I am anxiously waiting for the US inflation report tomorrow, so I am just looking at the US Treasury yield curve, mortgage rates and cryptos today.

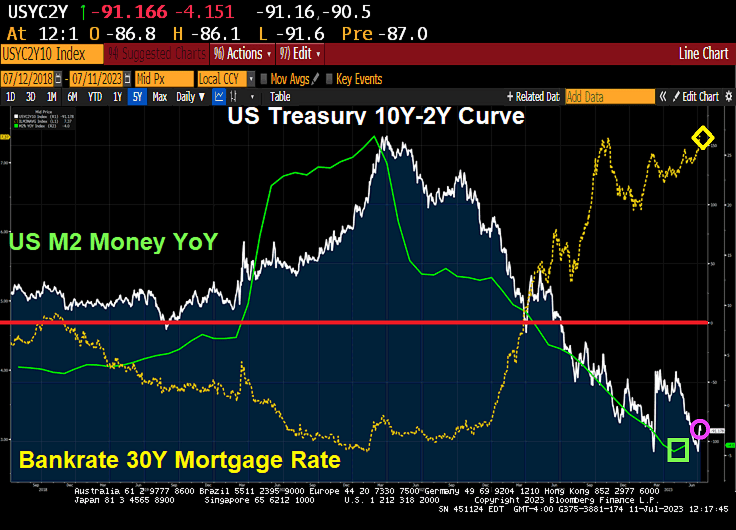

The US Treasury 10Y-2Y yield curve stumbled (just like Biden and Bidenomics) to -91.166 basis points as the turnaround in M2 Money growth has stalled. Bankrate’s 30Y mortgage rate is up to 7.37%, that is UP 156% under Bidenomics.

Bitcoin is down today. At least Solana is up.

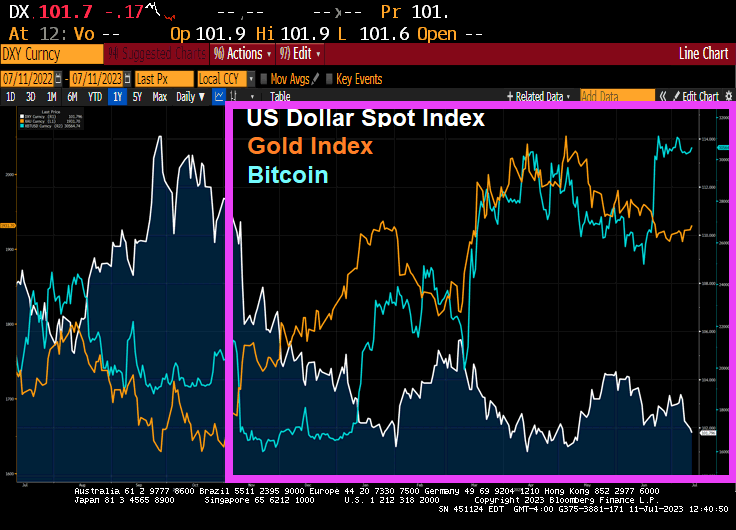

Since November 3, 2022, the US Dollar Index is DOWN -9.68%, Gold is UP 18.55% and Bitcoin (Elizabeth Warren’s latest obsession) is UP 51.11%.

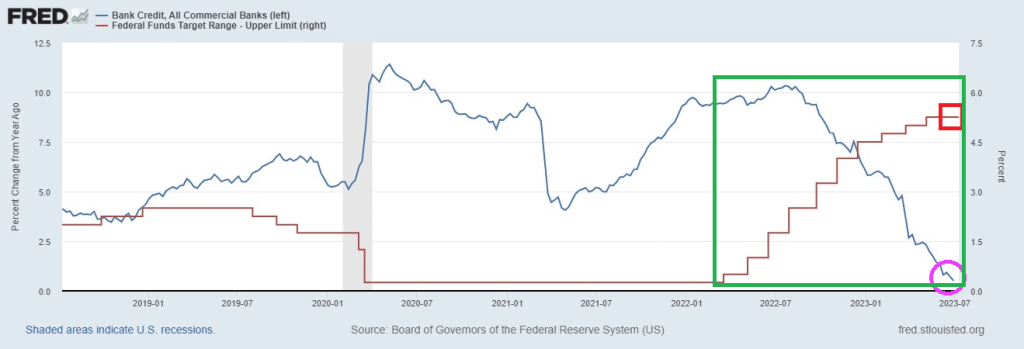

Bidenomics relied of massive Federal spending thanks to Covid and massive monetary expansion. This led to the highest inflation in 40 years (Bidenflation). But now The Fed is slowing M2 Money growth into negative territory and hiking their target rate.

