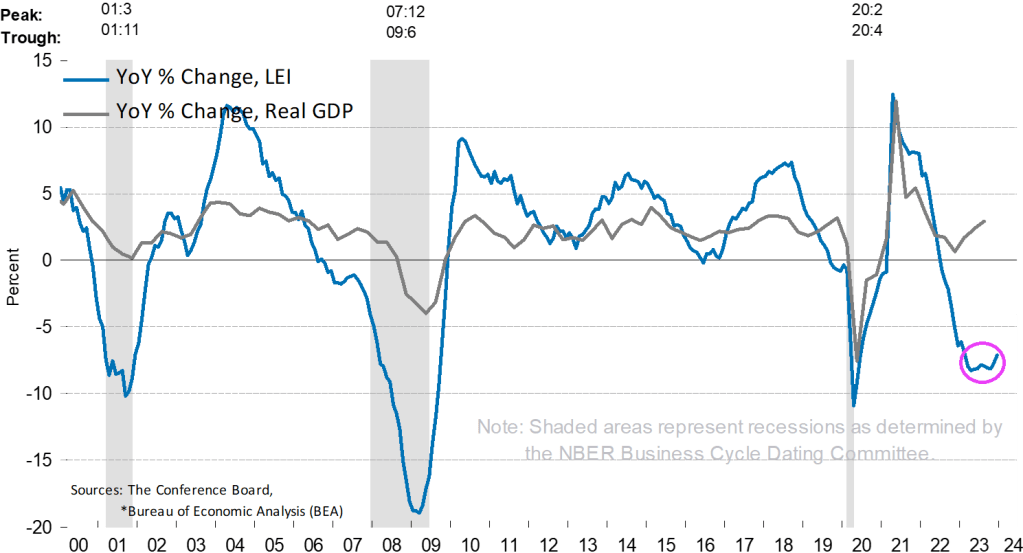

Not exactly the economic report that the Biden Administration and The Federal Reserve were hoping for. To quote The Rolling Stones, “You can’t always get what you want.” Actually, the Conference Board’s Leading Economic Indicator is more of a BLEEDING economic indicator as we enter 2024.

NEW YORK, Jan. 22, 2024 /PRNewswire/ — The Conference Board Leading Economic Index® (LEI) for the U.S. fell by 0.1 percent in December 2023 to 103.1 (2016=100), following a 0.5 percent decline in November. The LEI contracted by 2.9 percent over the six-month period between June and December 2023, a smaller decrease than its 4.3 percent contraction over the previous six months.

“The US LEI fell slightly in December, continuing to signal underlying weakness in the US economy,” said Justyna Zabinska-La Monica, Senior Manager, Business Cycle Indicators, at The Conference Board. “Despite the overall decline, six out of ten leading indicators made positive contributions to the LEI in December. Nonetheless, these improvements were more than offset by weak conditions in manufacturing, the high interest-rate environment, and low consumer confidence. As the magnitude of monthly declines has lessened, the LEI’s six-month and twelve-month growth rates have turned upward but remain negative, continuing to signal the risk of recession ahead. Overall, we expect GDP growth to turn negative in Q2 and Q3 of 2024 but begin to recover late in the year.”

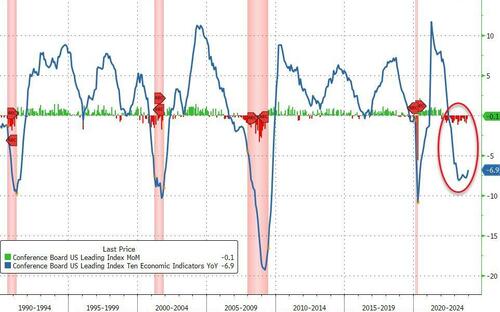

The annual growth rate of the LEI remains deeply negative.

On an annual basis (YoY), the LEI is down -6.9%.

Am I surprised that the LEI is bleeding so badly? Not with “Vacation Joe” Biden at the helm! Or his eloquent Climate Envoy John Kerry!

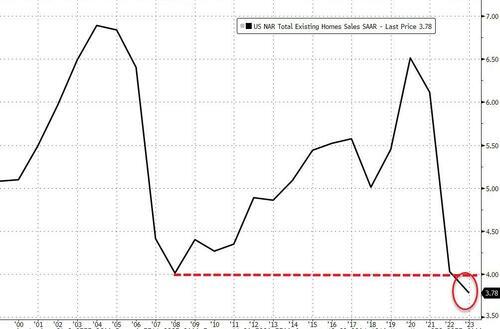

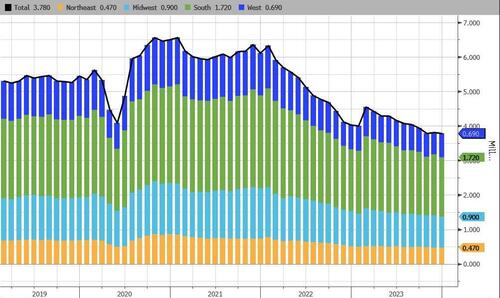

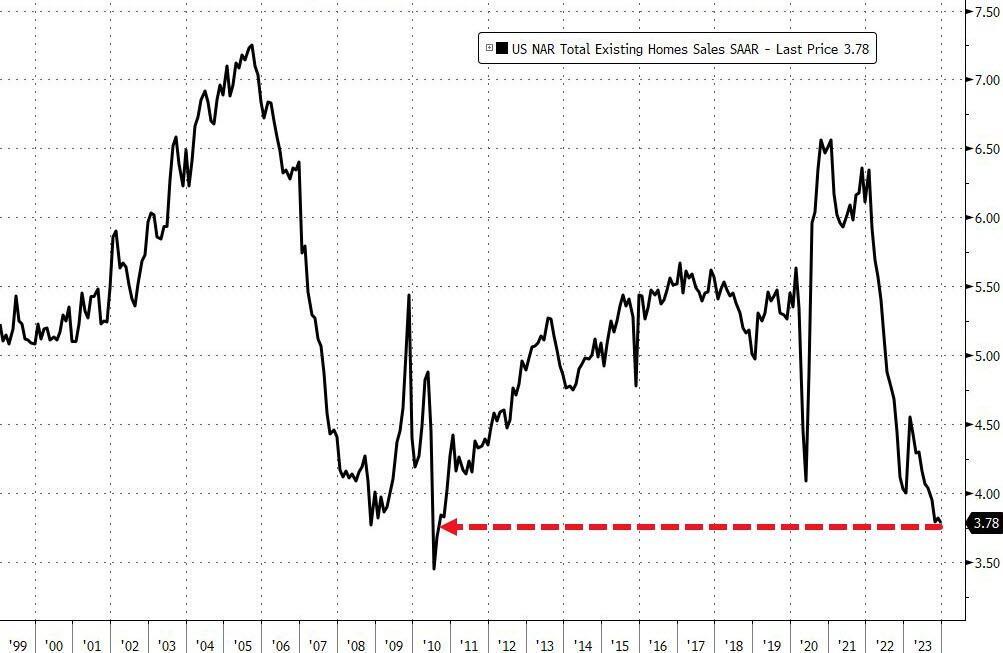

Existing Home Sales fell 1.0% MoM in December, worse than the +0.3% expected, leaving sales down

