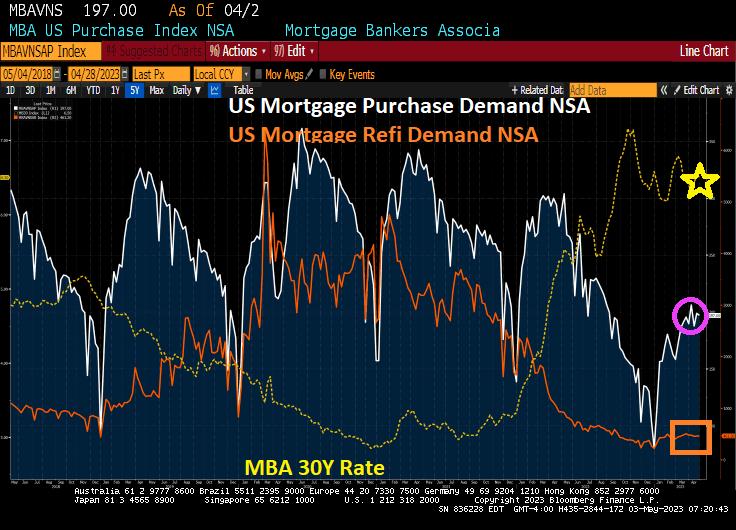

This is last data dump for mortgage demand (applications) before Biden’s idiotic woke mortgage policies go into effect (taxing those with good credit to subsidize those with lousy credit) take effect. I call this Bolshevik Biden’s Mortgage Market.

Mortgage applications decreased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 28, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 0.4 percent compared with the previous week. The Refinance Index increased 1 percent from the previous week and was 51 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 32 percent lower than the same week one year ago.

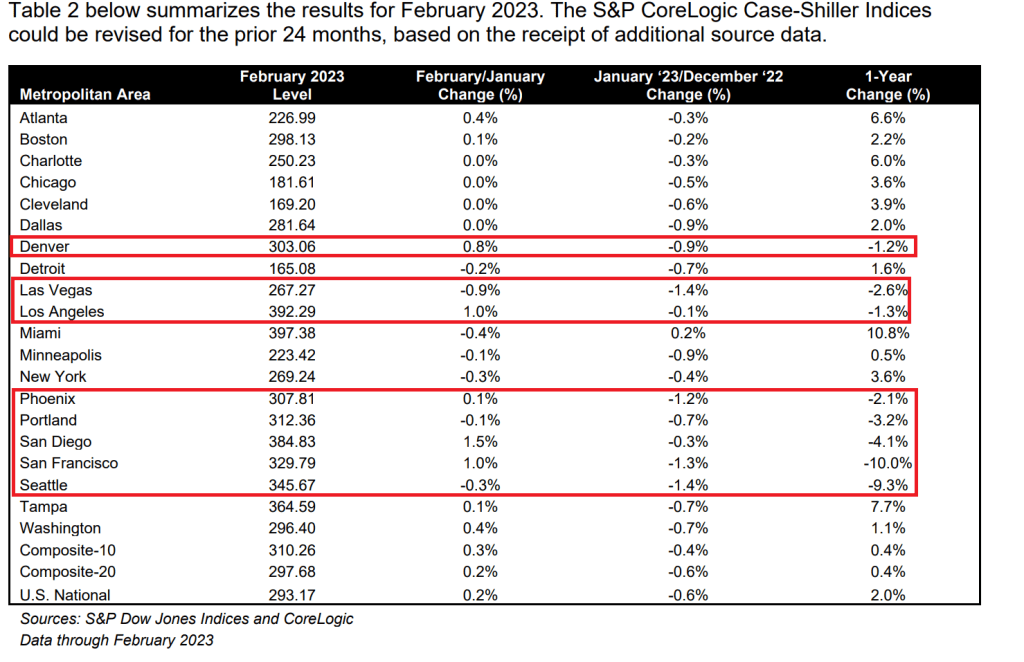

Drifting into darkness, we have the West getting battered with my old hometown of San Francisco leading the pack at -10% YoY with Seattle down -9.3% YoY.

You know things are bad out west when Cleveland, Detroit and Chicago are gaining ground in prices. And Miami was up 10.8% YoY.