The result? Bank credit growth has crashed to 0.5% YoY. In other words, banks are no longer expanding credit for the first time since the aftermanth of The Great Recession and Financial Crisis of 2008/2009. Of course, Washington DC bailed out their bestest buddies, the banks, while middle America suffered.

As America loses steam under Biden and The Fed, 41+ countries have signed on to the BRICs gold-backed reserve currency. Unlike the USA with its fiat currency (backed by Babbling Biden and Janet “The Midget Marxist” Yellen), this reserve currency will be backed by gold.

The US has passed the 32 trillion mark in national debt, and is going much, much higher. More like 32 tons on the back of taxpayers. When we add unfunded liabilities like Social Security, Medicare and Medicaid, the tab soars to $224.5 TRILLION.

In the first six months of 2023, there were 340 corporate bankruptcies, topping every other comparable span in 13 years, according to S&P Global Market Intelligence. This is up 93 percent from the same time a year ago and higher than in 2020, when there was a spike during the early days of the coronavirus pandemic.

There were 54 recorded corporate bankruptcy filings in June, unchanged from the 54 bankruptcies in May. Last month, some of the most notable companies to submit filings were Lordstown Motors, Rockport Co., Instant Brands Acquisition Holdings, and iMedia Brands.

“Lordstown Motors Corp. filed for bankruptcy June 27, with plans to restructure its business and seek a buyer, according to a company release. The electric vehicle manufacturer’s assets include its Endurance pickup truck and related resources,” S&P noted in the July 6 report.

“Instant Brands Acquisition Holdings Inc. also sought bankruptcy protection June 12. The tightening of credit terms and higher interest rates had impacted the company’s liquidity levels, according to an official release. The company has also already secured $132.5 million from existing lenders and plans to continue discussions with its financial stakeholders.”

Year-to-date through June, 15 companies with more than $1 billion in liabilities filed for bankruptcy, such as Cyxtera Technologies, Diebold Holding, Bed Bath & Beyond, Diamond Sports Group., and Party City.

Epiq Bankruptcy, a U.S. bankruptcy filing data provider, confirmed that 2,973 total commercial Chapter 11 bankruptcies were filed in the first half of 2023, up 68 percent from the same period in 2022.

Higher Interest Rates Impacting Businesses

Banking experts purport that higher interest rates are the leading cause of the increase in corporate bankruptcies. Many businesses either maintain vast debt loans that will require refinancing or need more liquidity to stay afloat.

“The increase in commercial and individual bankruptcy filings during the first half of 2023 underscores the economic challenges faced by businesses and individuals,” said Mr. Gregg Morin, Vice President of Business Development and Revenue at Epiq Bankruptcy, in the report. “Our objective is to provide bankruptcy professionals with timely and accurate data necessary for analyzing stakeholder volumes and trends for making informed business decisions.”

The situation could be exacerbated should the Federal Reserve pull the trigger on two more rate hikes this year. The futures market is penciling in a quarter-point boost to the benchmark fed funds rate at this month’s Federal Open Market Committee (FOMC) policy meeting.

Meanwhile, according to a recent Fitch Ratings report, the corporate default rate is projected to climb to as high as 4.5 percent in 2023, up from the previous forecast low of 2.5 percent. The updated projections reflected “the tighter lending conditions and capital access resulting from stress in the banking sector and inflation uncertainty.”

However, some argue that corporate bond market indicators are “less ominous.”

“The interest rate differentials, or spreads, between the 10-year U.S. Treasury note and investment grade (IG) and high yield (HY) corporate bonds continue to hover within their average width over the past 25 years, a bond market signal indicating the likelihood of a less severe recession, with traders pricing in fewer corporate defaults,” wrote John Lynch, the CIO at Comerica Wealth Management, in a research note.

Economists contend that the worst corporate bankruptcies typically occur one or two years into a recession. Today, they are happening before the official start of an economic downturn as the U.S. economy is still expanding.

What’s happening?

“Simple,” says Mr. Pete St. Onge, a Heritage Foundation economist, “banks aren’t lending.”

“Banks are battening down the hatches, hogging their bailout money instead of lending it out,” he said in a recent podcast. “That credit crunch means not only do we get bankruptcies like in any recession, on top of that, we get a lending wall that cuts off even the healthy businesses. Of course, their jobs go down with them.”

Since the Federal Reserve launched the Bank Term Funding Program (BTFP) following the Silicon Valley Bank collapse in March, financial institutions have kept tapping into these emergency lending facilities. After hitting a record high at above $103 billion at the end of June, it remains elevated at $102 billion.