Source: Bloomberg

Total Existing Home Sales in December 2023 were 3.78mm – the lowest SAAR since 2010…

Source: Bloomberg

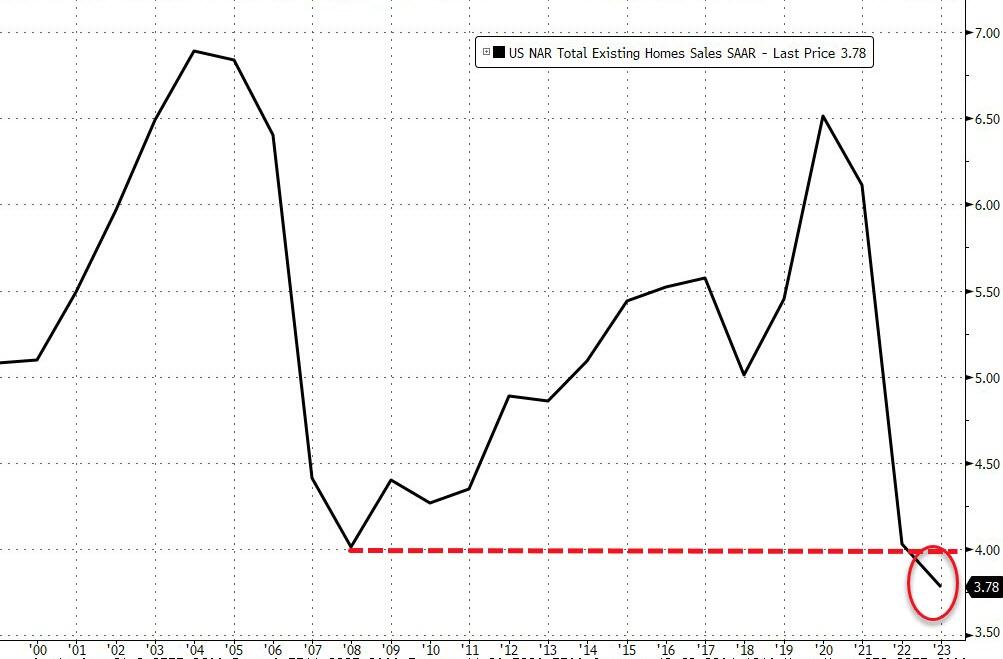

But, on an annual basis, this is the worst year on record (back to at least 1995)..

Source: Bloomberg

“The latest month’s sales look to be the bottom before inevitably turning higher in the new year,” said NAR Chief Economist Lawrence Yun. “Mortgage rates are meaningfully lower compared to just two months ago, and more inventory is expected to appear on the market in upcoming months.”

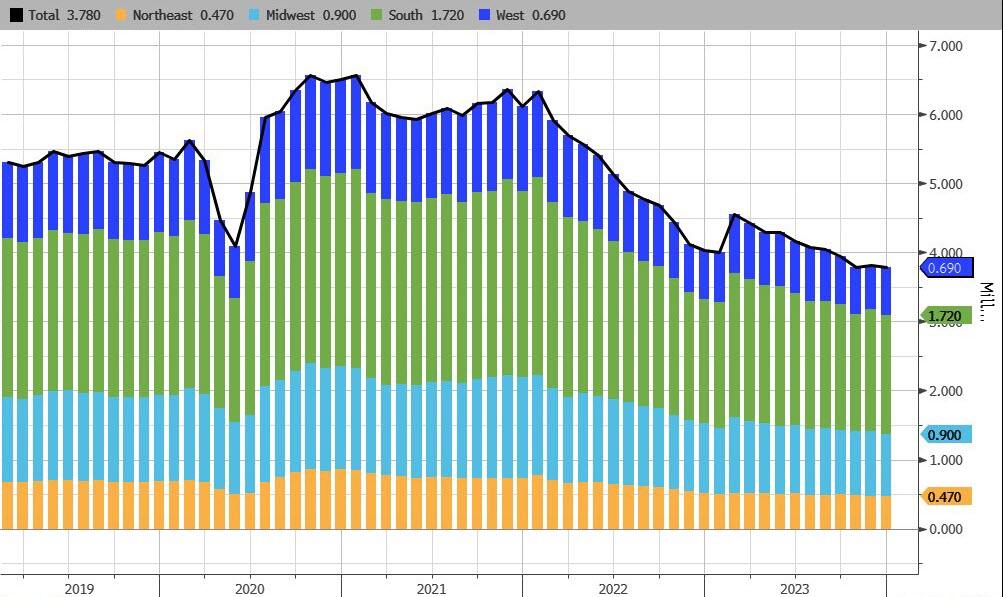

Existing Home Sales were flat in the Northeast, lower in the MidWest and the South, and up marginally in the West (driven by single-family-home sales as condo sales declined)…

Source: Bloomberg

Last month, the number of previously owned homes for sale dropped to 1 million, the lowest since March.

