Biden/Harris will be remembered for many things, mostly BAD. Uncontrolled immigration, crime out of control, endless wars, grossly incompetent government administrators, 200k+ missing immigrant children, etc. But wreckless inflation coming from insane government spending takes the cake. And it is heating up again, with the help of The Feral Reserve. Yes, The FERAL Reserve.

Under Biden/Harris, prices are WAY up, real weekly earnings are WAY down.

For the 52nd straight month, core consumer prices rose on a MoM basis in September (+0.3% MoM – hotter than the 0.2% expected) – the strongest since March. That left Core CPI YoY up 3.3%, hotter than the 3.2% expected…

Source: Bloomberg

The headline CPI also printed hotter than expected (+0.2% MoM vs +0.1% MoM exp), with the YoY CPI up 2.4% (hotter than the 2.3% expected but lowest since Feb 2021)…

Source: Bloomberg

Core Services and Food costs surged in September…

Source: Bloomberg

Overall, headline consumer prices are up over 20% (5.1% p.a.) since the Biden-Harris admin took over, which compares to around 8% (1.97% p.a) during Trump’s first term…

Source: Bloomberg

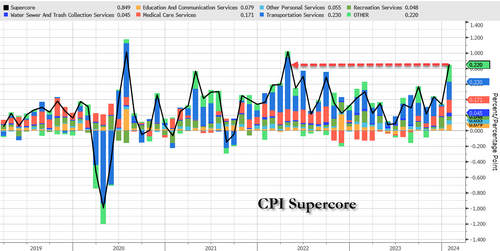

The so-called SuperCore CPI also increased on a YoY basis to +4.6%…

Source: Bloomberg

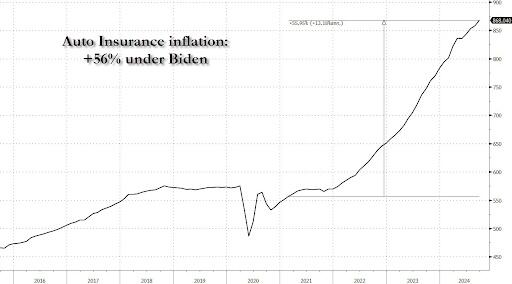

A surge in Transportation Services costs (record high auto insurance) and Medical Care Supplies lifted Super Core…

Source: Bloomberg

Why is the cost of auto insurance up 56% since Biden and Harris took over?

Source: Bloomberg

Real wages are down since the start of the Biden-Harris administration…

Source: Bloomberg

Finally, we note that money supply is resurgent once again, suggesting The Fed’s confidence in CPI’s decline may be misplaced…

Source: Bloomberg

Could we really replay the ’70s once again?

Source: Bloomberg

Will that really be Powell’s legacy? Or will the timing of this resurgence in inflation be perfectly timed to coincide with Trump’s election victory… and offer a perfect patsy for who is to blame?

Mortgage rates are rising again with Friday’s surprising jobs report. But as it just a false election report. If Rasmussen is correct, mortgage rates should FALL again.

Whenever the 10Y-2Y Treasury yield curve slope goes negative, it is following by positive slope … then recession. Like clockwork.

Following every recession since the 1970s, the 10Y-2Y Treasury yield curve slope has risen, then declined. This time around, the 10Y-2Y Treasury curve has remained negatively-slope long than usual suggesting a larger than normal snapback. Into a hard landing.

Democrats in particular love hard landings because that green lights them for massive wasteful spending.

The US is already at $35+ trillion with unfunded liabilties totalling $218+ trillion. Of course, the Biden Administration is attempting to cut Medicare for seniors and raise the price while handing out unlimited benefits to illegal immigrants.

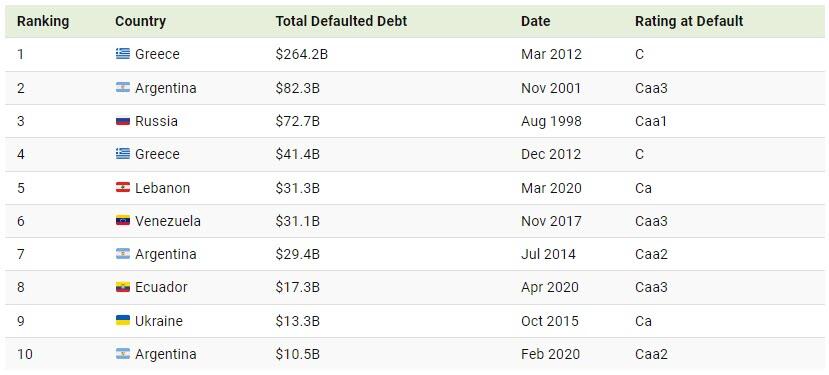

.Given the financial burden of war, the country suspended interest payments on international debt over the last two years, which was set to expire on August 1, 2024.

Without this new debt restructuring, this default would have ranked among the 10 largest in recent history. The last time Ukraine defaulted on its debt was in 2015, after Russia’s invasion of Crimea.

Below, we show the biggest sovereign debt defaults between 1983 and 2022:

Greece’s $264.2 billion default in 2012 stands as the largest overall, unfolding when the country was mired in recession for the fifth consecutive year.

The country defaulted again just nine months later, making it the fourth-largest ever. Leading up to the crash, Greece ran significant deficits despite being one of the fastest-growing countries in Europe. Furthermore, in 2009, the newly elected prime minister revealed that the country was $410 billion in debt—substantially more than previous estimates.

With the second-highest default recorded, Argentina failed to repay interest on $82.3 billion in foreign debt in 2001. Like Greece, it is a repeat offender, defaulting numerous times since independence in 1816. Today, Argentina is the largest debtor to the International Monetary Fund, despite being Latin America’s third-largest economy.

Following next in line is Russia’s 1998 default on $72.7 billion in loans, coinciding with a currency crisis that erased more than two-thirds of the ruble’s value in a matter of weeks. That year, several other countries including Venezuela, Pakistan, and Ukraine defaulted on their debts after the Asian Financial Crisis of 1997 spurred instability in global financial markets.

Just as 1998 saw a wave of defaults, 2020 was a year marked by major debt upheavals. Due to the pandemic and collapsing oil prices, it was a record year for sovereign defaults, reaching seven in total. Among these, Lebanon, Ecuador, and Argentina saw the largest defaults amid deepening fiscal pressures.

Harris is just another free-spending politician who will eventually lead the US into default. But at least Harris/Walz exude joy.

At least Harris/Walz haven’t adopted (stolen) the phrase “Work makes one free”.