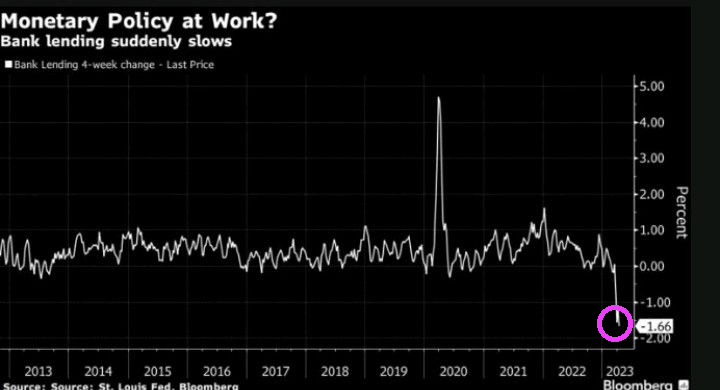

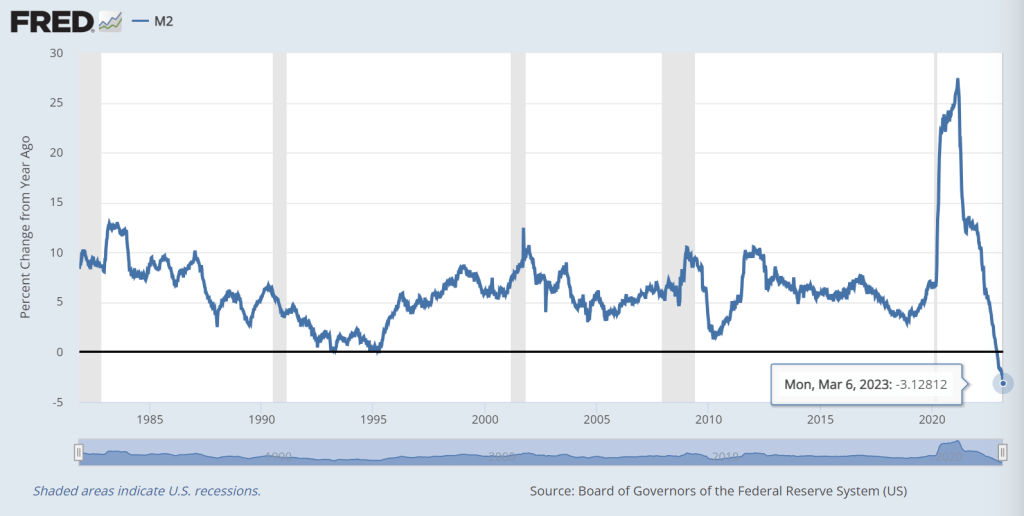

America’s mega bank, The Federal Reserve, is slowing M2 Money growth so rapidly that it looks like it is depthcharging the US economy.

Inflation in the US has been booming since 1) Biden attacked fossil fuels, 2) The Fed’s overresponse to Covid (+27.48% YoY on February 22, 2021 near the beginning of Biden’s Reign of Error). and 3) out of control Federal spending under Biden, Pelosi and Schumer.