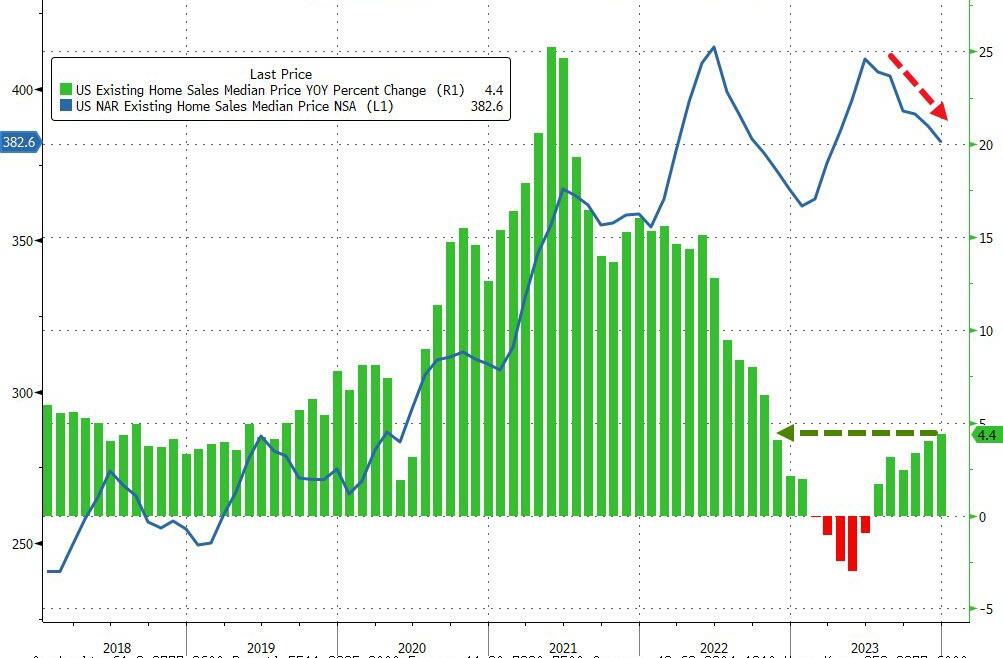

At the current sales pace, selling all the properties on the market would take 3.2 months.

Realtors see anything below five months of supply as indicative of a tight resale market.

That lack of inventory is helping to keep prices elevated.

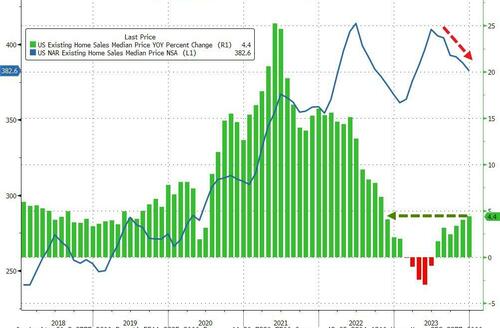

The median selling price climbed 4.4% to $382,600 in December from a year ago, reflecting increases in all four regions. Prices hit a record of $389,800 in 2023.

Source: Bloomberg

But, with mortgage rates having tumbled (and given the lagged responses), are sales about to start rising again?

Source: Bloomberg

So The Fed managed to kill sales, collapse inventories, send home prices higher, destroying affordability… and now what is going to happen?

As only Clueless Joe can do, Biden brags about something that he has nothing to do with: falling mortgage rates.

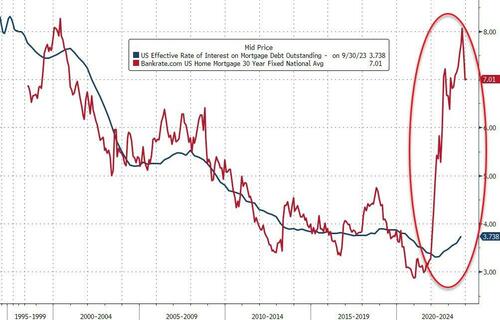

Mortgage rates (30-year conforming rate) are up 392 basis points or a whopping 142% under Biden. Mortgage rates are down from the 2023 peak of 7.83% to 6.69% as of yesterday. One reason that mortgage rates are stable is that M2 Money GROWTH has been negative since the end of 2022.

Of course, it is The Federal Reserve acting to slow down inflation caused by excessive Federal government spending that is leading to mortgage rates declining, not Biden’s open border policy or his green agenda.

But for the future, does Biden know something that we don’t know? Like is Biden buying into the hypothetical Disease X (20 times worse than Covid) that was discussed in Davos at the World Economic Forum. If a major pandemic is unleashed (again) in the election year, The Fed would have to cut rates (again) to offset the damage done by another round of goverment economic shutdowns. Not to mention the shutting down of schools again.

Or did Biden just tell us that he knows the US economy is slipping and The Fed will come riding to the rescue of Biden (or Newsom or Michelle Obama) like in an old John Ford western with John Wayne. That would also lead to declining mortgage rates in 2024.

