In August 2020, the Federal Reserve unveiled its new strategic framework. One major objective of the Fed was to address its concerns over the potential consequences for the conduct of monetary policy when the policy rate was constrained by its effective lower bound. This article concludes that there are significant flaws in the new strategy and that it encourages a more discretionary approach to monetary policy and increases the risks of policy errors. The new framework is an overly complex and asymmetric flexible average inflation targeting scheme that introduces a significant inflationary bias into policy and expands the scope for discretion by broadening the Fed’s employment mandate to “maximum inclusive employment.” In a postscript, the article describes how quickly the flaws have been revealed and urges a reset toward a more systematic and coherent strategy that is transparent and broadly understood by the public.

I attended a speech by macoeconomist Gershon Mandelker at the National Association of Realtors where he called on the Federal Reserve to follow some observable rule rather than the complex (or seat of the pants) approach to monetary policy.

With today’s inflation report (core inflation YoY of 6%) results in a Taylor Rule estimate of The Fed Funds Target Rate of 12.07%. We are struggling to reach 5% as a “terminal” Fed target rate (currently at 4% and likely to rise 50 basis points at tomorrow’s Fed meeting).

The matrix of CPI and unemployment under the Taylor Rule shows that The Fed’s target rate isn’t at even 5% for any relevant combination of core CPI (inflation) and unemployment rate.

Note that since the financial crisis the Fed’s target rate (white line) has been consistely below the Taylor Rule implied rate (blue dashed line).

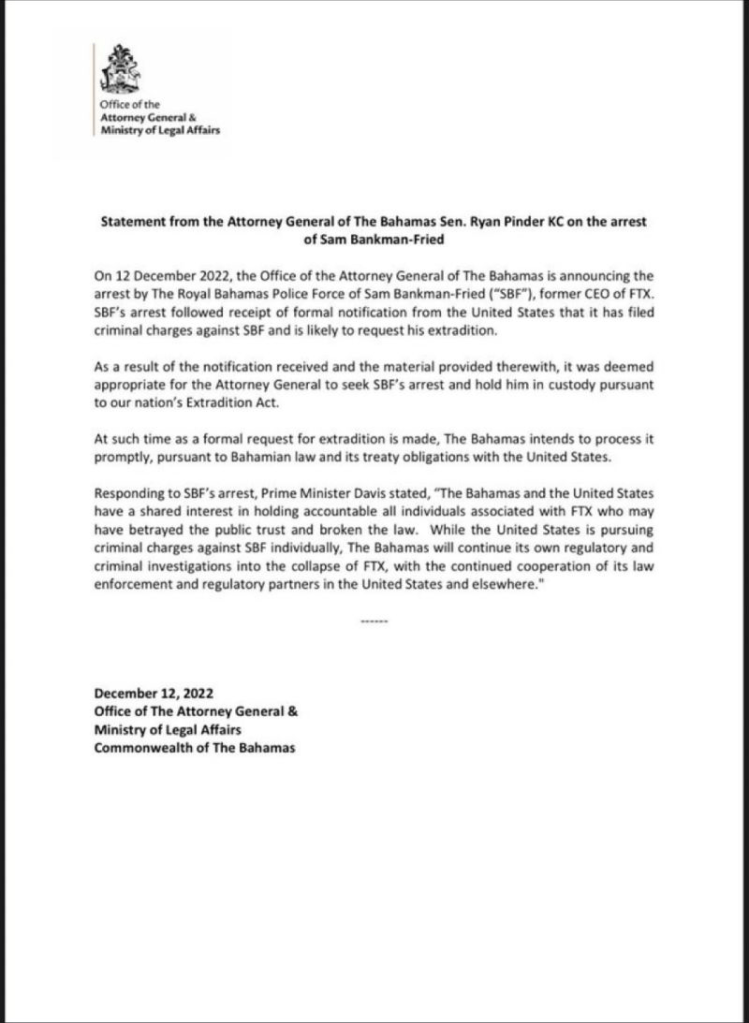

First, Sam Bankman-Fried agreed to testify in the House Financial Services Committee meeting on December 13, 2021. Then Bankman-Fried said he would testify remotely. Then ,,, he was arrested by the Bahama’s police. How convenient!