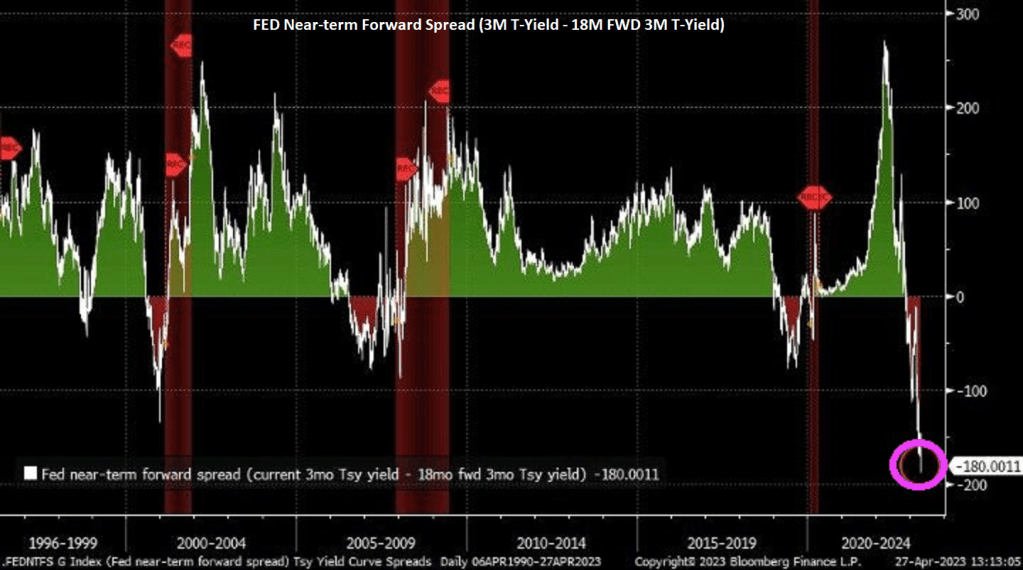

Fed Funds Futures point to two more Fed rate hikes before The Fed drop rates like a depthcharge. This depthcharge will help create a rekindling of asset bubbles.

The Taylor Rule suggets a Fed Funds Target rate of 11.77 while the current target rate is only 5%. This is called “leading from behind.”

Here is The Fed monitoring the US economy in order to decide on firing more financial torpedos!

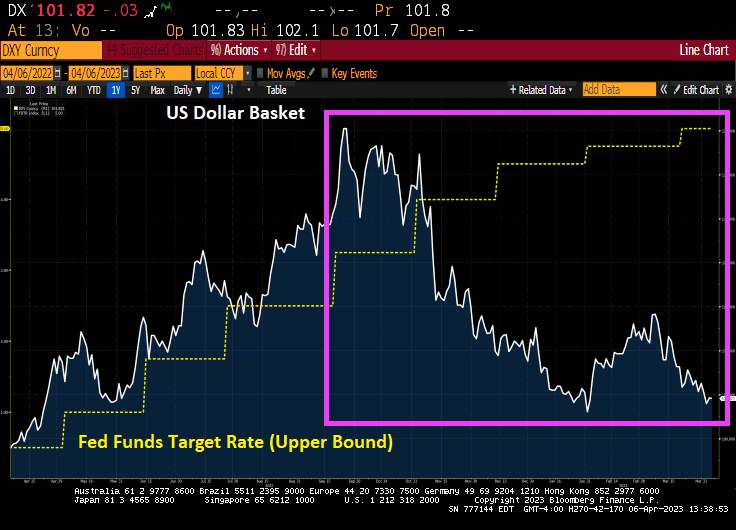

Biden, The Federal Reserve and insane Federal spending are killing King Dollar. Countries that used to use the US Dollar as reserve currency are dumping the dollar like a month old burrito.

What countries are dumping the dollar?

A lengthy list of countries are moving away from using the US dollar, which has long been the reserve currency of the world. The following countries are in the process of reducing their dependency on the dollar.

Russia

China

Iran

Brazil

Argentina

Saudi Arabia

UAE

India

The result?

Biden has vacationed 40% of the days he has been President. In his defense, he has probably needed that time to hunt down the classified documents has left strewn around his his home, vacation home, the Penn-Biden Center and Chinatown in DC.

My friend Phill Hall asked me about the state of the US housing market yesterday. My answer? “Chaos.” Why chaos? Here is why: 23 consecutive months of NEGATIVE real wage growth, declining availability of homes for sale, still expensive home prices following the Covid spending surge, and rising mortgage rates as The Fed fights inflation.

And now we have mortgage demand shrinking 4.1% from the previous week according to the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 31, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 4.1 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 4 percent compared with the previous week. The Refinance Index decreased 5 percent from the previous week and was 59 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 4 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 35 percent lower than the same week one year ago.

Throw in the declining inventory of homes for sales, and we have chaos.

Not to mention 23 consecutive months of negative REAL wage growth.

