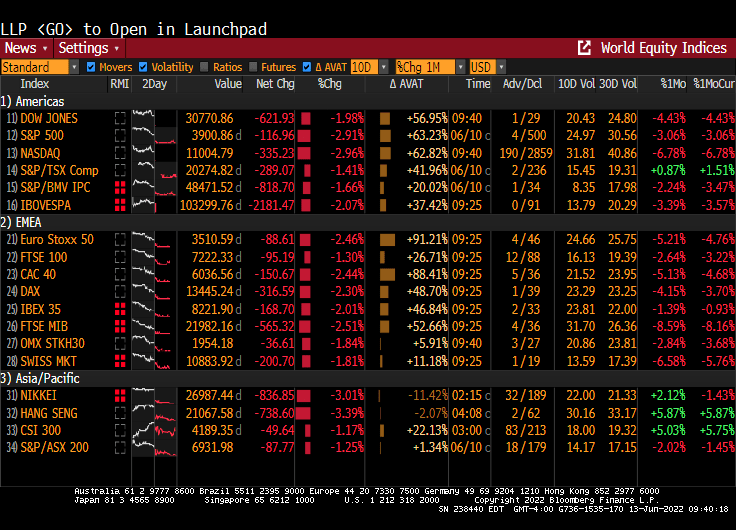

The CPI news on Friday was so awful that it changed the bond market’s view of Fed trajectory, and the weakest sector broke. In bond jargon, MBS went “no-bid.”No buyers for MBS. Then a few posted prices beyond borrower demand, not wanting to buy except at penalty prices. (Courtesy of Cherry Creek Mortgage)

Despite what Treasury Secretary Janet Yellen has said, Friday’s inflation report demonstrated that inflation is no longer transitory. And with that realization, there was a dearth of bidders for Agency Mortgage-backed Securities (Agency MBS) on Friday.

As a result, agency MBS 2.5% dropped to under $90 as markets expect The Fed to keep raising rates to combat inflation.

Duration of the FNCL 2.5% agency MBS has been extending with growing inflation. Duration was under 1 on August 2, 2021 but is now 7 times greater at almost 7.

Note to Yellen: inflation seems be permanent, not transitory. Or at least inflation will remain high for the foreseeable future, crushing the life out of Agency MBS.

