As The Fed takes away the massive monetary punch bowl, mortgage rates have risen to the highest since November 2008. And with the withdrawal of monetary stimulus (raising Fed Target Rate), mortgage purchase applications have declined.

Here is a photo of The Federal Reserve fighting the housing and mortgage market.

The monetary noose tightens on the housing and mortgage markets.

Mortgage applications decreased 0.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 2, 2022. They are now the lowest since 1999.

The Refinance Index decreased 1 percent from the previous week and was 83 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was23 percent lower than the same week one year ago.

At least the percentage of adjustable rate mortgages (ARMs) remained the same at 8.5%.

For the sake of the housing and mortgage market, somebody stop Powell and The Gang from tightening!

Joe Biden is the king of malaprops. But his press secretary is just as bad as her boss. Recently, she said that under Biden, there were 10,000 million jobs created. Better known as 10 BILLION jobs created. Not bad, considering that the total population of the US is 333 million. THAT is a hot labor market! /sarc

But seriously, the US U-3 unemployment rate is 3.7% in August, the lowest since Donald Trump was President and BEFORE the Covid outbreak. The Covid economic shutdown saw a surge in the unemployment rate to 14.7% in April 2020 that begat a huge spike in M2 Money growth (22% YoY in May 2022 (green line). Only now is M2 Money growth returning to Trump-era growth rates.

But as The Federal Reserve removes its hefty monetary stimulus, it is unlikely that the unemployment rate will remain low.

In defense of Biden’s press secretary, the US economy saw 10.247 million jobs added under Biden (although while technically correct, even MSNBC wouldn’t give Biden credit for job creation in his first several months as President. Check that. They probably would.

April 2020 saw a decline in US jobs of -20.493 million jobs thanks to the Covid economic shutdowns. BUT with the M2 Money surge, we saw +12.1 million jobs added between May and November 2020 under Trump. Then the US elected China Joe (or Beijing Biden) as President.

The economic shutdowns due to Covid were an economic disaster for millions. But the surge in M2 Money (supporting the various Federal spending programs and inflation) explains the surge in jobs added, not economic wizardry of Biden.

For some reason, Biden and his press secretary failed to mention that inflation is so bad that REAL average hourly earnings YoY are declining at a 3% pace.

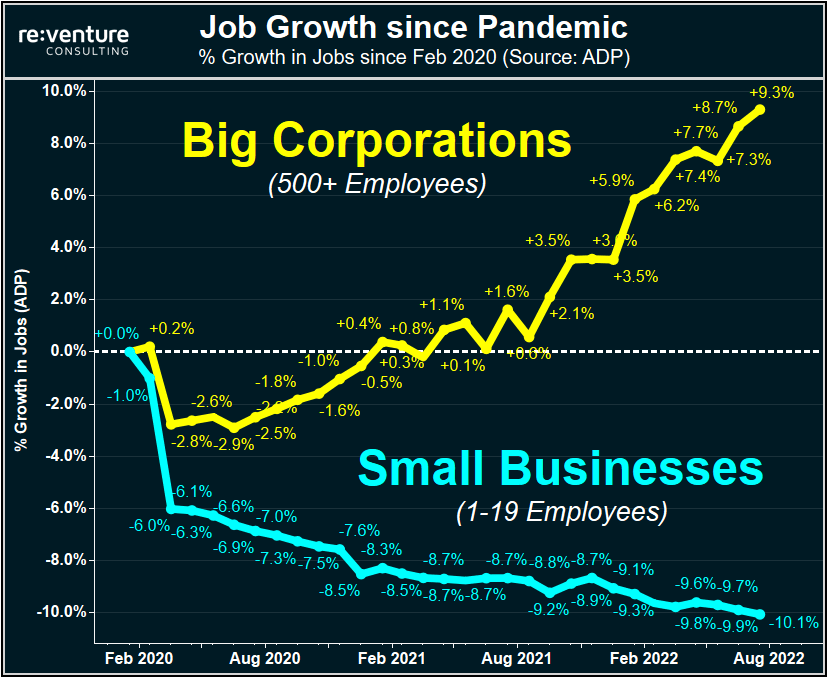

And not surprisingly, job growth has accrued to big corporations and not small businesses.

(Bloomberg)Investors who might be looking for the world’s biggest bond market to rally back soon from its worst losses in decades appear doomed to disappointment.

The US employment report on Friday illustrated the momentum of the economy in face of the Federal Reserve’s escalating effort to cool it down, with businesses rapidly adding jobs, pay rising and more Americans entering the workforce. While Treasury yields slipped as the figures showed a slight easing of wage pressures and an uptick in the jobless rate, the overall picture reinforced speculation the Fed is poised to keep raising interest rates — and hold them there — until the inflation surge recedes.