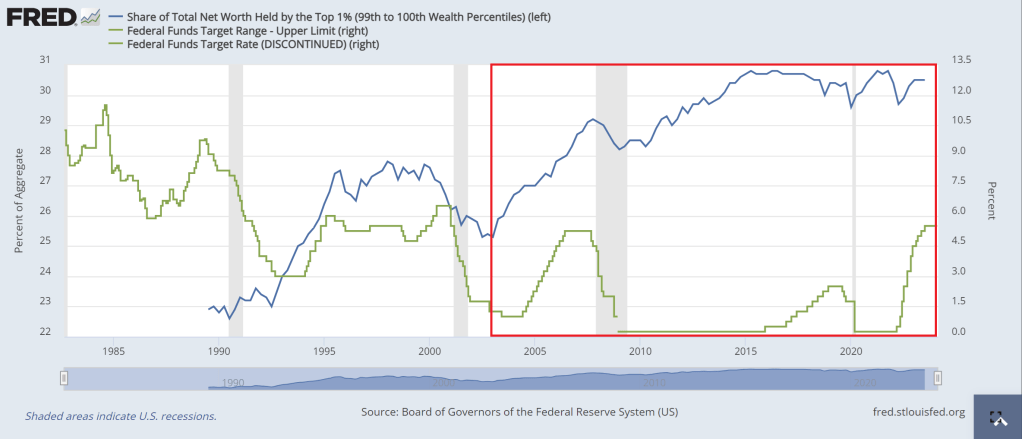

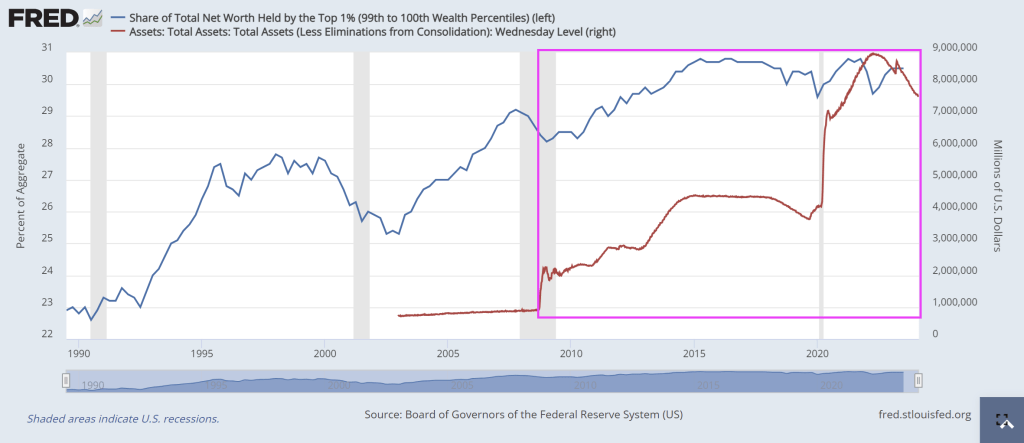

An example of the Sisyphus economy? The top 1% of earners (blue line) have seen an incredible increase in net worth, particularly after Fed Chair Alan Greenspan’s big rate cuts (green line) from 2000 to 2004. Each subsequent rate cuts under Bernanke (2007-2008) and Yellen (who just kept rates too low for too long). The end result? In the red box, the top 1% made out like bandits.

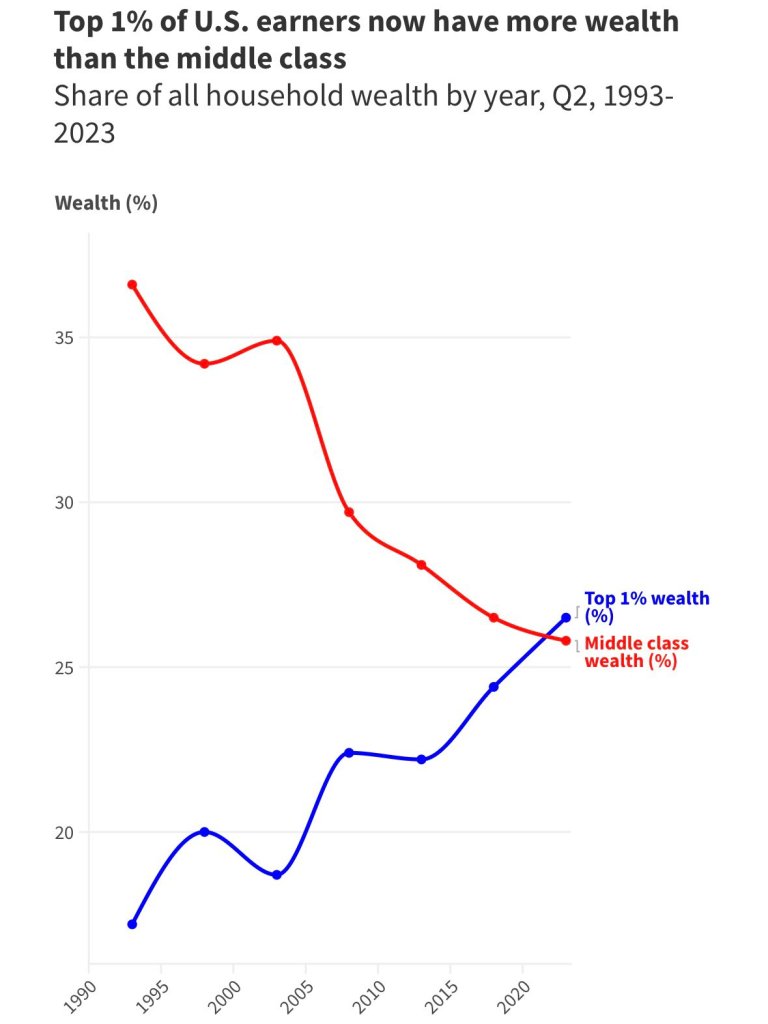

The end result? The top 1% of earners now have more wealth the the middle class.

Of course, asinine Federal government policies (like open borders and making donors wealthy with green energy spending) and the lack of a serious approach to corruption have complicated matters.

So the working class, middle class and low wage workers, are the ones pushing the boulder up a hill while government insiders like Biden make millions through influence peddling. So, unlike the Sisyphus legend, the middle class and low wage workers are being punished by simply existing.

The Fed’s balance sheet has had a similar effect, particularly since the financial crisis of 2007-2008 when The Fed truly became unhinged under Janet Yellen. So of course, Yellen was made Secretary of Treasury, the largest honey pot in the world, so she could continue growing the elites power while minimizing the wealth of all others.

Should we end The Fed? Of course! But we can’t even have a rational discussion on why we are funding a war in Ukraine (to protect their border?) while we leave our borders open to invasion?

Here is one of the 1% who made a fortune by simply having a big mouth and being in politics.

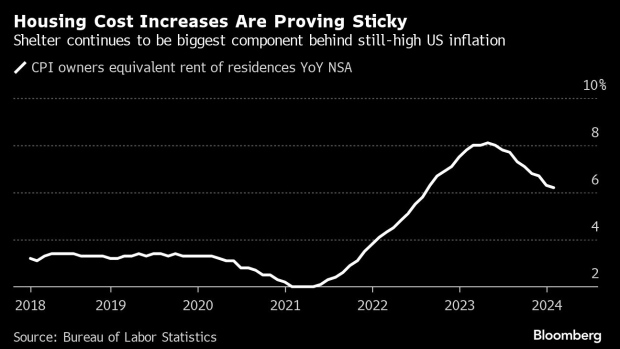

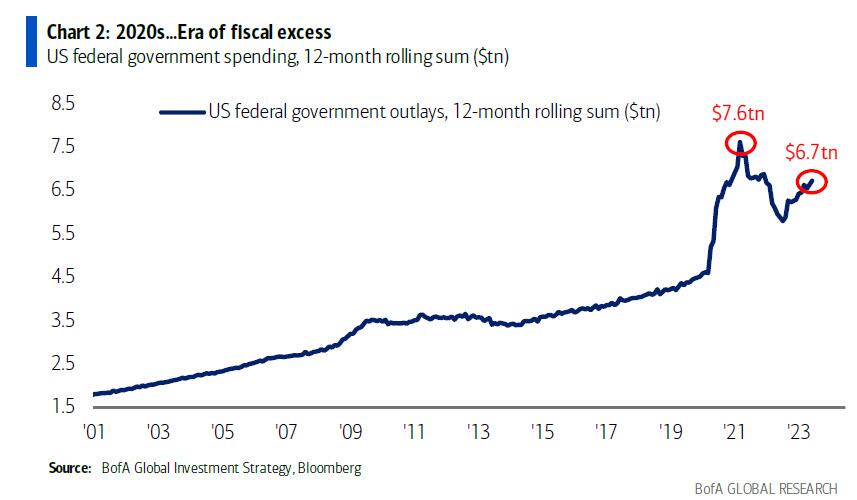

The Federal Reserve (aka, The Keep) is back in the saddle again. The Fed has been unable to control inflation since Federal government spending was so fast and furious after Covid that little thought was given to the long-term ramifications of insane spending. Not to mention The Fed’s overreaction to Covid.

Example?

