Federal Reserve Governor Lael Brainard said the U.S. central bank will continue to tighten policy methodically and shrink its balance sheet at a rapid pace as soon as May.

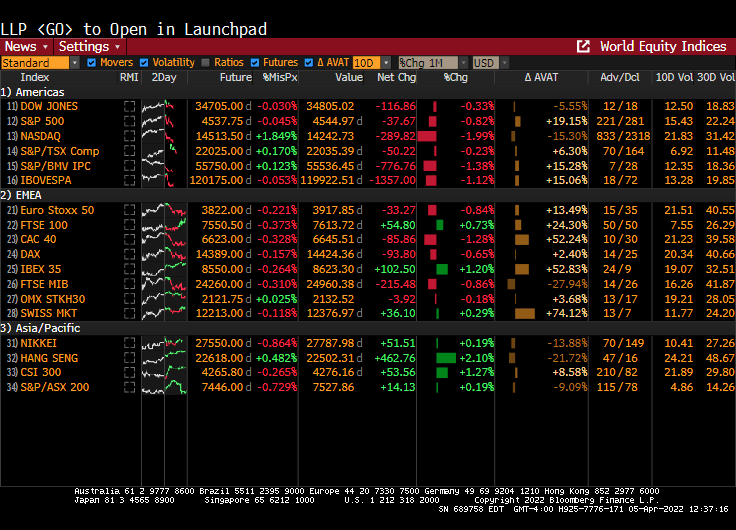

Brainard’s hawkish remarks sent bond prices crashing and 10Y bond yields up over 16 bps.

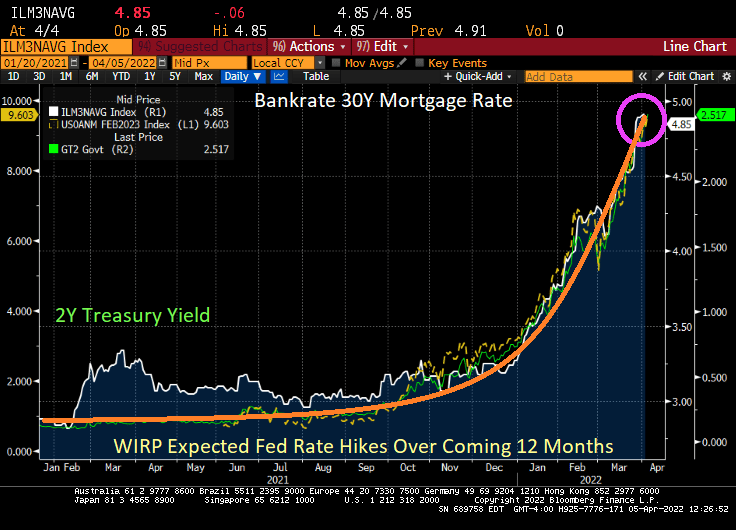

While Bankrate’s 30Y mortgage rate is down slightly today, the surge in the 10Y and 2Y Treasury yields could push mortgage rates above 5% by tomorrow,

Even Europe is feeling Brainard’s wrath. Italian 10Y sovereign yields are up almost 20 bps.

The NASDAQ index is down 300 points on Brainard’s utterance.

Gee thanks Lael from all us wanting to finance the purchase of a house.

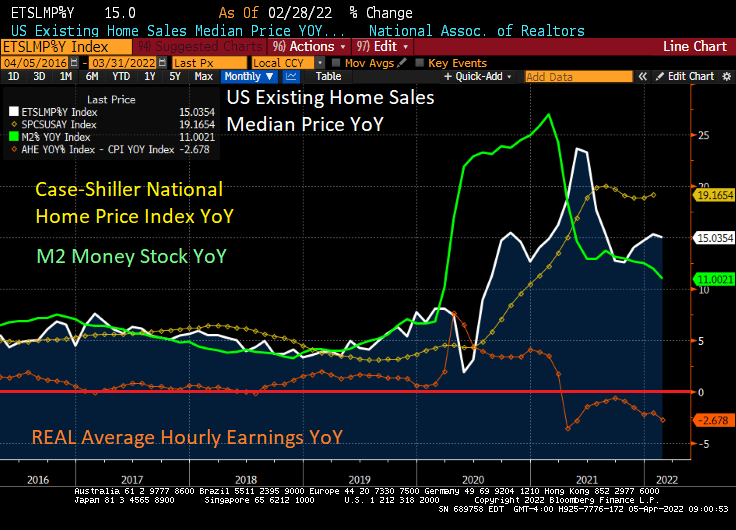

CoreLogic’s Home Price Insights revealed that home prices rose 20% YoY in February despite REAL average hourly earnings declining -2.678% YoY. THAT is euphoria! Or Stimulypto, as I like to call it.