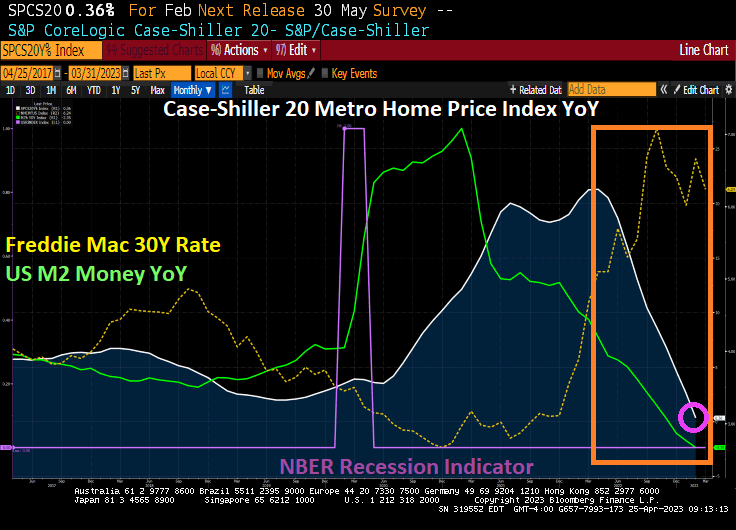

Well, at least REAL home prices are growing more slowly (-3.86% YoY) than REAL weekly wage growth -1.9% YoY). So much for housing as a hedge against inflation!

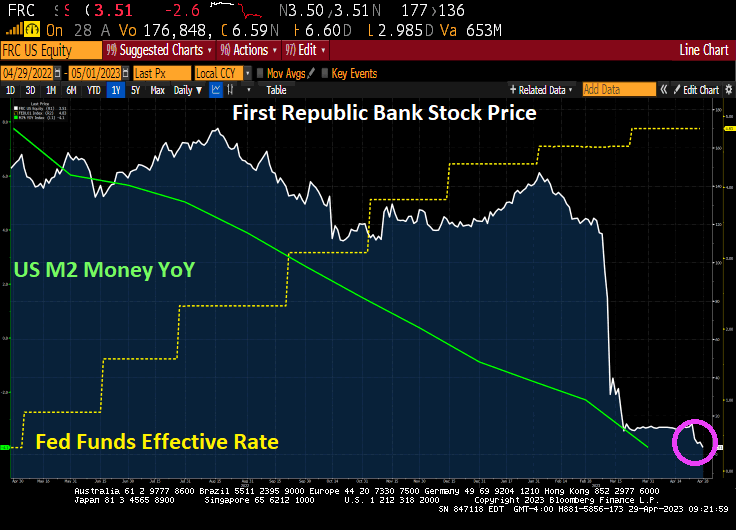

Thanks to Yellen’s catestrophic Too-Low-For-Too-Long (TLFTL) and insane Federal spending, we are seeing the aftermath of The Fed trying to fight inflation. A fire sale of failed bank assets!!

With interest rates still rising, prices retreating and credit evaporating—and a stressed-out banking system moving to shore up balance sheets—expect more fire sales of older CMBS loans and an acceleration of plunging CRE values in markets across the US.

Last month, a fire sale of CMBS loans was lit as $72B in assets from the failed Silicon Valley Bank (SVB) were sold. The SVB assets—including about $13B in real estate exposure and at least $2.6B worth of CRE loans—were sold at a discount of $16.5B, which translates into about 77 cents on the dollar, according to a report in MarketWatch.

The Federal Deposit Insurance Corp. has lit a fuse on an even larger fire sale of assets—a bonfire in terms of CRE loans—for NYC-based Signature Bank, which like SVB was a regional bank that collapsed and was taken over by regulators last month.

FDIC last week tapped Newmark to sell $60B in assets held by Signature, according to the Wall Street Journal, including nearly $36B in CMBS loans backed primarily by multifamily properties, the lion’s share of them in New York City. Since 2020, Signature initiated more than $13.4B in loans backed by NYC buildings, the most of any lender.

Experts who specialize in pricing CRE loans believe a discounted sale as large as the disposal of Signature’s assets will speed a markdown of valuations by banks who until recently have been reluctant to set off a downward spiral. The 77 cents on the dollar benchmark established by the SVB sale likely will be the top end of where prices are heading, the experts say.

“The SVB trade created a baseline for the market. To me, that’s the top end, not the bottom end, for CRE loans,” David Blatt, CEO of CapStack Partners, told MarketWatch. CapStack is a credit fund that buys CMBS loans from banks and originates short-term bridge loans and mezzanine debt.

“What everybody has been operating under is this hold-to-maturity veneer,” Blatt said, referring to banks that have continued to value loans at 100 cents on the dollar, known as par.

In the wake of the SVB asset sale, “there’s just no way these things get resolved at par,” Blatt said, adding “the write-down is kind of implied.”

