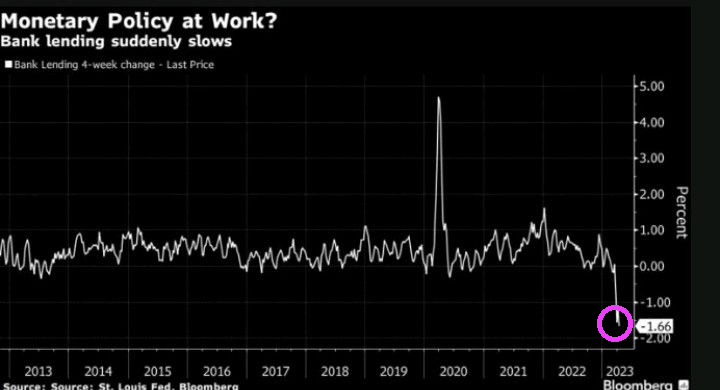

Yes, the banking system under green zealots and spendiholics Biden, Pelosi and Schumer have helped drive inflation to 40 years highs leading The Fed to counterattack and raise interest rates and slow M2 Money supply.

Ok, it is well-known that Biden was the stupidest man in the US Senate. And with Washington’s Patty Murray in the Senate, that is quite an accomplishment.

But Biden is President and is still stupid and spiraling down the dementia rabbit hole. He is blaming Republicans for their budget proposal to end the debt ceiling crisis despite saying previously that he would negotitate. Apparently, Biden’s puppet masters are telling him to risk default by playing the blame game.

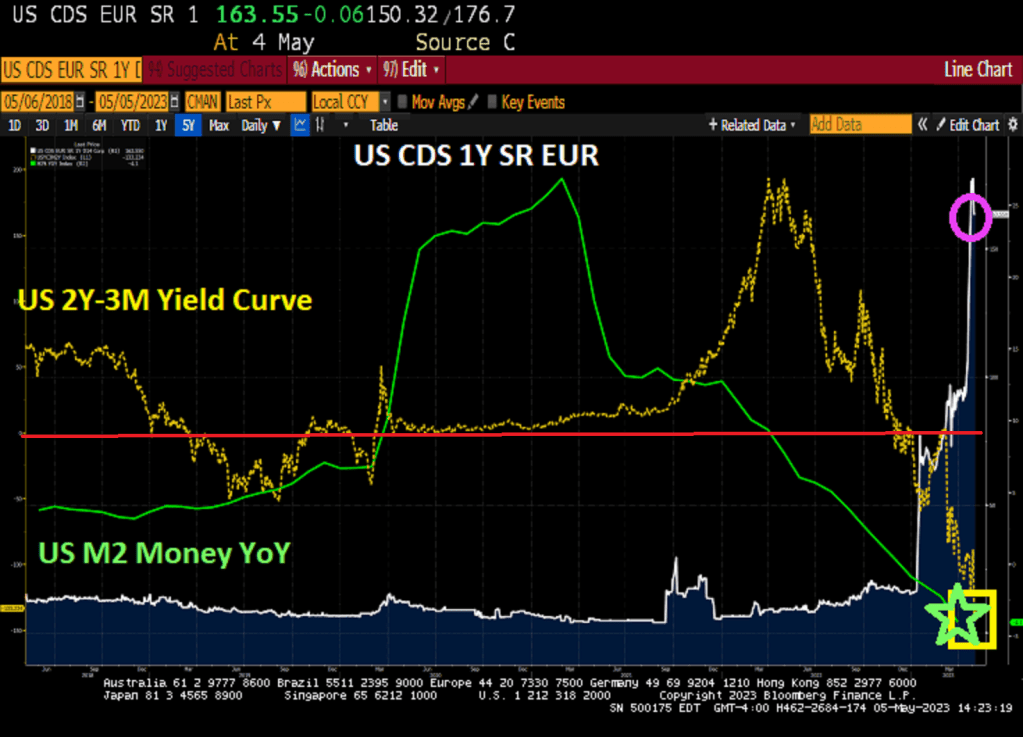

So, US credit default swap (CDS 1Y, SR, EURO) price remains elevated which indicates that Biden, Yellen and Schumer may actually default on US debt.