Swaps traders are pricing in a slightly better-than-even chance that the central bank will continue lifting its benchmark rate by three-quarters of a percentage point on Sept. 21 and tighten policy until it hits about 3.8%. That suggests more downside potential for bond prices because the 10-year Treasury yield has topped out at or above the Fed’s peak rate during previous monetary-policy tightening cycles. That yield is at about 3.19% now.

Then we have Bankrate’s 30-year mortgage rate soaring on Fed intervention expectations.

Inflation? US inflation is near its highest in 40 years and the USDollar Plain Vanilla Swap was at 0.50 when Biden first took office as President and is now 3.371 (quite an increase!).

Here is an interesting chart of FNCL 2% Agency MBS.

The August jobs report is out. 315k jobs were added, which was considerably higher than the ADP jobs added report of 132k. Hmm.

Be that as it may, US Average Hourly Earnings YoY remained at 5.2%. That’s a shame since the last inflation report had US inflation at 8.5%. That translates to REAL Average Hourly Earnings YoY of … -3.3%.

Labor force participation rose to 62.4%.

This is a decent jobs report and will likely lead The Fed to continue raising rates, particularly when The Fed sees that multiple jobholders has increased to cope with inflation.

The ADP National Employment Report SA Private Nonfarm Level Change printed this morning confirming what most of us already knew … the US economy is slowing if not already in recession.

The ADP jobs added grew by only 132k in August as The Fed’s M2 Money growth slowed.

Since The Federal Reserve and Federal government overstimulated the economy when Covid surfaced in early 2020, The Fed’s balance sheet expanded to near $9 TRILLION which helped existing home sales median price YoY hit 25.2% in May 2021 but falling to 10.8% YoY in July 2022 as The Fed tightened rates.

It will be a monetary inferno if The Fed decides to actually unwind its $9 trillion balance sheet.

US home price growth is decelerating as The Federal Reserve let’s some of the air out of the monetary tires.

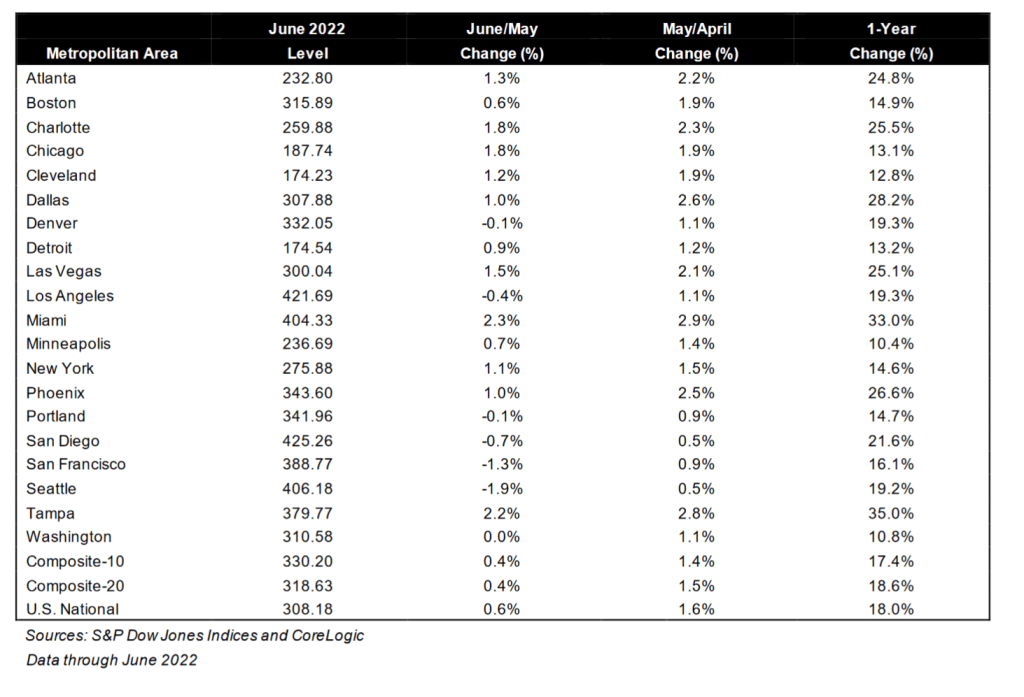

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported an 18.0% annual gain in June, down from 19.9% in the previous month. The 10-City Composite annual increase came in at 17.4%, down from 19.1% in the previous month. The 20-City Composite posted an 18.6% year-over-year gain, down from 20.5% in the previous month.

Tampa, Miami, and Dallas reported the highest year-over-year gains among the 20 cities in June. Tampa led the way with a 35.0% year-over-year price increase, followed by Miami in second with a 33.0% increase, and Dallas in third with a 28.2% increase. Only one of the 20 cities reported higher price increases in the year ending June 2022 versus the year ending May 2022.

