Citi’s economic surprise index fell to -7.80 in February. This is the remnant of Biden/Democrats horrible economic policies and fear of Trump’s tariff policies.

Gold, Bitcoin and the S&P 500 are doing quite well on the prospects for growth in the US under Trump.

The US economy like an aircraft carrier, doesn’t turn on a dime. Think of the Japanese carriers at Midway in WWII. Thanks Admiral Biden! And Rear Admiral Harris!

During the first three months of 2023, U.S. office vacancy topped 20 percent for the first time in decades. In San Francisco, Dallas, and Houston, vacancy rates are as high as 25 percent. These figures understate the severity of the crisis because they only cover spaces that are no longer leased. Most office leases were signed before the pandemic and have yet to come up for renewal. Actual office use points to a further decrease in demand. Attendance in the 10 largest business districts is still below 50 percent of its pre-COVID level, as white-collar employees spend an estimated 28 percent of their workdays at home.

A new report from Moody’s offers yet another grim outlook that the commercial real estate downturn is nowhere near the bottom. Elevated interest rates and persistent remote and hybrid working trends could result in around 24% of all office towers standing vacant within the next two years. The office tower apocalypse will result in more depressed values that will only pressure landlords.

“Combining these insights, with our more than 40 years of historic office performance data, as well as future employment projections, our model indicates that the impact on office demand from work from home will be around 14% on average across a 63- month period, resulting in vacancy rates that peak in early 2026 at approximately 24% nationally,” Moody’s analysts Todd Metcalfe, Anthony Spinelli, and Thomas LaSalvia wrote in the report.

In a separate report, Tom LaSalvia, Moody’s head of CRE economics, wrote that the office vacancy rate’s move from 19.8% in the first quarter of this year to the expected 24% by 2026 could reduce revenue for office landlords by between $8 billion and $10 billion. Factor in lower rents and higher costs, this may translate into “property value destruction” in the range of a quarter-trillion dollars.

In addition to remote working trends, Moody’s analysts pointed out that the amount of office space per worker has been in a “general downward trend for decades.”

At the peak of the Dot-Com boom, office workers used an average of 190 sq ft. The figure has since slid to 155 sq ft in 2023.

“The argument for maintaining or even increasing remote work practices remains compelling for many businesses,” the analysts said, adding, “If productivity remains stable and costs can be reduced by forgoing physical office spaces, the rationale for mandating in-office attendance diminishes.”

Related research from the McKinsey Global Institute forecasts that office property values will plummet by $800 billion to $1.3 trillion by the decade’s end.

Moody’s expects vacancy rates to top out as office towers are demolished or converted to residential ones in the coming years.

“Right-sizing will continue over the next decade as the market shakes out less efficient space for flexible floorplans that support our relatively new working habits,” they said.

Earlier this year, Goldman analyst Jan Hatzius pointed out that a further 50% price decline would make office tower conversions financially sensible.

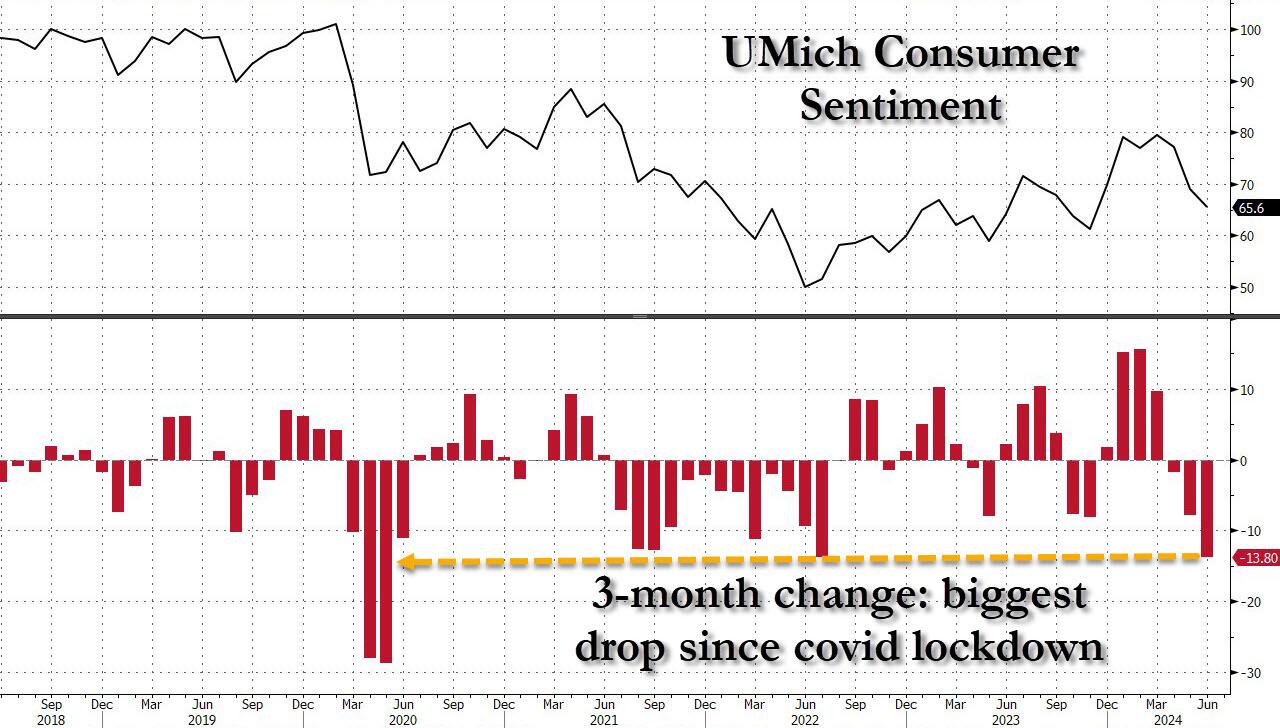

One month after the May Consumer Sentiment printed at a record 7-sigma miss to expectations, consumer sentiment once again “unexpectedly” slumped, this time from an upward revised 68.8 to 67.6, the lowest print since last November, and the biggest 3-month drop in sentiment (-13.8 points) going back to the covid lockdowns.

