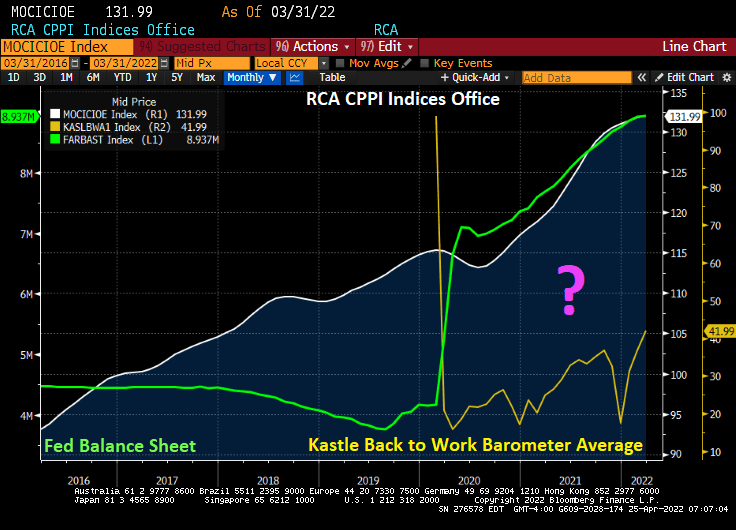

Do you want to see a magic trick? Like how governments shut down the US economy resulting in collapsing office occupancy rates while the price of office buildings rose dramatically (+16.3% since Q2 2020)?

Kastle’s “Back to work barometer” is showing that the 10 city average occupancy rate in the US is now only 42.8% as remote working has caught on. And the fear of yet another Covid mutation is keeping office occupancy below 50%.

Even Washington DC, home of Dr. Anthony Fauci, has only a 37.5% occupancy rate. Of the top 10 cities, Austin TX has the highest office occupancy rate at 62.4%.

So, the magic trick is not why America is so slow to return to the office, but why commercial office prices are rising so fast. Ah, Federal government STIMULYTPO! Aka, The Federal Reserve has been overstimulating the economy since 2008 and particularly since 2020 and Covid.

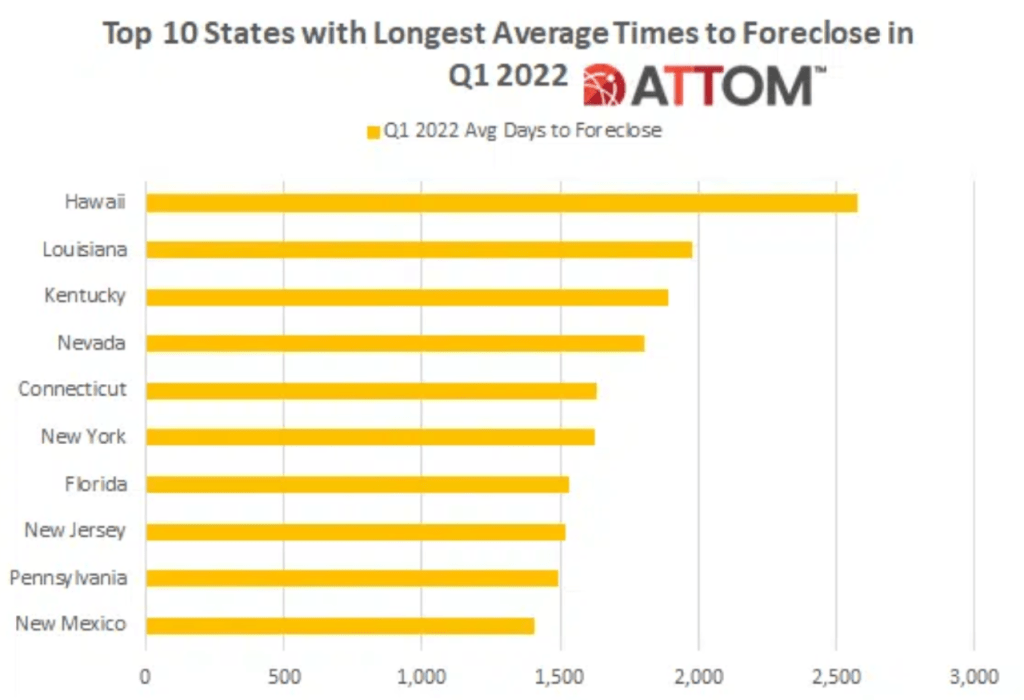

Speaking of a magic trick, here is how government’s make the average time to foreclosure up to over 7 years in Hawaii and 4.4 years in New York. In simple terms, you can buy a home in New York, never make a mortgage payment and live rent free for an average of 4.4 years.