While the Case-Shiller National home price index slowed to 18% YoY in June, the median price for existing home sales slowed to 10.55% YoY in July as The Fed’s M2 Money growth YoY slowed to 5.28% and Freddie Mac’s 30yr mortgage rate rose to 5.3%.

Bear in mind that Case-Shiller is lagged compared to the existing home sales numbers. Much like the New York Yankees manager picking the hottest batter in June to start in September. The Yankees traded poor-hitting Joey Gallo to the LA Dodgers to supplement poor-hitting Cody Bellinger.

In any case, as of June 2022, the 20 metro areas covered by Case-Shiller all grew in price in double digits with alligator-infested Tampa and Miami FL in the 30% rate, rattlesnake-infested Dallas is in 3rd place at 28.2%. Phoenix AZ, where I used to live, slowed to 26.6%. Yes, I had rattlesnakes on my property (a nest of Mohave Rattlers) and a large Diamond-backed Rattler behind my house).

Let’s see how housing holds up with more Fed monetary tightening. Fed Chair Powell is predicting “pain.”

As inflation burns the US middle class and low wage workers, The Federal Reserve reaffirmed at Jackson Hole that they are the NEW Smoky The Bear (only The Fed can fight inflation fire!) But of course, Federal spending and energy policies can drive up prices too.

Having said that, the 2-year Treasury yield and 30yr mortgage rate are rising rapidly.

The Fed is trying to cool demand by raising rates after lax monetary policy since late 2008.

While the US 2-year Treasury yield is up only slightly today, the Eurozone is seeing their 2-year sovereign yields spiking by 11-15+%.

I remember appearing on Fox Business’ Varney and Company about The Federal Reserve. When Stuart Varney asked me what will happen when The Fed finally removes the monetary stimulus, I made an explosion gesture. Well, its starting to happen.

(Bloomberg) The rally that’s bolstered risk assets over the past month was just a blip in a bear market that’s likely to worsen from here.

That’s the view of investors who seem to be finally getting the message that a resolutely hawkish Federal Reserve and central bank peers are planning to raise interest-rates at all costs to combat the hottest inflation in a generation.

Monday’s trading give credence to that prospect: equities, developed and emerging-market currencies and even haven Treasuries tumbled as fund managers digested Fed Chair Jerome Powell’s stern message that rates would keep going up even if it spells pain for households and businesses everywhere.

“The environment has changed,” said Kim Fournais, founder and chief executive of Saxo Bank A/S. “I just have a hard time seeing how this market, that is still trading close to all-time highs, can stay at those levels. There will be a period of great volatility.”

Goldman Sachs Group Inc. pegs the dollar as the main beneficiary amid the market chaos, Westpac Banking Corp. warns of fresh yen pressure and BNP Paribas Wealth Management sees more losses for developing-nation assets.

Almost every equity benchmark tumbled in Asia trading Monday as the fallout from the Fed’s hawkish rhetoric ripped through markets. S&P 500 futures dropped as much as 1.3%, indicating that US stocks are poised to extend a rout that saw the index erase $1.2 trillion on Friday.

Yields on two-year Treasuries jumped to the highest since 2007 as traders ratcheted up rate hike bets, while the yen hurtled toward the closely-watched 140 level. The risk-sensitive Korean won led losses among emerging peers, tumbling to a 13-year low.

Oddly, the Fed Funds Futures market wasn’t rattled by Powell’s announcement at Jackson Hole. The Fed’s target rate is 2.50% and is expected to rise to 3.863% by March then cool-off. The Cleveland Fed’s Mester said 4% then keeping it at 4% for an extended period of time.

But it is in Europe where Lagarde and company where the REAL action was. The ECB’s target rate is at 0% with a negative effective rate of -0.08%. But the ECB is expected to keep raising their target rate to 2.136% by July 2023.

Sovereign yields are rising across the board. Except for jolly old England.

Global equity futures are down across the board as well. But not like Friday’s plunge.

It is amazing that Biden is rising in the polls, simply because he got several inflation-generating, crony pay-off bills passed through a Democrat-controlled Congress. Even more amazing is that Americans aren’t more furious with Biden given that inflation is still raging at 8.5% YoY and the US Personal Savings Rate to cope with raging prices is at -51.5% YoY.

It looks like one quick fix to the inflation problem is for The Federal Reserve to shrink its balance sheet. But they are taking their own sweet time doing it.

And then we have the S&P 500 index which has done poorly since Powell and The Fed have undertaken their “fight inflation” mantra caused by their own folly and Biden’s green, anti-fossil fuel policies. Not to mention Congress spending like drunken sailors in port.

But the same is going on in Europe where inflation is even higher than in the USA and the EUR/USD is plunging like a paralyzed falcon.

And then we have Biden shrinking the Strategic Petroleum Reserve (orange line).

And in Europe, we have Germany suffering through a horrible energy price spike.

You must be logged in to post a comment.