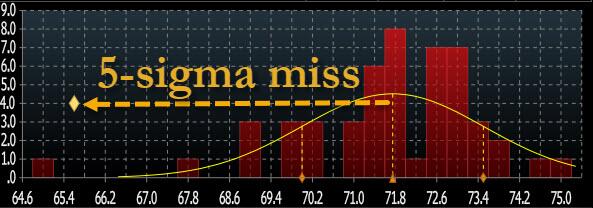

… which was not only a 5-sigma miss to the median estimate (an improvement from last month’s 7-sigma)…

… but also the biggest miss of 2024.

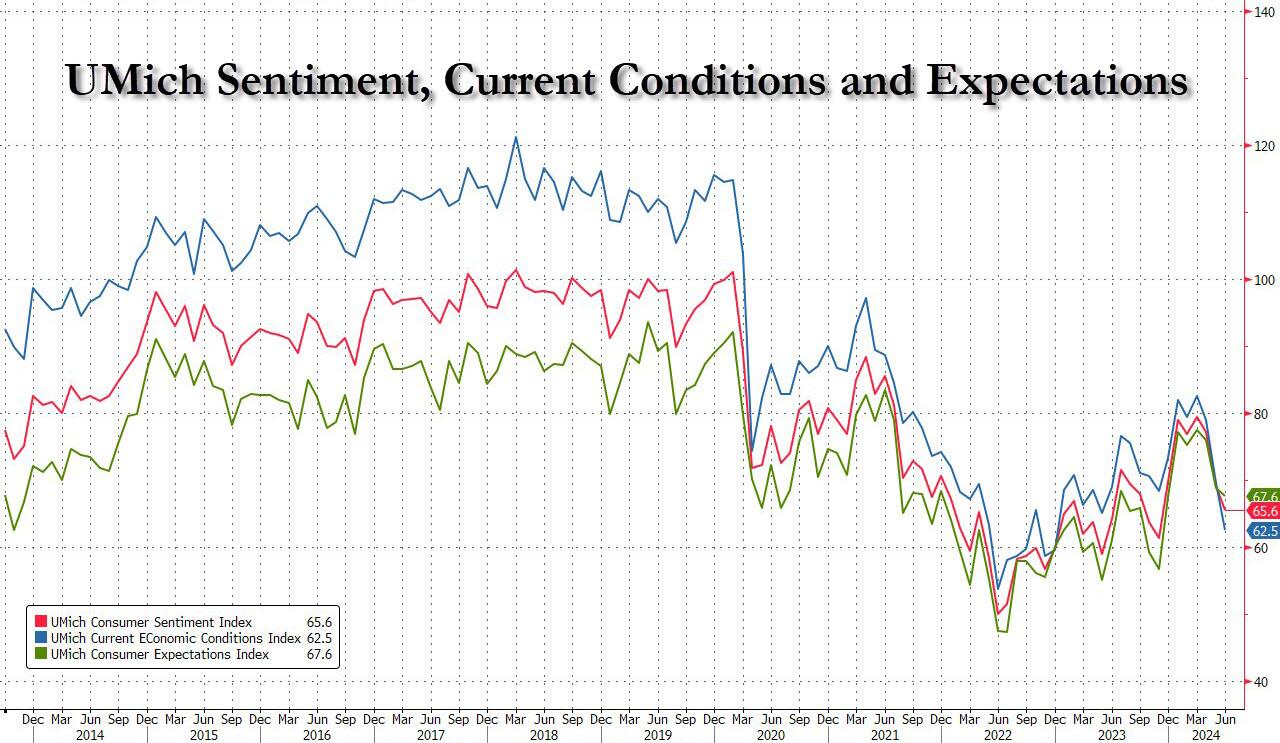

The collapse in sentiment was broad based, and hammered both current conditions – which plunged from 69.6 to 62.5, the lowest since 2022 and badly missing estimates of 72.2 – and also expectations, which dropped from 68.8 to 67.6 (and also far below the 72.0 estimate).

The decline in sentiment coincides with signs that the labor market, which has driven consumer spending over the last year, is also falling apart. The unemployment rate rose to 4% last month, the highest in more than two years, while jobless claims unexpectedly soared following a firing frenzy out of California.

“While lower-income families have, as a group, seen notable wage gains in a strong labor market, their budgets remain tight amid continued high prices even as inflation has slowed,” Joanne Hsu, director of the survey, said in a statement.