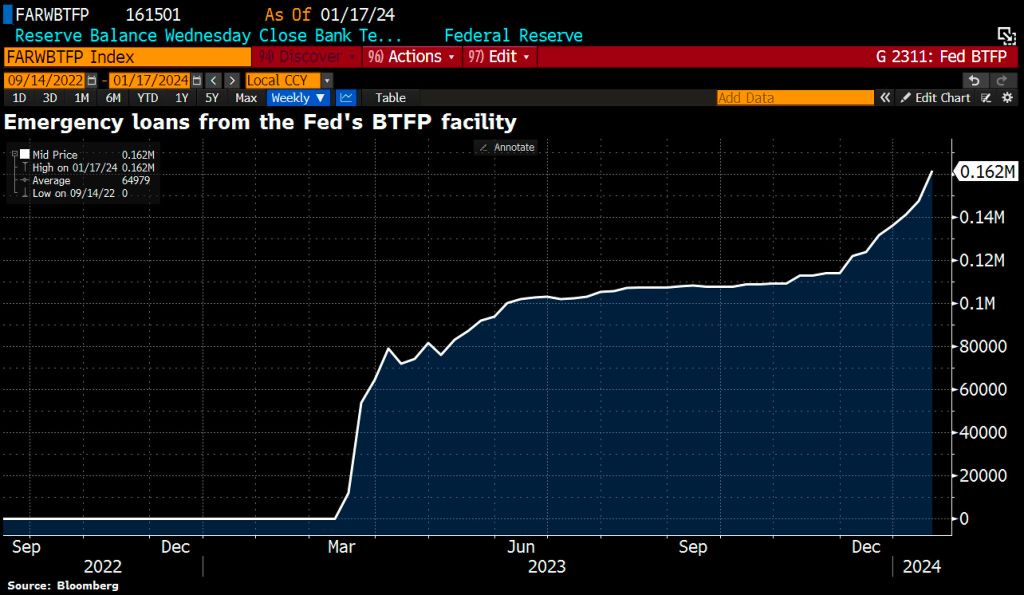

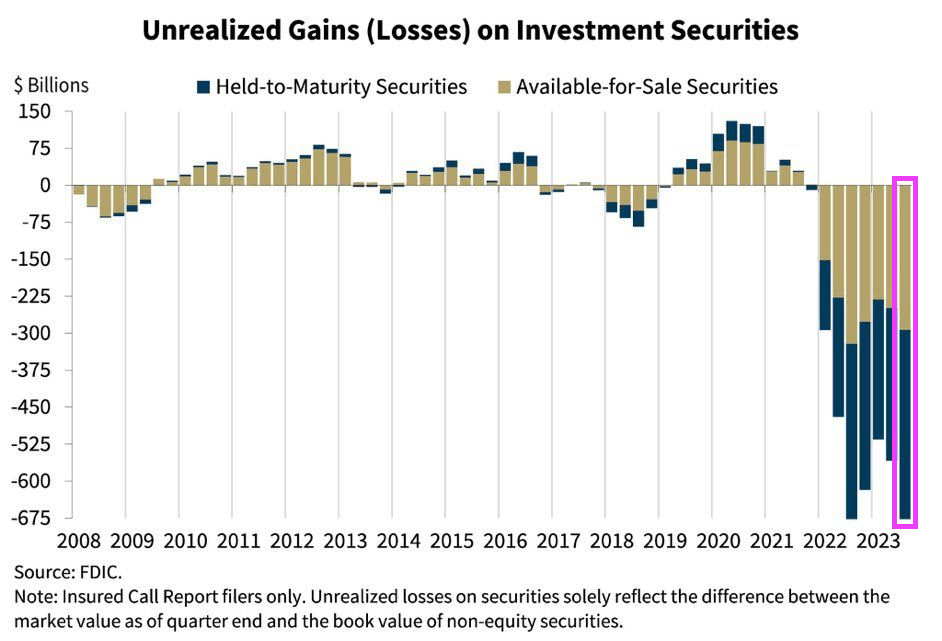

But all is not well in the banking sector. Use of Fed funding tool jumps most since April to fresh record: Banks borrowed record sum of $161.5bn from Fed’s Bank Term Funding Program, w/demand at $14.3bn climbing the most in 9 months as they piled into a reliable arbitrage trade just weeks ahead of its scheduled closure.

The availability of mortgage credit remains VERY TIGHT.

Whether its Disease X (unleashed The Kraken!) or just a slowing economy, The Fed (the master manipulator) will likely cut rates in 2024. Making mortgage rates come down.

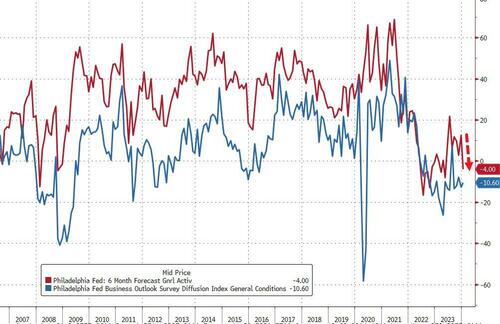

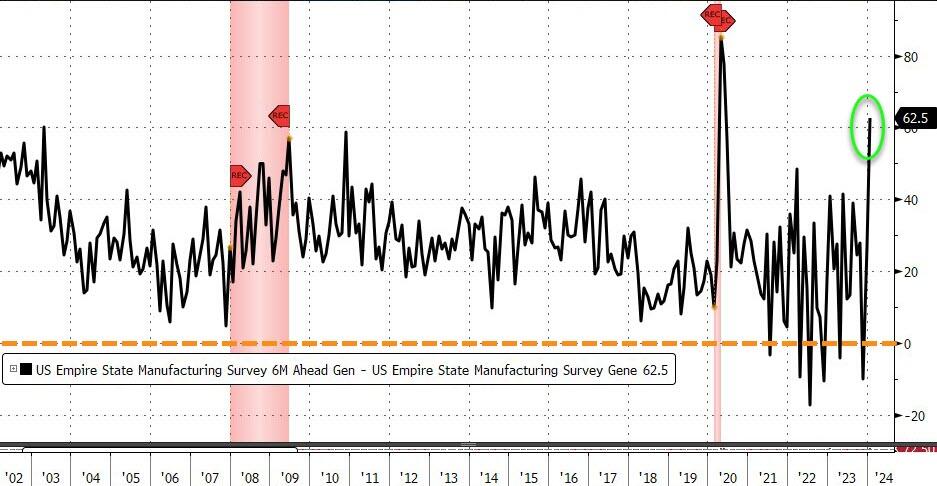

More worrying is the fact that hope appears to be dwindling fast as the six-month-forecast for the survey plunged back into contraction (from +12.6 to -4.00)…

Source: Bloomberg

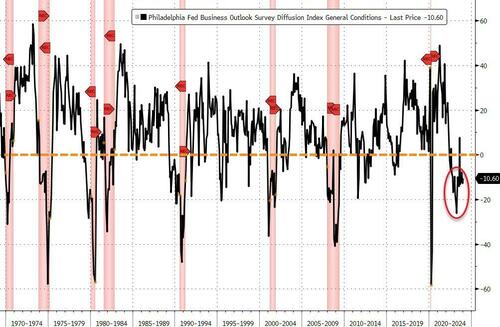

Philly Fed’s demise is consistent with the collapse of hope as ‘soft’ survey data has slumped in the last month, back to its weakest since July (as ‘hard’ data improves relative to expectations)…

Source: Bloomberg

On the bright side for the doves, the dis-inflationary trend remains in tact as priced paid and prices received both plunged in January. However, we highlight the fact that Philly businesses expect price pressure to return in the next six months…

Source: Bloomberg

Overall, the ‘bad news’ in this report should buoy stocks and bonds (lower inflation and lower growth enables sooner and faster cuts)… But will it.

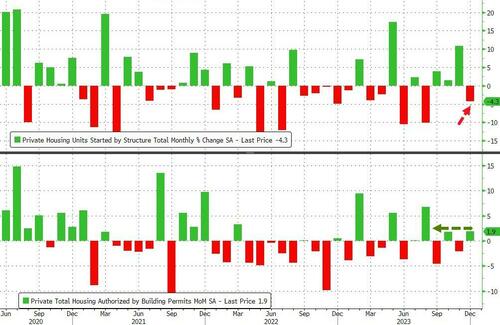

While the Nestea plunge was meant to be refreshing, the housing starts plunge is not refreshing at all. Just another warning about the shortcomings of Bidenomics.