WASHINGTON, Dec 12 (Reuters) – Sam Bankman-Fried, the founder and former CEO of now-bankrupt crypto exchange FTX, on Monday said he would testify remotely at Tuesday’s U.S. House Financial Services Committee hearing to examine the collapse of the company.

FTX filed for U.S. bankruptcy protection last month and Bankman-Fried resigned as chief executive, triggering a wave of public demands for greater regulation of the cryptocurrency industry.

That might be kind of difficult, since Sam Bankman-Fried has been arrested in the Bahamas.

Perhaps, The SEC Gary Genslar will testify as to why he met with SBF and gave him the green light for his trading? And why did Genslar erase Hillary Clinton from his schedule after meeting with her? And why was Genslar meeting with Hillary in the first place since she is now just an American cititzen??

Will SBF be extricated by tomorrow morning hearing time?

Central bankers won’t ride to the rescue when growth slows in this new regime, contrary to what investors have come to expect. They are deliberately causing recessions by overtightening policy to try to rein in inflation. That makes recession foretold. We see central banks eventually backing off from rate hikes as the economic damage becomes reality. We expect inflation to cool but stay persistently higher than central bank targets of 2%.

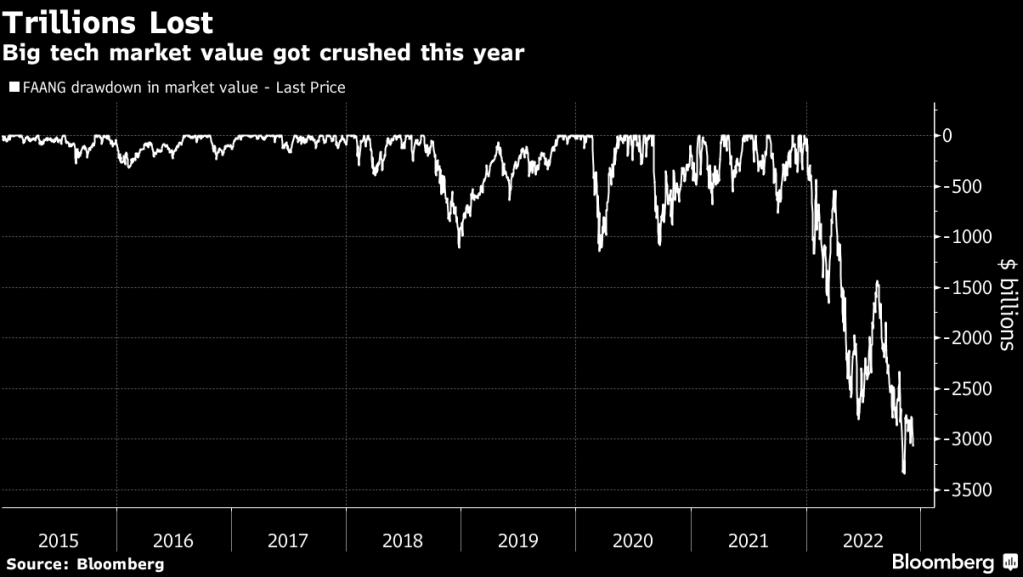

For some investors, this year’s rout in high-flying technology stocks is more than a bear market: It’s the end of an era for a handful of giant companies such as Facebook parent Meta Platforms Inc. and Amazon.com Inc.