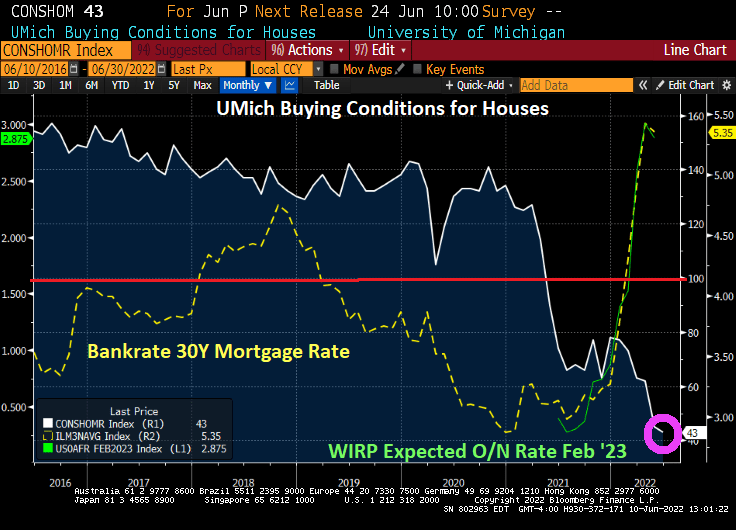

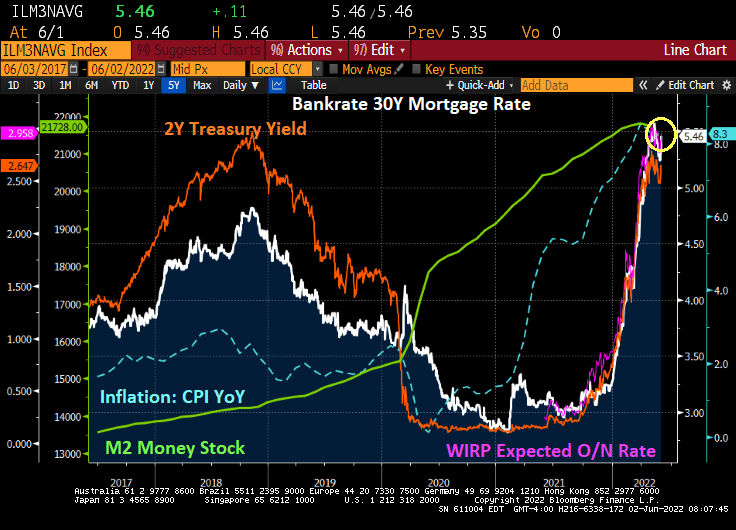

The Fed is expected to raise their target rate to 2.875% by February 2023. With that expectation, mortgage rates (yellow line) are soaring. And with that, University of Michigan’s Buying Conditions for housing has plunged to 43, the lowest levels since 1982 as the US was trying to recover from high inflation.

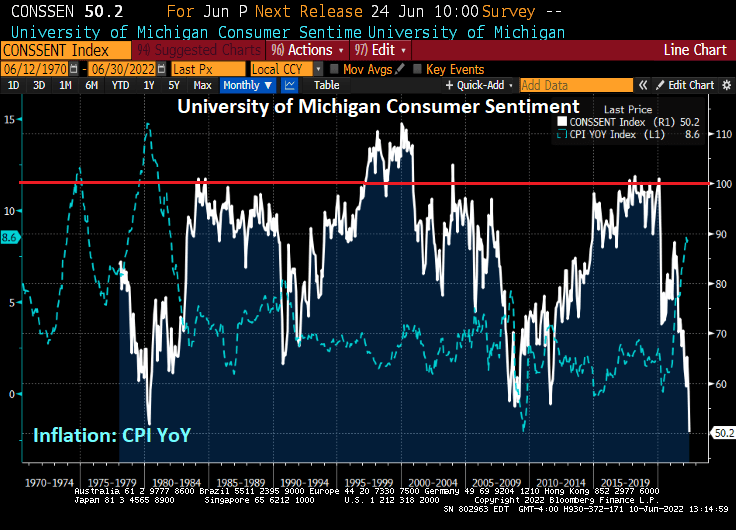

The University of Michigan consumer sentiment index just plunged to the LOWEST LEVEL in history on inflation and Fed’s reaction.