No, The Federal Reserve still hasn’t removed its staggering monetary stimulus. Notice that M2 Money Stock is still growing at a torrid 11% pace.

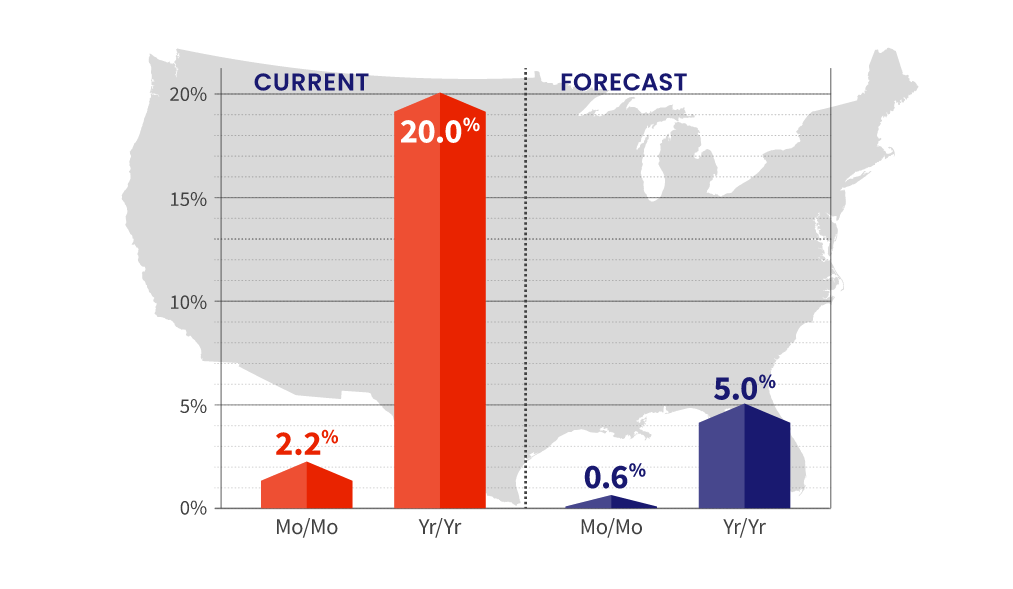

20% YoY home price growth in February? CoreLogic has increased their forecast of home price growth to 5%, likely because The Federal Reserve is imitating a sloth in removing its monetary Stimulypto.

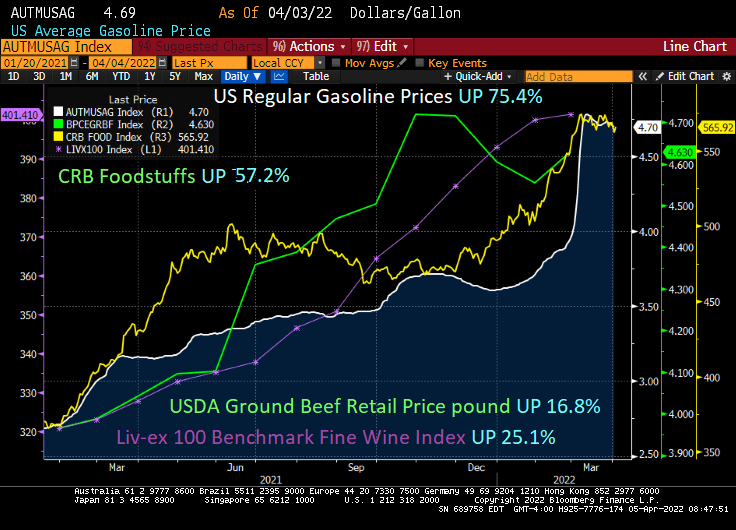

Of course, there are other assets growing at lightning speeds. US Regular gasoline prices are UP 75.4% under Biden. Foodstuffs are UP 57.2% since Biden was installed as President. At least ground beef is only up 16.8% while the fine wine index is up 25.1%.

Speaking of wine,Hitching Post II in Buellton, CA must be suffering from rising food and grape costs too (I highly recommend eating there and using their HP Magic Stuff at home). Not to mention their spectacular wines. Roast artichokes anyone??

Its official! I submitted my resignation from George Mason University effective June 1, 2022. I will miss teaching the students, past and present.

