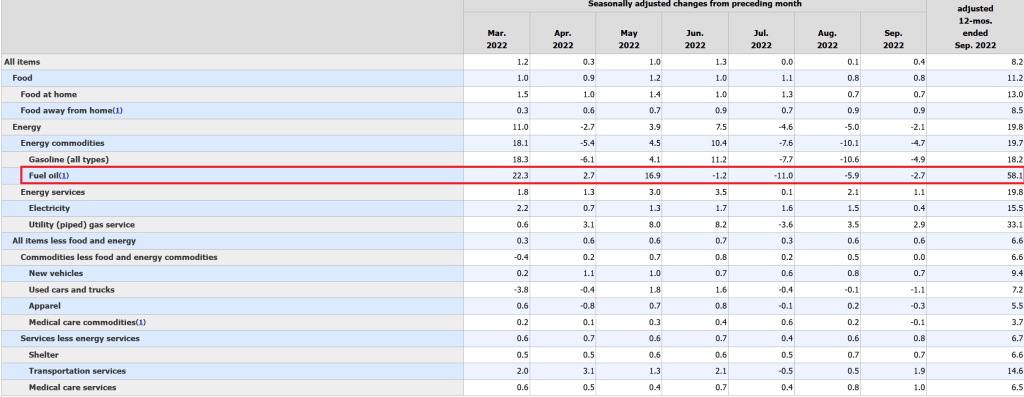

But back to the low-ball BLS inflation data. The biggest gain in price is … fuel oil at 33.1% YoY. Food at home rose 13.0% while gasoline rose 18.2%. Rent, according to the BLS, rose 6.6%.

Biden has probably been told by Ron Klain and Susan Rice that this is a good report.

You must be logged in to post a comment.