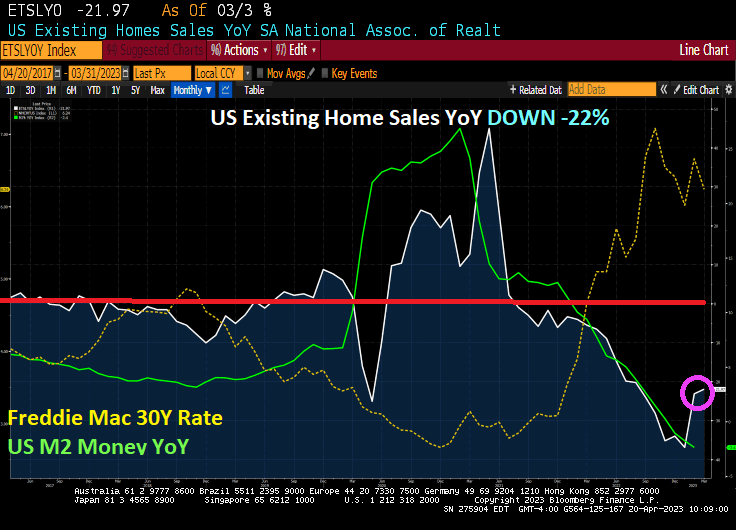

According to the National Association of Realtors, existing home sales fell -2.4% in March from February. And fell -21.97% since the same time last year (YoY).

And the median price of existing home sales fell -0.9% in March, the first negative growth since 2012.

It’s only mid April and mortgage demand should be approaching it’s yearly high. But under Biden and The Fed, mortgage demand seems to have peaked earlier than normal. It’s already late in mortgage cycle.

Mortgage applications decreased 8.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 14, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 8.8 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 8 percent compared with the previous week. The Refinance Index decreased 6 percent from the previous week and was 56 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 10 percent from one week earlier. The unadjusted Purchase Index decreased 9 percent compared with the previous week and was 36 percent lower than the same week one year ago.

The US is beginning to be out of time for agreeing on a debt limit increase. But you don’t need a fortune teller to tell you that Biden and McCarthy will eventually agree to increase the US debt limit because everyone in Washington DC love to borrow and spend money. Regardless, we are seeing the 1-year US Credit Default Swap (SR, EUR) rise above 100, higher than during the 2008/2009 financial crisis.