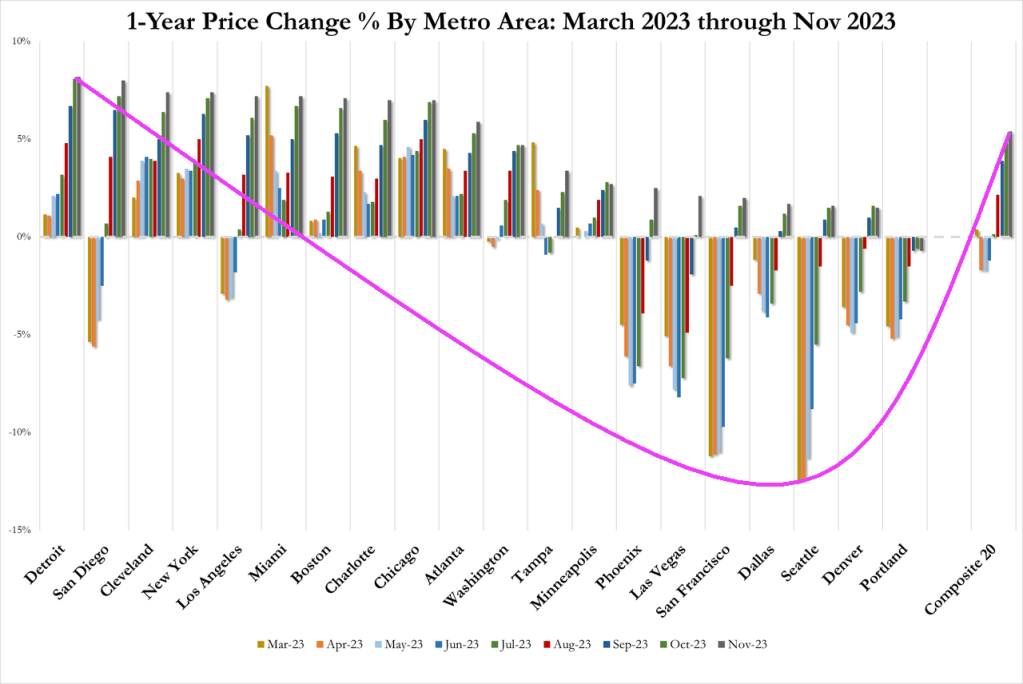

Home price growth is rising again. Home prices in traditional “bubble cities” out west were cooling, but are reaccelerating. Even Detroit and Cleveland are seeing rapid home price acceleration.

Yes, housing inflation is sticky.

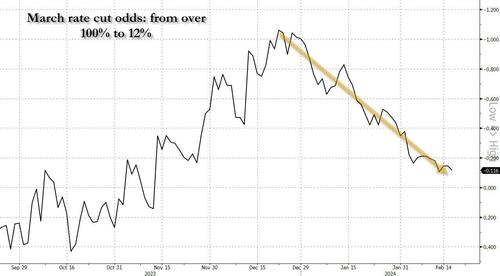

In retrospect, this wholesale dovish euphoria may have been rather short sighted, because after several strong economist reports hit the tape (with the Nov 2024 election growing closer by the day, that should hardly have been a surprise), March rate cut odds collapsed from over 100% in late December, to just 12% currently…

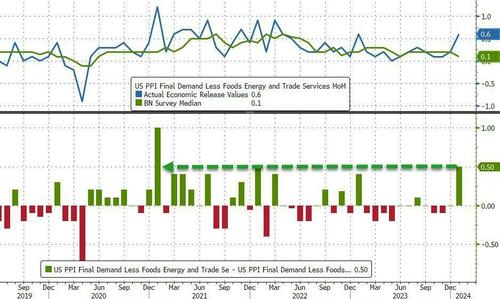

… as first the January CPI printed red blazing hot– with core coming in at 3.9% far higher than the 3.7% expected, with the 3-month annualized rate jumping to 4% from 3.3% and the 6-month annualized rate spiking to 3.7% vs 3.2%, but the biggest highlight was SuperCore CPI (i.e., core CPI services ex-Shelter) which soared 0.7% MoM, the biggest jump since Sept 2022…

… and then the January PPI print come in even hotter, with a core component surging in January by 0.5%, smashing expectations and beating estimates by the most since Jan 2021.

The result: not only has the market rapidly priced out what if formerly saw as many as 6 rate cuts in 2024, but growing speculation that a rate cut may not come at all unless the Fed tightens some more first (and with the S&P500 now over 5000, it is pretty clear that the market has already priced in virtually all rate cuts and has cornered the Fed).

Of course, the mass migration across the Mexican border (who knows? could be up to 11 million under Biden’s Reign of Error). While Paul Krugman, the resident lunatic economist for the New York Times, extols the virtues of mass immigration for driving up GDP, fails to recognize that mass migration is helping drive up prices. This is inflation that The Fed can’t control. And Biden/Mayorkas want even MORE mass immigration.

This headline from Zero Hedge makes me so glad I have eaten heart-healthy Quaker Oats and Cheerios every morning for the last 20 years! Study Finds 80% Of Americans Exposed To Fertility-Lowering Chemicals In Cheerios, Quaker Oats. The chemical (chlormequat chloride) was detected in “92 percent of oat-based foods purchased in May 2023, including Quaker Oats and Cheerios.” But that was nothing compared to this Zero Hedge headline: EU “Suicide Pact” Threatens To Flood Continent With 75 Million More Migrants. Makes me wonder if Biden/Mayorkas are under orders from the UN/WEF/Soros to let immigrants pour across our southern border (including 20,000+ Chinese military age males). But back to the economy.

