Huey Lewis and the News said it best about ESG goals: “The elites want a new drug.”

The World Economic Forum (WEF) is a leading pusher of the ESG drug, pushed by the elite class intending to control the world. Unfortunately, numerous American politicians and influencers have attended the Davos meetings and have openly praised the WEF and its leader Klaus Schwab.

ESG refers to the environmental, social and governance information about a firm. There is growing evidence that companies that take their environmental and social responsibilities seriously perform better financially. This has naturally made investors sit up and take notice.

ESG investing, or sustainable responsible investing (SRI), uses this information about a company to inform investment decisions that prioritize all stakeholders.

Here’s how the Forum’s partners are leading the switch to stakeholder capitalism.

There are 3 pillars to ESG and sustainable investment. This reminds me of the 10 pillars (or planks) of Marxism. So ESG is Marxism with a different name, but the end result is the same. Big government control.

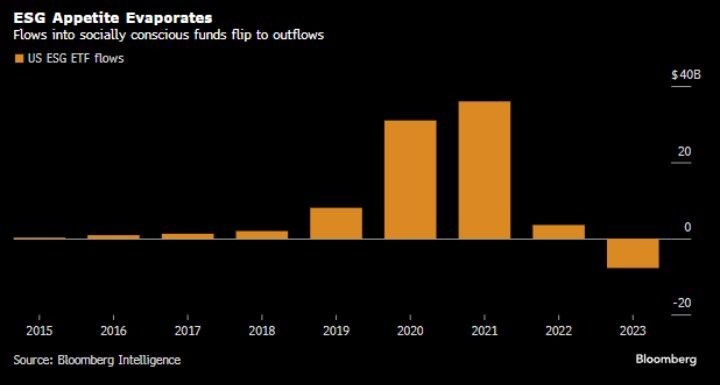

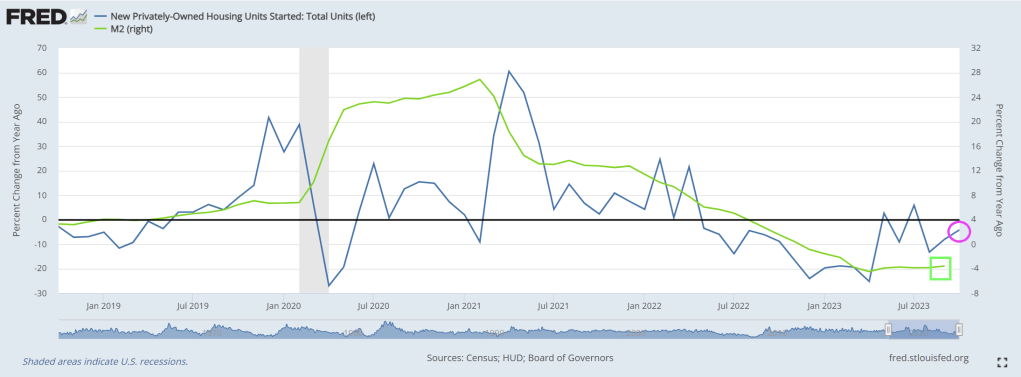