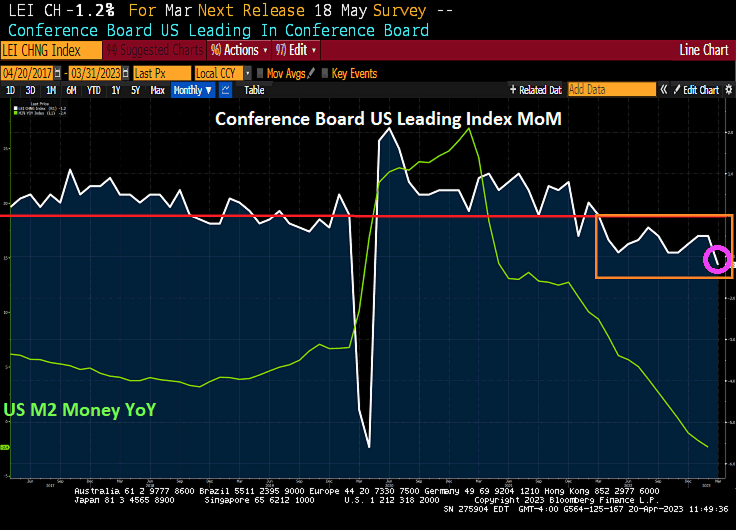

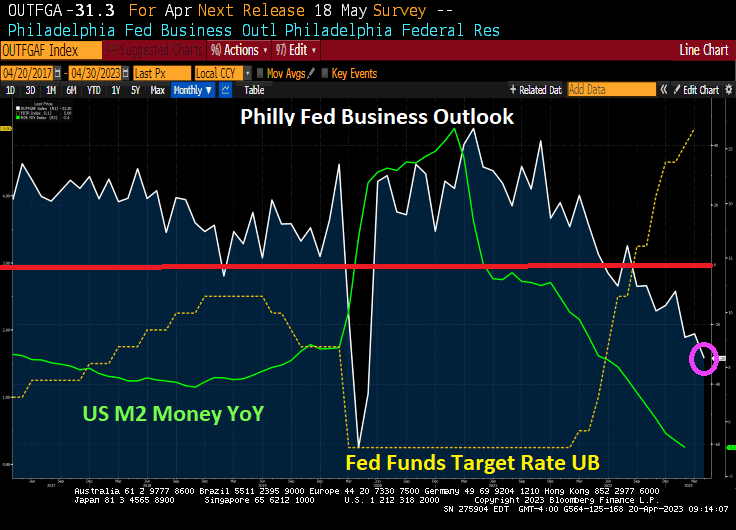

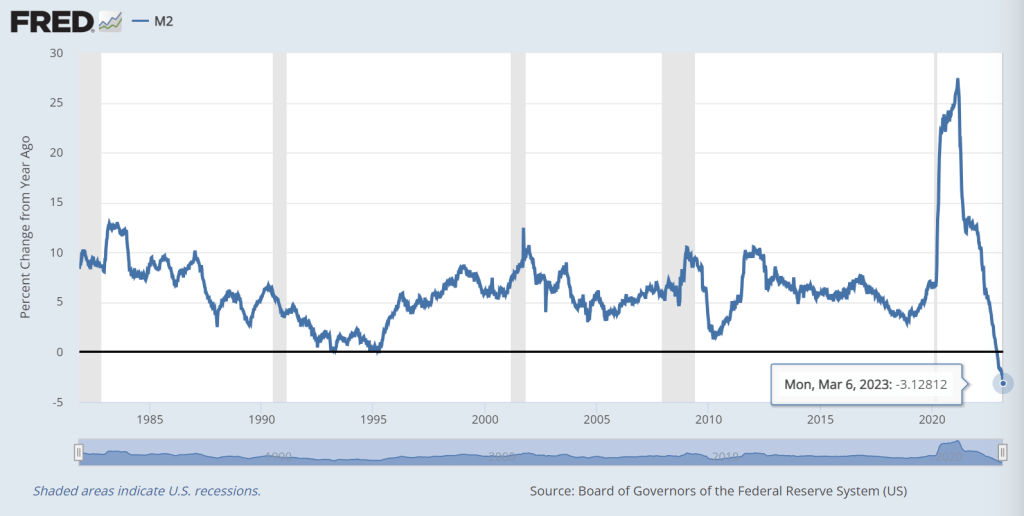

This is occuring as the US Treasury 10Y-2Y yield curve remains inverted and M2 Money growth has crashed.

But never fear! The Evil Hobbitt (aka, Janet Yellen) is still US Treasury Secretary. You know, the one who left interest rates too low for too long (TLFTL) as Federal Reserve Chair, then tightened as soon as Donald Trump was elected President.

America’s mega bank, The Federal Reserve, is slowing M2 Money growth so rapidly that it looks like it is depthcharging the US economy.

Inflation in the US has been booming since 1) Biden attacked fossil fuels, 2) The Fed’s overresponse to Covid (+27.48% YoY on February 22, 2021 near the beginning of Biden’s Reign of Error). and 3) out of control Federal spending under Biden, Pelosi and Schumer.

Fed Funds Futures point to two more Fed rate hikes before The Fed drop rates like a depthcharge. This depthcharge will help create a rekindling of asset bubbles.

The Taylor Rule suggets a Fed Funds Target rate of 11.77 while the current target rate is only 5%. This is called “leading from behind.”

Here is The Fed monitoring the US economy in order to decide on firing more financial torpedos!

US housing starts have declined in March by -17.2% since the same time last year (YoY) as The Fed rapidly removes Covid-related monetary stimulus (green line).

On the positive side, 1-unit detached housing actually rose by 2.74% from February to March (MoM). However, 5+ unit (multifamily) starts decline -6.71% MoM. Permits are similar: 1-unit permits were up 4.07% in March from February while 5+ unit permits were down -24.27%.

Housing starts out west were down -28.13% MoM as people are escaping “Gruesome Newsom Land” (aka, California). Starts are up by 6.8% MoM in The South.

“Hey Aunt Nancy, do you think American voters will vote for me for President after I helped destroy California? Can I be President and spend like a mad man like you did as Speaker of the House??”