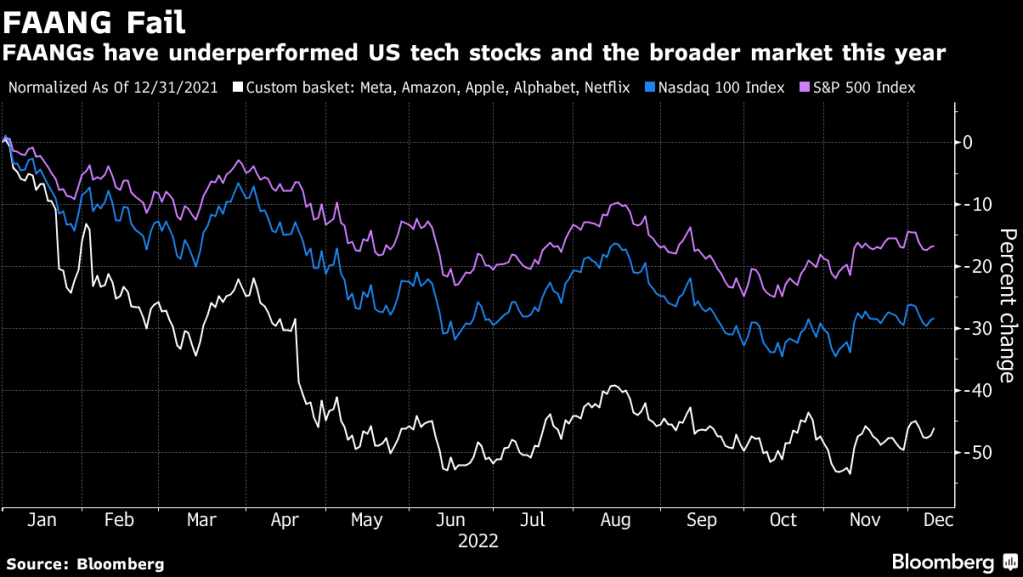

Those companies — known along with Apple Inc., Netflix Inc. and Google parent Alphabet Inc. as the FAANGs — led the move to a digital world and helped power a 13-year bull run. And FAANG drawdown have reached over $3 trillion.

FAANGs (Meta, Amazon, Apple, Alphabet, Netflix) are getting clobbered in 2022.

Typically, when The Fed prints too much money, such as 10% or higher (red line), inflation follows. Particularly when The Fed prints at 25% YoY in Q4 2020, it was followed by the highest inflation rate in 40 years. But if M2 Money continues to slow, inflation will likely slow, but not to The Fed’s target of 2%.

Despite what Minneapolis Fed’s Neal Kashkari said about The Fed having infinite printing resourses, The Fed is going to fight inflation THAT THEY HELPED CAUSE. Biden’s energy policies (did you see that Elon Musk has a car that uses plentiful hydrogen?), and excessive Federal spending by Biden/Pelosi/Schumer, are culprits in creating the supply chain problems facing America. BUT after the 25% surge in M2 Money in 2020 and 2021, we saw M2 Money VELOCITY crash and burn to its lowest level in history. Which means the “bang for the buck” for printing more money is negligible.

Of course, big tech firms got caught influencing the 2020 Presidential election (see Musk’s release of Twitter files) and engaged in restriction of the 1st Amendment (Freedom of Speech). How much will that impact FAANG stocks going foward?