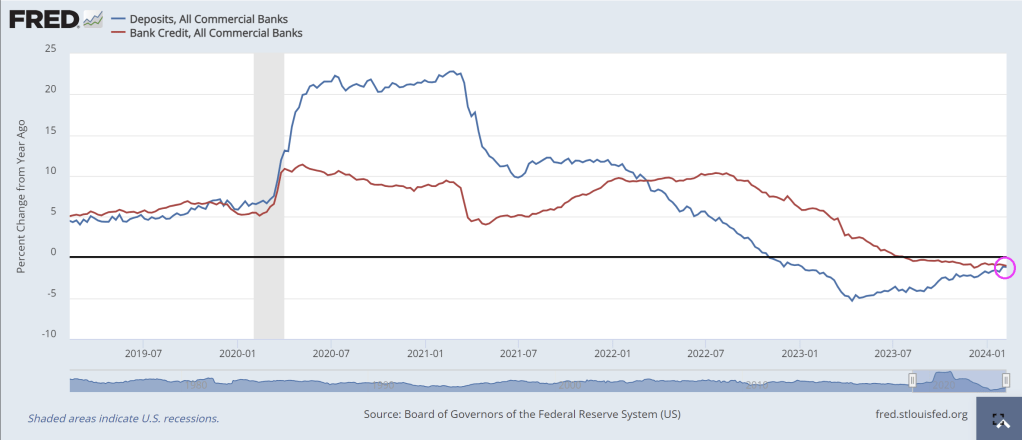

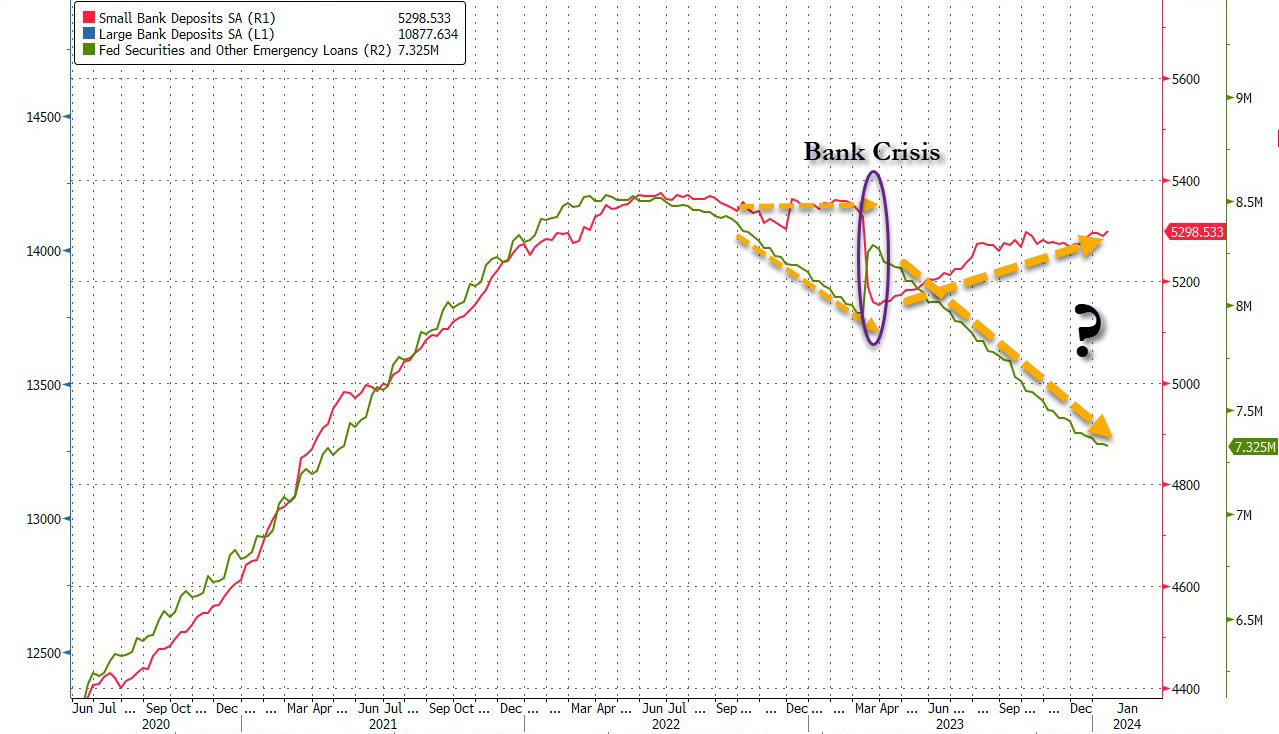

Both bank credit growth year-over-year (YoY) and bank deposit growth (YoY) are NEGATIVE. Covid resulted in massive Federal government stimulus spending (and Federal Reserve hyper stimulus) in 2020, but as the stimulus wears out, so does bank lending and deposits.

And after the prior week’s miraculous surge in deposits (again, according to The Fed), last week saw total bank deposits (seasonally-adjusted) drop $57BN – the biggest weekly drop since October…

This data is from the week when Regional bank shares shit the bed thanks to NYCB…

Interestingly, on a non-seasonally-adjusted basis, total bank deposits declined about the same as SA -$58BN (and are down $180BN YTD)…

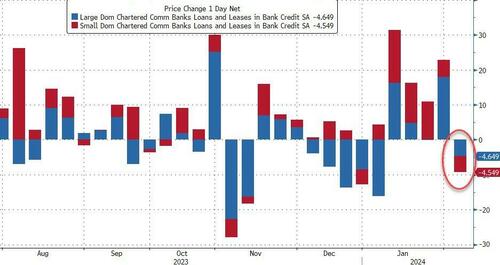

And, excluding foreign banks, domestic deposits dropped $52BN SA (Large Banks -$40BN, Small Banks -$12BN), and tumbled $65BN NSA (Large Banks -$57BN, Small Banks -$$8BN)

As the chart above shows, on an NSA basis, domestic banks have only seen one week of inflows in 2024.

As one might expect, loan volumes shrank during that week by just over $9BN (Large banks -$4.6BN, Small banks -$4.4BN)…

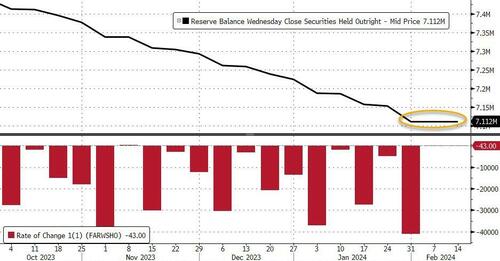

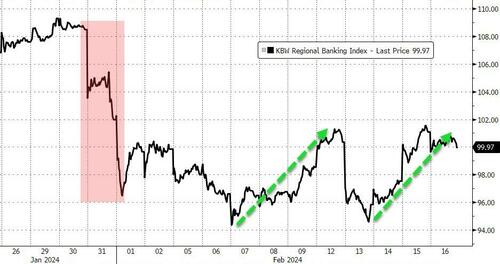

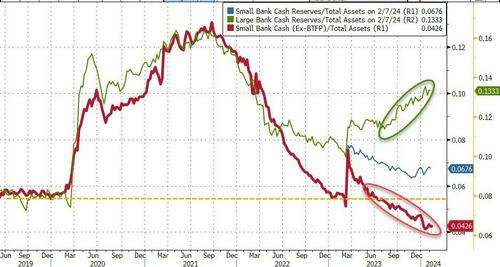

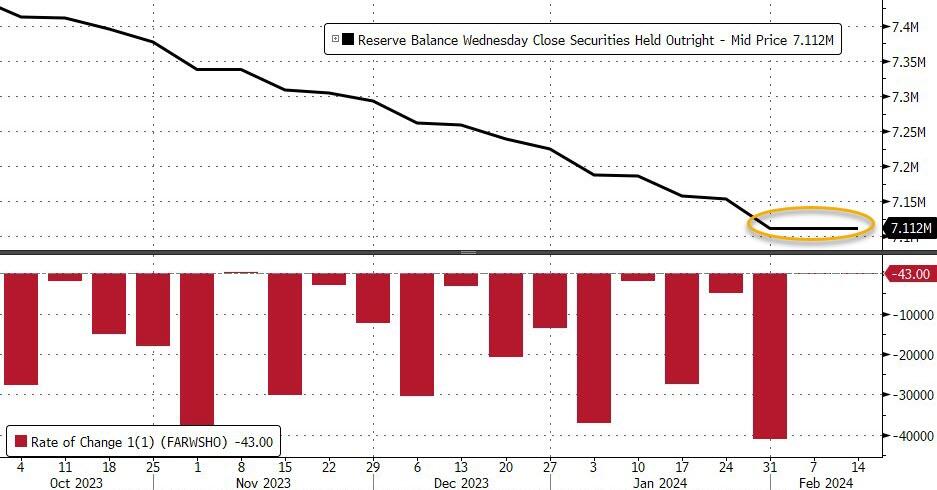

And finally, as a reminder – despite the rebound off the lows again this week in regional bank shares, which must mean everything is awesome, right? – the regional bank crisis is still very much alive as evidenced by the red line below (without The Fed’s imminently expiring BTFP facility)…

…what else are big banks (green line) going to do with all that cash burning a hole in their pockets?

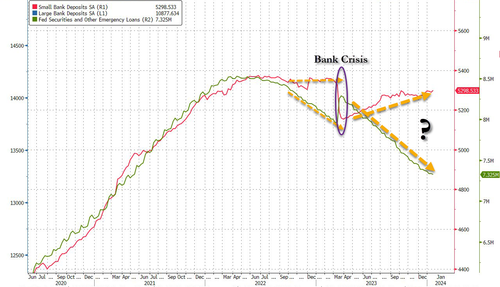

The bottom line is – this looks a lot like a ‘Small Bank’ crisis. The last time this happened, the crisis sparked a sudden $300BN ‘run’ in small bank deposits…

Is The Fed ‘hoping’ for a controlled bank-run this time – so as many small bank deposits are drained voluntarily, before they are drained all at once in a panic (and the Reverse Repo facility is empty, unable to provide any cushion)?

It is looking like a recession in mid-2024 as Covid Stimulypto has run its course. Is the US economy so lame that is requires constant Federal government and Federal Reserve manipulation??

Joe Biden (President of the top 1% of Americans) and his likely replacement “Greasy Gavin” Newsom, wrecker of the California economy. Two economy wreckers on the same stage.

Remember when Democrats were the party of the working man and Republicans (like George HW Bush) were called “Country Club Republicans”? Now Biden and Democrats represent the elitist top 1% of wealth and Trump/Republicans (that Biden snidely calls “Maga Republicans”) represent the bottom 99%. Who woulda thunk??

For visitors, Universal Studios Florida offers a chance to visit a fantastical land full of wizards, Minions and various characters from NBC Universal’s many film and television properties. But for the roughly 28,000 men and women who work at the 840-acre theme park and resort complex in Orlando, the troubles of the real world — like the rising cost of housing — are not far away.