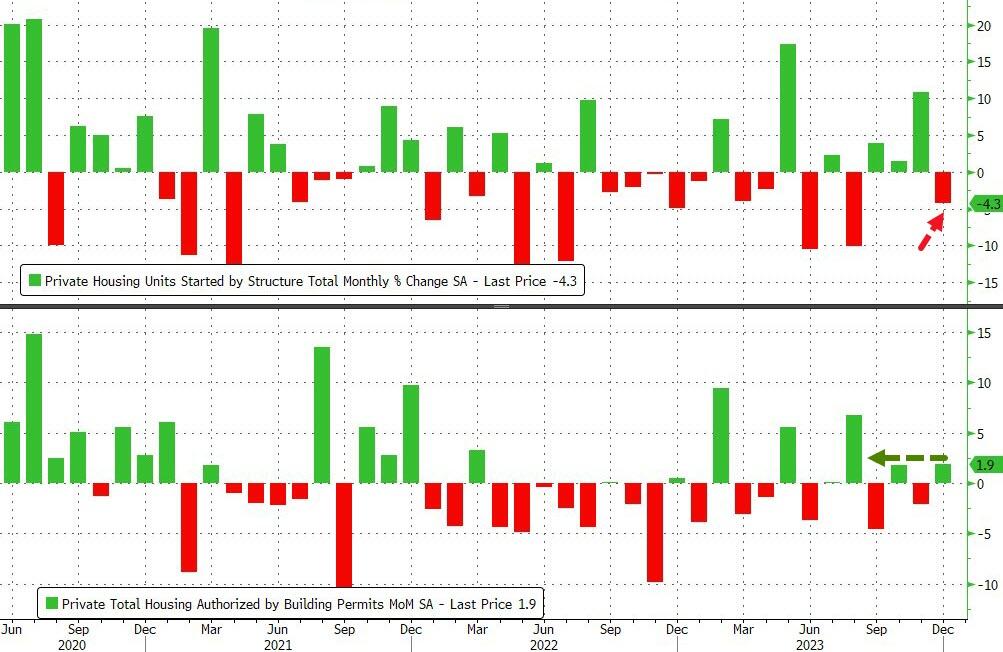

Analysts were right in direction but wrong in magnitude – too bearish. Housing starts declined 4.3% MoM (vs -8.7% MoM exp and +10.8% MoM in November, a big downward revision from the initial +14.8% MoM). Building permits also rose more than expected (+1.9% MoM vs +0.6% exp but saw November’s 2.5% MoM decline upwardly revised to -2.1% MoM…

Source: Bloomberg

On a SAAR basis, Housing Starts and Building Permits are higher YoY

Source: Bloomberg

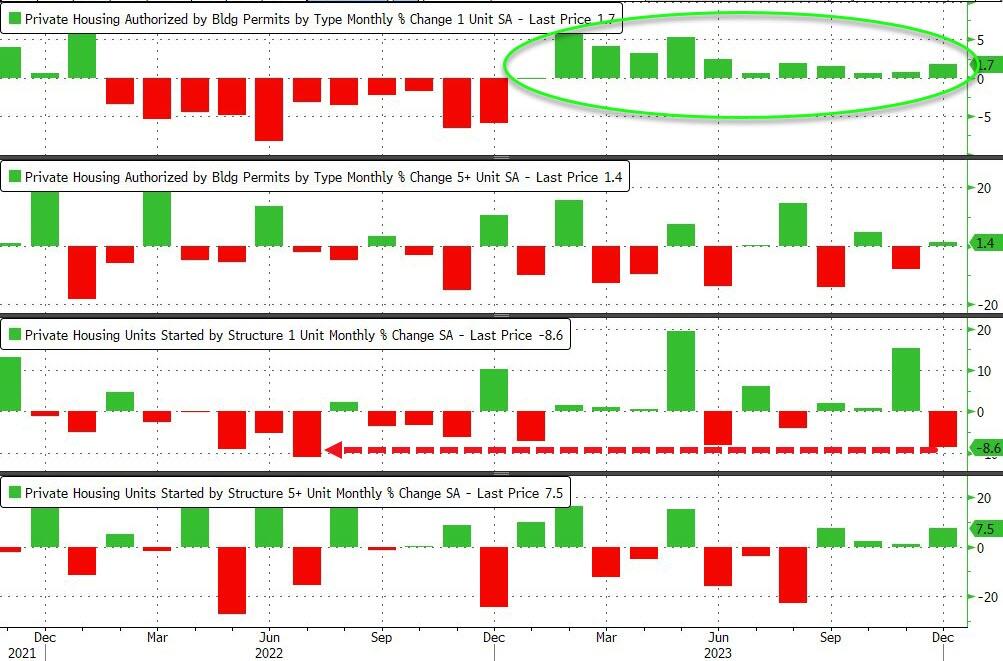

Under the hood, single-family permits rose for the 12th month in a row (i.e. every month in 2023) but single-family home starts plunged 8.6% MoM after surging 15.4% MoM in November… that is the biggest monthly decline since July 2022…

Source: Bloomberg

Perhaps the optimism among homebuilders about future sales is a little overdone given their actions?

Source: Bloomberg

And why would starts be down so much if rates are tumbling?

Source: Bloomberg

Still along way to go for mortgages to be affordable…

Source: Bloomberg

Will less supply of new homes do anything to help the Shelter component of CPI (hint – no!).

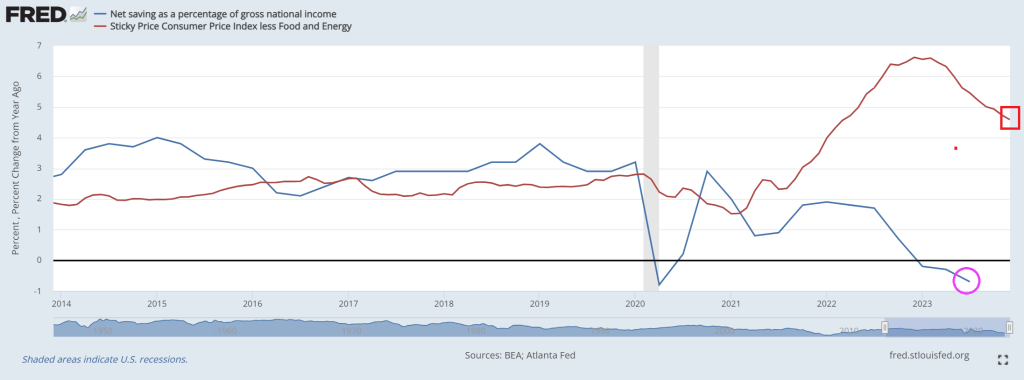

President Biden still shuffles around mumbling about Maga Republicans and defending democracy (while gettig his DOJ and affiliates to prosecute his leading Presidential opponent) even though …. consumers continue to struggle. While Biden is in wonderland, American consumers are in hell.