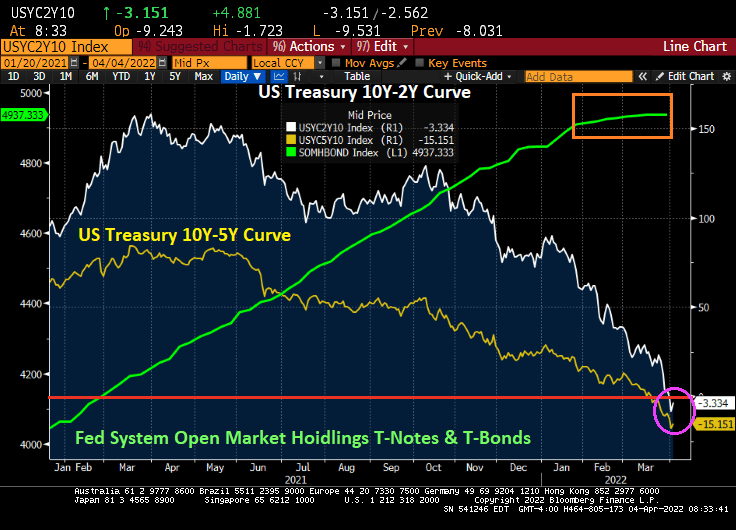

But back to the US Treasury yield curve. It remains in reversion (meaning shorter-term Treasuries have higher yields than longer-term Treasuries, usually a sign of impending recession. The Fed has actually started quantitative tightening (QT) and the growth rate of Treasury note and bond purchases has slowed to a crawl.

Meanwhile, Bankrate’s 30-year mortgage rate rose slightly to 4.91%.

Meanwhile, President Joe “The Big Guy” Biden has ordered carmakers to increase their average fuel economy to about 49 miles (78.8 kilometers) per gallon by 2026. Of course, this is intended to kill-off gasoline-powered autos and make all cars electric or hybrid like the Toyota Prius.

This can be the Democrat’s midterm election slogan: “Making living in the USA unaffordable!”

The middle-class unaffordable Ford F-150 Lightning at nearly $100,000. Thanks Joe!

Alternatively, you can buy a Buick Envision (made only in Shanghai China) with up to 24 city / 31 highway MPG. Well, kiss that baby goodbye under Biden’s new MPG mandate.

(Forbes) – Credit Suisse’s Zoltan Pozsar argues Bretton Woods II crumbled when the G7 countries seized Russia’s foreign exchange reserves. Keeping money inside financial institutions like the IMF was considered risk free. That is clearly no longer the case. Similarly, Bretton Woods I collapsed when Nixon took the US of the gold standard back in 1971 when dollars were convertible to gold at a fixed exchange rate of $35 an ounce. This led to Bretton Woods II, backed by “inside money” or the dollar, which itself is not linked to gold or any other commodity.

Now the basis of this system, which has operated for the past 50 years, is being called into question. The sanctions on Russia, which showed that reserves accumulated by central banks can simply be taken away, raised the question of “what is money?”

That question may explain why Pozsar believes a huge shift in the way the world organizes money and reserves is now underway, “creating a “Bretton Woods III backed by outside money,” (gold and other commodities). Including crude oil and bitcoin.

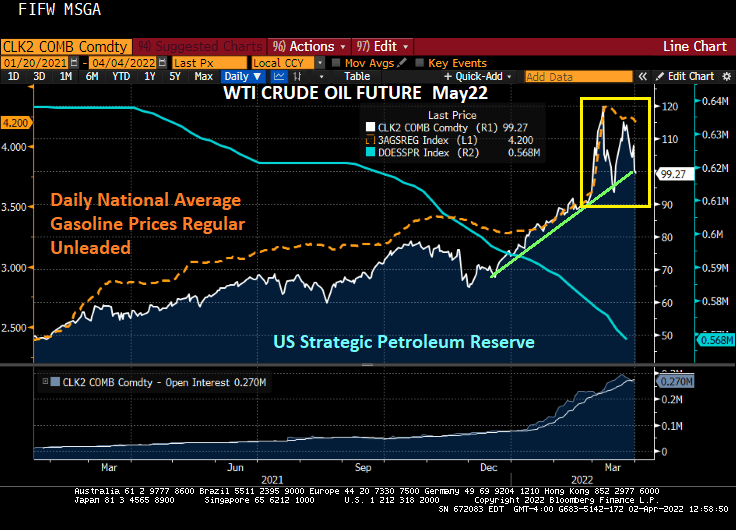

At least crude oil has fallen below $100 as Biden merrily drains the Strategic Petroleum Reserve (SPR). Gasoline prices have fallen slightly as this is being done before the midterm elections with political, not economic, intent. Once the midterms pass, will Biden continue draining the SPR until there is little left forcing the US to convert to “green energy”?