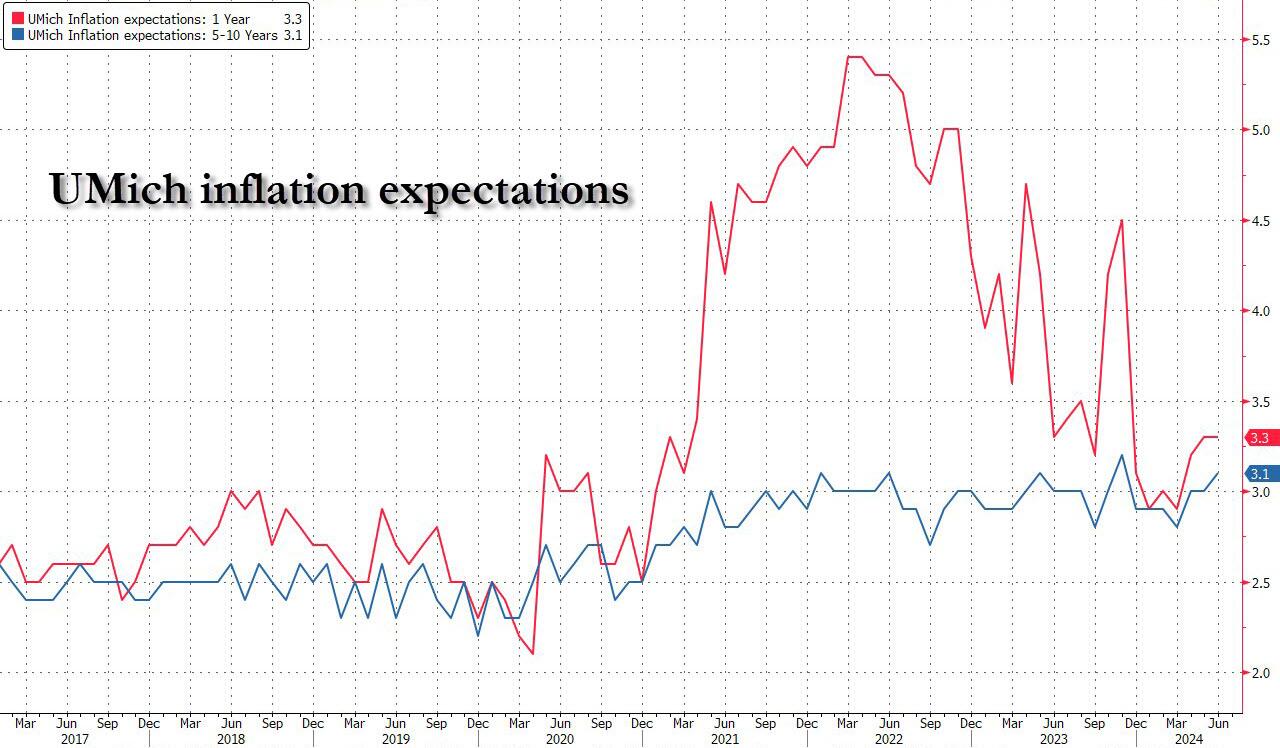

But wait there’s more, because if that was the “stag” part of the report, the UMich report also confirmed that the “flation” isn’t far behind, as the inflation outlook continued its recent deterioration, to wit: 1 Year inflation expectations remained unchanged at 3.3%, beating estimates of a drop back 3.2%, while 5-10 Year inflation expectations rose from 3.0% to 3.1%, the highest since November.

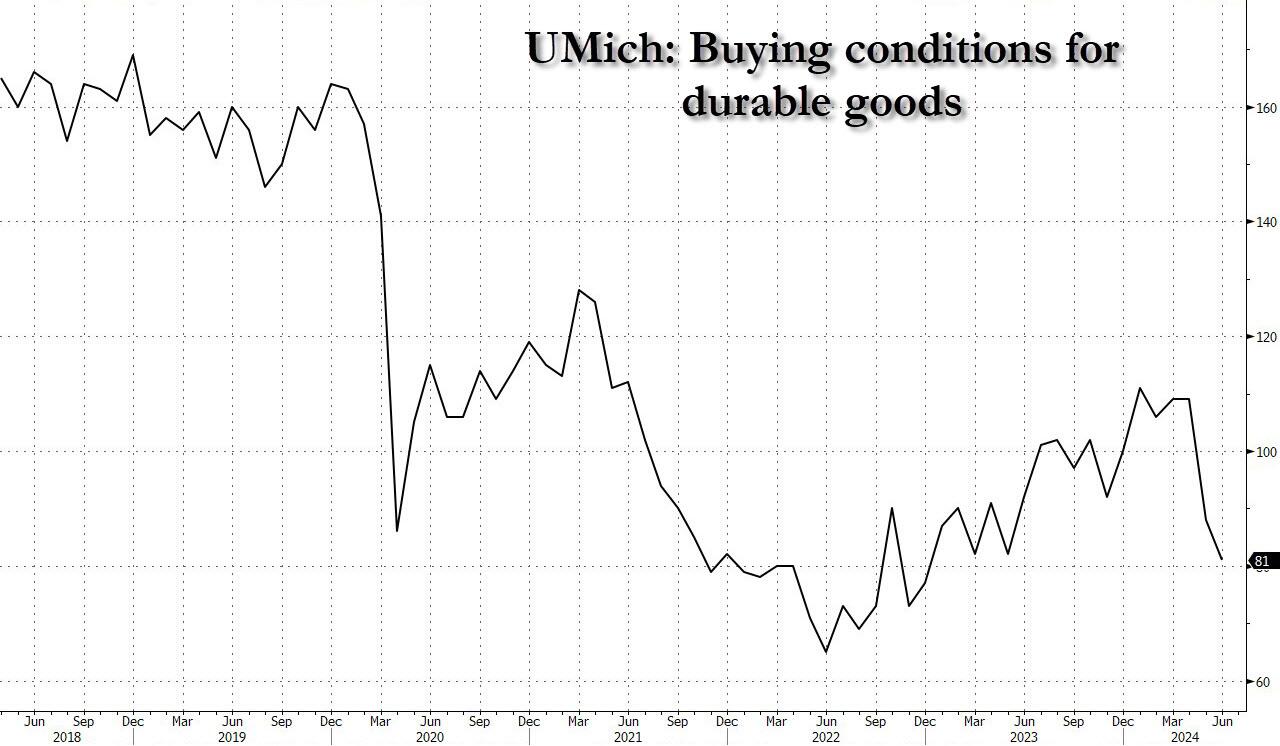

If that wasn’t enough, the slide in sentiment suggests restrained consumer demand in coming months. The university’s measure of buying conditions for durable goods decreased to the lowest level since December 2022, a glowing testament to just how tapped out the US consumer truly is.

In short: the verdict for Bidenomics is in, and it’s a complete disaster, as for Powell’s recent laughable comment that he can’t see the “stag” nor the “flation”… well, Fed chair, they just bit you on the ass.

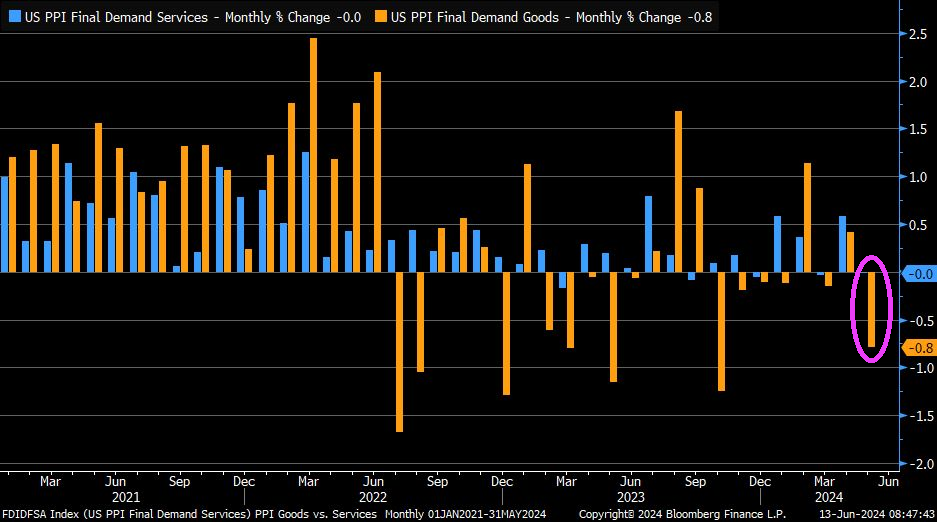

On top of a poor consumer sentiment report, the PPI Final Demand index was down … again.