Savings as a percentage of GDP is actually NEGATIVE as sticky price inflation remains above 4%.

Any good news? At least the US Treasury yield curve (10Y-5Y) is normalizing.

How true!

Speaking of Biden, is this photo real? With AI, I wonder.

The yield on the 10-year Treasury note was recently up 4 basis points at 4.108% after briefly getting to 4.117%, the highest since Dec. 13. The 2-year Treasury yield rose by around 11 basis points to trade at 4.335%.

December’s retail sales data indicated strong consumer demand at the holidays. Retail sales increased 0.6% for the month, above economists’ estimates of 0.4%, as compiled by Dow Jones. Excluding autos, sales rose 0.4%, which also topped a 0.2% estimate.

On Tuesday, yields jumped after comments from Federal Reserve Governor Christopher Waller, who suggested that while the central bank will likely cut rates this year, it may take its time.

At the World Economic Forum in Davos, more European Central Bank members indicated that markets were getting ahead of themselves on rate cut projections.

The president of the Dutch central bank, Klaas Knot, told CNBC Wednesday that the euro zone’s central bank looked at overall financial conditions, and that “the more easing the market has already done for us, the less likely we will cut rates.” Knot was referring to the fact that higher stock and bond prices in the fourth quarter of last year acted as the equivalent of easier interest rate policy, while lower prices act as the equivalent of tighter policy.

Rising interest rates are going to bite a big chunk out of The Fed’s massive ass (I mean balance sheet). Of course, The Fed sends the bill to Treasury. Gee, no wonder Biden/Yellen want so much money!

There is something wrong with letting aging politicians like Biden (81), Grassley (90), Pelosi (83), etc. borrow vast sums of money to spend when they will likely not be around for another 10 years.

You may remember that the Biden administration expected a significant deficit reduction from its tax increases and the expected benefits of its Inflation Reduction Act.

What Americans got was a massive deficit and persistent inflation.

According to Moody’s chief economist, Mark Zandi, the entire disinflation process seen in the past years comes from exogenous factors such as “fading fallout from the global pandemic on global supply chains and labor markets, and the Russian War in Ukraine and the impact on oil, food, and other commodity prices.” The complete disinflation trend follows the slump in money supply (M2), but the Consumer Price Index (CPI) should have fallen faster if deficit spending, which means more consumption of newly created currency, would have been under control. December was disappointing and higher than it should have been.

The United States annual CPI (+3.4%) came above estimates, proving that the recent bounce in money supply and rising deficit spending continue to erode the purchasing power of the currency and that the base effect generated too much optimism in the past two prints. Most prices rose in December, and only four items fell. In fact, despite a large decline in energy prices, annual services (+5.3%), shelter (+6.2%), and transportation services (+9.7%) continue to show the extent of the inflation problem.

The massive deficit means more taxes, more inflation, and lower growth in the future.

The Congressional Budget Office (CBO) expects an unsustainable path that still leaves a 5.0% deficit by 2027, growing every year to reach a massive 10.0% of GDP in 2053 due to a much faster growth in spending than in revenues. The enormous increase in debt will also lead to extremely poor growth, with real GDP rising much slower throughout the 2023–2053 period than it has, on average, “over the past 30 years.”

Deficits are not a tool for growth; they are tools for stagnation.

Deficits mean that the currency’s purchasing power will continue to vanish with money printing and that the real disposable income of Americans will be demolished with a combination of higher taxes and a weaker real value of their wages and deposit savings.

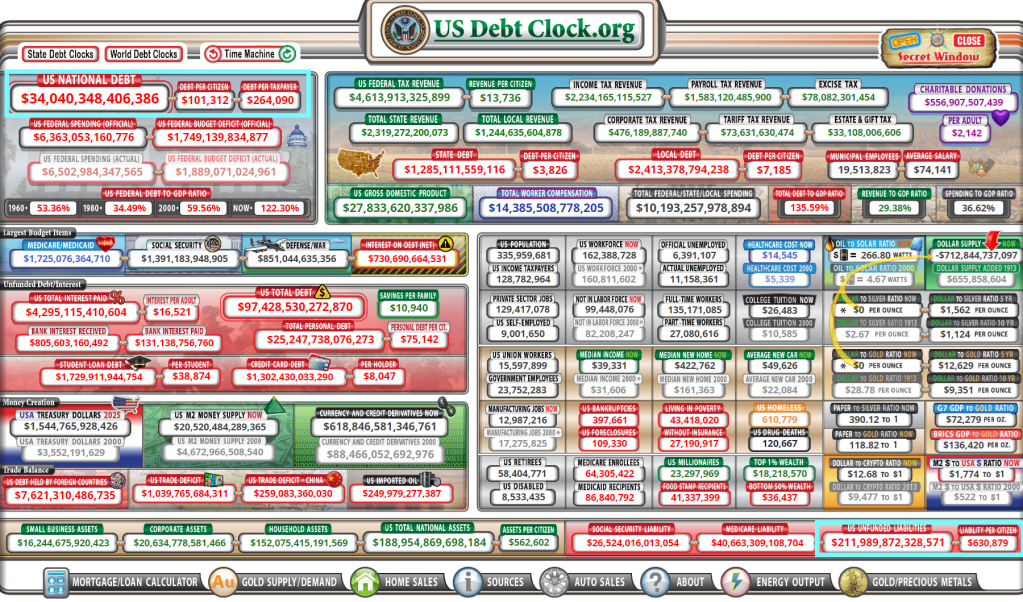

We must remember that, in Biden’s administration’s own estimates, the accumulated deficit will reach $14 trillion in the period to 2032.

Yes, the US has $34 trillion in national debt and $212 trillion in promises made to keep the 99% quiet while the 1% gut the economy for their own wealth. Think Biden, Clintons, and various Congress Critters who suddenly become millionaires.

The Debt Star was born under Obama and weaponized under Biden/Pelosi/Schumer.

Yes, national debt rose under Trump too. Bear in mind that spending originates in The House and Trump was saddled with warhawks like RINO Paul Ryan and insider trading expert and warhawk Nancy Pelosi.