Of course, the states with the longest average times to foreclosures at JUDICIAL foreclosures states (seen here is gray). Hawaii is now a judicial foreclosure state. That is, you must line up for a judge to hear your case.

So, the government’s magic trick is to 1) shut down local economies in fear of Covid, 2) provide excessive fiscal and monetary stimulus to combat the shutdown, 3) watch office building prices soar with stimulus as office occupancy remains below 50%.

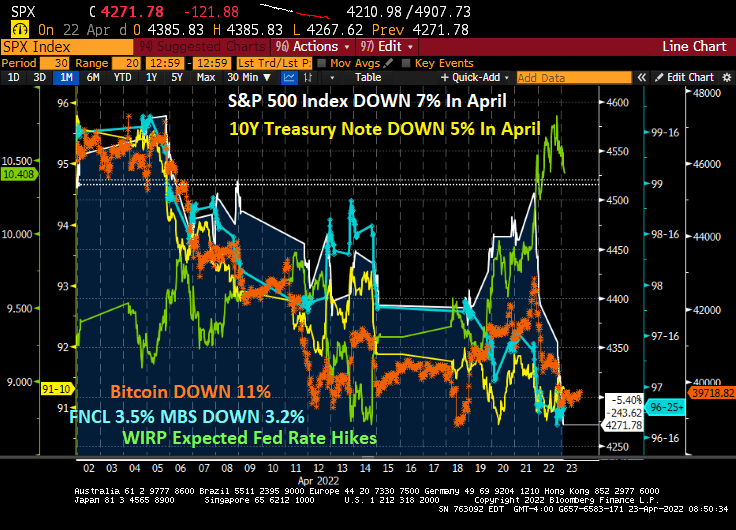

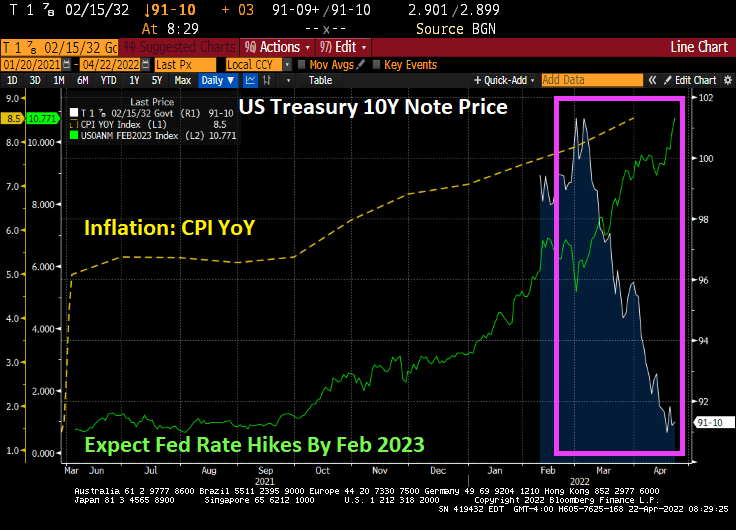