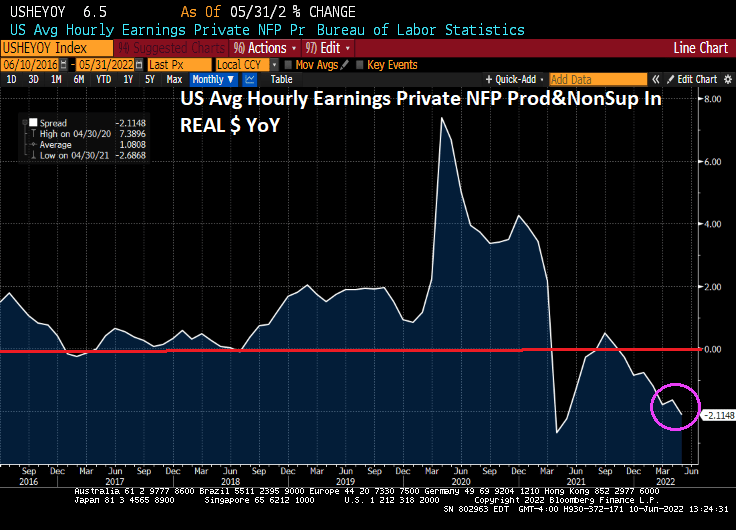

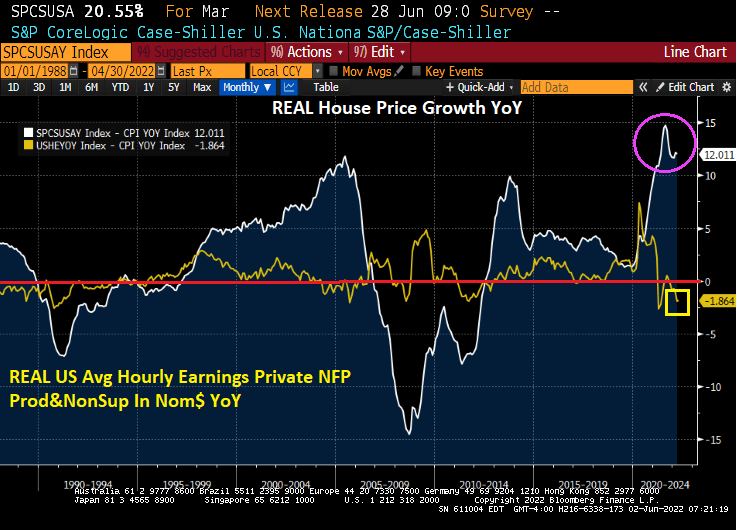

Average REAL wage growth has now declined to -2.11% YoY.

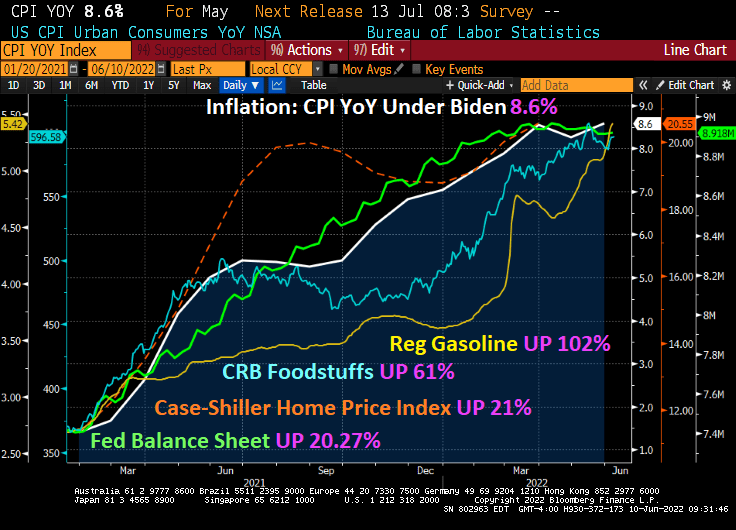

Inflation, the bane of the middle class and working families, just rose to 8.6%.

Core inflation, that excludes energy and food, actually declined slightly to 6% from 6.2% in April. But since most families are concerned with gas prices and food, (not to mention home prices growing at 21.17% YoY), core inflation really underestimates the suffering.

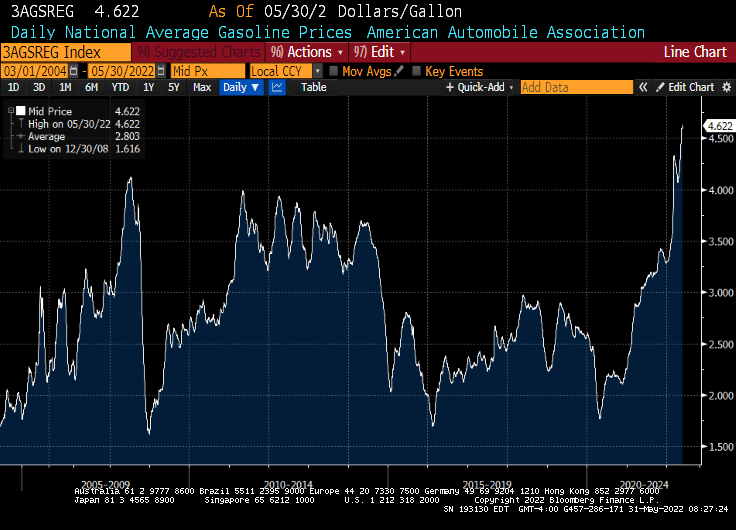

Under Biden’s leadership in cooperation with eternal Fed stimulus (until now), inflation started at 1.4% YoY and has increased to 8.6% YoY. The Fed’s balance sheet has increased by 20.27% (more monetary Stimulypto!), Case-Shiller home prices started at 10.44% YoY and has now doubled to 20.55% YoY. Regular gasoline started at $2.57 and is now at $5.42, up 102%. Food is up 61%.