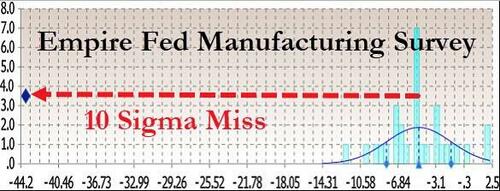

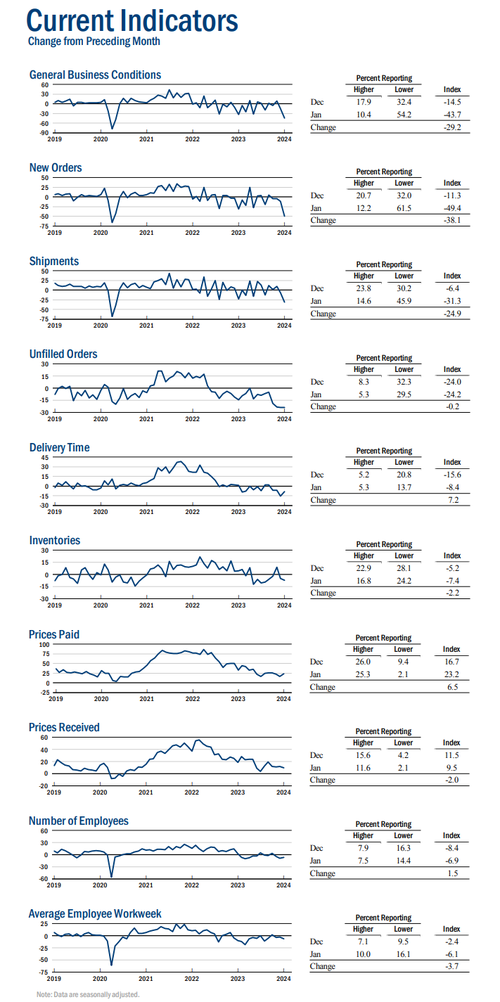

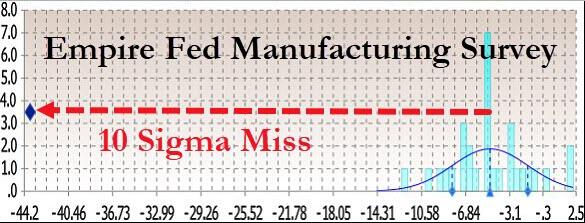

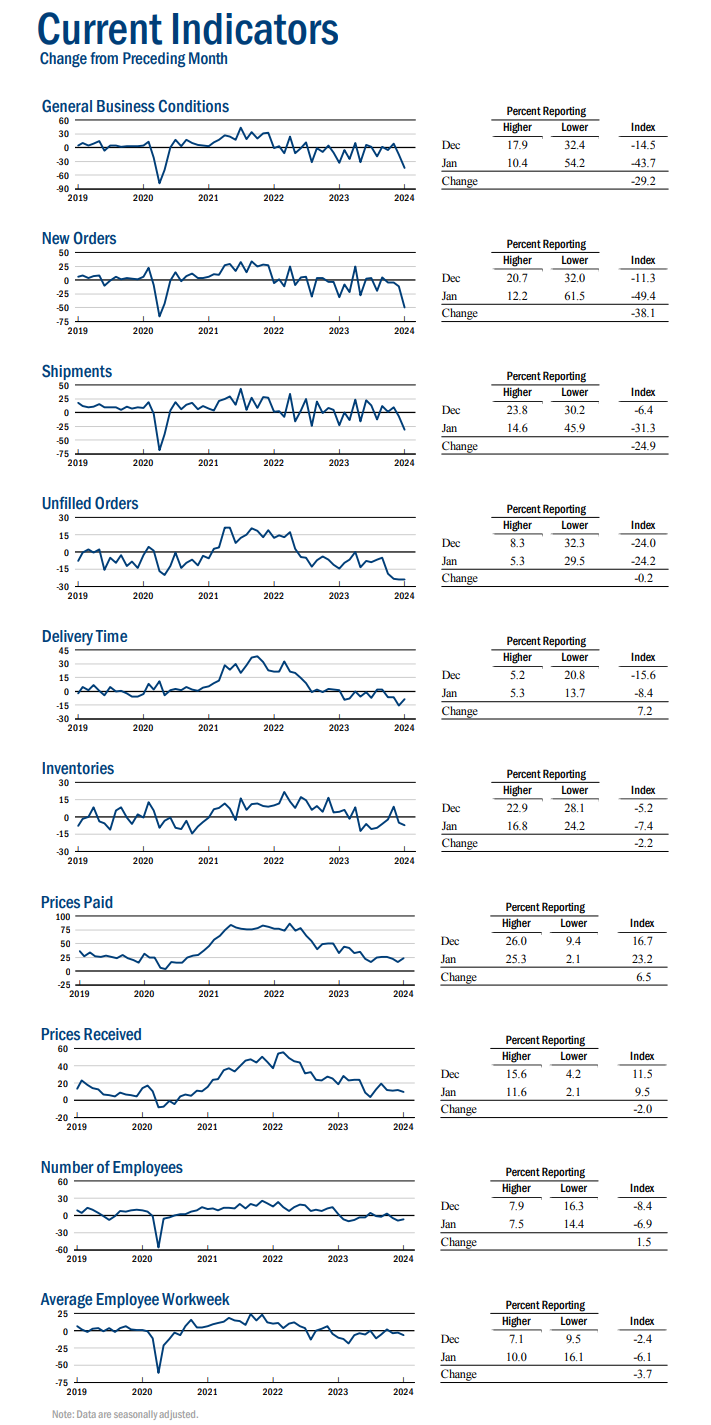

The -43.7 print was a stunning 10 standard deviations below expectations of a bounce to -5.0…

Source: Bloomberg

Under the hood, it was a bloodbath. New orders slumped more than 38 points to minus 49.4, the weakest since April 2020, while shipments dropped by the most since August. Worse still, the index of prices paid for materials increased to a three-month high.

But hope remains high as the six-month outlook for overall activity improved to a three-month high, suggesting manufacturing will stabilize at a weak level. The measure of the outlook for capital expenditures increased to the highest since April 2023, suggesting a pickup in investment.

However, the spread between current reality and a hopeful future is at near record highs (record Ex-COVID-lockdowns)…

Housing is simply unaffordable under Bidenomics, a strange brew of big corporate green subsidies, political handouts (any wonder why Biden is forgiving student loans in an election year?) and bad Fed policy errors.

