The US housing and mortgage markets are thunderstruck by The Fed’s attempts at cooling inflation down to 2%.

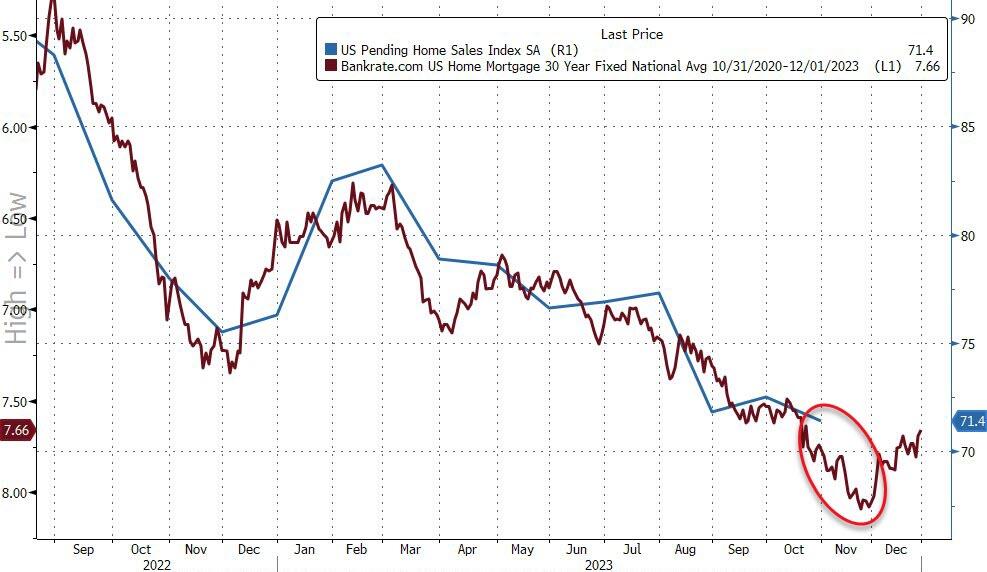

After a small bounce last month – following the puke in August – pending home sales dropped 1.5% MoM in October (better than the 2.0% MoM decline expected). This left YoY sales down 6.6% (negative for the 23rd straight month)…

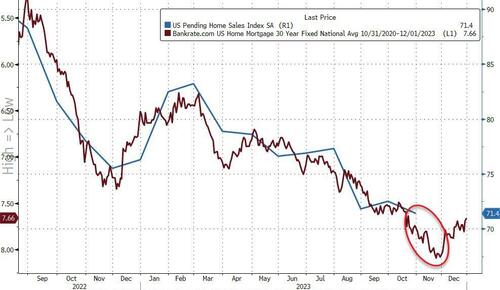

The Pending Home Sales Index dropped back to a new record low…

By region, only the Northeast saw an increase in pending sales last month.

Sales fell the most in the West, down 6%, while contract signings in the South and Midwest slipped 1.9% and 0.4%, respectively.

Home sales are rising in places with more inventory, Lawrence Yun, NAR’s chief economist said, noting that purchases of new houses are up so far this year because of builders’ ability to create inventory.

“During October, mortgage rates were at their highest, and contract signings for existing homes were at their lowest in more than 20 years,” Yun said in a statement.

“Recent weeks’ successive declines in mortgage rates will help qualify more home buyers, but limited housing inventory is significantly preventing housing demand from fully being satisfied.”