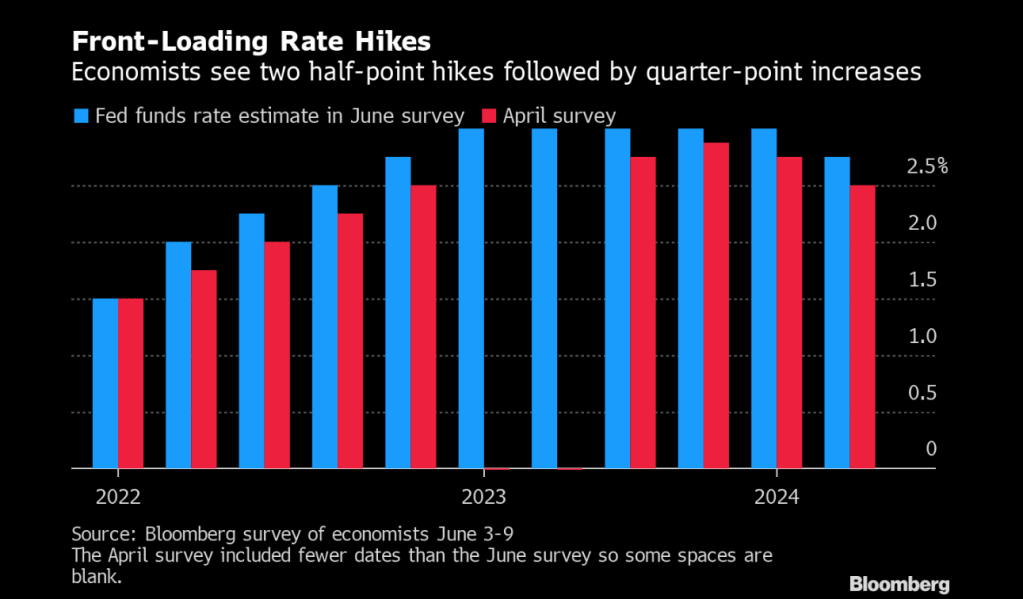

The Fed is expecting two half-point hikes followed by quarter-point increases.

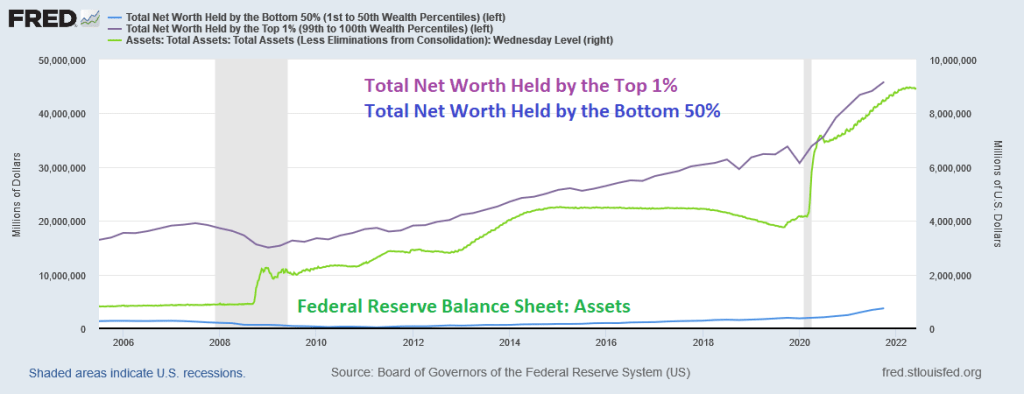

Pennies from Heaven. That is what the bottom 50% received from The Federal Reserve’s massive doses of monetary stimulus (or stimulypto).

There was one big dose of monetary stimulus in late 2008 surrounding the financial crisis and housing bubble burst, another doses (aka, QE 2 and QE3) then the biggest dose of all with the outbreak of Covid in early 2020.

President Biden should have mentioned on Jimmy Dimmel last night that The Federal Reserve has helped the bottom 50% with its endless monetary stimulus.

But if you were fortunate enough to own a home (the top 1% are likely homeowners), then you benefited from The Fed’s monetary stimulypto.

And I noticed that Biden didn’t mention plunging REAL average weekly earnings YoY.

The Federal Reserve’s monetary “policies” have benefited the top 1% and homeowners relative to the bottom 50% (who often rent and got clobbered with 20% growth in rents).