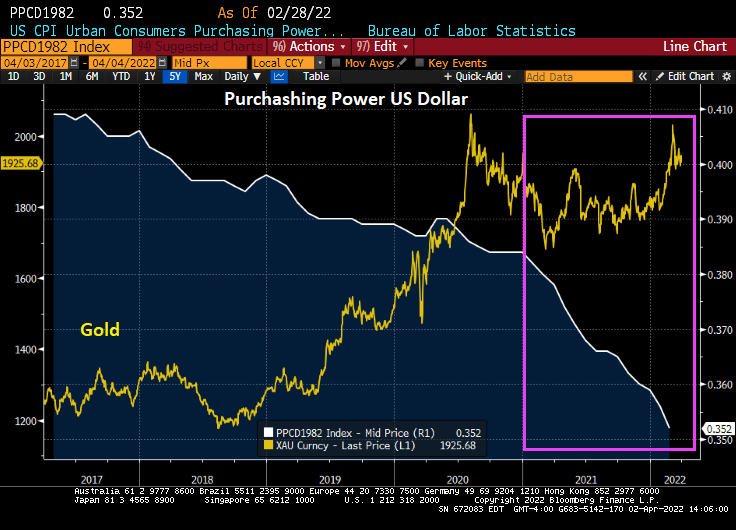

The purchasing power of the consumer dollar took a plunge under Biden as other commodities such as Bitcoin and crude oil soared.

An alternative asset, gold, have generally risen under Biden’s Reign of Error, but particularly after the Russian invasion of Ukraine.

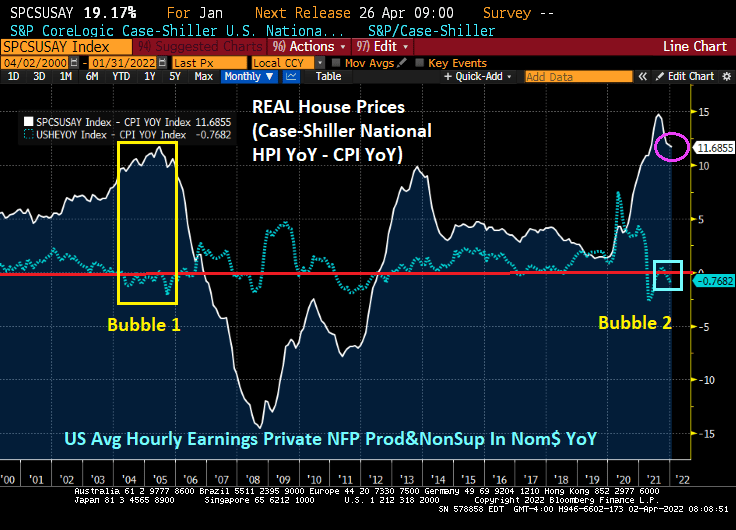

The Dallas Federal Reserve issued a warning recently that a housing bubble is brewing … after the economy drank its magic monetary elixir. We can see the housing bubble clearly (defined as the spread between REAL home price growth and REAL average hourly earnings). Notice that the current housing bubble looks similar to the infamous 2005 housing bubble. And the US is seeing several months of the spread between REAL home price growth and REAL hourly earnings be even higher than the peak of the 2005 bubble.

The Federal Reserve is starting to slow down its asset purchases, so we should see a cooling of the housing bubble. Unless, of course, The Fed changes its tune from quantitative tightening (QT) back to quantitative easing (QE) … again.

The Dallas Fed has a measure of housing “exuberance” which shows a bubble forming, but not there yet. I like the spread between real house price growth and real hourly earnings better.