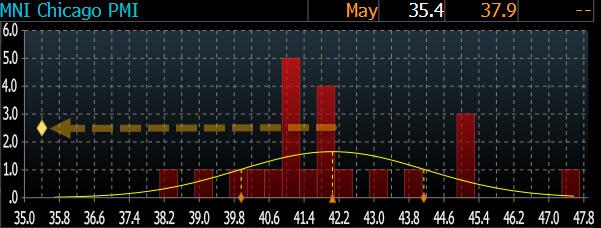

… which seems to suggest that at least according to Chicago-based purchasing managers, the economy is in a depression.

This is how the final number looked relative to expectations.

Looking at the report we find the following:

Business barometer fell at a faster pace; signaling contraction

New orders fell at a faster pace; signaling contraction

Employment fell at a faster pace; signaling contraction

Inventories fell at a faster pace; signaling contraction

Supplier deliveries fell at a slower pace; signaling contraction

Production fell at a slower pace; signaling contraction

Order backlogs fell at a faster pace; signaling contraction

Did nothing rise? One thing did:

Prices paid rose at a slower pace; signaling expansion

So we have not just a depression, but a stagflationary depression in which everything else is going to hell, except prices: they keep on rising.

And while it is unclear what has prompted this unprecedented bearishness (the surely negative contribution from Boeing is likely to blame for a substantial portion of the apocalyptic outlook), one thing is certain: Goldman will have to come up with even more goalseeked surveys that explain away reality and tell us how purchasing managers really should feel…

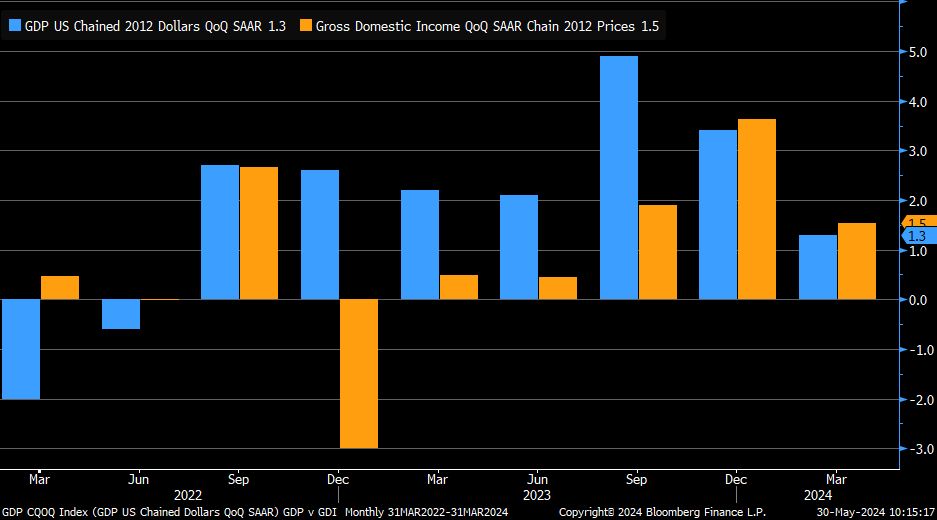

On the good news front, REAL Gross Domester Income rose to 1.5%.

As copper prices keep on rising. Which is bad news for Biden’s shift to EVs! (Once again, Biden is driven around in gas guzzling Chevy Tahoes/Suburbans and owns a Chevy Corvette). There isn’t enough copper production to build the EVs that Biden wants.

I have testified and sat through many trials in New York city and have never seen a court case quite like the one the Trump lost with the Judge effectively telling the jury to find Trump guilty.

I saw former President Obama criticizing former President Trump for not passing “transformative” changes. That is, Trump didn’t sign any Obama-like transformative changes (like Obamacare). Truimp did try to slow down the damage done by Obama and his transformative agenda (e.g., open borders, wealth redistritution, green energy) that Biden has attempted to continue.

As we approach the party conventions and Presidential election of 2024, we saw the Economic Surprise Index (ESI) in May decline to -0.126.

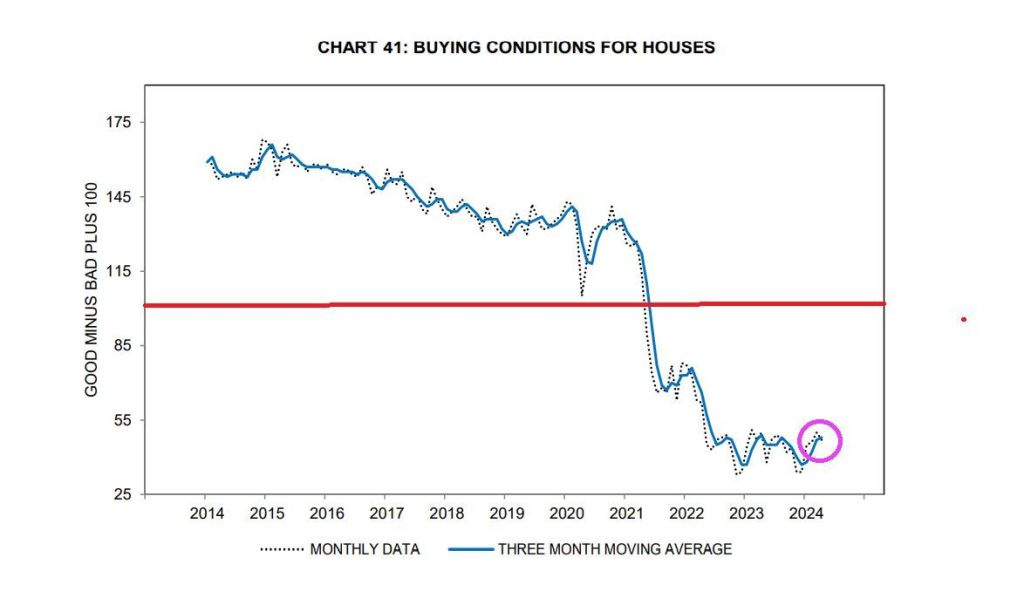

Coupled with Biden’s negative buying conditions for housing (higher mortgage rates and soaring house prices), Obama’s Jacobian transformative economic fantasty is on thin ice.