32.5 trillion in debt and $192 trillion in unfunded liabilities which means a total of $224.5 total debt + liabilities.

This is Bidenomics. Spend trillions, borrow trillions, promise entitlements. Rinse, repeat.

Bidenomics, the massive Federal spending spree that helped drive inflation to 40 year highs, is the most top-down Soviet-style command economy model imaginable.

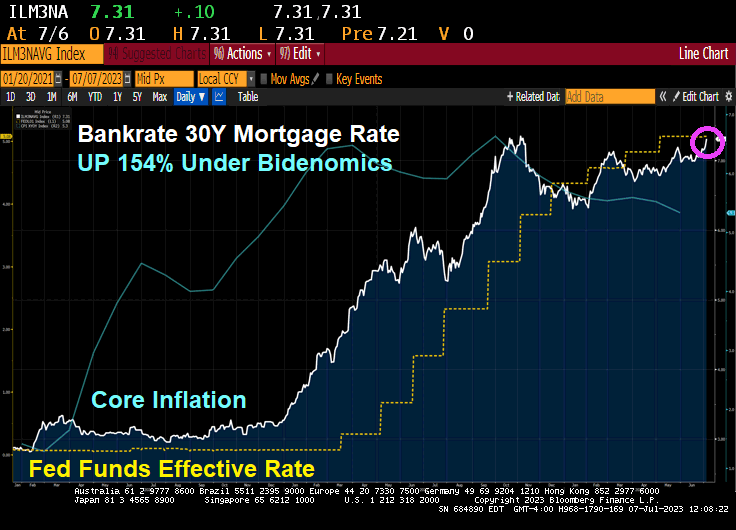

As The Fed battles Bidenflation, the 30-year mortgage rate has now risen to 7.31%, a far cry from 2.88% when Biden was installed as President. That is a 154% increase in the 30-year mortgage rate under Bidenomics.

Biden’s massive spending spree (aka, Build Back Better) has a new name: Build Back Bankrupt!

According to Epiq, Commercial Chapter 11 Filings Increased 68 Percent in the First Half of 2023.

NEW YORK – July 03, 2023— The 2,973 total commercial Chapter 11 bankruptcies filed during the first six months of 2023 represented a 68 percent increase over the 1,766 filed during the same period in 2022, according to data provided by Epiq Bankruptcy, the leading provider of U.S. bankruptcy filing data. Individual Chapter 13 filings increased by 23 percent during the same period.

Overall commercial filings registered 12,107 for the first half of 2023, representing an 18 percent increase from the commercial filing total of 10,258 for the first half of 2022. Small business filings, captured as Subchapter V elections within Chapter 11, totaled 814 in the first six months of 2023, a 55 percent increase from the 525 elections during the same period in 2022.

Overall commercial filings increased 12 percent in June 2023, as the 2,123 filings were up from the 1,891 commercial filings registered in June 2022. The 404 commercial Chapter 11 filings in June represented a 9 percent increase from the 371 filings in June 2022. Total Subchapter V elections within Chapter 11, experienced a 111 percent increase from 94 in June 2022 to 198 in June 2023.

“The increase in commercial and individual bankruptcy filings during the first half of 2023 underscores the economic challenges faced by businesses and individuals,” said Gregg Morin, Vice President of Business Development and Revenue at Epiq Bankruptcy. “Our objective is to provide bankruptcy professionals with timely and accurate data necessary for analyzing stakeholder volumes and trends for making informed business decisions.”

Total bankruptcy filings were 217,420 during the first six months of 2023, a 17 percent increase from the 185,352 total filings during the same period a year ago. Total individual filings also registered a 17 percent increase, as the 205,313 filings during the first half of 2023 were up from the 175,094 filings during the first six months of 2022. The 85,390 individual Chapter 13 filings in the first half of 2023 represent a 23 percent increase over the 69,367 filings during the same period in 2022.

All chapters increased in June 2023 compared to June 2022, with 37,700 total bankruptcy filings representing an increase of 17 percent from the 32,198 filed in 2022. Total commercial filings were up 12 percent from 1,891. Total Individuals were up 18 percent from 30,307.

While not the Epiq data, the Bloomberg Corp Bankruptcy Index shows the rise in bankruptcies as The Fed fights Bidenflation.

What is Bidenomics? It isn’t what Press Secretary Karine Jean Pierre thinks. She said Biden hates “trick down economics”. Instead, Biden prefers a Soviet-style command economy where The Federal Government spends trillions of dollars and directs where the money goes. We also have the Socialist Federal Reserve that relies on rate manipulation to achieve policy results.

