I feel sorry (sort of) for people like White House Press Secretary Karine Jean-Pierre who has to read ridiculous scripts in defense of awful Federal policies. For example, yesterday she touted Biden’s “accomplishments” of rising real disposable US income and declining gasoline prices. What? Doesn’t she read Confounded Interest?? /sarc

First, REAL disposable personal income growth for the US is NEGATIVE and has been since Biden and Congress embarked on their green energy crusade driving US inflation to its highest level in 40 years. Not exactly a great sales point for the midyear elections.

If we look at REAL average hourly earnings growth, a similar measure, we see that it is negative also. So, what on earth is Jean-Pierre talking about?

She also mentioned that gasoline prices are falling. Except that they are rising again. Apparently her talking points were from September.

Then we have diesel fuel prices, the backbone of the shipping industry, rising like crazy as Biden drains the strategic petroleum reserve.

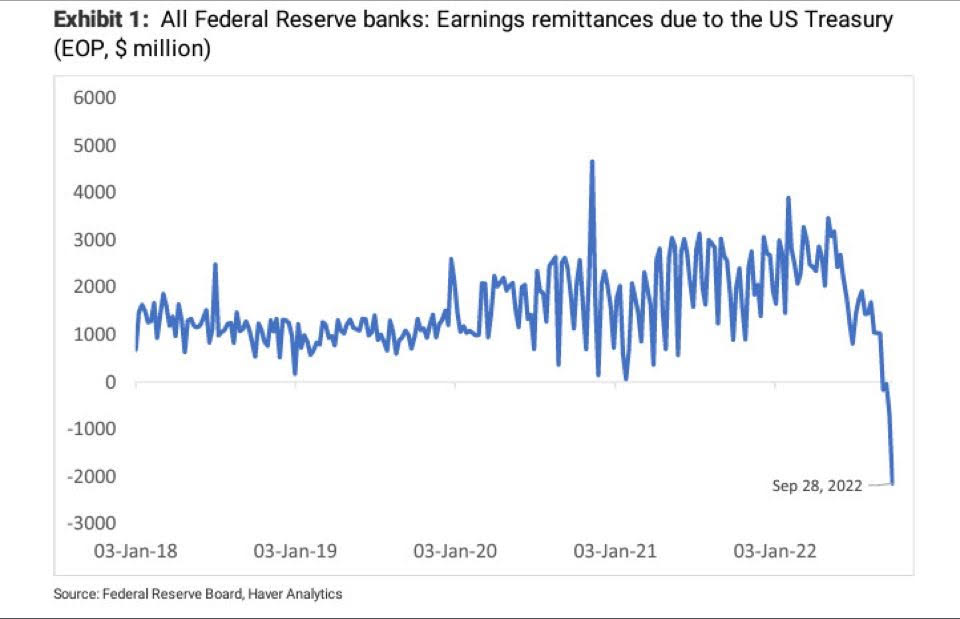

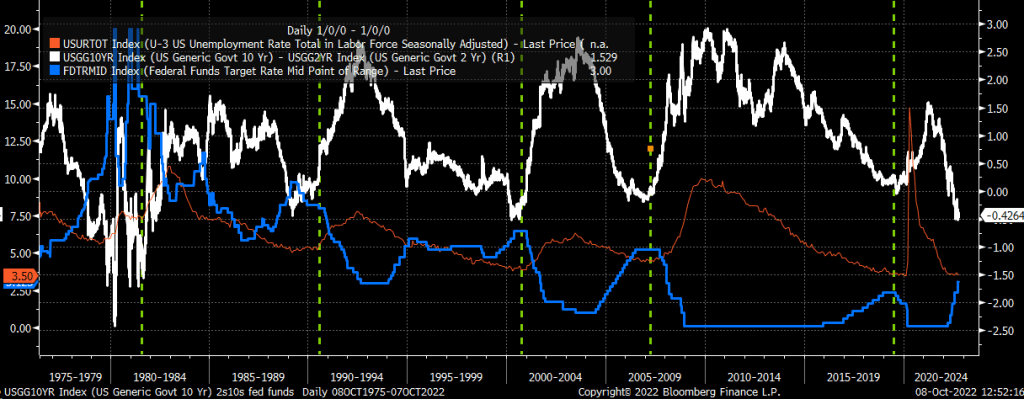

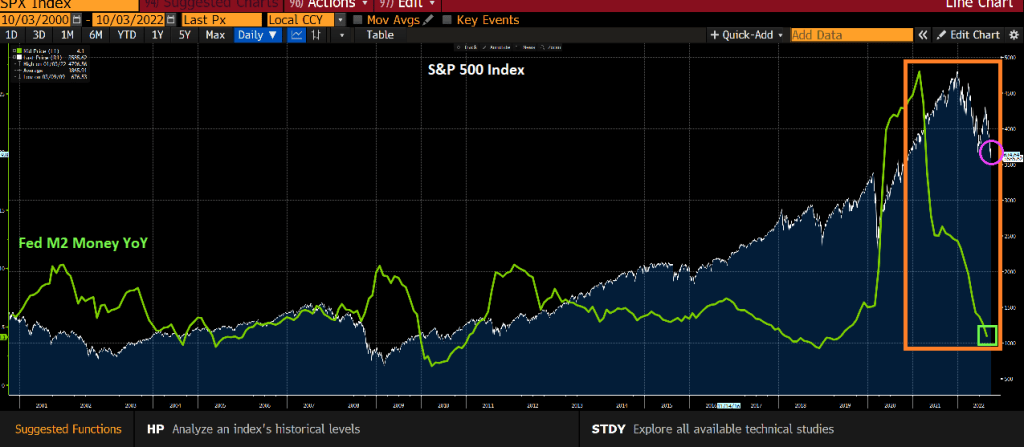

Meanwhile, The Federal Reserve is tightening their uber-loose monetary policies (thanks Bernanke, Yellen and Powell). Will The Fed pivot to help with the midterm elections OR will The Fed keep trying to extinguish inflation by raising rates and withdrawing Fed monetary stimulus?

The we have Biden speaking (incoherently) with Jake Tapper about the possibility of recession.

You must be logged in to post a comment.