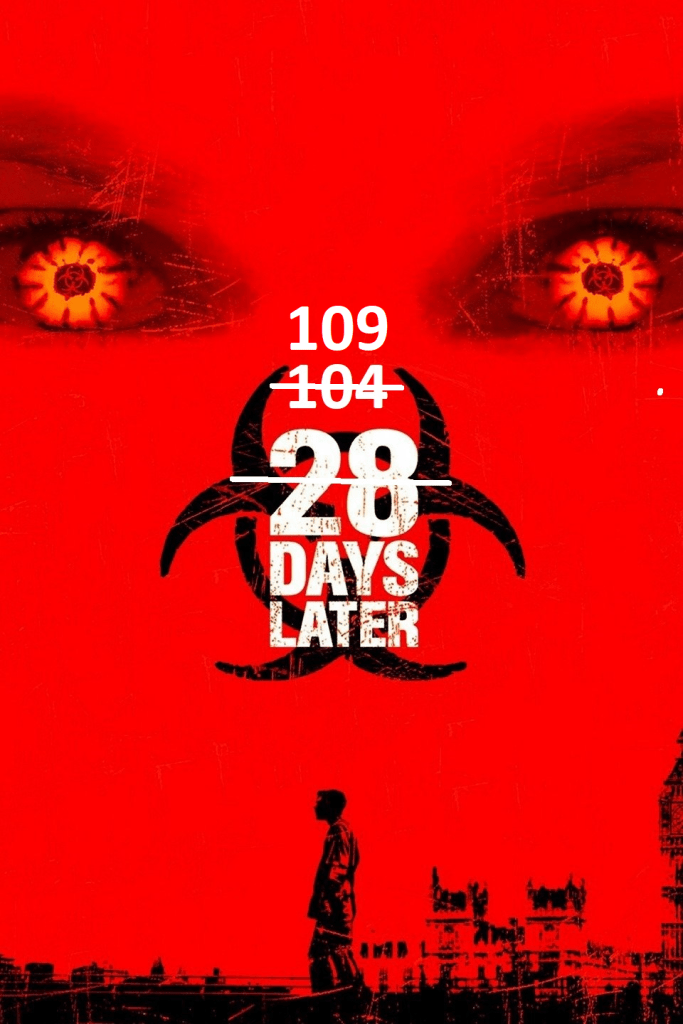

And yes, the US Treasury yield curve is inverted pointing to a recession in 2023.

And yes, apparently Biden was complicit in the Twitter fiasco.

The Federal Reserve is removing the massive punch bowl from the US economy and markets. And with the rising US mortgage rates, we got crashing buying conditions for housing.

The UMich consumer survey for buying conditions for house rose slightly in December to 36, well below 100 (the baseline).

Unlike Archie Bell and the Drells, this tighten-up is about The Federal Reserve tightening-up its monetary policy.

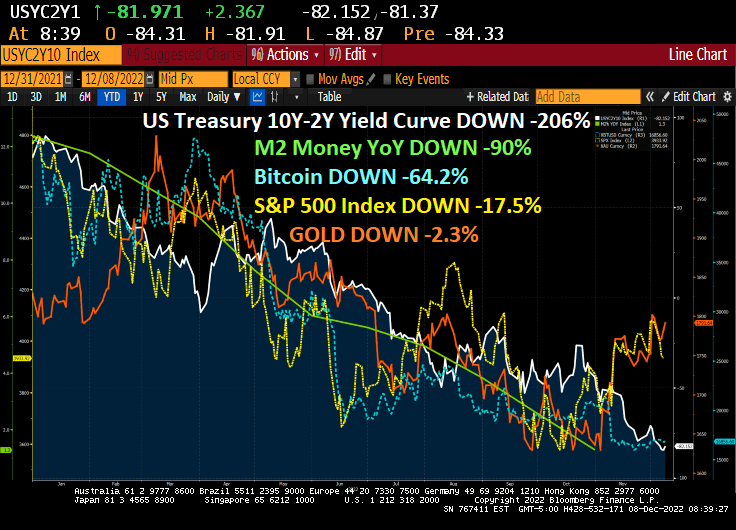

On December 31, 2021, the US Treasury yield curve (10Y-2Y) stood at +77.4 basis points, generally a good omen.

Then markets woke up. And not in a woke way.

As The Fed tightens to tamp down on inflation in 2022, we are seeing a pattern. The US Treasury 10Y=2Y yield curve has sunk to -82 basis points, a -206% decline.

In addition to the inversion of the US Treasury yield curve we have witnessed M2 Money growth declining -90%, the S&P 50) index down -17.5%, Bitcoin down -64.2% and gold down only -2.3%.

But we now have to worry about Project Cedar, a seemingly innocent project to replace the US Dollar. A new digital currency would allow Washington DC to monitor your purchases and behavior. And perhaps create a Social Credit Score like in China measuring how well you conform to Biden’s notion of a utopian, green society.

And the US yield curve has been inverted for 109 straight days.

The Fed has signaled the terminal rate will likely be around 5% — we think an upper bound of 5% — reached in early 2023. To get there, the central bank will likely raise rates by 50 basis points at its December 2022 meeting, followed by two more 25-bp hikes in 2023. We then see it holding at 5% throughout the year. Markets have priced in a similar amount of tightening.