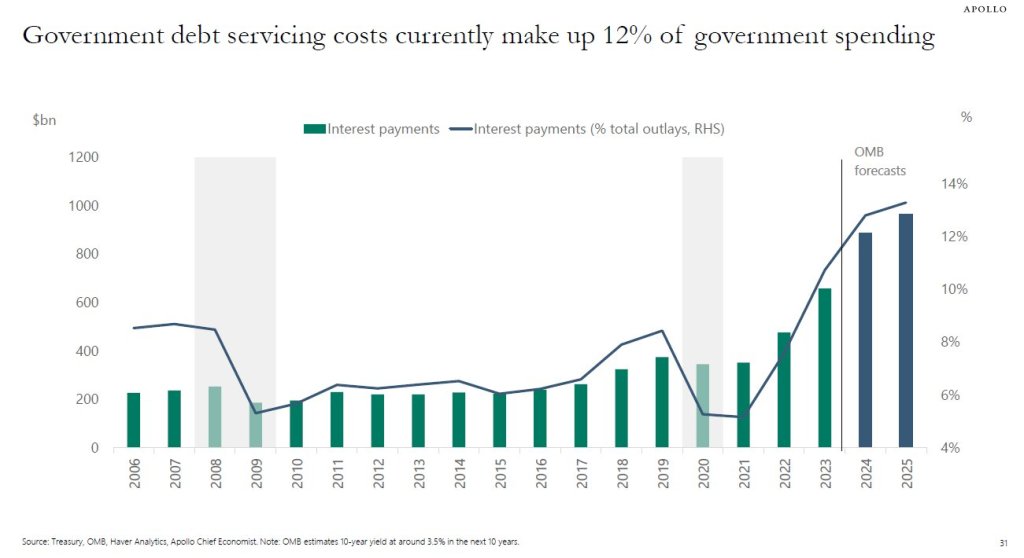

Speaking of higher interest rates, US debt servicing costs currently make up 12% of government spending. Jacobin revolution = Cloward-Piven.

Let’s hope the Obama/Biden Jacobin revolution doesn’t get to this point!

The US middle class and low-wage workers are back on the chain gang while the top 1% party hearty.

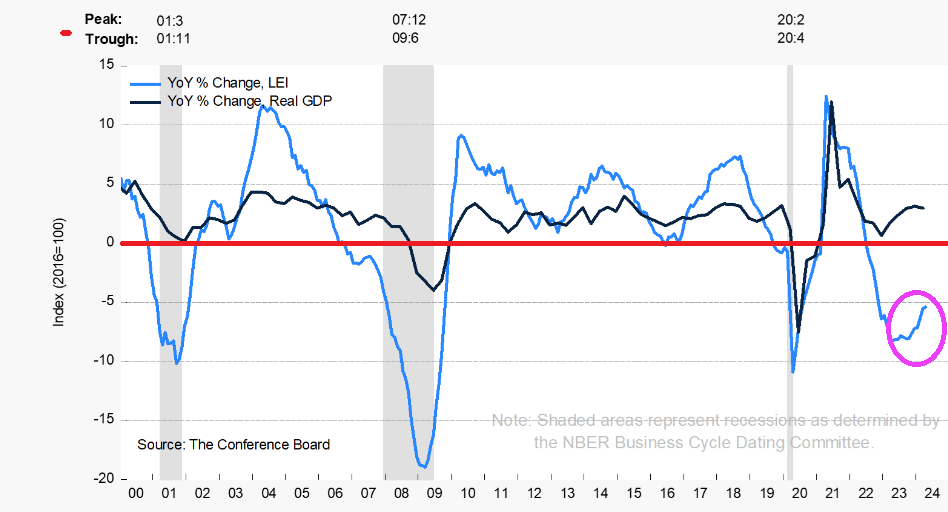

The Conference Board Leading Economic Index® (LEI) for the U.S. decreased by 0.6 percent in April 2024 to 101.8 (2016=100), after decreasing by 0.3 percent in March. Over the six-month period between October 2023 and April 2024, the LEI contracted by 1.9 percent—a smaller decrease than its 3.5 percent decline over the previous six months.

It is surprising that Americans trusts the millionaires in the Administration (like Biden) or Congress (like Schumer, McConnell, etc) to have our backs on the roaring inflation rate. At least Speaker Mike Johnson isn’t a millionaire … yet. But that might explain his selling out conservatives.

One year after regional banks crashed and burned due to the combination of tumbling debt/treasury prices coupled with cratering commercial real estate loans, fears about the current state of Commercial Real Estate – where most offices still see tenants at best 3 to 4 days a week and are literally burning through rents – appear long forgotten. Is that sensible?

For one answer, we turned to the latest report from Goldman’s REIT/CRE expert Chandhi Luthra who has published a visual assessment of the state of CRE in 2024 in terms of loan maturities, 2023 extensions, and property and lender groups. She also looks at the latest transaction and leasing volumes, and shares several key takeaways.

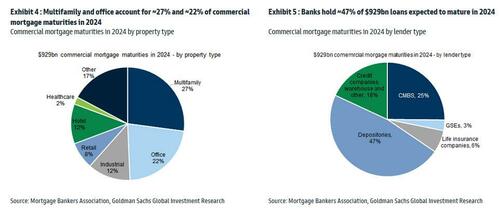

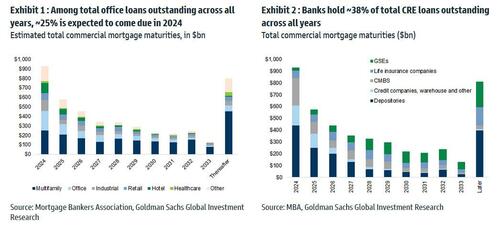

There are ~$4.7tn of outstanding commercial/multifamily mortgages outstanding, according to the Mortgage Bankers Association’s 2023 Commercial Real Estate Survey of Loan Maturity Volumes.