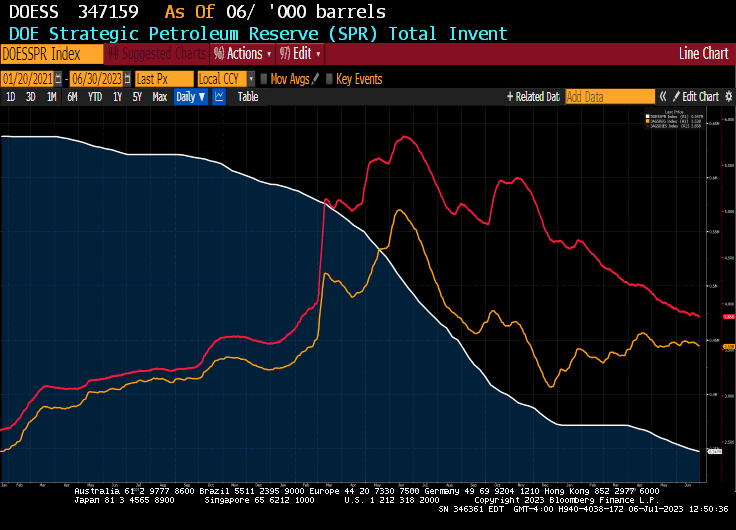

A good example of Biden’s Soviet-style “Bidenomics” is his use of the Strategic Petroleum Reserve (SPR). Biden has now drained almost 50% of the SPR from when he was sworn in as President. And has drained the SPR for 14 straigth weeks to manipulate gasoline and diesel fuel prices in an effort to lower fuel prices ahead of the 2024 Presidential election. Watch Biden suddenly stop caring about fuel prices once he wins reelection!

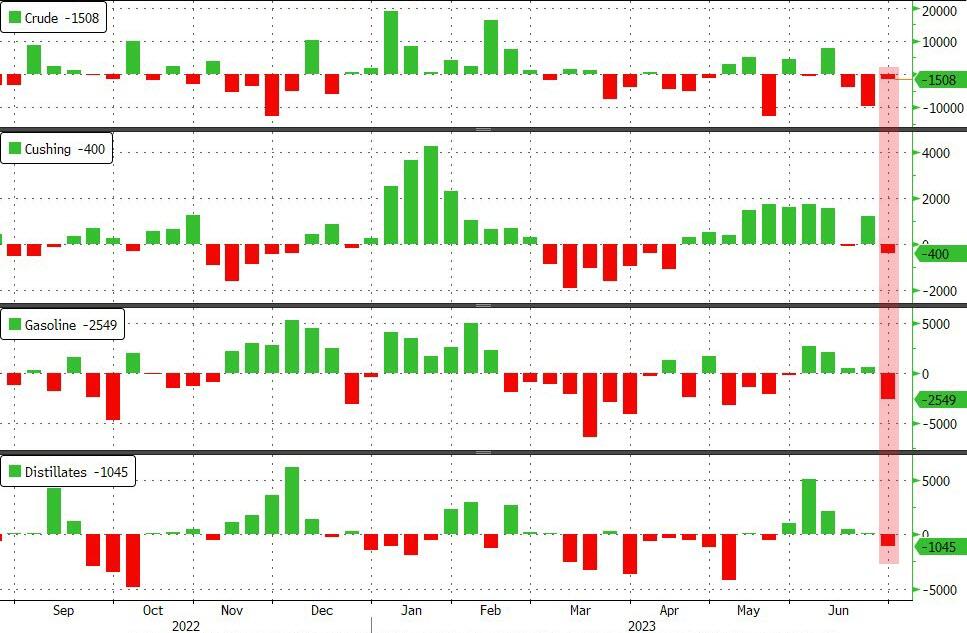

After last week’s huge draw, expectations were for a smaller draw (which API showed last night), but the actual crude draw was smaller – just 1.5mm barrels. Stocks at the Cushing hub fell 400k barrels and products also saw notable draws..

At least we now know who left cocaine in the White House!

Joe Biden, or “Blow Biden” after the cocaine was discovered in the White House the other day, owns the abysmal mortgage and housing market thanks to The Fed fighting inflation caused by Bidenomics (massive Federal spending and massive Fed stimulus).