Central Florida has seen some of the nation’s fastest pandemic-era rent increases, thanks to a confluence of job growth, migration and housing underproduction that has put a strain on residents. The average tenant in the region saw their monthly rent jump by $600 between early 2020 and early 2023. According to the National Low Income Housing Coalition, the Orlando-Kissimmee-Sanford metro area has one of the worst affordable housing shortages in the US, with only 15 available units for every 100 extremely low-income renter households.

The dire need for workforce housing is behind the entertainment conglomerate’s latest project in Central Florida: a 1,000-unit mixed-use development, set to open in 2026, that promises to give tenants who work in the service industry a short commute to the constellation of tourist attractions and hotels nearby. To launch the project, Universal donated 20 acres of land adjacent to the Orange County convention center. Called Catchlight Crossings and built in partnership with local developer Wendover Housing Partners, the project broke ground in November.

Universal’s nearby rival is also wading into affordable housing. In 2022, Walt Disney Co.announced plans to donate 80 acres for a proposed 1,450-unit affordable development a few miles to the southwest. Also set to open in 2026, the project would be built near Flamingo Crossings Village, a campus for participants in Disney’s college internship program that also leases units to some Disney World cast members. (Oh great, brainwashing by woke Disney types).

As housing costs in Central Florida have soared, the theme park giants have faced criticism for underpaying workers. In June, Universal raised its minimum wage by $2 to $17 an hour, while Disney, which employs 82,00 people in Florida, agreed to bump its starting hourly rate to $18 in 2024. Still, both lag behind the $18.85 that the Massachusetts Institute of Technology’s Living Wage Calculator estimates would be needed to support an adult with no children in Orange County.

Visitors throng Disney’s Magic Kingdom in Orlando.Photographer: David Ryder/Bloomberg

Even smaller theme parks in more affordable areas have become homebuilders in an effort to ease the housing crunch. In May, Indiana’s Holiday World opened a $7 million development called Compass Commons, which is meant to provide seasonal housing for up to 136 employees. It will replace a proposed theme park attraction that was set to open last summer.

Such partnerships between entertainment industry employers, developers and local government represent the latest spin on a solution for the ongoing scarcity of apartments for lower-income households. Catchlight Crossings is part of Universal’s Housing to Tomorrow initiative, which was inspired by the Orange County mayor’s Housing for All Task Force. The company represents almost 10% of the tax base of Orange County, which includes Orlando.

“What could we do that would be more than just the typical corporate response?” said John Sprouls, executive vice president and chief administrative officer at Universal Parks and Resorts. “If you’re going to provide affordable housing, providing affordable housing where the jobs are sure makes a lot of sense.”

The Truly Missing Middle

Workforce housing is a much-needed housing type without a precise definition. Unlike affordable housing, which must meet stringent rental rates matched to specific income levels to qualify for government support and subsidies — typically 40% of units need to be priced to support those households who make 60% of the area median income — workforce housing stands as more of a catch-all term. Some define it as housing that serves those making between 80% and 120% of median area income. Often, the term is used to invoke housing for teachers, first responders and other public servants who have been increasingly priced out of expensive metros.

Over the last decade, and through the recent pandemic-era surge in apartment construction, developers have largely ignored the lower end of the market, focusing instead on Class A apartments. Beginning in 2013, half or more of units delivered each year were considered high-end or luxury, according to statistics from the National Multifamily Housing Council. Only since the middle of 2022 has that shifted towards Class B, or more affordable units.

Seeking lower production costs and rents, a handful of big developers have created new sub-brands of apartments designed to appeal to less-monied tenants. Grubb Properties launched a series of “car-light” developments called Link, which emphasize accessibility to major urban employers, while Greystar’s Modern Living Solutions concept offers modular multifamily buildings that are assembled on site from factory-built elements in an effort to trim construction costs.

To promote more construction of this type of housing, a bipartisan coalition of federal lawmakers recently introduced the Workforce Housing Tax Credit Act. Like the low-income housing tax credit, the proposed legislation would provide tax credit to investors who build affordable apartments. The bill’s sponsors, including Oregon Senator Ron Wyden, say the credit would finance approximately 344,000 affordable rental homes. It’s been a pet issue for Wyden in particular; 70% of Oregon school districts have built or rented housing to provide support for their teachers.

Nationwide, the US is short approximately 2.2 million workforce units, according to a 2022 Fannie Mae study. Central Florida’s service-based economy has left it with one of the highest levels of need, Wendover founder and Chief Executive Officer Jonathan Wolf said. There are roughly 100,000 people living within a five-mile radius of Catchlight Crossings who would income-qualify for the development.

Besides pools for residents, the proposed Universal development will include such amenities as a preschool and adult education center.Credit: Wendover Housing Partners

Rents at the Universal-led project will range from $400 to $2,200, depending on income qualifications (the average two-bedroom unit in the area rents for just shy of $1,900 a month). The development will also contain medical offices, retail, community space including pools and fitness centers, bike and walking paths and a tuition-free Bezos Academy preschool and adult education center. A transit center will connect residents to buses, ride-hailing services and company shuttles; a stop on the proposed Sunshine Corridor, a new east-west rail line that’s designed to help tourism workers get around, may take shape nearby.

“You’re not creating an economic ghetto,” Wolf said. “You’re creating a lifestyle enhancement for so many people, giving folks the ability for mobility.”

The theme park giant owns a few thousand acres in the area, so this was a relatively small donation, according to Sprouls. It also comes during a time of booming profits: Central Florida’s tourism industry generated a record $87.6 billion in economic impact in 2022. And since Universal transferred the land via a 501c3 charity with deed restrictions, the donation can lower development costs and help ensure long-term affordability; lots of affordable housing tends to revert back to market-rate pricing after a set term.

Employer-sponsored projects like Catchlight Crossings can’t mandate that only their employees can be tenants — that would violate fair housing rules. But for a customer-facing company like Universal, working to close the region’s housing gap can pay direct benefits, Sprouls said. When employees can’t find housing nearby and need to drive hours to get to work, it impacts not just their performance, but the guest experiences that drive satisfaction and repeat visits.

Park guests arrive at the Universal Studios theme park in Orlando in 2020.Photographer: Zack Wittman/Bloomberg

“It helps us to be able to recruit because people are able to have jobs here,” Sprouls said. “Salaries go into making you an attractive employer in the area, but you also need to make this an attractive place to live.”

Corporate Housing’s Mixed Record

Still, it remains to be seen if privately financed efforts like the Universal and Disney investments can have a significant impact on the lives of local renters. Other industries, most notably tech, have poured hundreds of millions of dollars and even billions into financing the construction of workforce housing near their headquarters. Amazon.com Inc., Google and Meta Platforms Inc. have all done variations of this kind of development, with mixed results. Many such efforts took off after severe backlash to the impact tech jobs had on local housing markets, and most were in the forms of loans, financing and leases, which can be helpful but not exactly game-changing. Recent swings in interest rates and increases in housing costs, not to mention struggles in the tech industry, have curtailed many of these programs.

“There was a lot of energy, and then there wasn’t,” Alex Schafran, a visiting scholar at San Jose State University’s Institute for Metropolitan Studies and a former consultant for Facebook’s housing initiative, told the Guardian. “The balloon didn’t pop overnight, but now there’s very little air in it.”

And the support of powerful local employers can’t inoculate these projects from community pushback. At a town meeting for the Disney project in September, residents raised a host of familiar objections about traffic congestion, school crowding and site location. When it comes to building multifamily developments, even Goofy has to contend with NIMBYs.

Wendover’s Wolf argues that while the financing part is critical, it may not be enough. His firm has been very involved in pushing for more government support for the affordable housing projects they specialize in. Associate Ryan von Weller, for example, was among the local developers who consulted with Florida lawmakers on a state bill, Live Local, which directed more than $700 million into supporting affordable housing. (Sprouls said Universal won’t see any tax benefits from their land donation.) But Wolf believes the area’s big corporate employers need to play a bigger role in solving this crisis.

“We need your involvement in it in a very direct way to work alongside us, to make this a success,” he said. “It’s not just a simple check and walk away. We need the land. We need cooperation.”