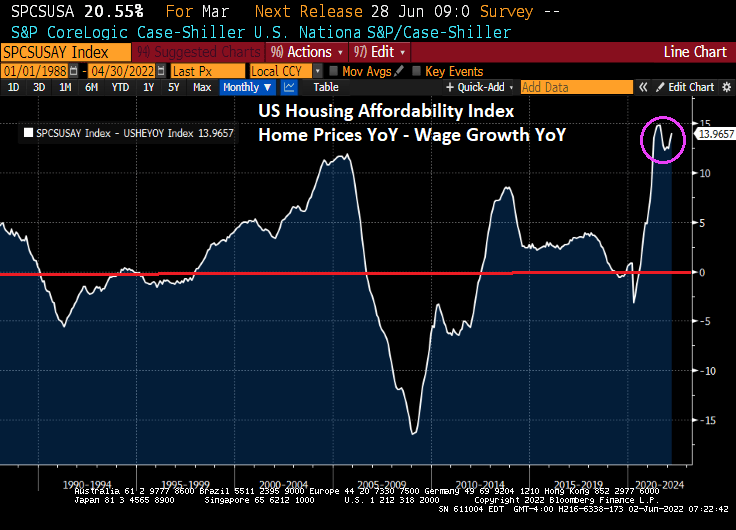

Great job, Fed! Making housing more unaffordable for rents (combine rising rents and declining REAL wages and we have a real affordability problem).

Home affordability for first time homebuyers?

And what is with Biden’s ear lobes? As inflation is rising, his ear lobes are shrinking.

The inflation numbers are out tomorrow. I noticed that Biden and Jimmy Dimmel only discussed gun control, not the sad state of the economy under Biden.

President Biden met with Federal Reserve Chairman Powell to discuss how to control the inflation that is crushing the middle class and low-wage workers.

Here is a good example of why Biden is worried. There is a mid-term election on the horizon and people are angry and scared. Housing, generally the largest asset owned (or rented) by a household is simply unaffordable thanks, in part, to the over-stimulation of the economy by 1) The Federal Reserve in terms of money printing and 2) the Federal government in terms of fiscal stimulus in response to the Covid outbreak in March 2020.

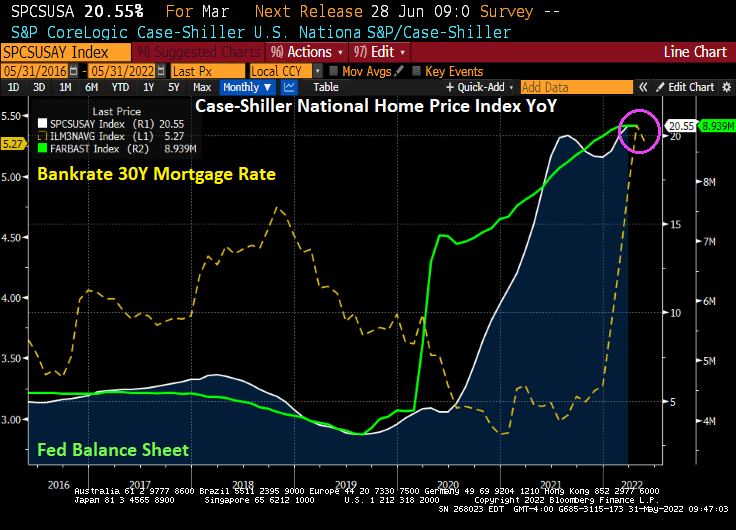

In nominal terms, the gap between US home prices (Case-Shiller National Home Price Index YoY – US Average Hourly Earnings YoY) is near the all-time high.

Yes, home price growth exploded upwards when The Fed rapidly expanded their balance sheet in response to the Covid outbreak … and only now are considering shrinking the balance sheet.