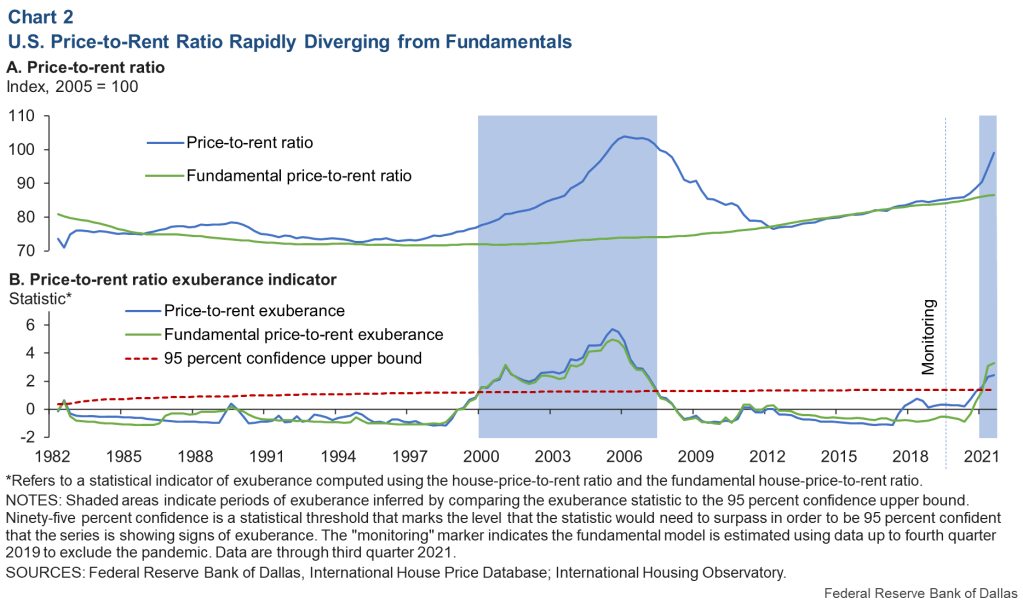

The Dallas Fed also has a price-to-rent chart also showing growing exuberance.

But if we look at the Case-Shiller National HPI YoY to US CPI Urban Consumers Owners Equivalent Rent of Residences YoY we see that the US is currently experiencing a price-to-rent ratio higher than the peak of the 2005 house price bubble. What is the culprit? The vast expansion of monetary and fiscal Stimuylpto surrounding the Covid outbreak in early 2020.

So, the Dallas Fed thinks that is a house price bubble is brewing, but it has actually been in the works since QE3 in 2013 (bubble 2), but really took off with The Fed’s stimulypto and Federal COVID spending surrounding the COVID outbreak in early 2020.

Wasting away again in Biden/Pelosiville, looking for my lost inexpensive gasoline and food. Some people say that Putin is to blame, but we know its Biden/Pelosi’s fault.

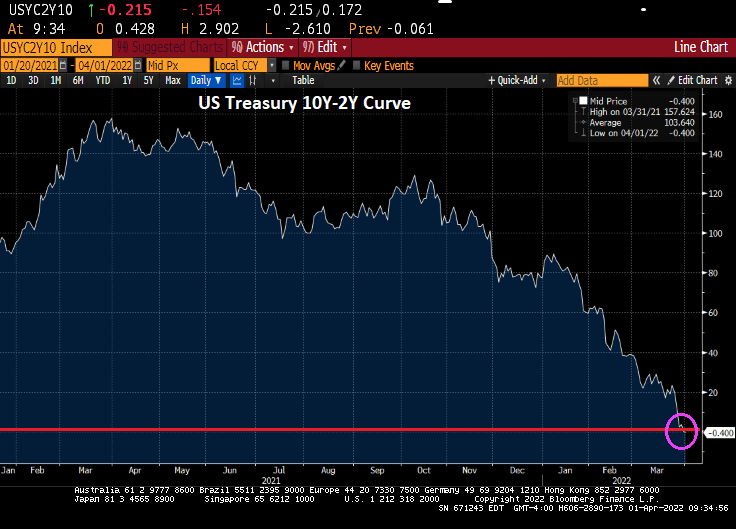

The US Treasury 10Y-2Y yield curve just inverted, generally a precursor to a recession. Called it, nothing but net!

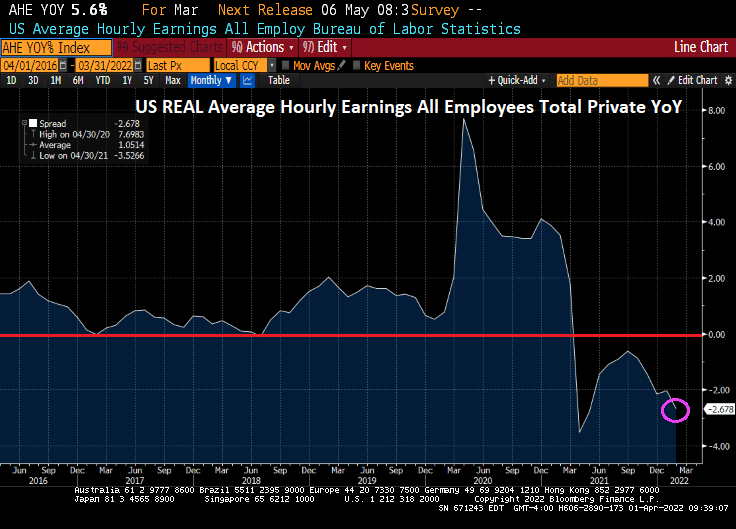

Meanwhile, today’s jobs report shows that Bidenflation is crushing America’s wage growth. While average hourly earnings grew to 5.6% YoY, we are still seeing inflation growing at 7.9% YoY meaning that inflation is reeling hurting the middle class and lower-income households.

