Mortgage application volume dropped and remained at a multi-decade low last week(back to 1997), led by an 8 percent decline in refinance applications, which now make up only 30 percent of all applications. Purchase applications have declined in eight of the last nine weeks, as demand continues to shrink due to higher rates and a weaker economic outlook.

Mortgage applications decreased 3.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 26, 2022.

The unadjusted Purchase Index decreased 4 percent compared with the previous week and was23 percent lower than the same week one year ago.

The Refinance Index decreased 8 percent from the previous week and was 83 percent lower than the same week one year ago.

Just wait for The Federal Reserve to start unwinding its enormous balance sheet!

US home price growth is decelerating as The Federal Reserve let’s some of the air out of the monetary tires.

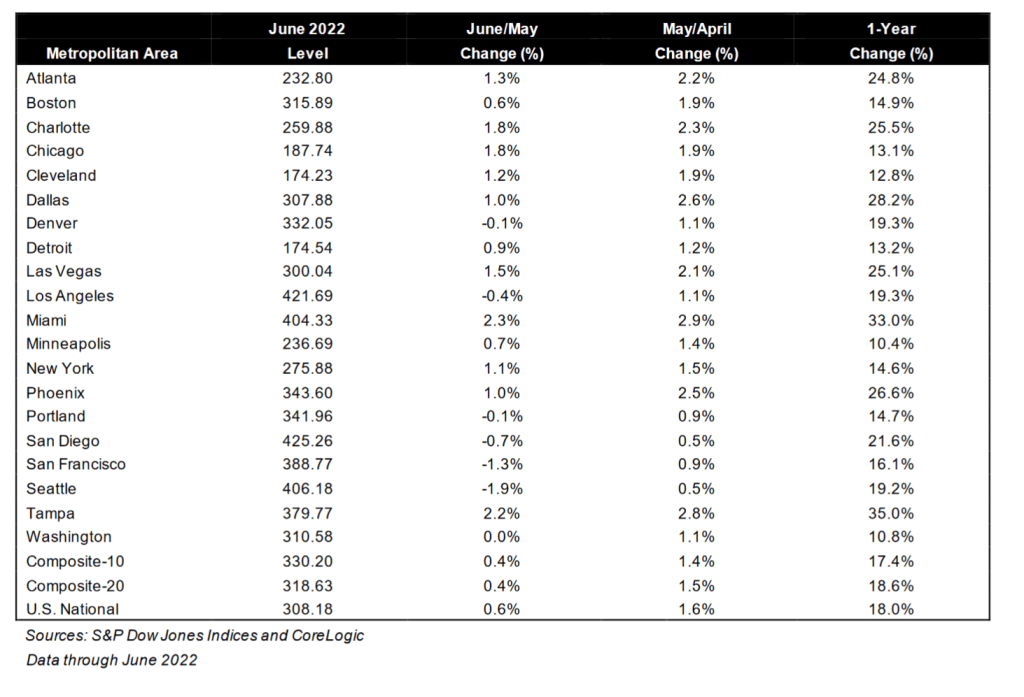

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported an 18.0% annual gain in June, down from 19.9% in the previous month. The 10-City Composite annual increase came in at 17.4%, down from 19.1% in the previous month. The 20-City Composite posted an 18.6% year-over-year gain, down from 20.5% in the previous month.

Tampa, Miami, and Dallas reported the highest year-over-year gains among the 20 cities in June. Tampa led the way with a 35.0% year-over-year price increase, followed by Miami in second with a 33.0% increase, and Dallas in third with a 28.2% increase. Only one of the 20 cities reported higher price increases in the year ending June 2022 versus the year ending May 2022.

While the Case-Shiller National home price index slowed to 18% YoY in June, the median price for existing home sales slowed to 10.55% YoY in July as The Fed’s M2 Money growth YoY slowed to 5.28% and Freddie Mac’s 30yr mortgage rate rose to 5.3%.

Bear in mind that Case-Shiller is lagged compared to the existing home sales numbers. Much like the New York Yankees manager picking the hottest batter in June to start in September. The Yankees traded poor-hitting Joey Gallo to the LA Dodgers to supplement poor-hitting Cody Bellinger.

In any case, as of June 2022, the 20 metro areas covered by Case-Shiller all grew in price in double digits with alligator-infested Tampa and Miami FL in the 30% rate, rattlesnake-infested Dallas is in 3rd place at 28.2%. Phoenix AZ, where I used to live, slowed to 26.6%. Yes, I had rattlesnakes on my property (a nest of Mohave Rattlers) and a large Diamond-backed Rattler behind my house).

Let’s see how housing holds up with more Fed monetary tightening. Fed Chair Powell is predicting “pain.”