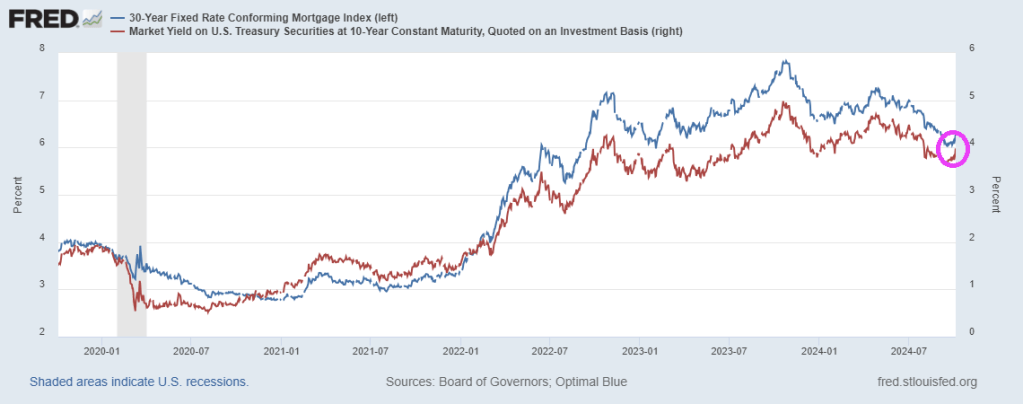

Here is the REAL problem with the lack of housing stock. Growth of new housing units has slowed to negative speeds as mortgage rates soared, but aren’t growing again with declining mortgage rates which remain relatively high. Add in the 11 million or so illegal immigrants crossing the border and we have a major problem.

The Federal Reserve has tightened their monetary manipulations to combat inflation caused by loose monetary policy and excessive spending by Biden and Congress.

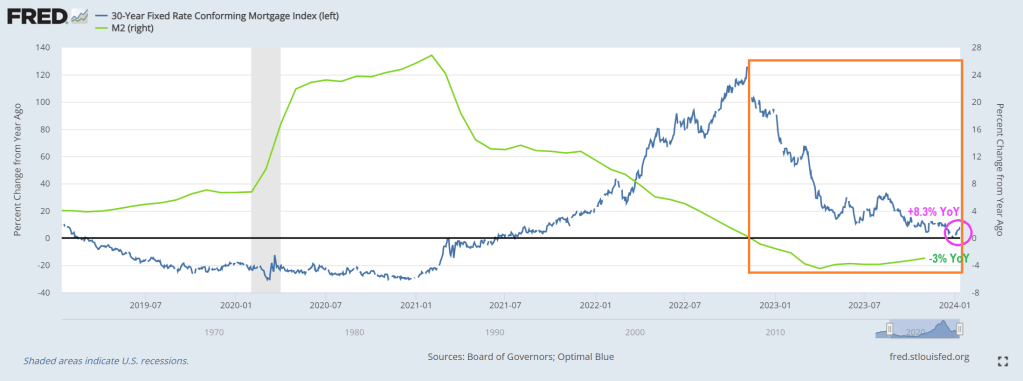

The result? US conforming 30-year mortgage rates are up 8.3% since last year and up a whopping 141% since the beginning of 2021 (the year Biden was selected to be President).

Check out mortgage rate GROWTH (blue line) as M2 Money growth *green line) went negative (orange box).

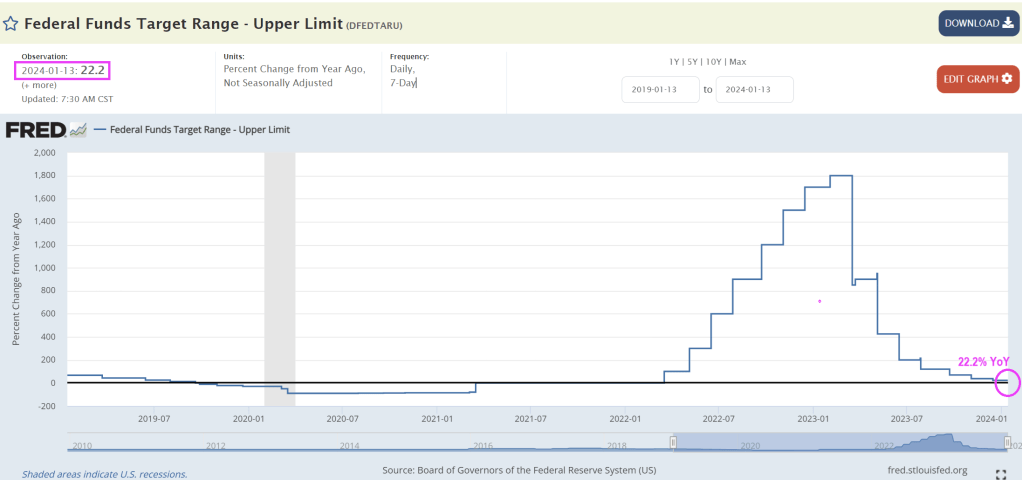

This graph corresponds nicely with this chart of YoY changes in The Fed Funds rate. Which is still rising at a rate of 22.2% year-over-year (YoY).

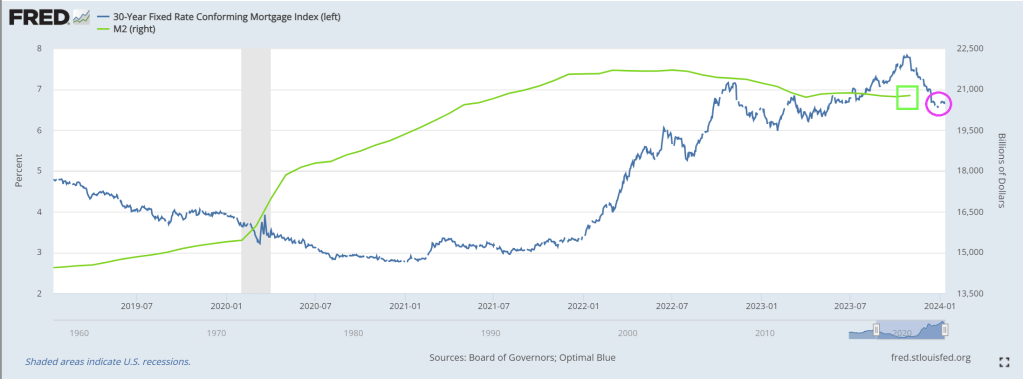

The 30-year mortgage rate had been falling after peaking in August 2023 after peaking at 7.299%. The latest reading on January 11, 2024 was 6.662%.

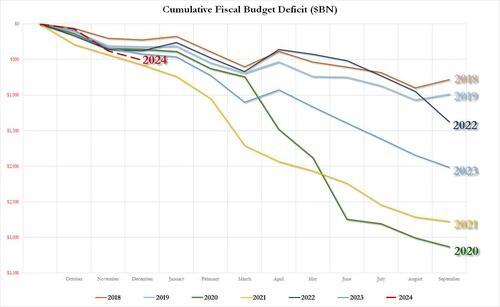

Well, we have news for you: if 2023 was bad, 2024 – an election year of course – is shaping up to be far worse.