“Everybody is dusting off their old playbook. There just hasn’t been [as] much distress for years,” Jack Mullen, founder of Summer Street Advisors, told Marketwatch. “People are not going to let it carry into next year. On the regulatory side, it’s coming to the front of the line. People are super-mindful about it.”

The rising cost of debt was cutting into the value of older, low-coupon loans before SVB and Signature were shut down. Now, everyone is guessing how low will prices go on CMBS loans in the wake of the fire sales of the fallen lenders’ portfolios.

A recent advisory from Cohen & Steers estimates the decline in values will likely be at least 25%. Loans associated with multifamily properties won’t be immune from the valuation hit; apartment rents declined for the fifth time in six months from January to February.

For office properties, especially in Manhattan, the decline in value will be much steeper. Older NYC office properties are facing a cliff-diving plunge of up to 70%.

CMBX S15 is plummeting like a paralyzed falcon after The Fed started raising rates.

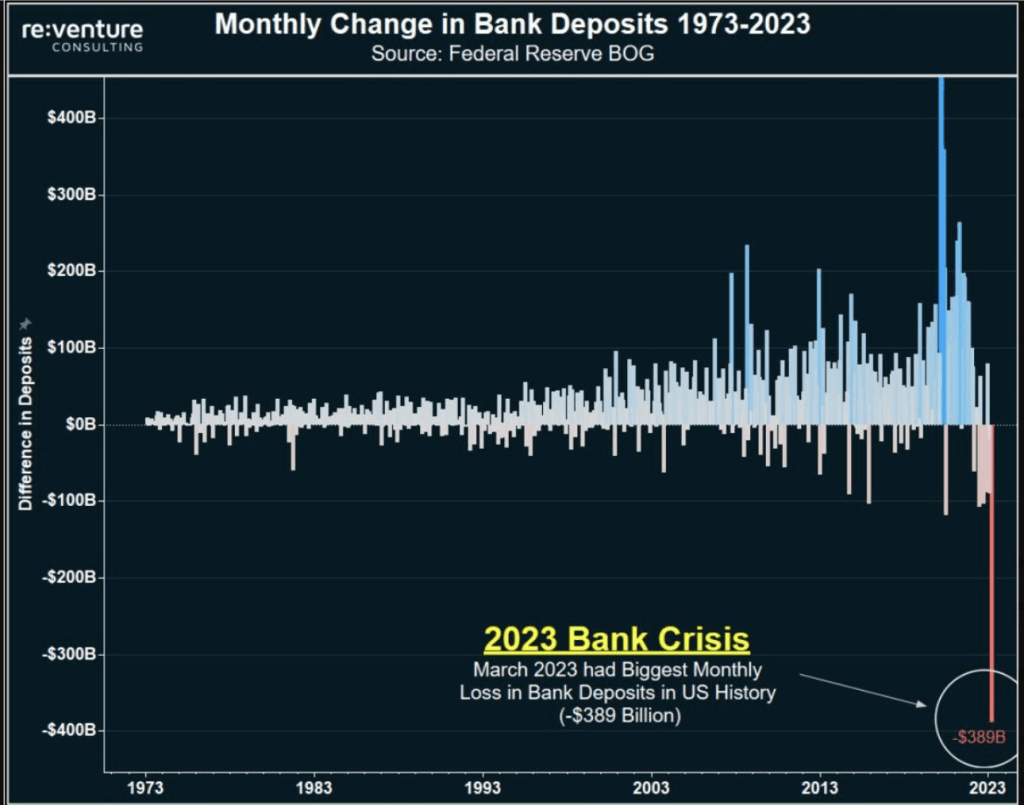

As bank deposits continue to crash and burn.