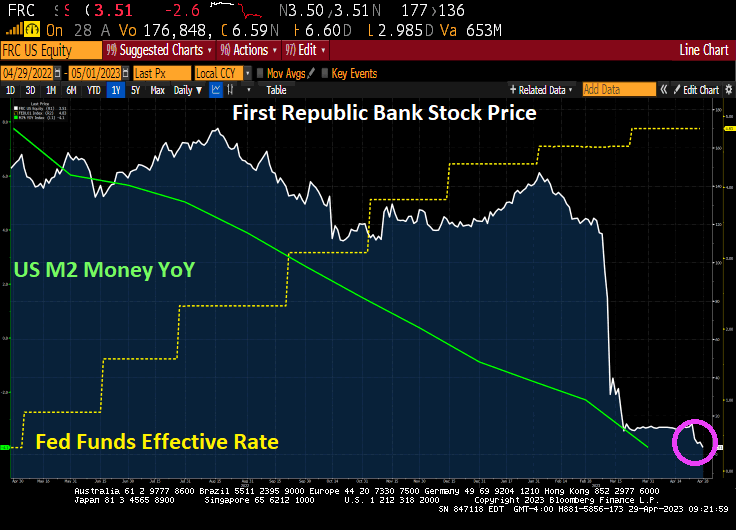

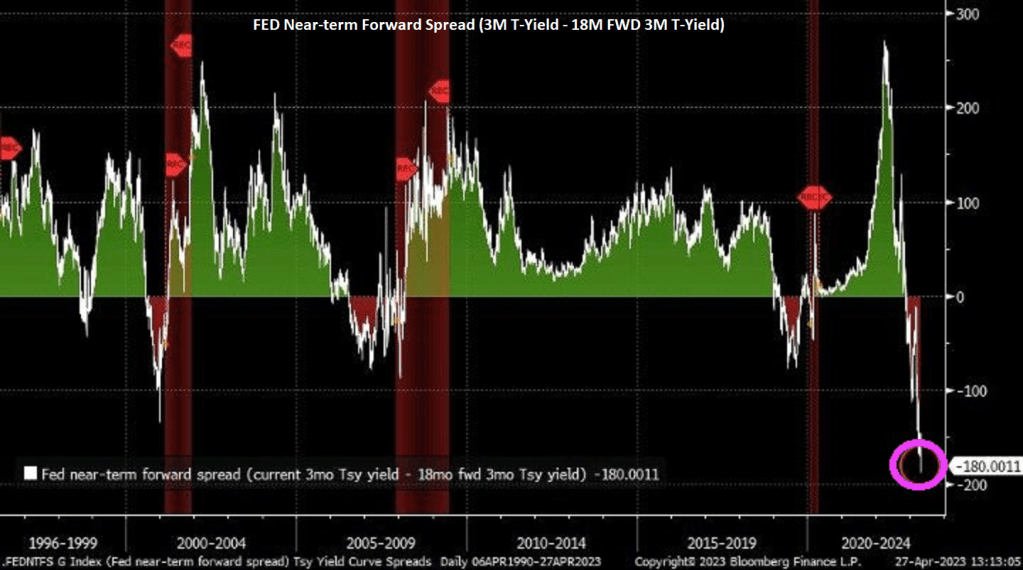

As M2 Money growth crashes and burns, the US Treasury 2Y-3M yield curve inverts to lowest in history.

Biden loves to brag about the greatest economy in history! Sure Joe. Life during Biden.

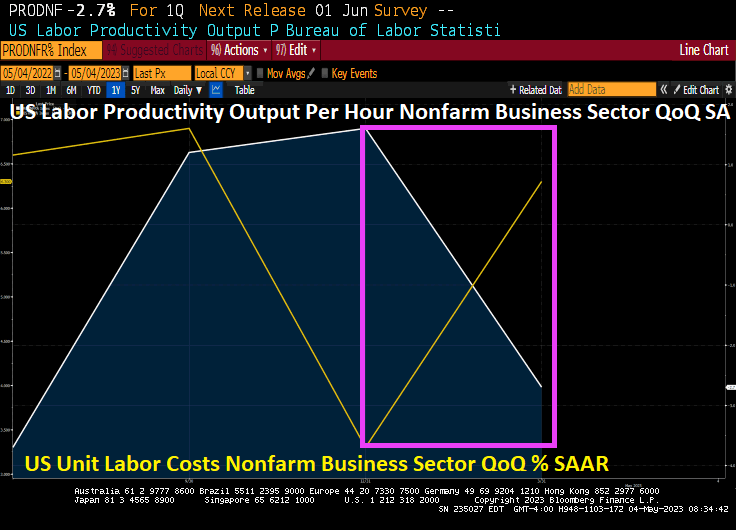

Challenger jobs cuts in April were 176% year-over-year. Non farm productivity in Q1 fell -2.7% QoQ. And unit labor costs in Q1 almost doubled to 6.3% QoQ, almost doubled from the Q4 2022 figure of 3.2%.

At least The Fed is going to pause it manic rate hikes. Then begin dropping them again.