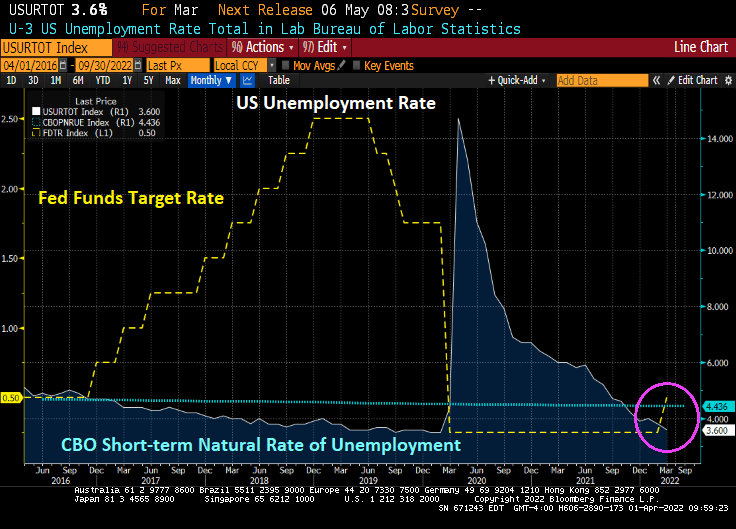

The good news is that the U-3 unemployment rate fell to 3.6%, almost back to the Trump-era unemployment rate of 3.5% prior to the Covid outbreak. And the unemployment rate remains below the CBO’s short-term natural rate of unemployment indicating that the labor market is OVERHEATED.

Today’s jobs report was pretty good, as we would expect from a recovery caused by governments shutting down economies, then reopening them. 431k jobs were added, but less than last month’s jobs added of 678k and less than the forecast 490k.

The number of people NOT in the labor force fell slightly, but it still around 100 million. The number of people holding multiple jobs to overcome Bidenflation rose to 7.5 million.

On the mortgage front, Bankrate’s 30-year mortgage rate rose to 4.90% as the 2-year Treasury rate (yellow) rises and the number of expected Fed rate hikes over the coming year is 9.26%.

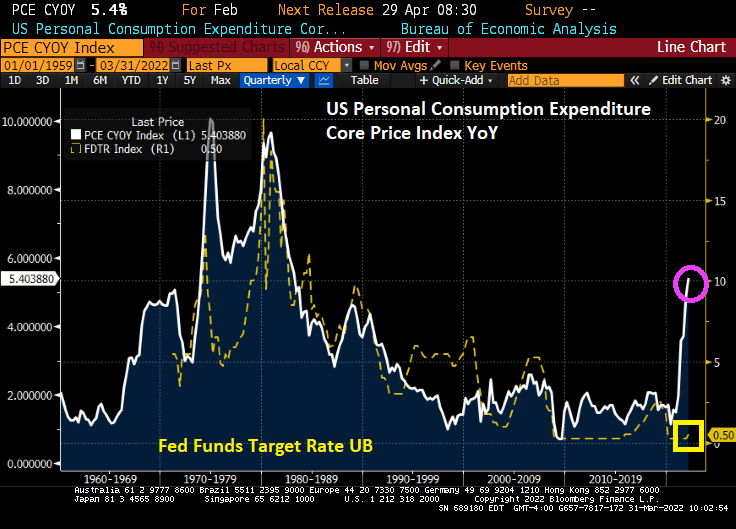

February’s Core Personal Consumption Expenditures (PCE) price YoY grew to 5.4%, the highest since 1983. The spread between the PCE Core Deflator and The Fed Funds Target Rate (upper bound)

In terms of the spread, it is the highest since the 1970s.

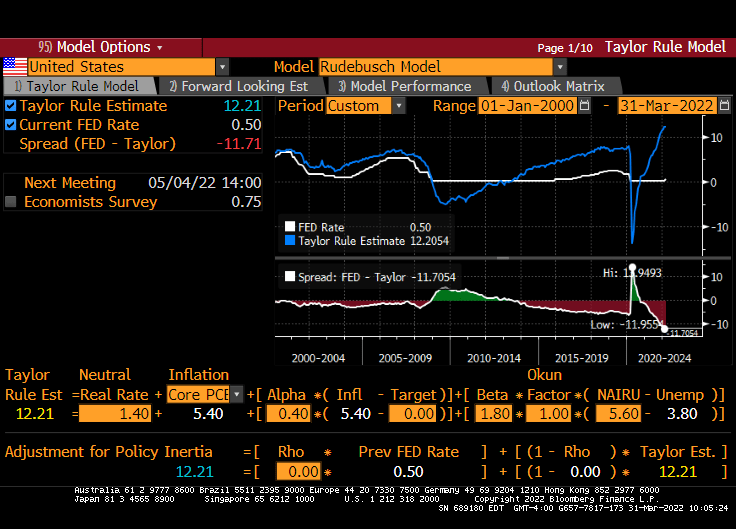

The Taylor Rule (which Jerome Powell probably thinks is the New Jersey breakfast meat “Taylor Ham”) indicates that The Fed’s target rate should be 12.21%. This is using the Rudebusch specification of the Taylor Rule.