But young Americans don’t always have a sugar daddy like Hunter Biden has who are willing to pay for rent for political parasites like those in Washington DC.

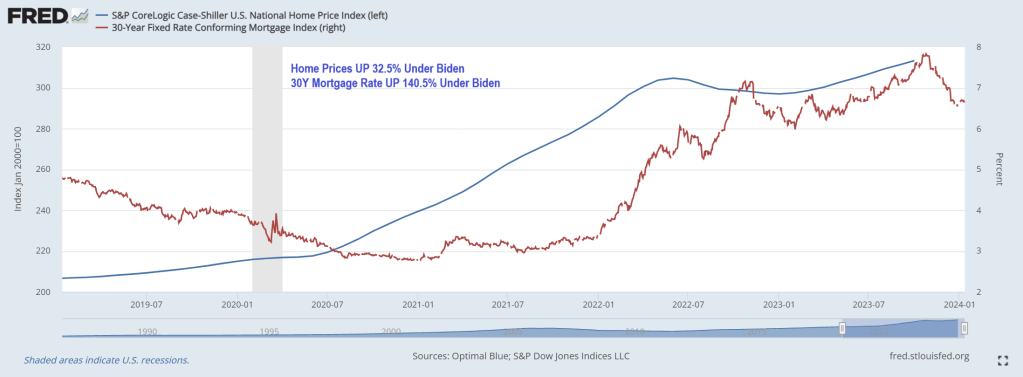

Young adults used to dream of moving out of their parents’ homes and into their own apartments, but living alone has become a luxury not everyone can afford. Not surprising, since home prices under Biden have risen 32.5% while 30-year mortgage rates are up a staggering 140.5% under Clueless Joe.

But in growth terms (year-over-year), White House Propagandists Karine Jean Pierre and John Kirby will no doubt focus on the cooling of housing prices and mortgage rates … although both are reaccelerating.

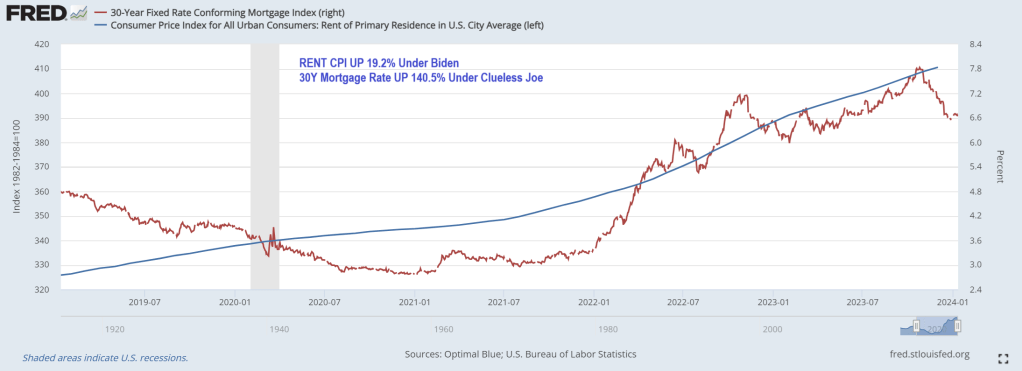

Rent CPI is up 19.2% under Clueless Joe.

How does this impact younger Americans? According to a recent study by Intuit Credit Karma, 31% of Gen Zers are living with their parents because they can’t afford to rent or buy their own place. Overall, 11% of American adults still live at home with their parents.

“The current housing market has many Americans making adjustments to their living situations, including relocating to less-expensive cities and even moving back in with their families,” said Courtney Alev, a consumer financial advocate at Intuit Credit Karma.

Even young adults who live alone are reconsidering their living arrangements because costs are too high.

About a quarter (27%) of Gen Zers reported that they could no longer afford rent and 25% said they’ll have to move back in with family to make ends meet.

Millennials are in the same boat: 30% say rent is unaffordable, and 25% are thinking about moving back in with their parents.

The research is consistent with a 2021 study conducted by the U.S. Census Bureau, which showed that one in three adults ages 18 to 34 live with their parents.

In a 2022 study, Pew Research also found that the percentage of Americans living with their parents has increased steadily since 2000. Pew calls these living arrangements “multigenerational households,” and said young adults ages 25 to 29 are most likely to cohabit with their parents.

Different studies, but all tell the same story: Finances are the top reason young adults are still living with family.

Housing and rental costs rise

It’s hardly surprising that young adults are struggling to make ends meet. Housing costs and living expenses have skyrocketed since the pandemic, and younger generations have faced the most financial hardship.

As Creditnews Research reports, Millennials and Gen Zers have been locked out of homeownership due to rising home prices, elevated interest rates, and stagnant real wages (adjusted for inflation).

For example, in 2023, Millennials accounted for only 28% of homebuyers despite being in their prime home-buying age. Gen Zers barely made a dent in the housing market, accounting for a paltry 4% of all buyers.

According to Fed data, average home prices were $431,000 as of the third quarter of 2023.

The rental market isn’t much better. Although rent costs have declined for three straight months, landlords are still asking for $1,964 per month on average, per Redfin data. Average rents were below $1,650 at the start of Covid.

But the problem of surging rents goes back much longer than that. According to a report from Moody’s Analytics, rent prices grew 135% between 1999 and 2022, while average incomes for all age groups were up 77% over the same period.

In terms of earning potential, younger generations are at the lower end of the totem pole, so they’re more likely to be affected by rising rent prices.

Where’s the “strong economy” everyone always talks about?

While the U.S. economy has steered clear of recession and unemployment remains near historic lows, Americans are still struggling to afford basic expenses. This is especially true for younger generations.

A 2023 study conducted by Deloitte found that more than half of Millennials and Gen Zers were living paycheck to paycheck. Perhaps shockingly, 37% of Millennials and 46% of Gen Z reported taking another part-time or full-time job just to afford their bills.

Working longer hours and barely scraping by is one of the main reasons why younger adults feel they’re worse off financially than their parents were at their age.

An August 2023 study conducted by The Harris Poll found that 74% of Millennials and 65% of Gen Zers believe they are starting further behind financially than previous generations.

“They’re telling us they can’t buy into that American dream the way that their parents and grandparents thought about it—because it’s not attainable,” said The Harris Poll CEO John Gerzema.

Remember, Clueless Joe Biden is in charge!(or Obama, take your pick).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.