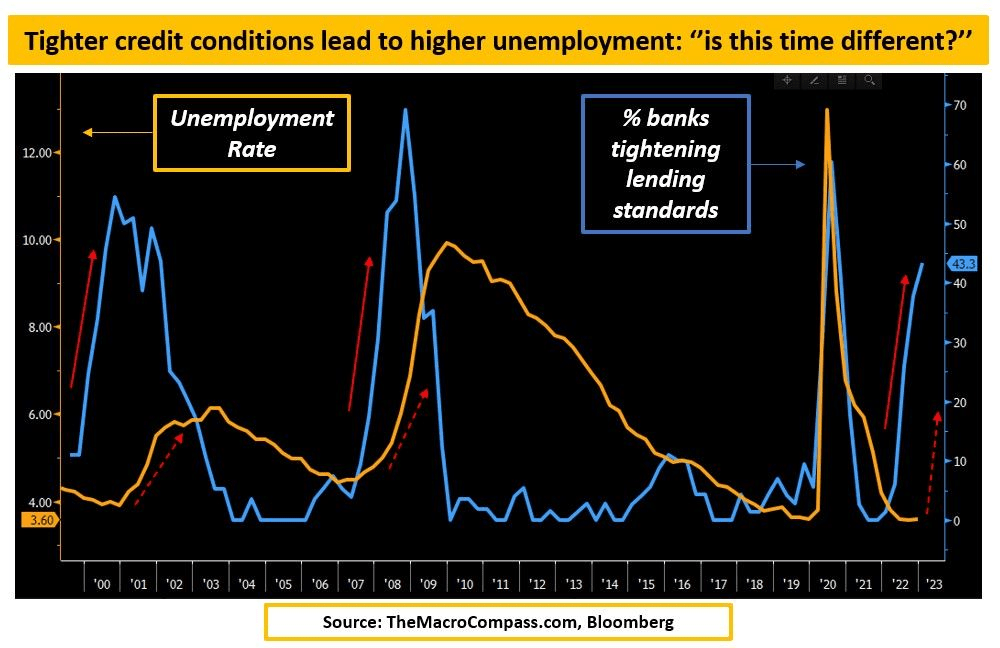

Now we have banks tightening lending standards.

So instead of The Boston Strangler, we have the DC Strangler.

To show you how Yellen/Powell’s Too Low For Too Long (TLFTL) monetary polices coupled with Biden/Pelosi/Schumer’s (add McConnell to this foul-smelling witches’ brew), Powell and The Gang (aka, The Fed) slammed on the monetary brakes. On a year-over-year basis, M2 Money growth has crashed tl -3.13%. The shocking number is The Fed Fund Effective Rate which rose over 5,000% YoY.

Actually, the US has been on a money printing spree since 1995, but it was Covid spending and monetary expansion in 2020 that crushed M2 Money Velocity (GDP/M2).

Here is Supernatural’s Leviathan monster Dick Roman handing an award to sparkless President Joe Biden. But Biden did spark massive inflation that crushed the US middle class and low wage workers.

Former Fed Chair (and current Treasury Secretary) Janet Yellen protected President Obama by raising The Fed’s target rate only once while Obama was in office. Then raised rates 8 times after Donald Trump was elected in November 2016. Well, Fed Chair Jerome Powell was following Yellen’s TLFTL (Too Low For Too Long) playbook by delaying raising rates once inflation hit 2% in March 2021. Then Powell started raising rates like crazy, unlike Yellen and her zero interest rate policies (ZIRP or ZORP for zero OUTRAGEOUS rate policy).

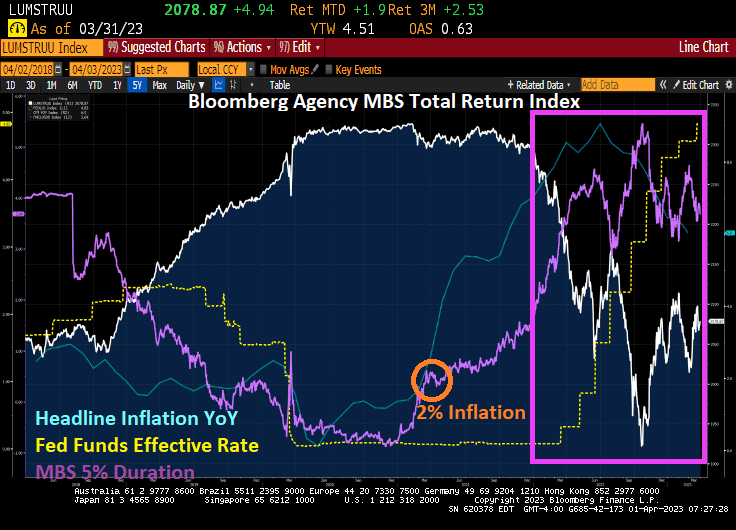

One of the safe assets that Federal regulators encouraged banks to hold was agency mortgage-backed securities. The orange circle denotes when headline inflation YoY hit 2% (March 2021). Powell and the gang waited over a year (remember, they said inflation was “transitory”). But another Democrat, Biden, was now President and Powell (like Yellen) didn’t want to rock the boat. So, Powell and the gang waited until headline inflation hit 7% before they took action. Like Yellen, Powell waited too long .