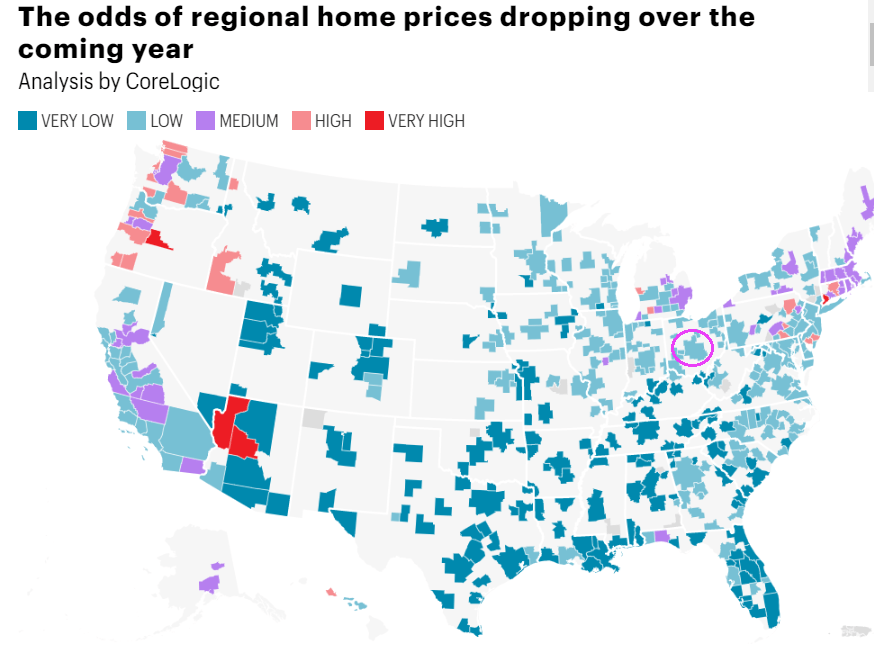

In terms of house prices, CoreLogic has a nice chart depicted the odds of home prices dropping over the coming year. I circled Columbus Ohio because that is where I am moving (knock on wood).

And then we have the 30-year mortgage rate rising with The Fed’s expected tightening of monetary policy. That will certainly make housing even less affordable, unless house price growth cools dramatically.

Heartaches By The Number … for American households and mortgage lenders as The Federal Reserve begins FINALLY removing monetary stimulus.

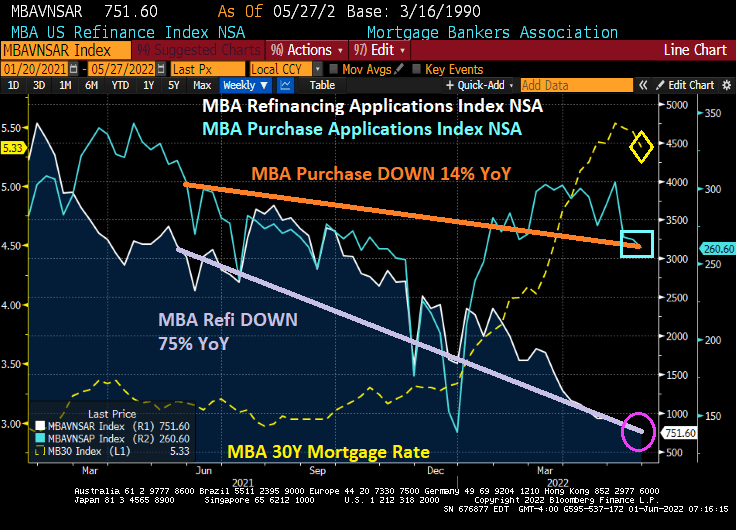

Mortgage applications decreased 2.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 27, 2022.

The Refinance Index decreased 5 percent from the previous week and was 75 percent lower than the same week one year ago.

The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 14 percent lower than the same week one year ago.

Under Biden, mortgage refi applications are down -82.4%, purchase applications are down -7.5% and mortgage rates are up +80.7%.

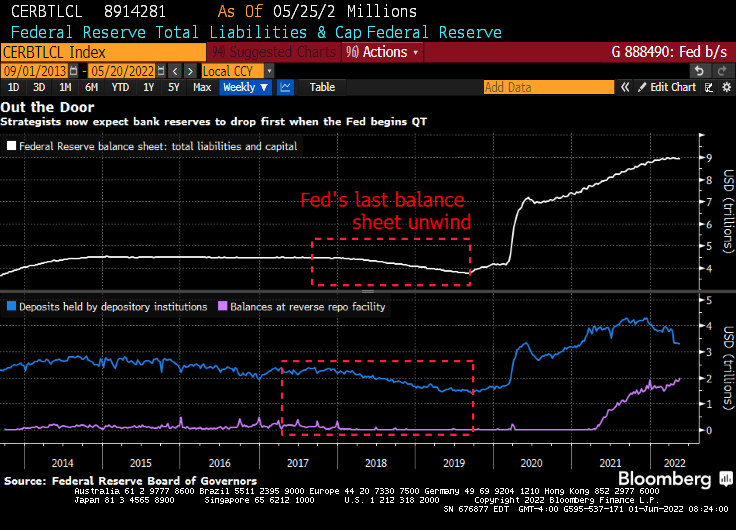

Then we have this headline: “Fed Starts Experiment of Letting $8.9 Trillion Portfolio Shrink”