As inflation burns the US middle class and low wage workers, The Federal Reserve reaffirmed at Jackson Hole that they are the NEW Smoky The Bear (only The Fed can fight inflation fire!) But of course, Federal spending and energy policies can drive up prices too.

Having said that, the 2-year Treasury yield and 30yr mortgage rate are rising rapidly.

The Fed is trying to cool demand by raising rates after lax monetary policy since late 2008.

While the US 2-year Treasury yield is up only slightly today, the Eurozone is seeing their 2-year sovereign yields spiking by 11-15+%.

I remember appearing on Fox Business’ Varney and Company about The Federal Reserve. When Stuart Varney asked me what will happen when The Fed finally removes the monetary stimulus, I made an explosion gesture. Well, its starting to happen.

(Bloomberg) The rally that’s bolstered risk assets over the past month was just a blip in a bear market that’s likely to worsen from here.

That’s the view of investors who seem to be finally getting the message that a resolutely hawkish Federal Reserve and central bank peers are planning to raise interest-rates at all costs to combat the hottest inflation in a generation.

Monday’s trading give credence to that prospect: equities, developed and emerging-market currencies and even haven Treasuries tumbled as fund managers digested Fed Chair Jerome Powell’s stern message that rates would keep going up even if it spells pain for households and businesses everywhere.

“The environment has changed,” said Kim Fournais, founder and chief executive of Saxo Bank A/S. “I just have a hard time seeing how this market, that is still trading close to all-time highs, can stay at those levels. There will be a period of great volatility.”

Goldman Sachs Group Inc. pegs the dollar as the main beneficiary amid the market chaos, Westpac Banking Corp. warns of fresh yen pressure and BNP Paribas Wealth Management sees more losses for developing-nation assets.

Almost every equity benchmark tumbled in Asia trading Monday as the fallout from the Fed’s hawkish rhetoric ripped through markets. S&P 500 futures dropped as much as 1.3%, indicating that US stocks are poised to extend a rout that saw the index erase $1.2 trillion on Friday.

Yields on two-year Treasuries jumped to the highest since 2007 as traders ratcheted up rate hike bets, while the yen hurtled toward the closely-watched 140 level. The risk-sensitive Korean won led losses among emerging peers, tumbling to a 13-year low.

Oddly, the Fed Funds Futures market wasn’t rattled by Powell’s announcement at Jackson Hole. The Fed’s target rate is 2.50% and is expected to rise to 3.863% by March then cool-off. The Cleveland Fed’s Mester said 4% then keeping it at 4% for an extended period of time.

But it is in Europe where Lagarde and company where the REAL action was. The ECB’s target rate is at 0% with a negative effective rate of -0.08%. But the ECB is expected to keep raising their target rate to 2.136% by July 2023.

Sovereign yields are rising across the board. Except for jolly old England.

Global equity futures are down across the board as well. But not like Friday’s plunge.

Of course, Friday was one of those “Black Fridays” for investors. And pension funds.

The Dow Jone Industrial Average fell -1008.38 points after Powell’s “Mr T” remarks on pain. That was a whopping -3%. The NASDAQ composite index fell almost -4%.

Equity markets struggled in Europe as well, particularly the German DAX index.

The UMich Buying conditions for houses rose slightly, but remains near the lowest level since 1982.

Clubber Powell, Federal Reserve Chairman.

The Case-Shiller house price numbers are due out Tuesday for June and it is expected that they will show a significant slowing in home prices. Biden and Clubber Powell could then take “credit” for slowing “inflation.”

At The Fed continues to tighten to fight inflation, pending home sales in July crashed and burned. That is, pending home sales fell -22.5% in July as M2 Money growth slowed

If I was still teaching at Ohio State or Chicago, I would ask the students if they see the relation between M2 Money growth and pending home sales.

US mortgage applications just hit the lowest levels in 22 years, January 2000 as The Federal Reserve continues monetary tightening to combat Bidenflation.

Mortgage applications decreased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 19, 2022. The Refinance Index decreased 3 percent from the previous week and was 83 percent lower than the same week one year ago.The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 21 percent lower than the same week one year ago.

MBA mortgage applications just declined to their lowest level in 22 years (January 2000) as The Fed has begun raising rates to fight inflation caused by 1) excessive monetary stimulus since late 2008, 2) Biden’s green energy policies driving up transportation costs, 3) distortionary Federal spending (e.g., Covid relief, infrastructure bills and now green energy/IRS spending by Biden/Pelosi/Schumer).

Here is the data summary for the latest MBA applications report.

Fed Chair Jerome Powell shrinking The Fed’s balance sheet.