More specifically in 2024, $929bn of CRE mortgages are expected to mature, ~20% of ~$4.7tn total commercial mortgages outstanding. In terms of property type, multifamily and office account for ~27% and ~22% of commercial mortgage maturities in 2024 respectively. In terms of lender type, banks hold ~47% of debt maturing in 2024, followed by CMBS at ~25%.

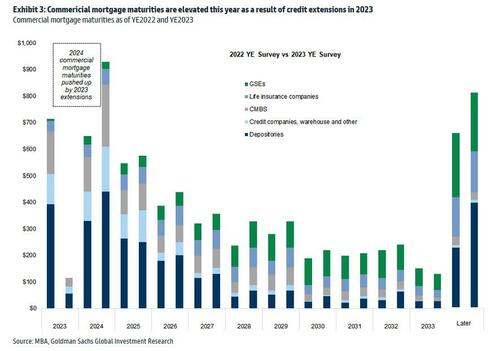

It is worth noting that 2024 commercial mortgage maturities are pushed up by 2023 extensions. As shown in Exhibit 3, among the CRE loans scheduled to mature in 2023, ~$610bn were refinanced, with ~$300bn pushed into 2024 and the remainder into future years. As a result, the total CRE refinancing volume is expected to be ~$929bn in 2024.

Of course, it does not end there, and since there has been no fundamental improvement, it is certain that extension volumes in 2024 will be high as well. However, as interest rates are expected to come down, demand for refinancing in 2024 may outpace that in 2023 according to the Goldman analyst (rates are still far, far higher than where they were when most of the loans were originated several years ago). At the same time, for loans that have already been extended in the past, it is also likely that future extensions could be harder.

Among the loans backed by office properties overall, ~25% is expected to come due in 2024. In terms of lender type, banks (primarily small, regional banks) hold ~38% of total CRE loan outstanding across all years, followed by the GSEs at 20%.

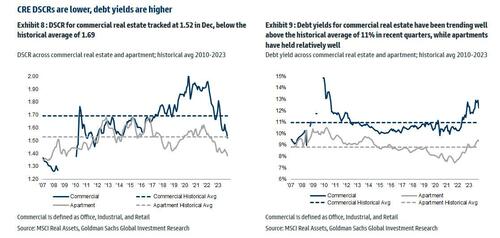

Looking at different debt metrics, DSCR for commercial real estate (office, industrial and retail combined) tracked at 1.52 in Dec, below the historical average of 1.69; debt yields for commercial real estate have been trending well above the historical average of ~11% in recent quarters, while apartments have held relatively well.

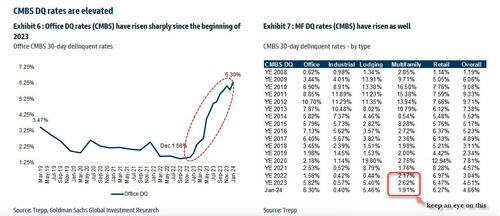

Office CMBS DQs have risen significantly, with Jan tracking at 6.3%, up significantly from 1.58% in Dec 2022. And while everyone knows the Office canary in the coalmine is dead and buried, keep an eye on Multifamily CMBS DQs which tracked at 1.91% vs 2.62% in December, with the sequential decline associated with a large San Francisco apartment loan that was recently disposed. The overall DQ rate tracked at 4.66% in January.

The Goldman strategist concludes with a word about CRE transaction and leasing: U.S. CRE transaction market continues to be muted, primarily driven by elevated interest rates, limited sources of capital, and the pricing gap between buyers and sellers. January volume was down -11% yoy, driven by easier compares in Jan 2023 (down -55%). In terms of leasing, Jan preliminary trends indicate weakness in activities, with office down -25% yoy and industrial down -28% yoy.

Here, Goldman trader Sara Cha chimes in (her report is also available to pro subs) and notes that we can see from the transaction data “why sentiment in CRE brokers is a bit more mixed of late – thought yesterday’s JLL print had mixed reception – while you’ve seen some signs of life in capital markets space broadly to start the year, not seeing that as much on the CRE front (remember those 3Q-4Q greenshoots?).“

Multifamily CRE

The commercial real estate sector continues to experience elevated stress . The latest crack to emerge is the increasing number of delinquencies on multifamily mortgages.

In April, about 8.6% of commercial real estate loans bundled into collateralized loan obligations were distressed, reaching the record high set in January, according to Bloomberg, citing new data from analytics firm CRED iQ.

The loans bundled into CRE CLOs were merged with funds from individual investors to acquire multifamily housing during the Covid era. After that, borrowing rates surged, catching many off guard. A significant portion of the deteriorating loans had floating-rate interest rates, putting massive pressure on landlords’ cash flows, diminishing the market worth of the properties, and obliterating equity in a large number of investments.

According to data provider Trepp, $78.5 billion of CRE CLO loans are outstanding. This means many CRE CLO issuers are racing to find ways to prevent a tsunami of bad loans from defaulting or risk losing the fees they collect on the securities.

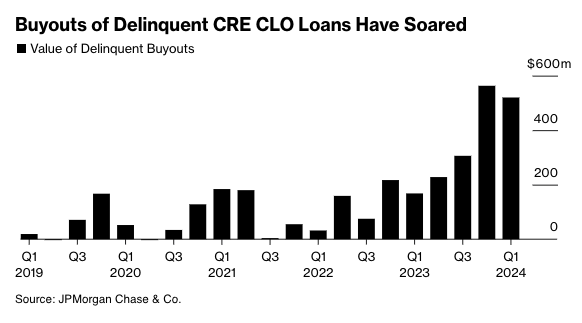

Recent estimates from JPMorgan show lenders purchased $520 million of delinquent loans in the first quarter of this year. Lenders have been ramping up the number of buyouts over the last four quarters because of mounting bad loans in a period of elevated rates.

Source: Bloomberg

JPMorgan strategist Chong Sin said he’s surprised by lenders’ ability to obtain warehouse lines to purchase bad debt, given tightening credit conditions.