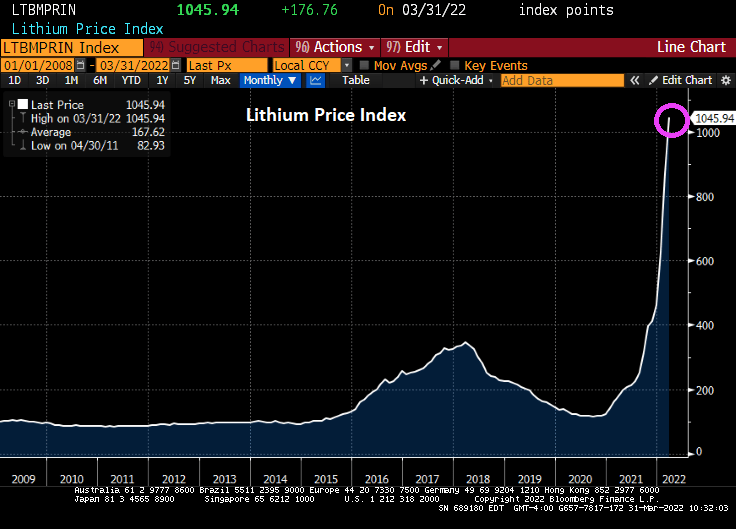

Now that the Biden Administration is going gangbusters on building electric cars, lithium prices are going through the roof.

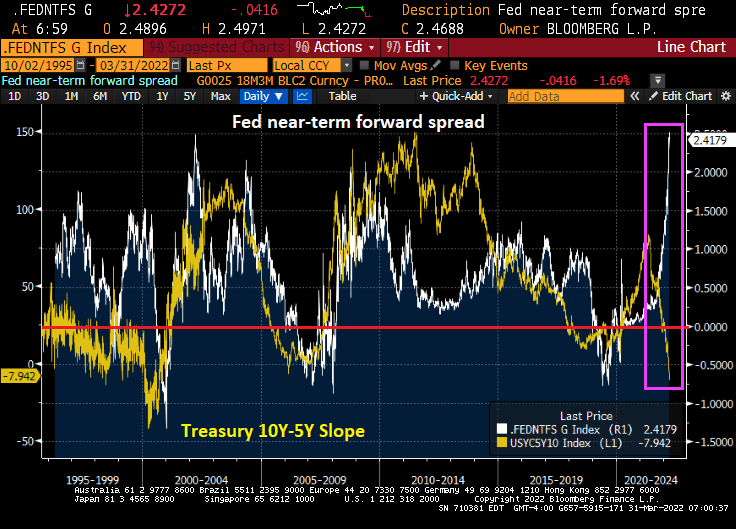

There is a massive divergence between the collapsing US Treasury 10Y-2Y yield curve and the near-term forward spread. The near-term forward spread is the difference between the implied interest rate expected on a three-month Treasury bill six quarters ahead and the current yield on a three-month Treasury bill.

As we already know, the 10Y-5Y yield curve has inverted signaling a coming recession.

This divergence between the Treasury yield curves and the near-term forward spread is occurring as US inflation hits the highest rate in 40 years.

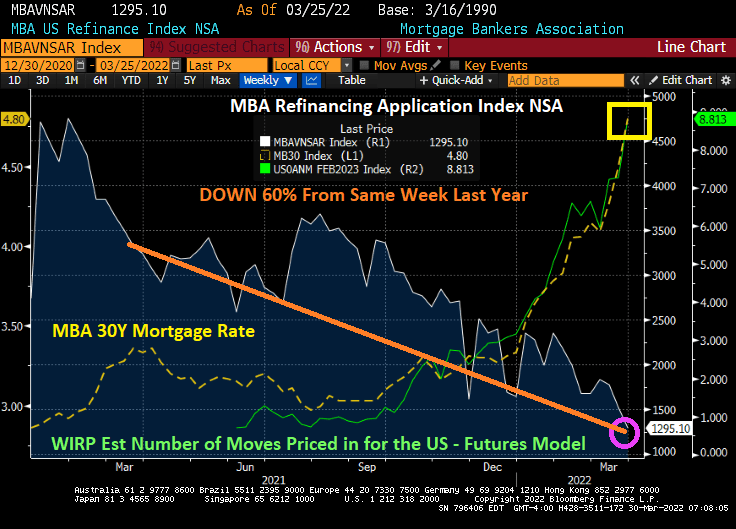

Anticipation about Federal Reserve rate hikes over the next 12 months are seeding mortgage rates soaring and mortgage refinancing applications plummeting.