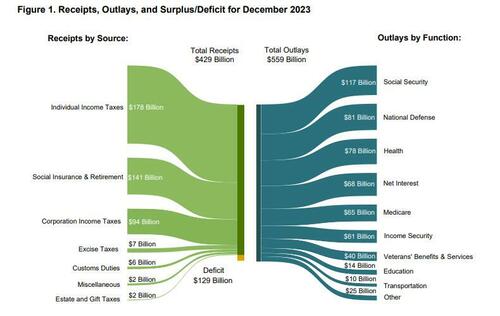

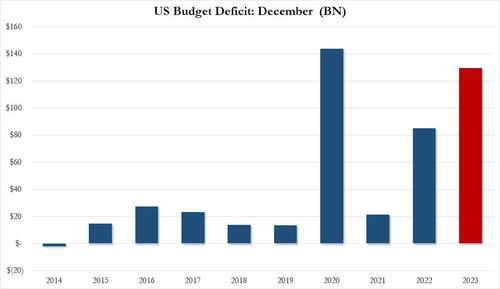

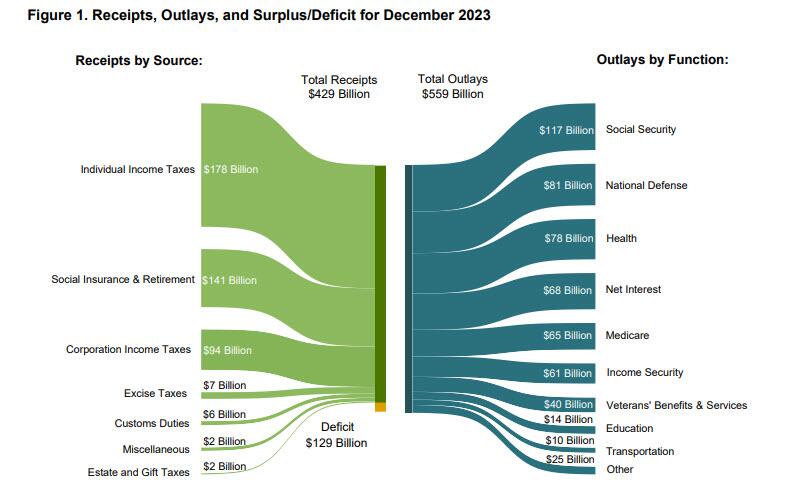

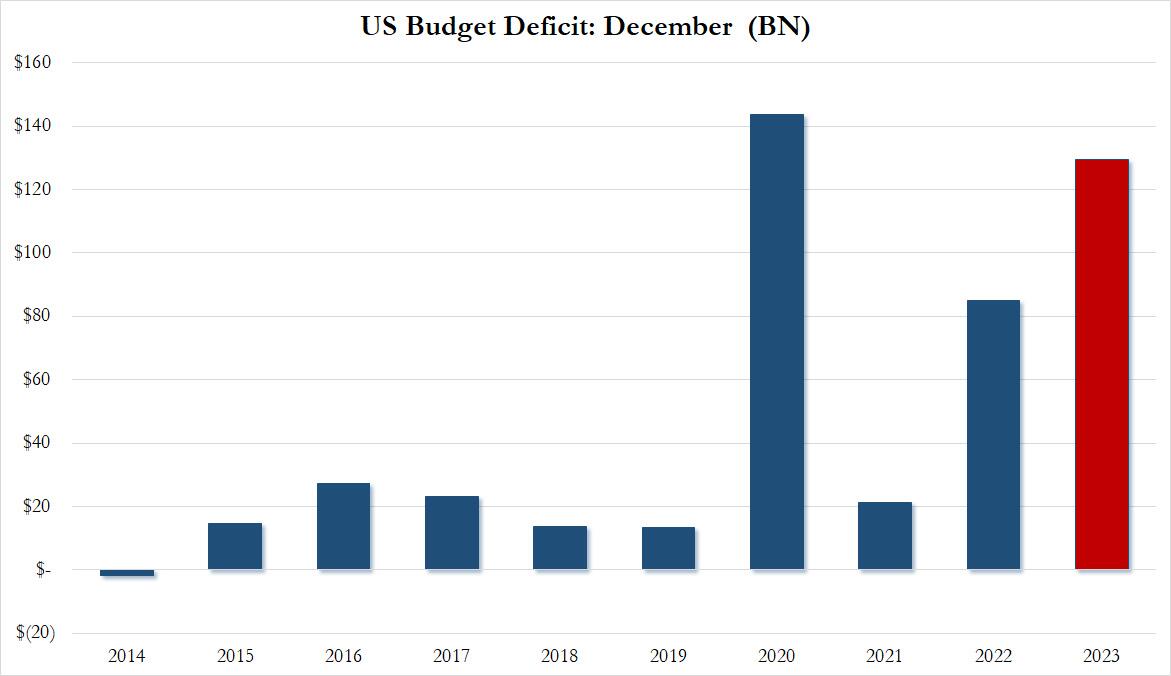

Moments ago the US Treasury reported the budget deficit picture for December and it will come as no surprise to anyone that the US has continued to spend like a drunken sailor, or rather, even more. As shown in the chart below, in the month of December, the US collected $429 billion through various taxes, while total outlays hit $559 billion…

… resulting in a December deficit of $129.4 billion.This may not sound like a lot, but December is actually one of those months when the US deficit is relatively tame, or used to be.

As shown in the next chart, traditionally the December deficit was barely in the $10-20BN range… until 2020 when it exploded to an all time high of $140BN. And while it dropped sharply in 2021, it rebounded dramatically in 2022, and rose to just shy of the December crisis high last month!

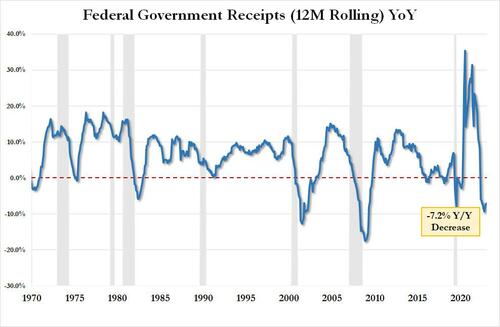

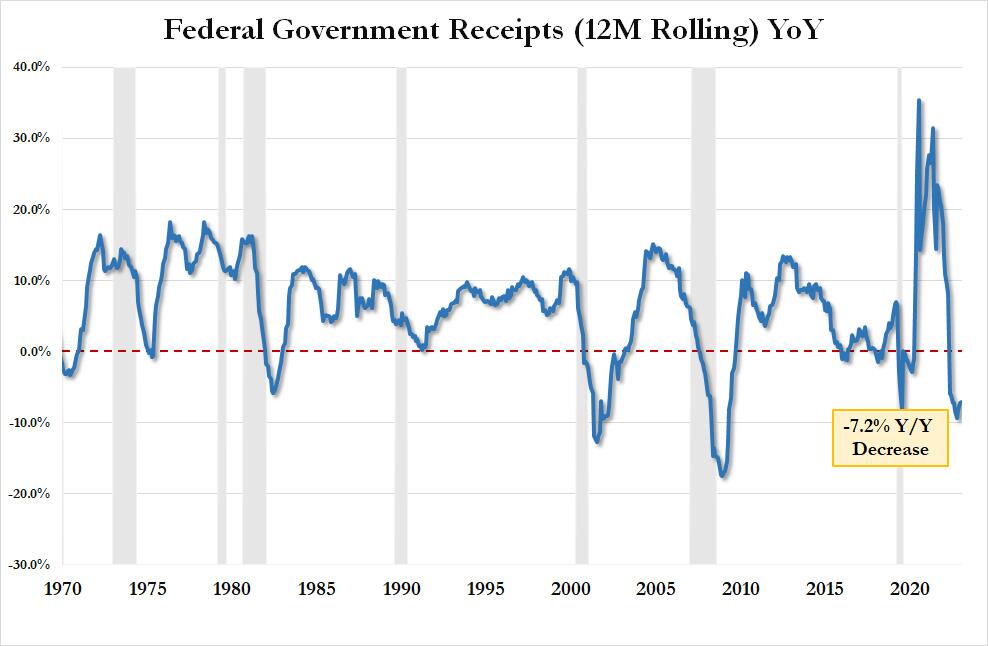

Here is some more context: tax receipts of $429.3BN in December were down 5.6% from the $454.9BN in December 2022 and down a whopping 11.8% from December 2021. On an LTM basis, US total tax receipts were $4.521TN, or down 7.2% YoY. This is now the 9th consecutive YoY decline in LTM tax receipts, something that historically has only taken place when the US was in a recession. As an aside, the “smart economists” were certain that the collapse in tax receipts would reverse after November when the postponed California taxes would be collected. Well, November has come and gone and the big picture is just as ugly.