“The reason these managers are engaged in buyouts is to limit delinquencies,” Sin said, adding, “The wild card here is, how long will financing costs remain low enough for them to do that?”

Anuj Jain, an analyst at Barclays Plc, expects buyouts to continue as distress increases across the CRE CLO space.

“If the outlook for the Fed shifts materially to hikes or no rate cuts for a while, that might lead to a sharp increase in delinquencies, which can stifle issuers’ ability to buy out loans,” Jain said.

Bloomberg explains much of the CLO space derives from multifamily bridge loans originated around 2021-2022:

CRE CLO issuance surged to $45 billion in 2021, a 137% increase from two years earlier, when buyers of apartment blocks sought to profit from the wave of workers moving to the Sun Belt from big cities. Three-year loans would give them time to complete upgrades and refinance, the thinking went.

Fast forward to today and the debt underpinning many of the bonds is coming due for repayment at a time when there’s less appetite for real estate lending, insurance costs have skyrocketed and monetary policy remains tight. Hedges against borrowing cost increases are also expiring and cost significantly more to purchase now.

Those blows helped increase multifamily assets classed as distressed to almost $10 billion at the end of March, a 33% rise since the end of September, according to data compiled by MSCI Real Assets.

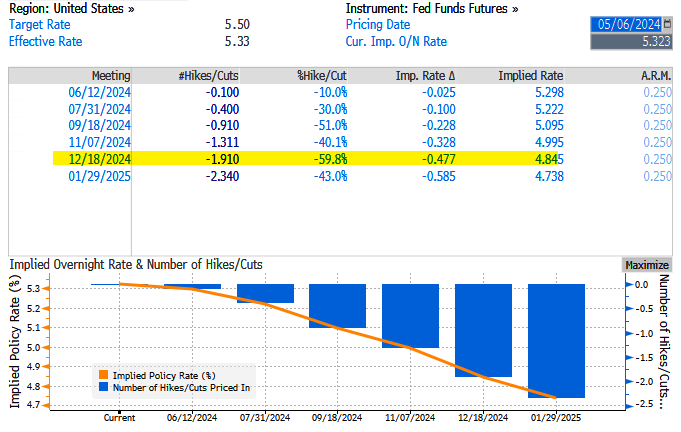

Last Wednesday, the Fed left interest rates unchanged at around 550bps as inflation data reaccelerates and economic growth tilts to the downside, stoking stagflation fears.

Fed swaps are pricing in just under two cuts – this is down from nearly seven earlier this year and about 1.14 before last week’s FOMC.

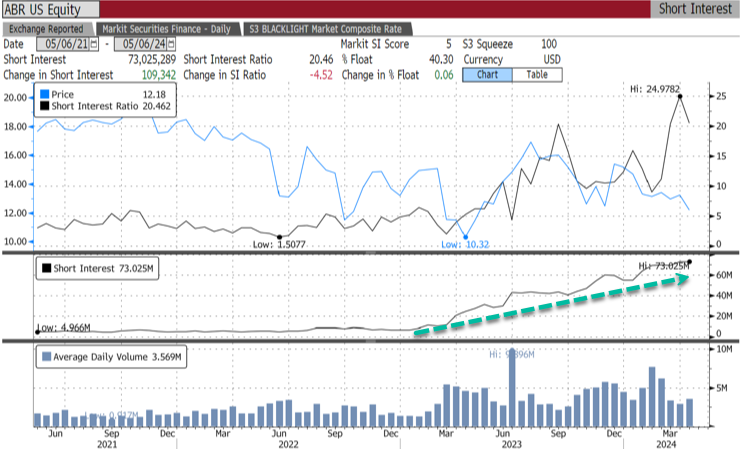

Meanwhile, bears are piling in on CRE CLO issuer Arbor Realty Trust Inc., with 40.3% of the float short, equivalent to 73 million shares short.

“The multifamily CRE CLO market was not prepared for rate volatility,” said Fraser Perring, the founder of Viceroy Research, which has placed bear bets against Arbor, adding, “The result is significant distress.”

The longer the Fed delays rate cuts, the worse the CRE mess will get.

The Green Slime! The global movement towards Green Energy (or global Marxist movement) is really The Green Slime! Or maybe it should be renamed “The Red Slime.”

And then we have Hertz dumping its inventory of EVs. A slew of used Teslas have hit the Hertz car sales website after the company announced Thursday it planned to sell off 10,000 more electric vehicles from its fleet than originally planned, bringing the fire sale’s total to 30,000. Perhaps one of the reasons you can get such a good deal on a Tesla at Hertz right now is that the outlook for EV value retention is pretty grim at the moment.

Given the incidents of electric cars catching fire, perhaps saying its a fire sales is a bad choice of words. But what it says is that DESPITE massive incentives to buy EVs, consumer demand stinks. Although Transportation Secretary Pete Buttigieg will claim the market is booming.

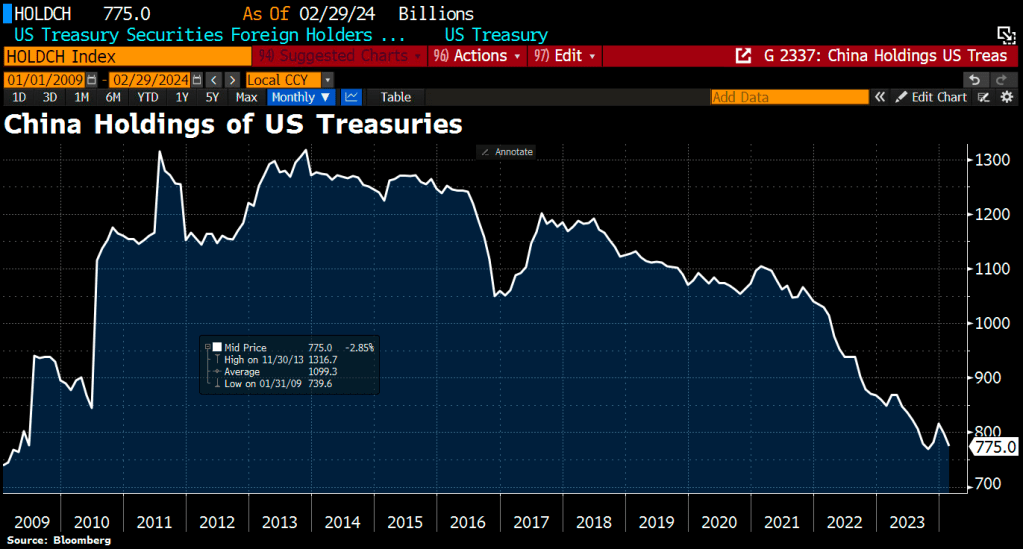

How bad is the trainwreck that is the Biden Regime? China is bailing on US Treasuries.