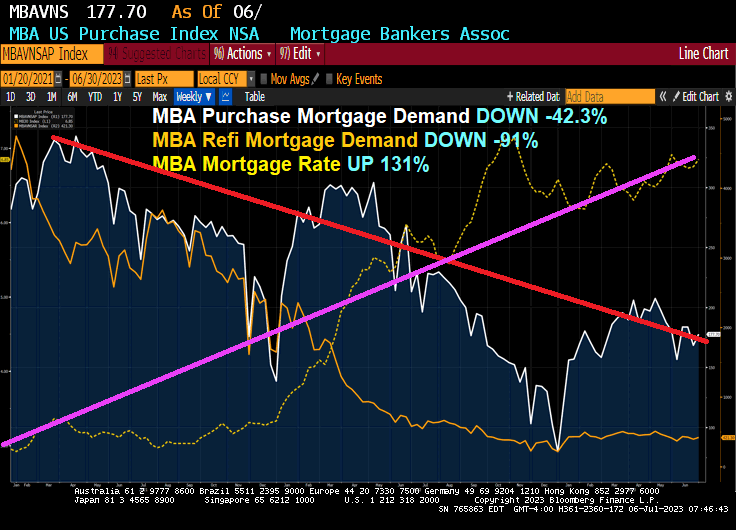

Mortgage applications decreased 4.4 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 30, 2023. Last week’s results included an adjustment for the Juneteenth holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 4.4 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 6 percent compared with the previous week. The Refinance Index decreased 4 percent from the previous week and was 30 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 5 percent from one week earlier. The unadjusted Purchase Index increased 6 percent compared with the previous week and was 22 percent lower than the same week one year ago.

Here is the rest on the story:

As liquidity dries up under Bidenomics. Or Yellenomics. Take your pick!

Seriously, can The Biden Administration get any more embarrassing? Or dangerous to American civil liberties?

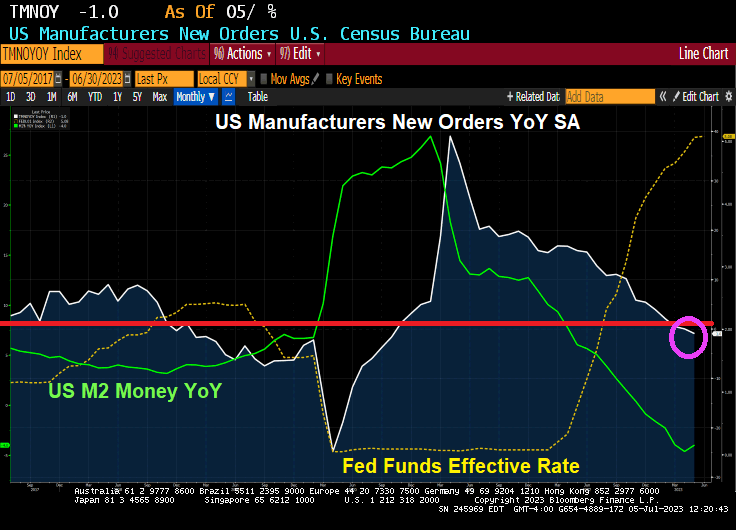

As Powell and The Gang raise interest rates, the more the economy is … slip slidin’ away. US Manufacturers New Orders YoY in May declined -1.0% for the first time since Covid.

The Federal Home Loan Bank system (aka, FLUBs), a relic of FDR and The Great Depression, subsidizes banks, not individuals. Much like its twin sibling, The Federal Reserve system, it is a Socialist institution that rely of manipulation rather than free markets.

The first sign of deep trouble in US banking this year came from a sunbaked office complex in a San Diego suburb. There, a small firm called Silvergate Capital Corp. assured investors it was weathering a run on deposits. Its lifeline: about $4.3 billion from a Federal Home Loan Bank.

Heads turned across the financial industry.

Silvergate didn’t have a network of branches serving consumers, and it barely offered mortgages. It specialized in moving dollars for cryptocurrency ventures.

Soon it became apparent that a roster of troubled regional banks was leaning on FHLBs — a relic of the Great Depression originally aimed at ensuring financial firms have cash to lend to homebuyers. Yet the banks had little to do with everyday mortgage lending.

Silicon Valley Bank, catering to venture capitalists and tech startups, said it held $15 billion from an FHLB at the end of 2022. Signature Bank, with clients including crypto platforms, had $11 billion. And by April, First Republic Bank, offering mortgages to millionaires on unusually sweet terms, ended up with more than $28 billion. All four banks collapsed.

For many, that was a crystallizing moment for the 90-year-old Federal Home Loan Bank system, which has ballooned to more than $1.5 trillion while playing a growing role as a backstop for banks taking all kinds of risks — and a diminishing role in funding new mortgages. That’s raising questions about the purpose of FHLBs and why the private institutions enjoy so much government support.

As Milton Friedman once said, “Nothing is so permanent as a temporary government program.”

Of course, rate increases are crushing regional banks as well as the middle class. But as M2 Money growth crashes, home price growth is slowing into negative territory.

You must be logged in to post a comment.