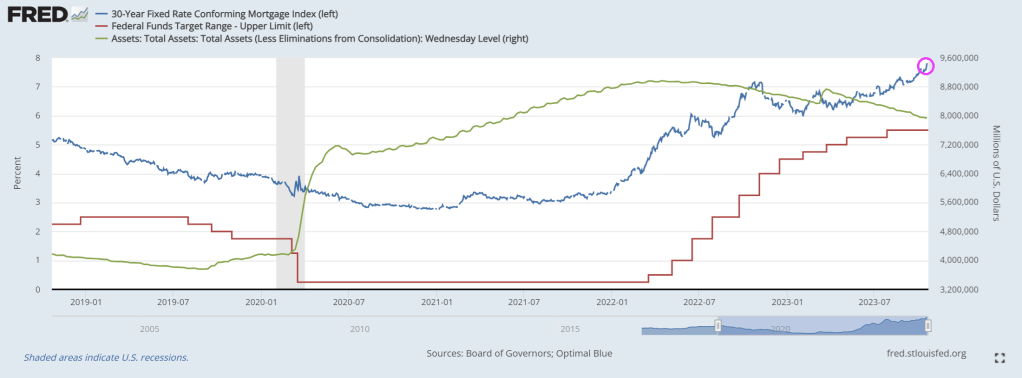

The trend in pending home sales is following the mortgage rate (with a one month lag) and is set to fall further still…

The pending-home sales report is a leading indicator of existing-home sales given houses typically go under contract a month or two before they’re sold.