As Connor MacLeod said in the film Highlander, “There can only be one!” The US banking system under Joe Biden’s Reign of Error is like the film Highlander: apparently, there can only be one bank. And it is likely JP Morgan Chase.

Take the JP Morgan Chase (JPMC) acquisition of First Republic Bank:

In Acquiring First Republic Bank, JP Morgan Has:

Bypassed laws against acquiring bank while controlling 10%+ of US deposits

Shared $13 billion in losses with the FDIC

Received a $50 billion loan from the FDIC

Effectively bought back its own deposits

Expects to profit $5 billion+ over the next 5 years

This crisis has taught us that rules don’t matter in times of panic, particularly to regulators.

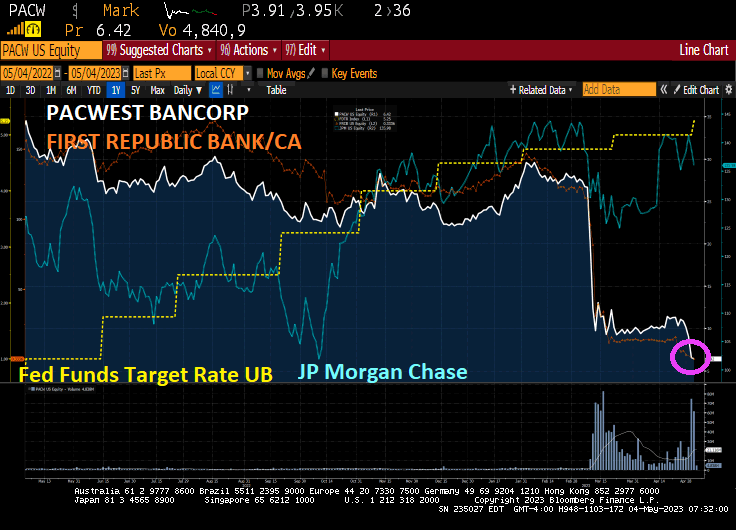

And now we have PacWest Bancorp. Lender says it’s been approached by potential investors. Bill Ackman warns US regional banking system at risk.

The turmoil at PacWest shows how investor angst still remains elevated after a string of failures and deposit outflows in the sector despite Federal Reserve Chair Jerome Powell’s assurance Wednesday that authorities were closer to containing the crisis. It’s reignited the debate over whether more US regional lenders will fall after this year’s collapse of SVB Financial Group’s Silicon Valley Bank, Silvergate Capital Corp., Signature Bank and most recently First Republic Bank.

Smaller banks are under pressure after a year of interest-rate hikes hammered the value of their bond holdings and drove unrealized losses to an estimated $1.84 trillion. Trouble in commercial real estate is adding to the pain, while depositors take their money out to seek better returns elsewhere. These stresses have put the spotlight on these lenders, which typically have fewer resources to defend themselves.

We are seeing a consolidation of the banking system .. again as smaller and regional banks fail and get gobbled up by the Too-Big-To-Fail (TBTF) banks like … JP Morgan Chase.

Biden’s Reign of Error is not over yet. His campaign slogan (which was also Bill Clinton’s campaign reelection slogan) is “Finish the job!” With Biden’s idiotic mortgage idea of punishing borrowers with good credit and giving subsidies to those with bad credit, Biden is trying to finish off the US economy and banking system.

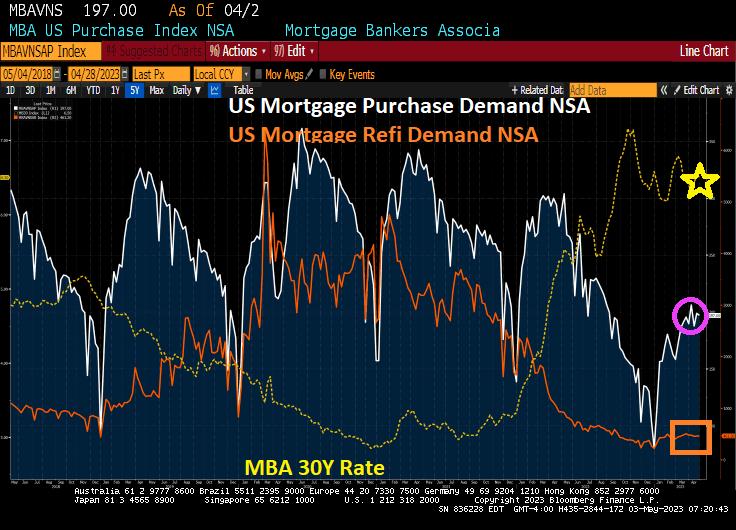

This is last data dump for mortgage demand (applications) before Biden’s idiotic woke mortgage policies go into effect (taxing those with good credit to subsidize those with lousy credit) take effect. I call this Bolshevik Biden’s Mortgage Market.

