Years ago, Brent Ambrose, Michael Lacour-Little and I wrote a paper on the US 30-year jumbo mortgage spread over conforming 30-year mortgage rates entitled “The effect of conforming loan status on mortgage yield spreads: a loan level analysis.” But that paper was written before Covid and the dramatic distortion caused in mortgage markets by The Federal Reserve’s massive increase in money.

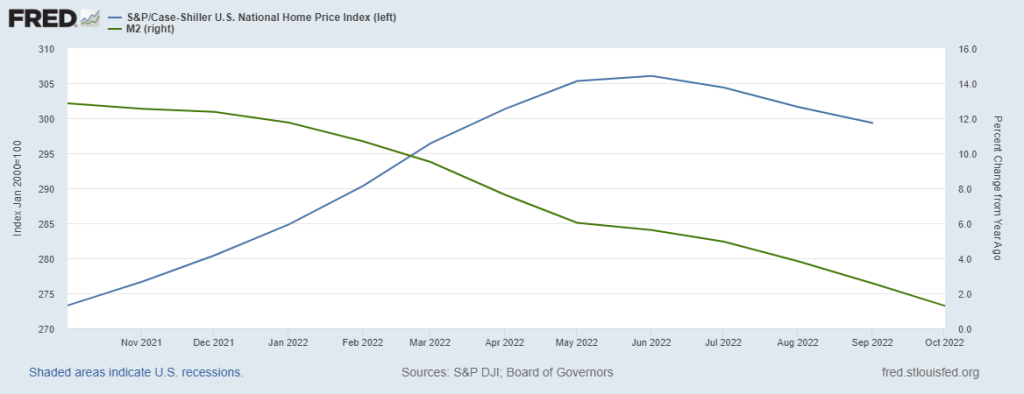

Here is the spread between Bankrate’s 30-year mortgage rate and their 30-year JUMBO mortgage. Notice that between 2007 and early 2020, the median “jumbo spread” was 49 basis points. But after Covid and The Fed’s counterattack (by printing M2 Money), the median Jumbo spread from 4/1/2020 to today is only 1 basis point.

In the following chart, you can see the jumbo mortgage rate (yellow) against the conforming mortgage rate (white) and there is almost always a spread between the two UNTIL 2020 where we saw M2 Money growth (green line) spike and The Fed increased their purchases of Agency MBS (purple line). Since Covid and The Fed’s massive reaction, the jumbo rate and conforming rate are virtually the same. In fact, the latest jumbo spread is 1 basis point over the conforming rate.

Why is this happening? One explanation is that demand from the investors who ultimately buy jumbo mortgages. The strong demand by investors appears to have driven down the yields on jumbos relative to conventional loans, especially as the use and accessibility to jumbos has grown.

A second explanation is that Loan Level Price Adjustments that were added to conforming loans post-financial crisis never went away (until just recently on selected loans). This makes jumbos and conforming loans very close in yield.

So, when will the mortgage market return to normal and jumbo mortgages go back to the normal 50 basis point spread? We may see normalization if The Fed speeds up its withdrawal from markets. Also, getting rid of Loan Level Price Adjustments would help normalized the mortgage market.

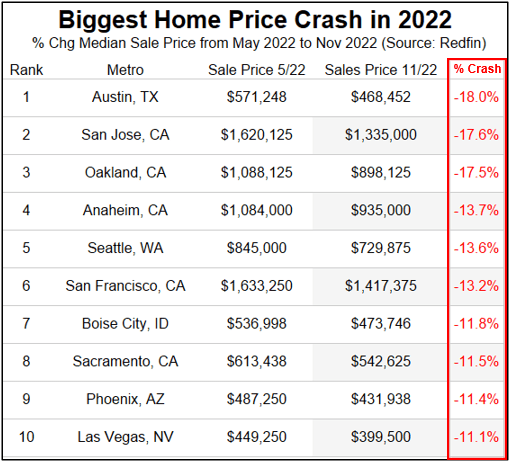

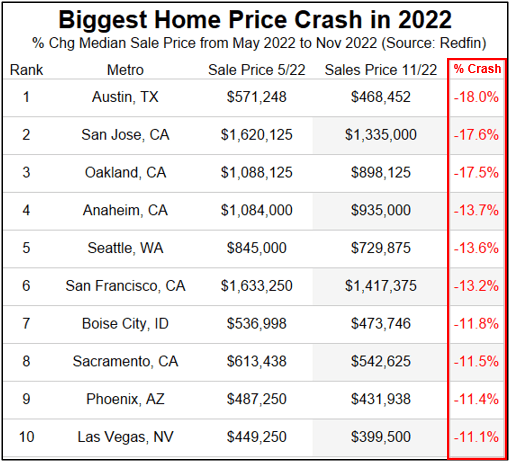

But things are getting stressed in jumboland (California) where home prices are crashing in 5 of the top 8 metro areas.

Harry Houdini couldn’t have created a more tantalizing mystery … and one I wish would go away.

You must be logged in to post a comment.