Here is a chart of US office vacancies nationally (yellow), New York (white), San Franciso (green) and Los Angeles (orange). Note the rapid decline in office vacancies just prior to the financial crisis (often mislabeled as the subprime mortgage crisis). Then look at office vacancies after The Fed’s massive monetary experiment of setting rates to near zero and buying a ton of Treasuries, Agency MBS. etc. While San Francisco returned to pre-financial crisis levels of office vacancy, in general the office market never fully recovered.

And then “the slammer” struck: the COVID economic shutdowns. After 2020 shutdowns, office vacancy rates rose dramatically. Two complicating factors: 1) the US moved to working at home rather than commuting to an office and largely remains that way. 2) crime is going bonkers in American cities, particularly New York, Los Angeles and San Francisco (don’t worry, I haven’t forgotten about other gang nests like Chicago and Detroit). I saw that California’s woke governor Gavin “Nancy Pelosi’s nephew” Newsom said the word “gang” then apologized and replaced it with “organized groups.” No wonder Newsom can’t fix anything, but he is running for President of the US! (insert Edvard Munch’s “The Scream” painting here,)

The Fed responded to the financial crisis by lower rates to 25 basis points and printing a boat load of money. Unfortunately, office vacancies rose to a peak in October 2010 then began falling again. Only to start rising again after Trump took office in 2017. Alas, Covid struck in 2020, The Fed and Federal government panicked. States and local governments (not to mention teacher’s unions) shut down economies and schools. Office vacancies are now higher than at peak of the Covid shutdowns!!!

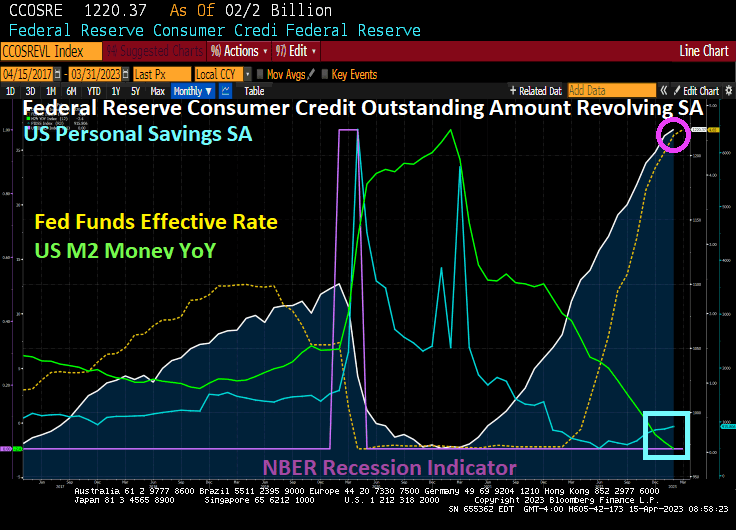

Of course, what is really troubling is that credit card useage is soaring as The Fed hikes interest rates to combat inflation … caused by Janet Yellen and The Fed keeping rates near zero for too long under Obama. Then we have Biden fighting fossil fuels and Congress spending like drunken sailors in port. All together? Consumers turn to credit cards to cope and their personal savings are dwindling.

How to protect yourself against out-of-control Fed money printing? Gold is up over $2,000.