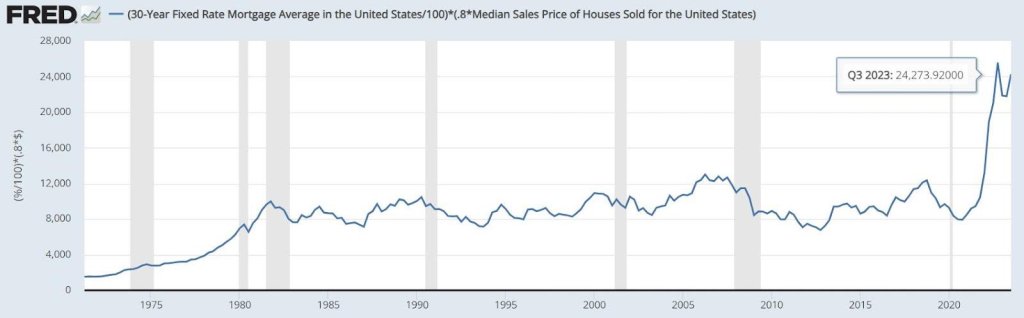

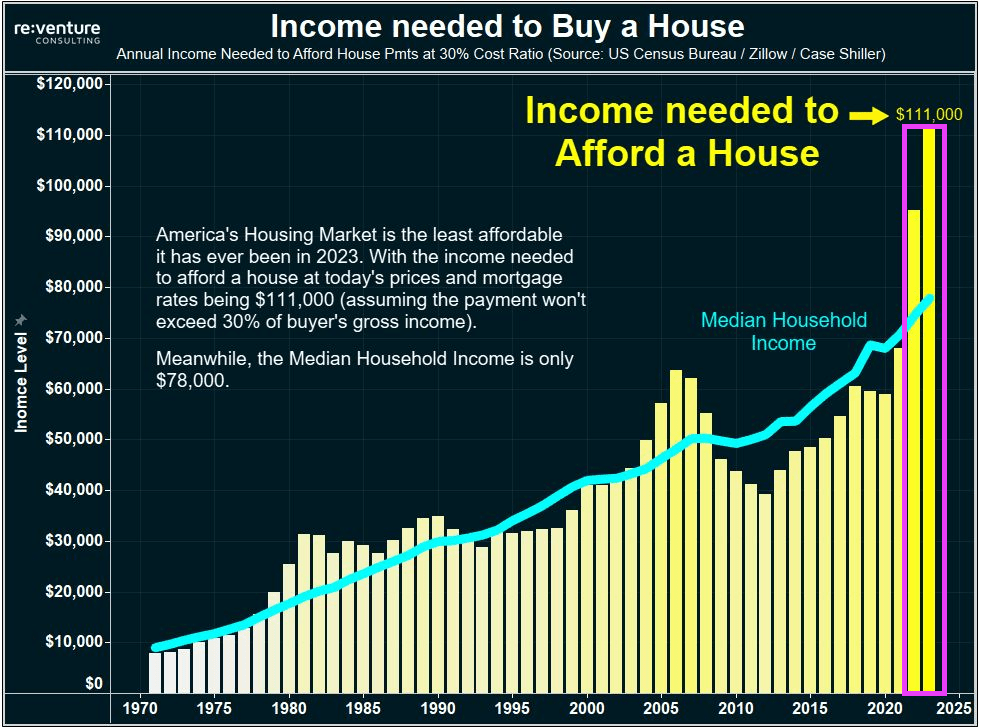

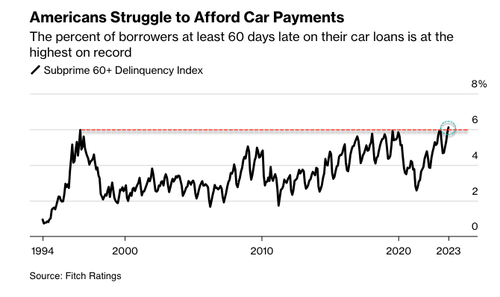

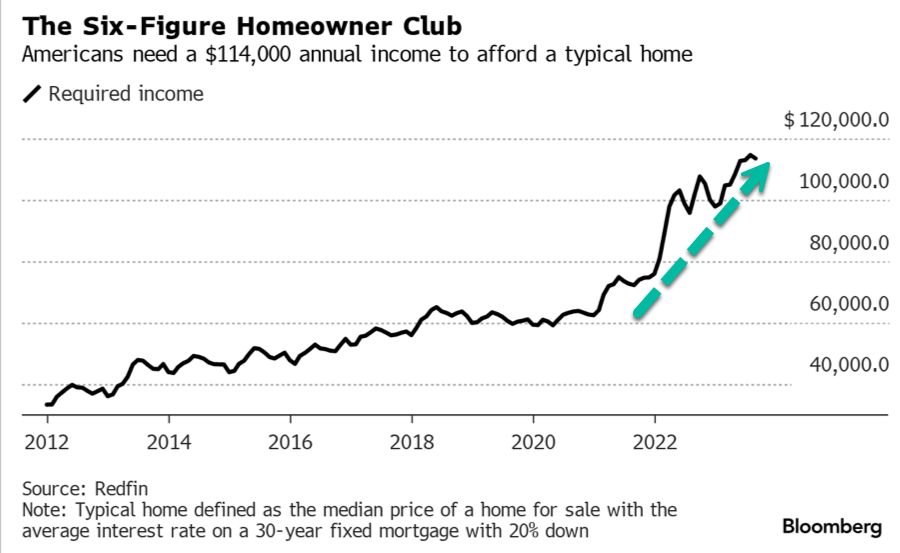

How long with Powell and his pals be able to keep this ‘higher for longer’ stress up as Americans’ largest source of wealth evaporates?