Mortgage applications decreased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 28, 2023.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 0.4 percent compared with the previous week. The Refinance Index increased 1 percent from the previous week and was 51 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 32 percent lower than the same week one year ago.

The Fed Funds Futures data is pointing to one more hike at the upcoming May FOMC meeting. Then reversal of policy.

With the massive bank failures under Clueless Joe, The Fed will intervene to make the problem worse. And with Biden’s insane mortgage policies, Prince’s “Let’s Go Crazy!” is the perfect themesong for Biden and The Fed.

As part of the Biden administration’s plan to make housing affordable for everyone (we’ve seen this story before), upfront fees for loans backed by Fannie Mae and Freddie Mac will be adjusted based on the borrower’s credit score. Borrowers with high credit scores will pay more in fees, while those with lower credit scores will pay less.

The Wall Street Journal cited data from Evercore ISI that shows borrowers with credit scores between 720-759 who make around 15-20% down payments will see loan-level pricing adjustment (LLPA) costs rise by .750%. Inversely, under the new adjustments, risky borrowers with a credit score below 639 and who put down only 5% of the value of their home will only have to pay 1.750%, compared with 3.750% under old rules.

Backlash over LLPA changes prompted the FHFA to publish a statement last week, calling such concerns “a fundamental misunderstanding.” The Biden administration ensures the new changes are meant to help those with poor credit scores obtain homes amid the worst housing affordability in a generation. Note that Biden did not speak on this himself since he would undoubtedly get confused and call people names. And get lost leaving the podium.

According to the FHFA, the new adjustments will redistribute funds to reduce the interest rate costs paid by risky borrowers. This sounds like socializing home buying to us.

Even more alarming is data from the American Enterprise Institute found that default rates of Fannie/Freddie owner-occupied 30-year fixed-rate purchase loans acquired in 2006-2007 were between 39.3% and 56.2% for borrowers with credit scores between 620 and 639 and less than 4% down payments. Those with credit scores between 720 and 769 and 20% down payments had default rates between 4.2% and 8.8%.

Joe Biden’s new nickname is “The Punisher.” Not only for this sick and twisted theft from people who work hard and are careful with their credit, but also for his crazy obsession with going green and driving energy prices (and inflation) through the roof.

Thanks to O’Biden (Obama/Biden) and Senate Majority Leader Chuck Schumer’s failure to negotiate a debt ceiling increase, the US has officially become a banana republic. Crazy government, lawless censoring and arrest of opposing political candidates.

The US CDS 1Y SR Eur just hit a staggering 176.53. That is the price of insuring against a debt default by O’Biden and Treasury Secretary Janet Yellen.

Is a US debt default likely? It shouldn’t be. But you never know with the circus clowns in the White House and nasty Chuck Schumer. But arresting the leading Republican Presidential candidate before the elections is pure Chavez/Maduro Banana Republic politics.

2 year Treasury yield up over 11 basis points today.

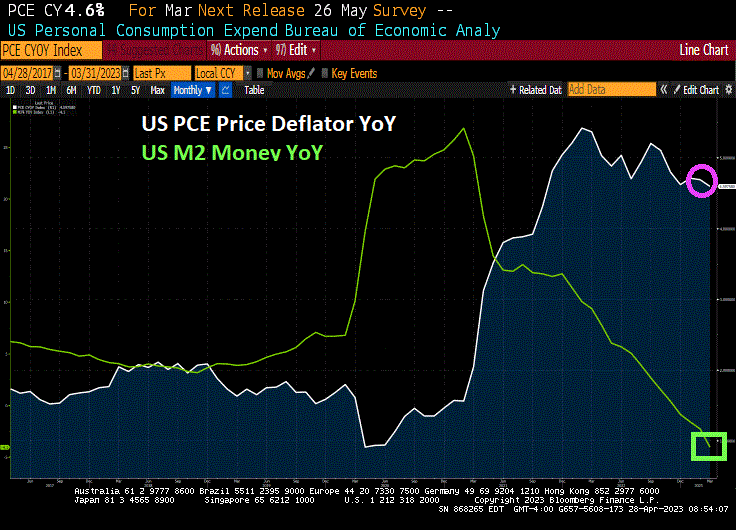

March’s Personal Consumption Expenditures Core Prices remain HOT despite The Fed crashing M2 Money growth. PCE Core price growth remained elevated at 4.6%.

Personal spending in March slowed to 0% growth.

The Taylor Rule infers a Fed Funds target rate of 10.27% Alas, we will never get there.

You must be logged in to post a comment.