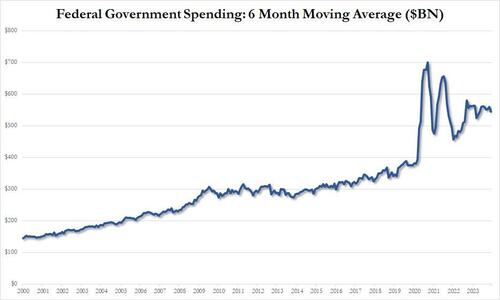

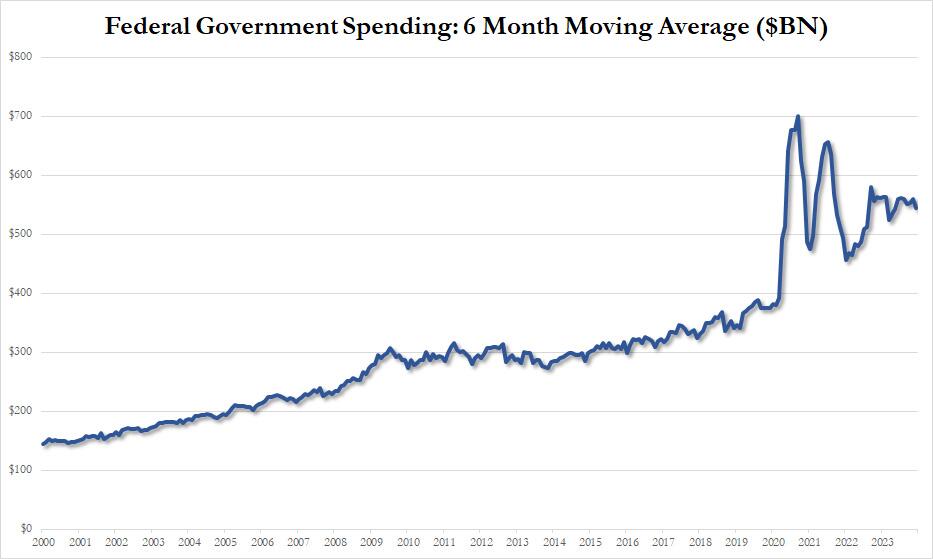

Looking at outlays, unlike tax receipts, there is danger of a decline… ever; and indeed in December the US spent a total of $559 billion, up 3.5% from the $540BN spent a year ago, and up even more from the $508BN in 2021. On a 6 month moving average basis, we are rapidly approaching the exponential phase even when accounting for the spending burst in 2020 and 2021.

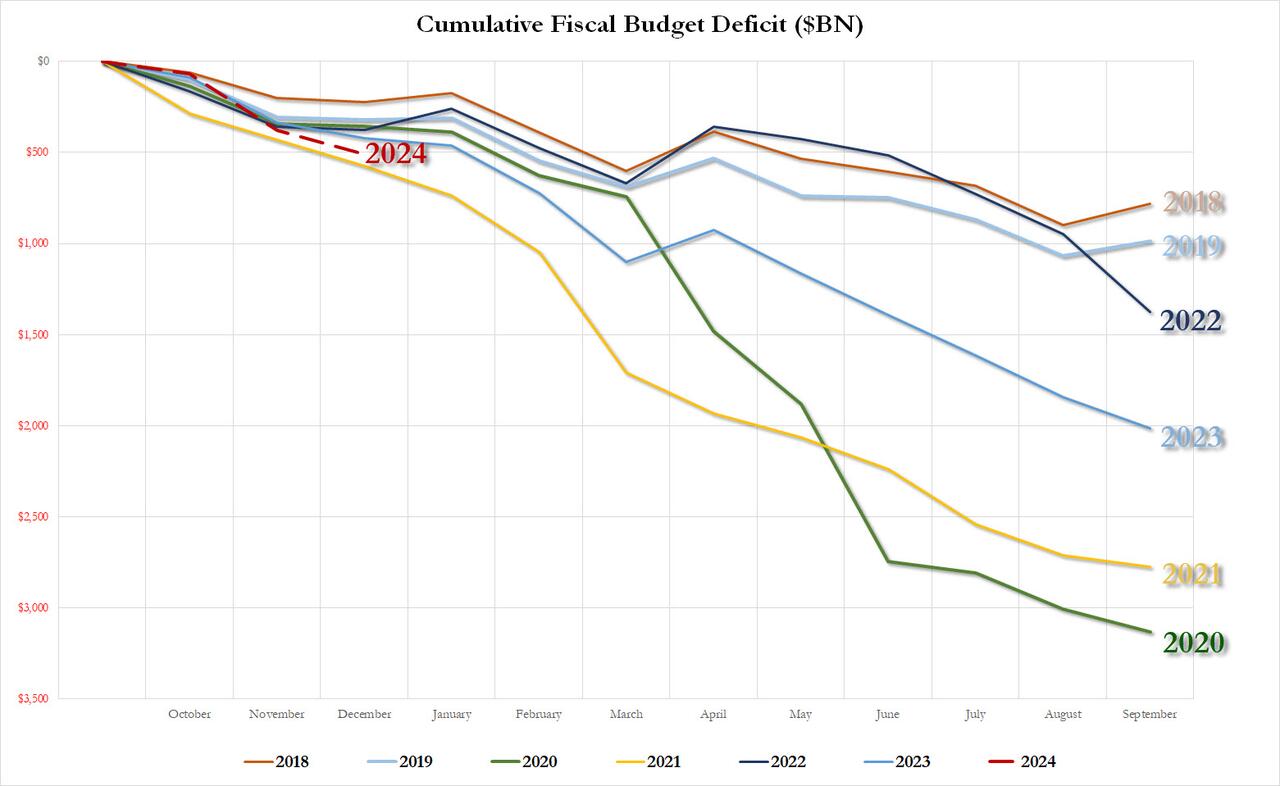

Putting it all together, we get the scariest chart of all: the YTD budget deficit three months into fiscal 2024 is already $509 billion, which would be the biggest deficit in US history after one quarter with the exception of the covid outlier year of 2021 when the US injected multiple trillions in stimmies.

As for the final, and most shocking, data point, the December budget deficit of $129.4 billion was more than $40BN higher than the $87.5BN median estimate, and was more than 50% higher compared to the $85BN December deficit in fiscal 2022.

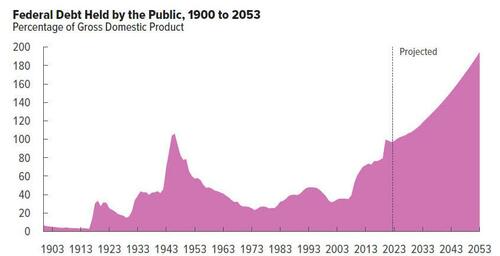

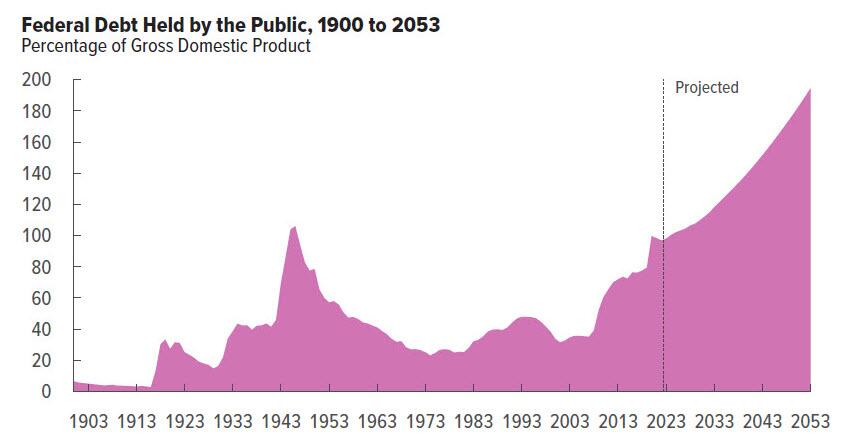

Needless to say, this is completely unsustainable and assures fiscal collapse for the US, not if, but when. Then again, we already knew this thanks to the CBO which was kind enough to chart the endgame:

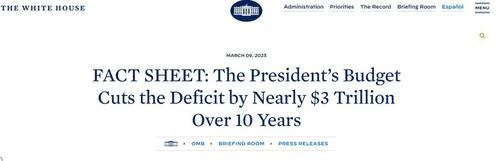

What is funniest about all this is that the US is on an accelerating path to ruin less than one year after the imposter in the White House published this laughable propaganda.

We can’t wait to see what really happens to the budget deficit over the next 10 years. Spoiler alert: there won’t be a happy ending.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.