The result? Agency mortgage-backed securities (MBS) got clobbered (white line) as MBS duration (purple line) rose dramatically. Duration is the weighted-average life of MBS and is a measure of risk.

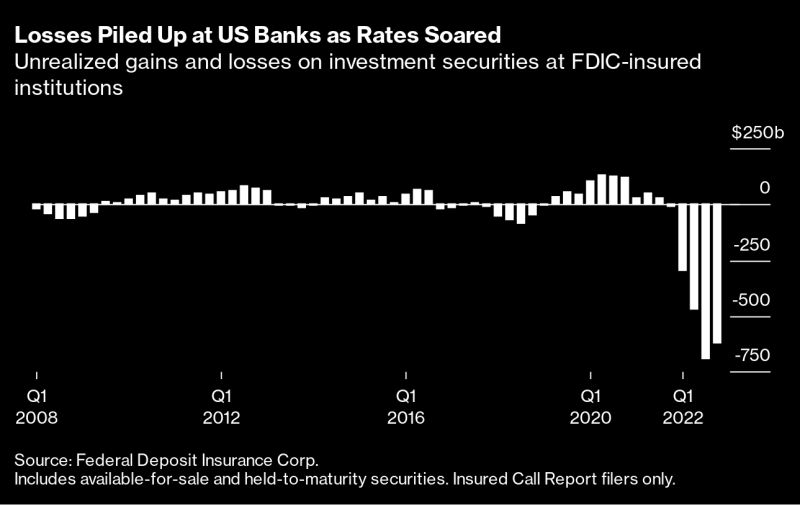

Any surprise that unrealized losses have been piling up at US banks? Not really, only some regional banks weren’t paying attention and got crushed.

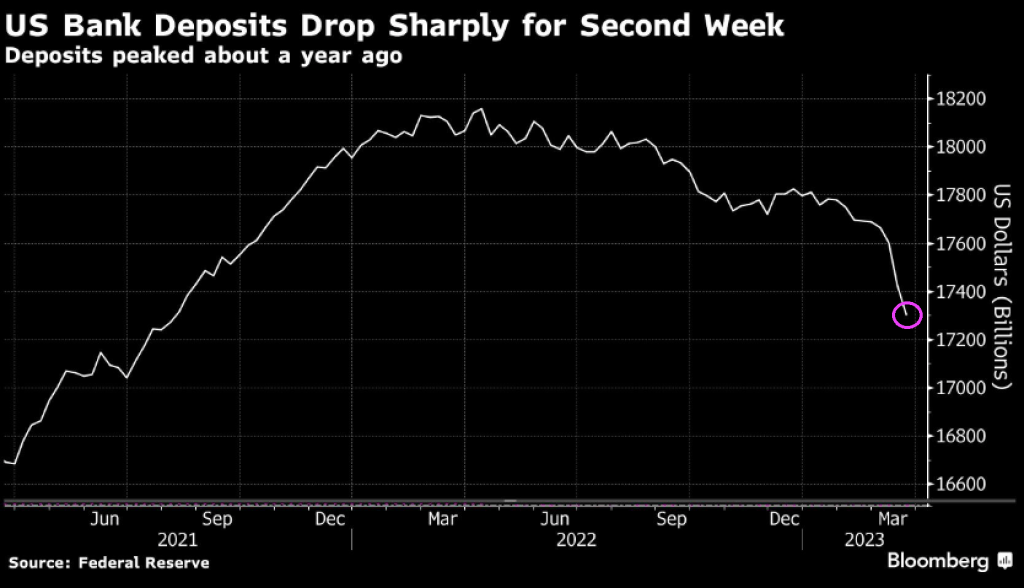

And US bank deposits are crashing despite Biden’s and Yellen’s saying the “all is well!”

Yellen and Powell praising ZORP (Zero OUTRAGEOUS rate policies).

You must be logged in to post a comment.