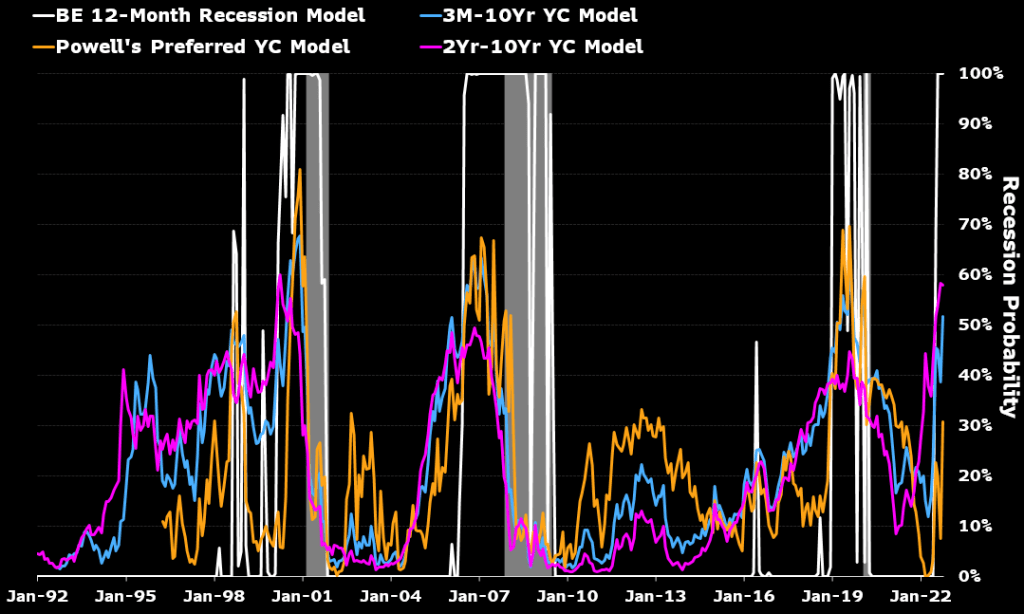

Controlling inflation comes at a cost to growth. Yield curves have inverted. A Bloomberg Economics model shows a 100% probability of recession starting by August 2023. Take that — like all model forecasts — with a grain of salt. But the basic view that aggressive Fed tightening will very likely tip the economy into a downturn is correct.

While various measures of impending US recession show a good chance of a 2023 recession, Powell’s preferred measure of the yield curve shows only a 30% chance.

What Might the Recession Look Like?

We project a 0.9% GDP contraction in 2H 2023, driven by an investment downturn as firms pare inventories amid a downshift in consumption. Residential investment will also contract with real interest rates likely to rise steadily throughout 2023 as nominal rates stay high and inflation moderates.

An Inventory-Led Downturn

Resilient consumption should help put a floor under demand.

Households have enough of a cash buffer — extra savings built up over the course of the pandemic, rising COLAs for Social Security recipients, ongoing state and local government stimulus and solid 2022 wage income growth — to sustain consumption during the recession. Our base case is for real spending to grow at a quarterly annualized pace of about 0.5% in 2023, with strength concentrated in services.

By one measure, households may still have $1.3 trillion in the coffers, based on flows within the personal income report through September. At the current rate of drawdown, that’s enough to last around 15 months, or through the end of 2023. Funds may dry up faster as job losses mount and the unemployed fall back on their savings.

$1.3 Trillion Extra Savings to Keep Spending Positive

The labor market remained exceptionally tight into the end of 2022. We expect it to soften significantly next year, with the unemployment rate rising to 4.5% by the end of 2023. The pace of hiring will slow markedly as support from catch-up hiring dissipates and the effects of restrictive monetary policy settle in. We estimate only 20%-30% of total employment is still in sectors experiencing labor shortages, implying demand for labor is falling fast.

Avoiding a Hard Landing Depends on Inflation, Fed

Extreme circumstances — the pandemic, Russia’s invasion of Ukraine — have made a recession more likely than not. Extreme circumstances can change, and so can policy makers’ response Whether the US can stick a soft landing depends substantially on how external conditions develop and how the Fed responds.

Not our base case, but we can envision a scenario in which the central bank opts to ease rates in 2023, boosting the chances of a soft landing.

One way that could happen is inflation falling faster than expected. Currently, our baseline is for headline CPI to drop to 3.5% and the core to 3.8% by the end of 2023. The most important assumption there is that energy prices remain flat next year from 2022.

In an alternative scenario, inflation fall faster as China maintains Covid controls and growth stumbles. A Bloomberg Economics model attributes the recent fall in oil prices entirely to a drop in demand — mainly from China. If China’s growth falls off the cliff, perhaps amid a sharp rise in Covid cases and resumed lockdowns, commodity prices could tumble sharply.

A warm winter in Europe and the US could also keep energy prices in check. Lower demand from Europe for US liquefied natural gas would help stem the increase in domestic electricity prices.