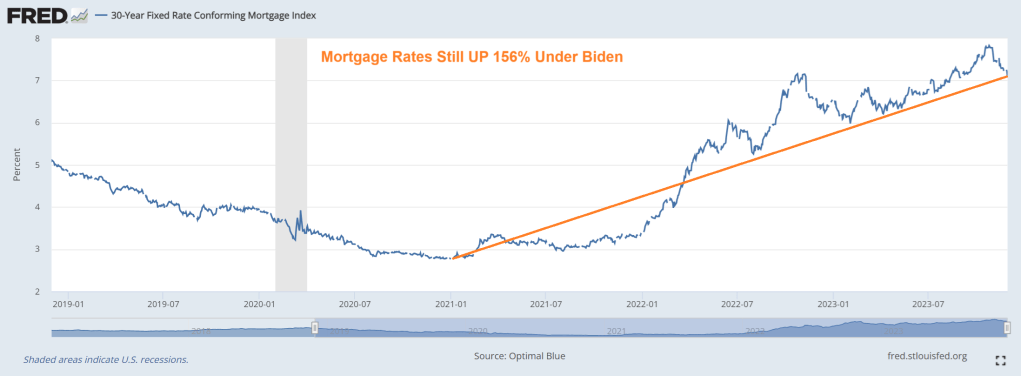

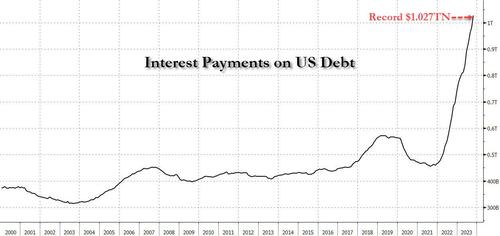

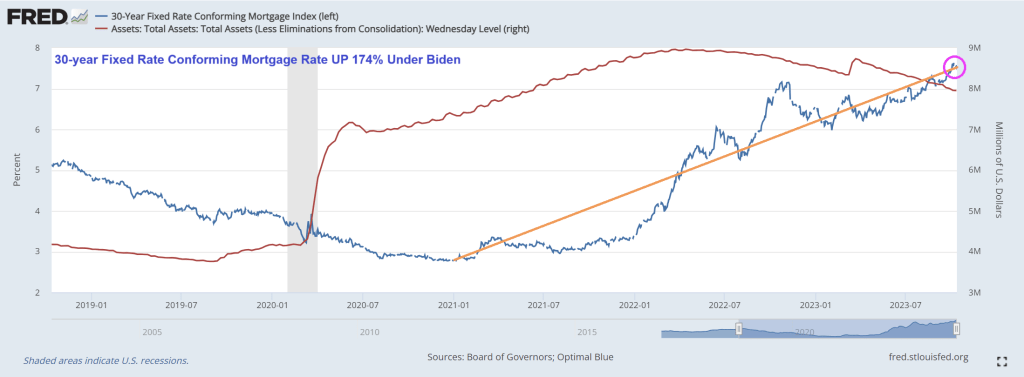

Mortgage rates have fallen recently, but are still up a staggering 156% under Biden.