The Fed is capping monthly runoff at $47.5 billion — $30 billion for Treasuries and $17.5 billion for mortgage-backed securities — until September. Those thresholds will then double to a combined $95 billion. That compares to a peak of $50 billion a month when the Fed performed the exercise starting in 2017.

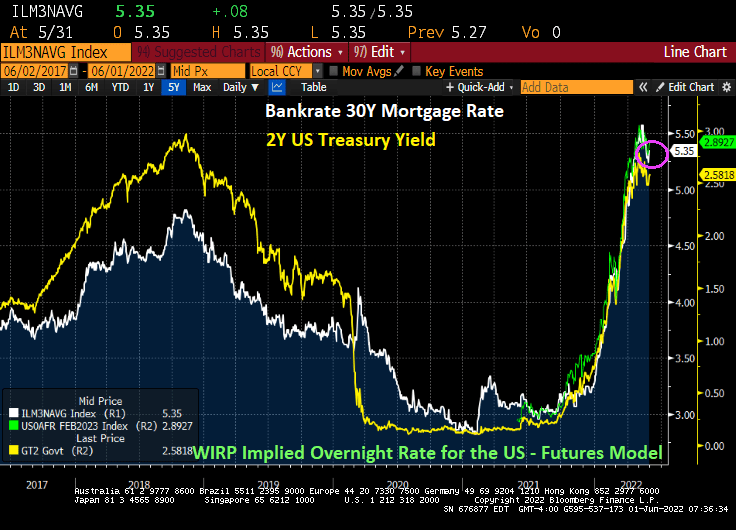

As expectation of Fed rate hikes increase, mortgage rates have soared like Tom Cruise’s Super Hornet aircraft from Top Gun: Maverick climbing over the steep mountain.

And mortgage rates are up a bit today.

Meanwhile, The Federal Reserve begins shrinking their balance sheet for the first time since Yellen and company started shrinking it under Trump.