The phrase “crossing the Rubicon” is an idiom that means that one is passing a point of no return. Its meaning comes from allusion to the crossing of the river Rubicon by Julius Caesar in early January 49 BC.

Indeed, the US crossed the FISCAL Rubicon in Q4 2012. That is when US Treasury Public Debt outstanding exceeded Real GDP. And the gap has been growing ever since.

In case you were wondering why M2 Money Velocity is so low, it is because the US is in constant crisis management mode as an excuse to spend trillions of dollars …. that generates progressively lower real GDP.

They built this nation on MMT (Modern Monetary Theory) which translates to the Federal government and Federal Reserve just wanting to spend trillions and trillions. Since 2005 (the peak of the housing bubble), the US Federal Reserve has increased the M2 Money stock more than real GDP growth in almost every quarter.

I remember when macroeconomists used to say “Everything is beautiful … as long as M2 Money growth is LESS than real GDP growth.” But we have apparently shifted to MMT when Everything is beautiful as long as there is a crisis and Congress can spend trillions.

Now Biden/Congress are spending billions in trying to reduce inflation (seriously, only in Washington DC would they think that massive spending bills would REDUCE inflation).

Dear Mr. Fantasy, play us a tune, something to make us all happy (like hitting 2% inflation WITHOUT crashing the economy). Do anything take us out of this gloom (caused by The Fed, Biden’s energy policies and Federal spending). Sing a song, play guitar, Make it snappy. Or in the case of housing, make it crappy.

(Bloomberg) — Federal Reserve Bank of Richmond President Thomas Barkin said the central bank was resolved to curb red-hot inflation, even if that meant risking a US economic recession.

“We’re committed to returning inflation to our 2% target and we’ll do what it takes to get there,” Barkin said Friday during an event in Ocean City, Maryland. He said that this could be achieved without a “tremendous decline in activity” but acknowledged that there were risks.

“There’s a path to getting inflation under control but a recession could happen in the process,” he said.

The US central bank hiked interest rates by 75 basis points in July for the second straight month as policy makers tackle inflation that’s running near 40-year highs. Fed officials speaking in recent days have said more rate increases are needed, but they are still deciding how big to move at their next policy meeting.

St. Louis Fed President James Bullard, one of the most hawkish policy makers, on Thursday urged another 75 basis-point move while Kansas City’s Esther George struck a more cautious tone.

Well, The Fed (aka, Der Kommissars) let the monetary stimulus blow out of control since 2000.

With the 2001 recession, The Fed crashed the target rate (white line) causing home price growth (blue line) to soar. Then The Fed decided that the economy was overheated and cranked up their target rate. This sudden rise in The Fed’s target rate helped to slow/crash housing prices. Resulting in … a frantic decrease in the target rate (late 2007- late 2008) and the adoption of asset purchases of Treasury Notes/Bonds and Agency Mortgage-backed Securities in late 2008.

The Bernanke/Yellen “loose as a goose” policies from late 2008 to Feb 2018 created a total mess. Bernanke/Yellen raised the target rate only one before Trump was elected President, and 8 times AFTER Trump was elected. And Yellen’s Fed began to let the balance sheet shrink a bit before Covid struck in early 2020. And with Covid came another massive expansion of The Fed’s Balance Sheet WHICH HAS NOT YET BEEN WITHDRAWN (despite Fed talking heads saying it would be reduced).

Here we sit with The Fed NOW trying to extinguish inflation (yellow line) by raising their target rate (white line) but NOT shrinking the balance sheet (orange line).

Wonder why this is a horrible homeless problem in the US, particularly in California? While Stanford University has an excellent study of the causes of California’s homeless problem, there is another cause of homelessness … The Federal Reserve’s insane monetary policies since late 2008. The Case-Shiller National Home Price Index is 65% higher in May than during the calamitous home price bubble of 2005-2007, helping to exacerbate the homeless problem.

One of the many problems created by the reckless Bernanke/Yellen/Powell monetary policies is the M2 Money Velocity is near an all-time low making a return to “easy money policies” far more difficult.

I won’t post any photos of the homeless encampments in Los Angeles since it is very sad. But here is a photo of the Dunder-Mifflin paper company “office” on Saticoy Street. The point is that thanks to The Federal Reserve’s loose monetary policies, housing is unaffordable for millions of households forcing many to live on the streets.

Figure 2: Median Rent for a Two-Bedroom Apartment, California, 2022

And a point of trivia. The Office’s Charles Miner (played by the GREAT Idris Elba) was allegedly hired from Saticoy Steel. The Dunder-Mifflin paper company site was on Saticoy Street in sunny LA, not Scranton PA.

Good luck to The Federal Reserve in combating inflation without causing a recession.

You must be logged in to post a comment.