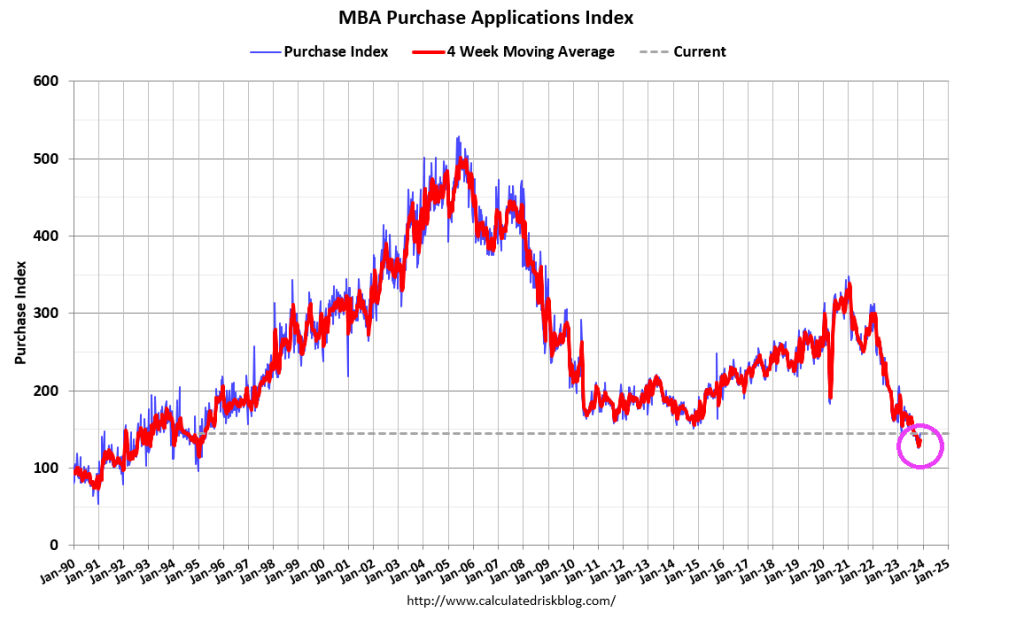

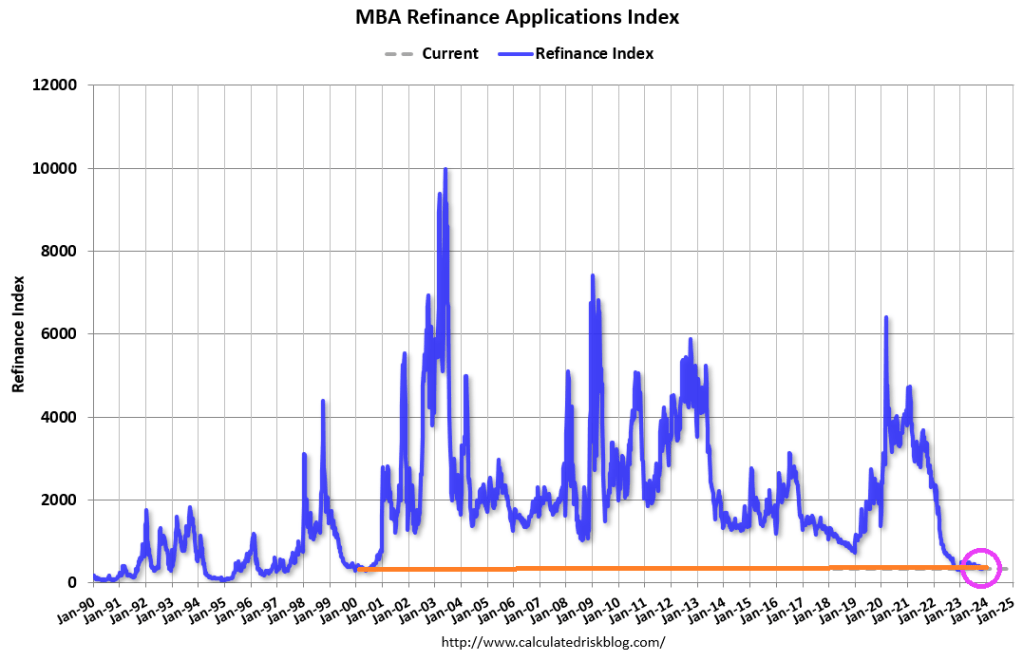

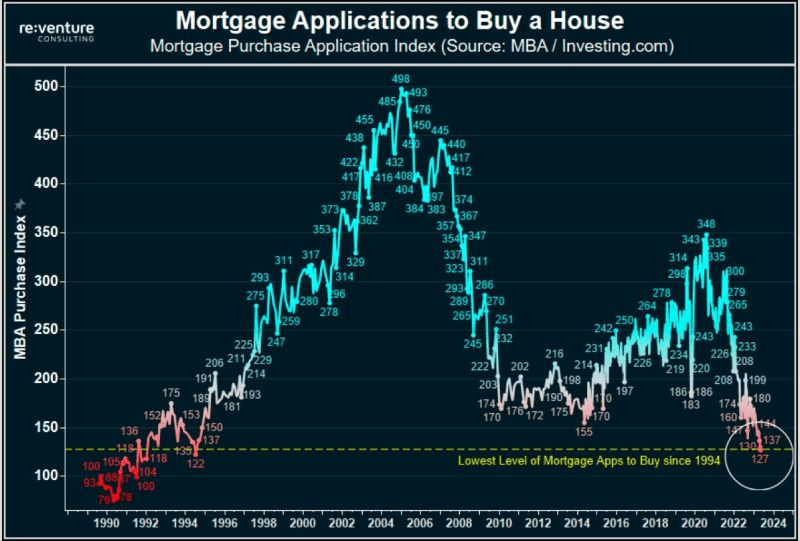

And mortgage purchase applications keep falling.

Here is The Fed keeping a close eye on the housing and mortgage market.

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.