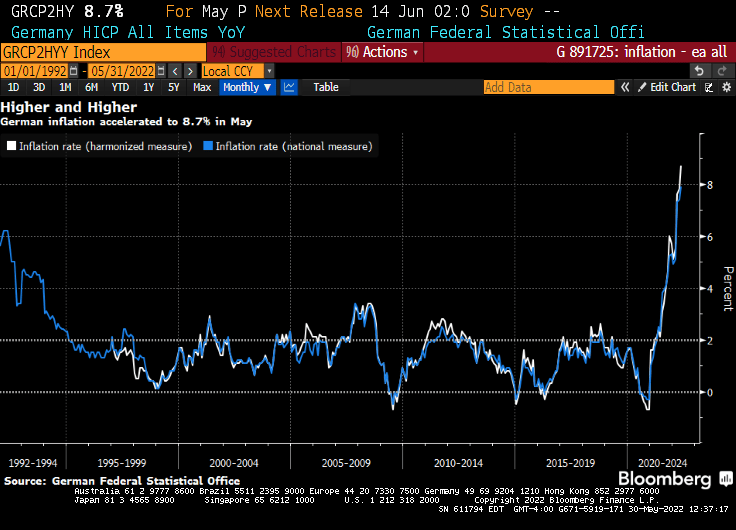

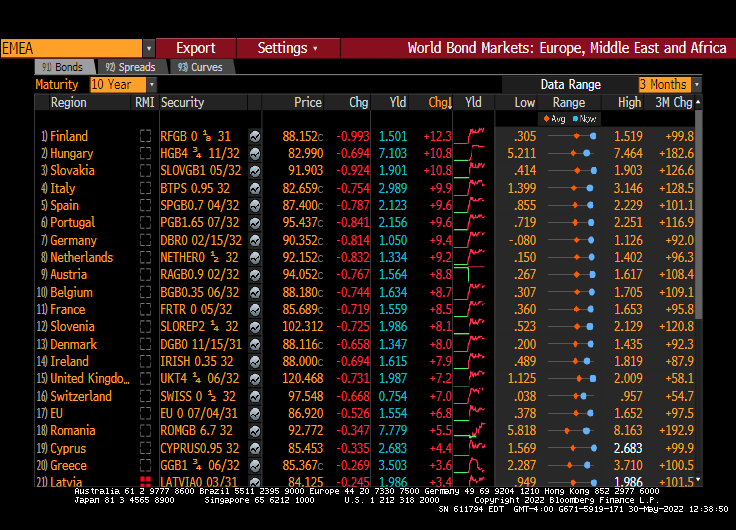

German inflation hit another post-World-War-II record high, piling pressure on The ECB’s need to exit from crisis-era stimulus after numbers from Spain also printed hotter than expected.

Driven by soaring energy and food costs, this morning’s data showed consumer prices in Europe’s largest economy surged 8.7% YoY – far hotter than the +8.1% expected (the highest since the start of the monthly statistics in 1963).

And top of that, the German 10-year Bund rate rose +9.4 BPS this morning, although Finland, Hungary and Slovakia all rose above +10 BPS.

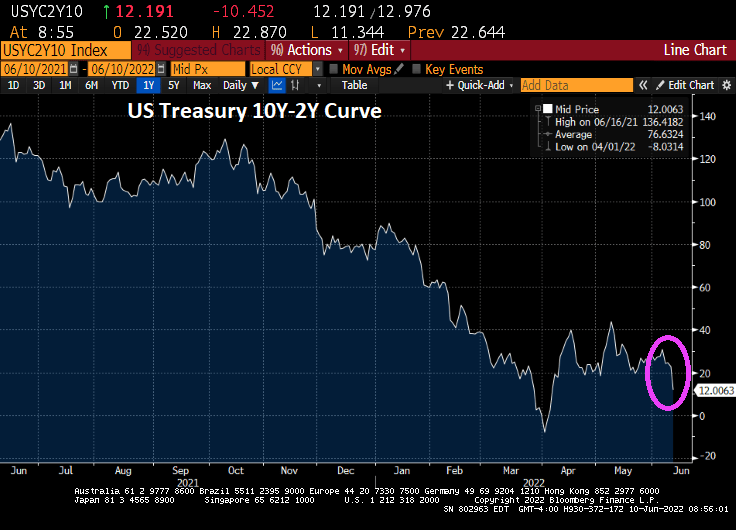

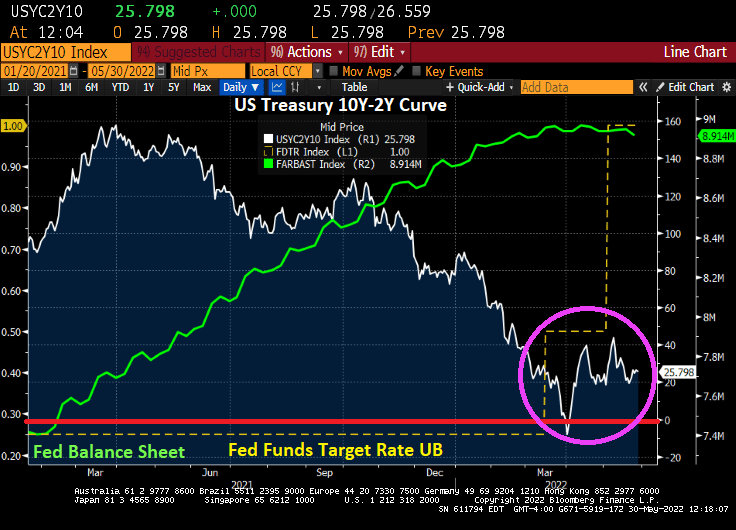

While US markets are closed today in honor of Memorial Day, the US Treasury curve (10Y-2Y) has stabilized at 25.8 basis points after the initial shock of The Fed finally raising rates for the first time under Biden.

Then there is this headline: Biden to Meet Powell to Discuss Economy Amid Inflation Pain. So much for Fed independence. I wonder if Powell will say “Joe, have you ever considered canceling your executive orders on oil and natural gas exploration?”

You must be logged in to post a comment.