Mortgage applications decreased 6.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 25, 2022.

The Refinance Index decreased 15 percent from the previous week and was 60 percent lower than the same week one year ago.

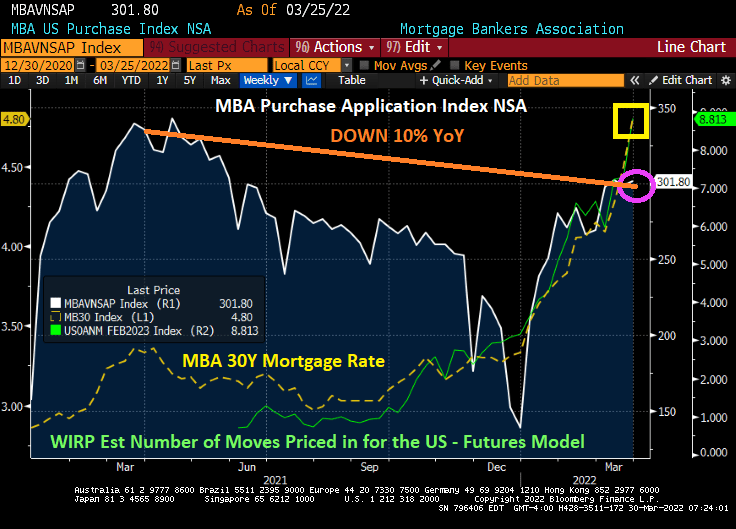

The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 1 percent compared with the previous week and was 10 percent lower than the same week one year ago.

Yes, I am surprised at the rise in mortgage purchase applications with rising mortgage rates, unless, of course, people are trying to buy ahead of Fed rate increases.

Inflation is roaring along caused by government spending and energy policies, hurting the American middle class and lower-income groups.

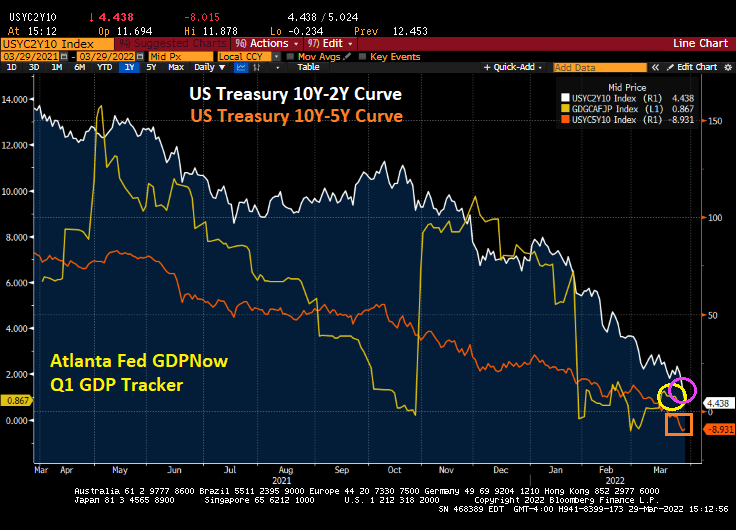

Now we see the US Treasury 10Y-2Y flattening towards zero and the10Y-5Y curve slipping deeper into inversion as Q1 GDP growth slows to 0.867.

The US yield and dollar swap curves remain steeply upward sloping, but with the dollar swap curve around 120 basis points high than the Treasury yield at the 6-month tenor.

“With inflation at a four-decade high, Fed Chair Jerome Powell has set the central bank on course for a series of interest-rate increases this year. He has stressed the toll that price increases are taking on lower-income Americans.” (No duh, Jay!)

“We understand that high inflation imposes significant hardship, especially on those least able to meet the higher costs of essentials like food, housing, and transportation,” Powell said after the Fed’s interest-rate decision this month (of only a 25 basis point increase).

Philadelphia Fed’s Patrick Harker, in a speech Tuesday, said “One of our contacts, for instance, mentioned whopping membership fee increases at his golf club, suggesting this summer may be a good time to play at your local muni instead,” said Harker, a former University of Delaware president and dean of the Wharton School of the University of Pennsylvania.

Perhaps Harker wins the Derek Zoolander award for his remarks on how the rich are impacted by inflation too.

You must be logged in to post a comment.