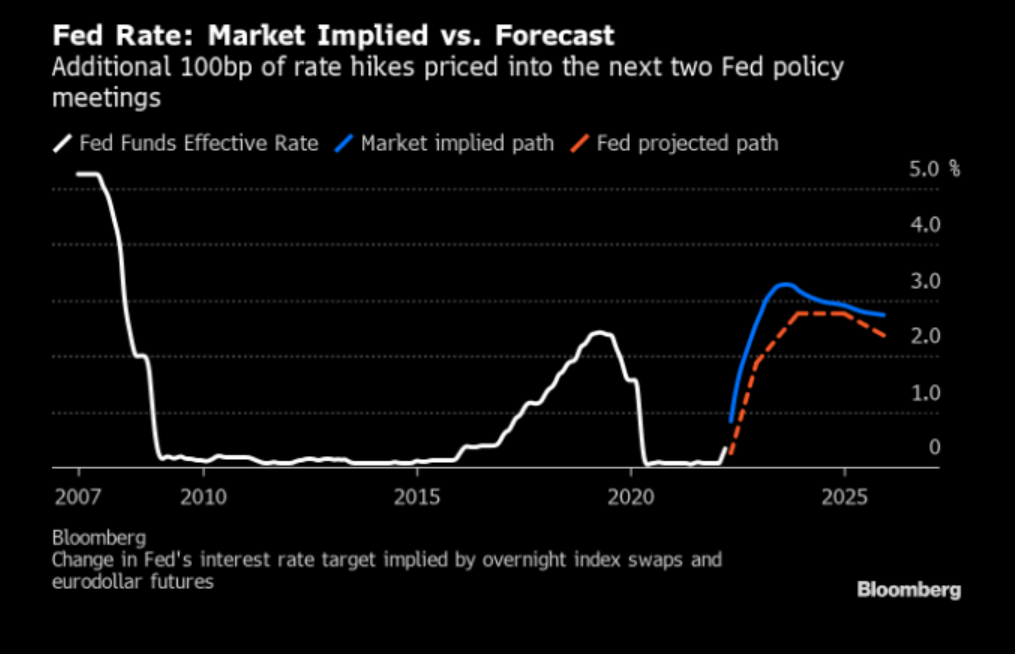

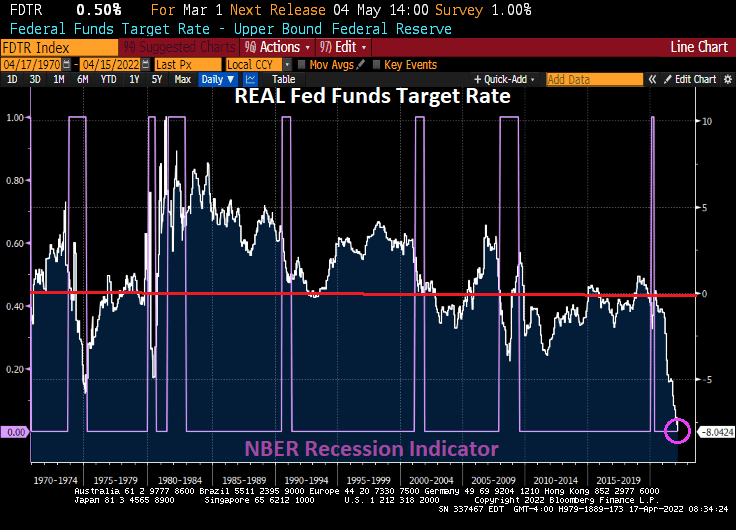

Do you want to see a magic trick? Watch The Fed try to tighten monetary easing and NOT crash the economy.

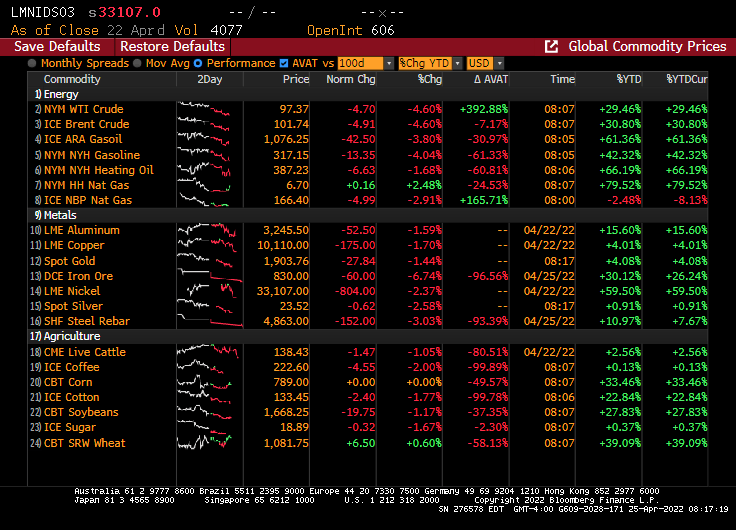

Update for 04/25/2022. 10Y Treasury yields DOWN 8.7 bps.

And commodities are tanking. WTI oil is down 5%, iron ore is down almost 7%.

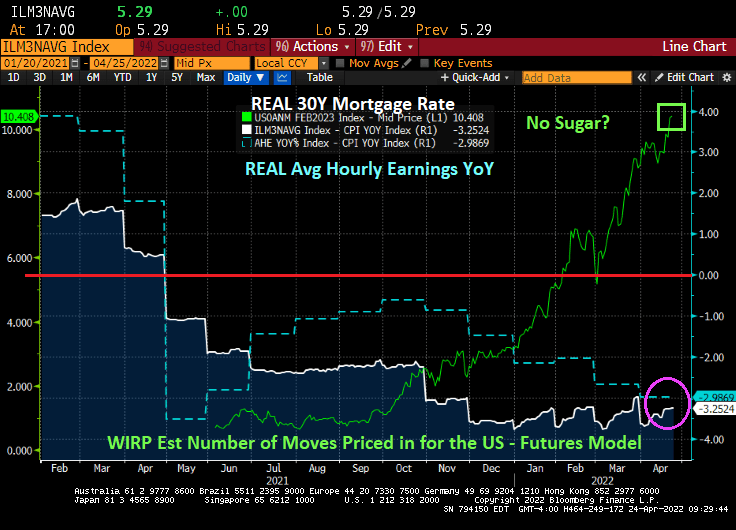

And the Dow is diving with increased expectations of Fed monetary tightening, but the expectations (green line) have been declining this morning.

You must be logged in to post a comment.