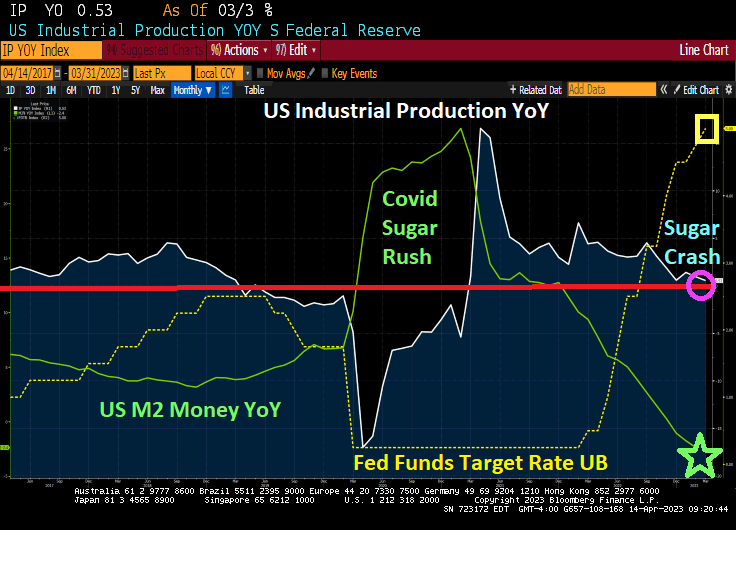

The US economy is barely chooglin along at a dismal 0.53% YoY (but 0.4% MoM in March). As the Covid “sugar rush” that caused a surge in Industrial Production in April 2021 of 16.56% has led to a “sugar crash” as M2 Money growth crashed and The Fed hiked rates to combat inflation. Known as a “sugar crash.”

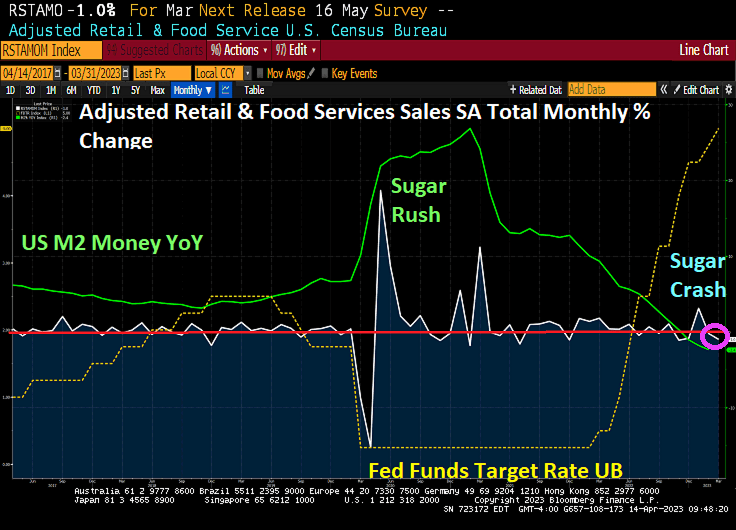

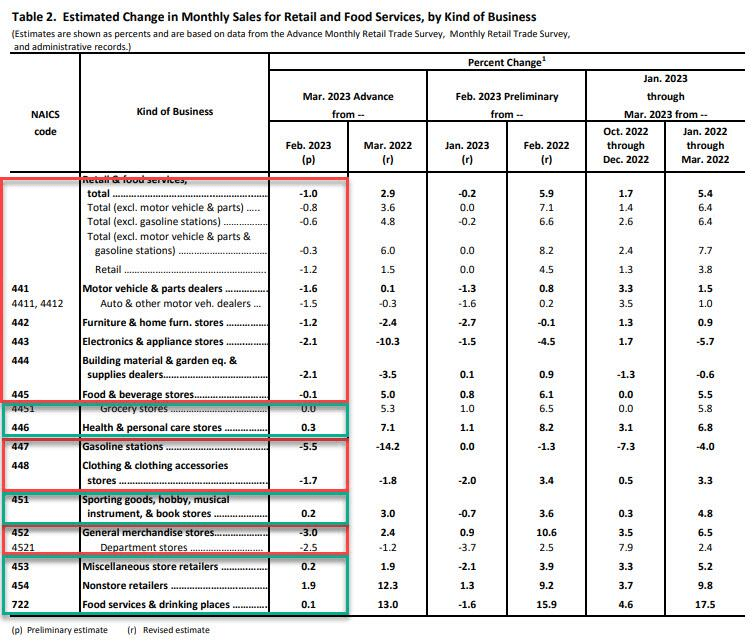

Also in today’s economic news is more Sugar Crash news. Advance retail sales dropped -1% in March. That is -155% lower than a year ago when it was +1.8%.

Here is the breakdown.

The Federal Reserve put a spell on us when Bernanke/Yellen kept rates too low for too long (TLFTL) and The Fed is now playing catch up. It is now creating havoc.

And on the Philly Fed’s Christopher “Fats” Waller saying that he favored more monetary policy tightening to reduce persistently high inflation, although he said he was prepared to adjust his stance if needed if credit tightens more than expected, we see that US Treasury 2-year yield jumping 13.5 basis points to 4.103%.

You must be logged in to post a comment.