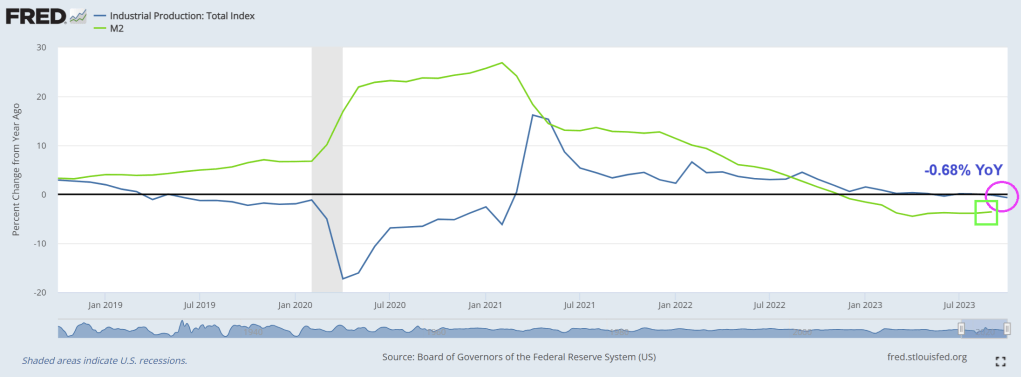

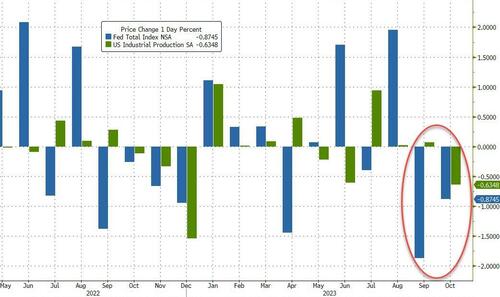

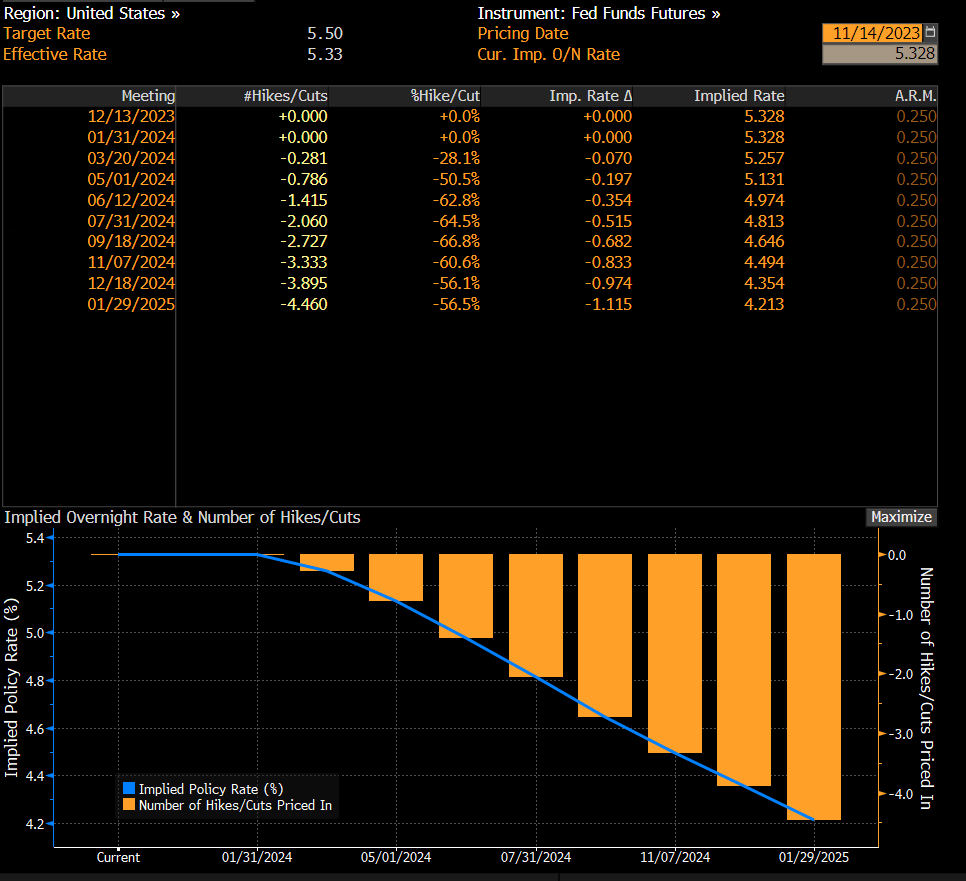

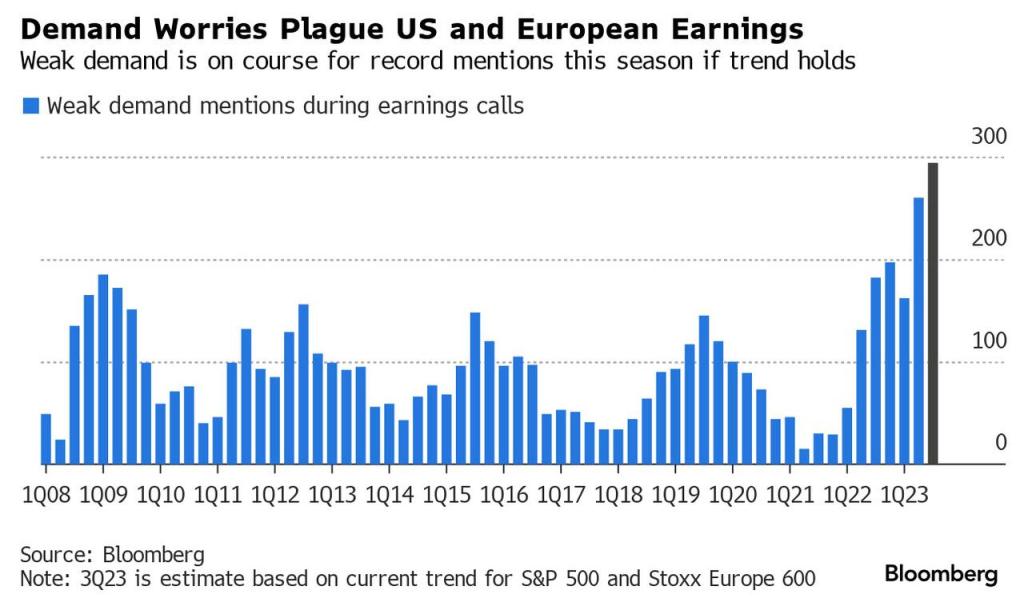

But all is not well with WEF’s ESG drug distribution. In fact, ESG flows into socially consious funds were a big thing during Covid (2020) and the first year of Biden’s Reign of Error. But ESG flows slowed sharply in 2022 and seeing net outflows in 2023.

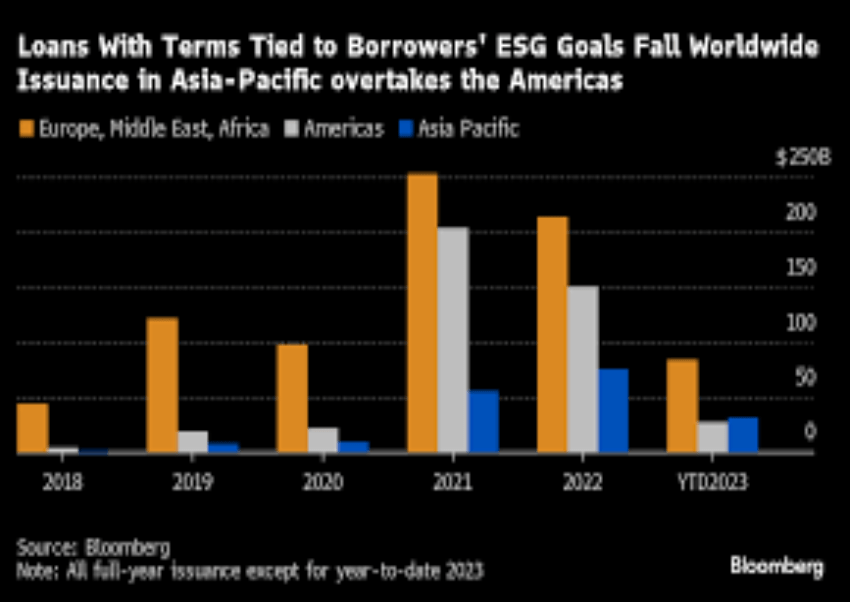

Issuance of sustainability linked loans is down 80% in the US.

US borrowers are retreating en masse from the world’s second-biggest ESG debt class.