In that scenario, US energy prices could fall 20% in 2023 and headline inflation may drop to 2% by the end of the year. Lower gasoline prices would work to soften inflation expectations, easing pressure on the Fed to hold rates at higher level. A rate cut could then come in 2H 2023, raising the possibility of a soft landing.

Scenarios of CPI Inflation in 2023

The risk cuts both ways. A quick and successful pivot to reopening in China could boost oil and other commodities prices. A colder winter in Europe and the US would generate upward pressure for electricity and utility prices. Assuming China is fully open by mid-2023 — the base case for our China team — energy prices could increase by 20% in the year. In that case, headline US CPI would hit a bottom of 3.9% in midyear before surging to 5.7% by year-end.

In that scenario, the terminal fed funds rate would most likely top 5%, possibly closing 2023 near the upper end of St. Louis President James Bullard’s estimated restrictive range of 5%-7%.

Bloomberg Economics US Forecast Table

Thanks to Yellen’s legacy of too low interest rates for too long, The Fed is playing catch-up by finally raising rates.

Always behind the curve, US Senators (Warren, Marshall, Kennedy) want to get to the bottom of Silvergate’s decline and its relationship with Sam Bankman-Fried and FTX. This reminds me of the 2008 financial crisis when The Federal Reserve claimed they never saw it coming. Despite the data.

But back to crypto bank Silvergate.

Crypto bank Silvergate Capital Corp. was asked by three US Senators to release all records about transfers of funds for the collapsed FTX empire of Sam Bankman-Fried.

“Your bank’s involvement in the transfer of FTX customer funds to Alameda reveals what appears to be an egregious failure of your bank’s responsibility to monitor for and report suspicious financial activity carried out by its clients,” Senators Elizabeth Warren, Roger Marshall and John Kennedy wrote in a letter released Tuesday. “The public is owed a full accounting of the financial activities that may have led to the loss of billions in customer assets, and any role that Silvergate may have played in these losses.”

Shares of the La Jolla, California-based bank fell as much as 8%. The slide extends Silvergate’s losses on the year to more than 84% and has it trading at a fresh 52-week low. Not surprisingly, Silvergates’ stock price is closely linked to cryptocurrency Bitcoin.

The letter cite concerns about the banking services that Silvergate provided to both FTX as well as Bankman-Fried’s trading firm, Alameda Research. It says the arrangement between FTX and Alameda depended on Silvergate’s depository services and puts the bank “at the center of the improper transmission of FTX customer funds.”

“Silvergate’s failure to take adequate notice of this scheme suggests that it may have failed to implement or maintain an effective anti-money laundering program, as required under the Bank Secrecy Act,” the Senators said.

Perhaps Silvergate should be renamed Silverfish. But seriously, no US Senator or DC regulator saw the following chart?? Bitcoin and other cryptos have been clobbered in 2022 as The Fed tightens monetary policy to combat inflation.

Here is our regulator, SEC’s Gary Genslar, keeping an eye on cryto exchanges like FTX.

Maybe US Senators and DC regulators thought Silvergate is a silverfish.

As The Federal Reserve continues its assault on inflation by raising their target rate, Blackstone Inc.’s $69 billion real estate fund for wealthy individuals said it will limit redemption requests, one of the most dramatic signs of a pullback at a top profit driver for the firm and a chilling indicator for the property industry.

Blackstone Real Estate Income Trust Inc. has been facing withdrawal requests exceeding its quarterly limit, a major test for the one of the private equity firm’s most ambitious efforts to reach individual investors. The news, in a letter Thursday, sent Blackstone stock falling as much as 10%, the biggest drop since March.

You can see the problem facing commercial real estate. Since December 31, 2021, NAREIT’s all-equity REIT index has fallen -23.6% while NAREIT’s mortgage REIT index has fallen -28.6%. It looks like Blackstone’s Real Estate Income Trust has a decline coming.

If I look at NCREIF’s commercial property index, we can see that The Fed helped boost CRE values. But what will happen if and when The Fed actually shrinks its balance sheet.

I call The Fed’s attempts at cooling inflation “Fed Dead Redemption” since it resulted in redemptions from real estate funds.

You must be logged in to post a comment.