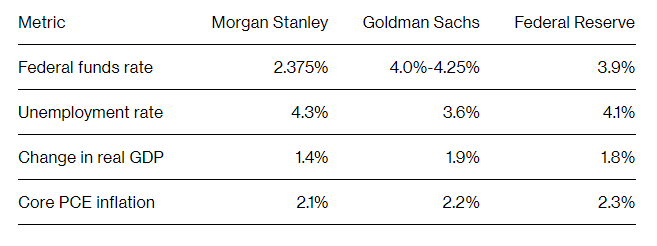

The $1.5 trillion market for sustainability-linked loans, in which borrowing is tied to environmental, social or governance goals, has seen an overall slowdown in volumes this year as both interest rates and greenwashing fears rise. But nowhere has the decline been as precipitous as in the US, where the number of new sustainability-linked loans is down 80% from a year earlier.

But ESG is still relatively popular in Europe, Middle East and Africa (orange). But taste for ESG is waning around the globe. But the selection of Biden as President in the US marked a surge in ESG -tied loans in 2021 and 2022 (not to mention the insane levels of spending out of Biden and Congress, much tied to the sustainability, green energy fantasy.

Loans with terms tied to borrower’s ESG goals have fallen worldwide.

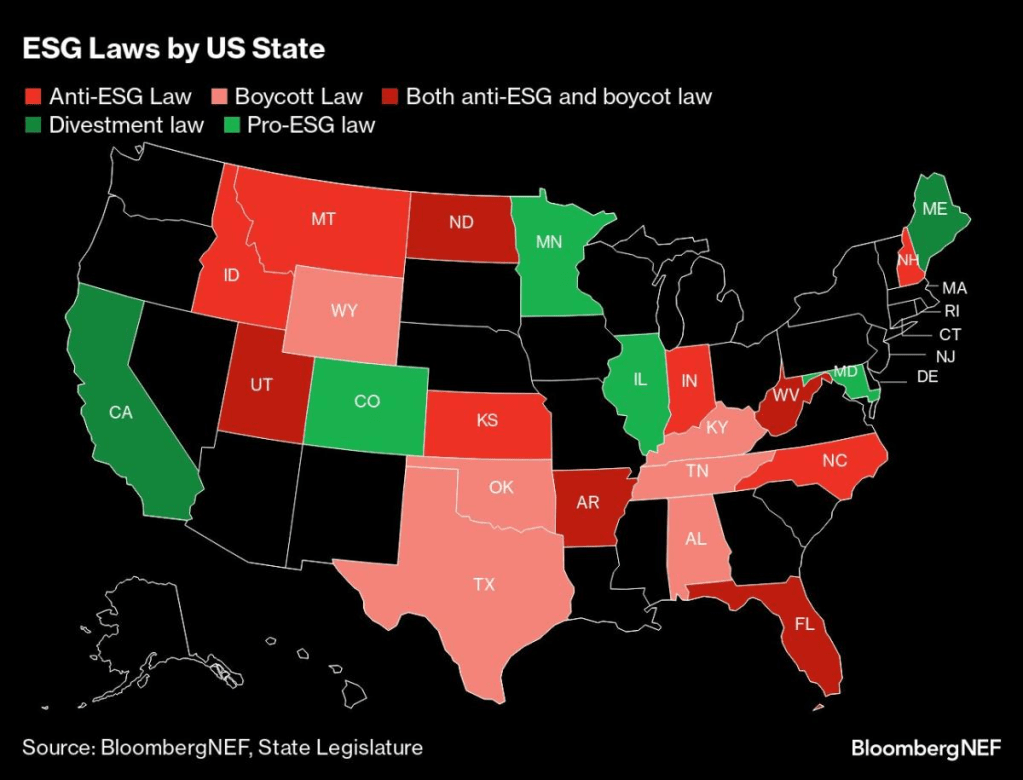

Several states (largely blue states like California, Minnesota, Illinois, and Colorado have pro-ESG laws) while several states have anti-ESG laws (largely red states like Montana, Idaho, North Dakota, Kansas, Utah, Indiana, Arkansas, Florida, and West Virginia).

And of course, global warning may not be as dire as John Kerry and Greta Thunberg say.

WEF’s Klaus Schwab about to get sniffed by his 80-year old puppet, Joe Biden. In fact, Biden is singing “I’m your puppet.”

Here is Hunter Biden welcoming the Green Energy fairy and all the trillions in misallocated spending it brings.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.