The Biden Regime is hereafter known as The Green Slime, given their horrible policies. Unfortunately, The Green Slime is here already … and Hertz knows customers don’t want them at least on a temporary basis.

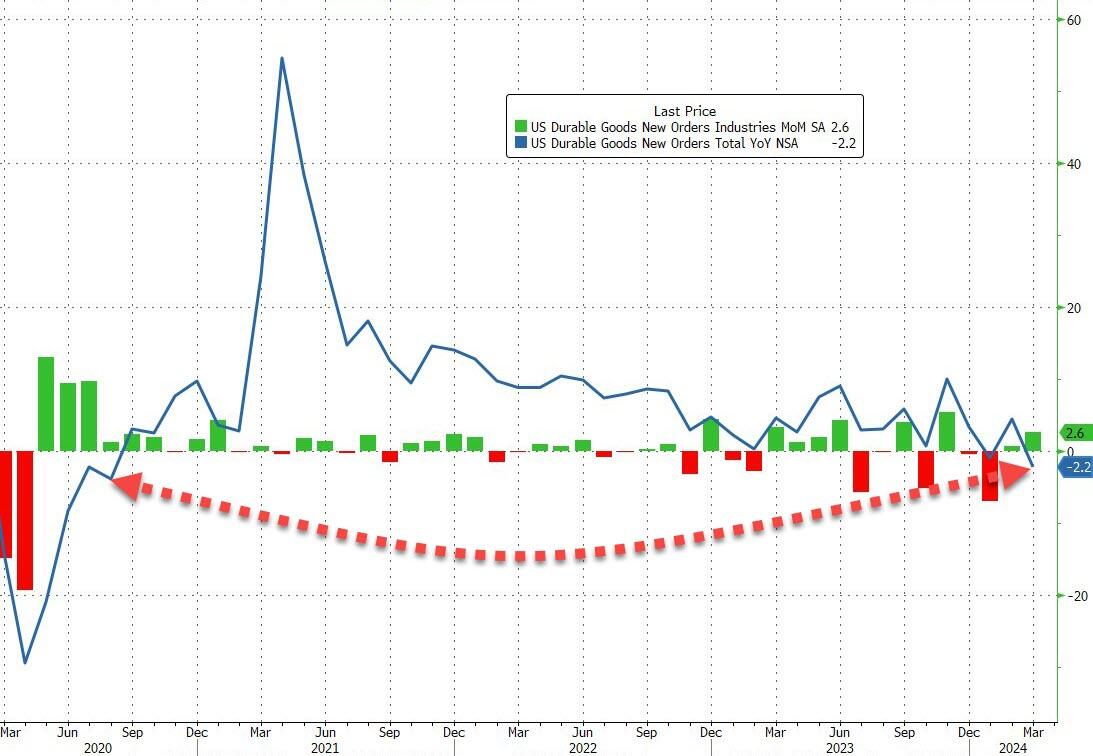

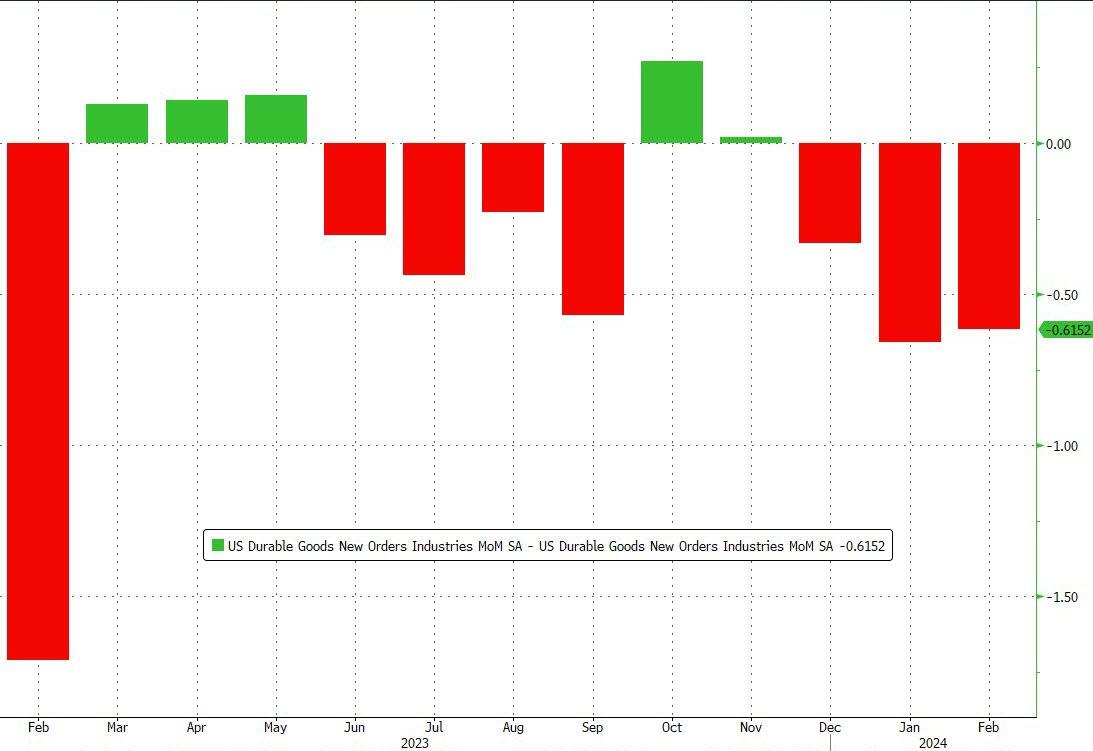

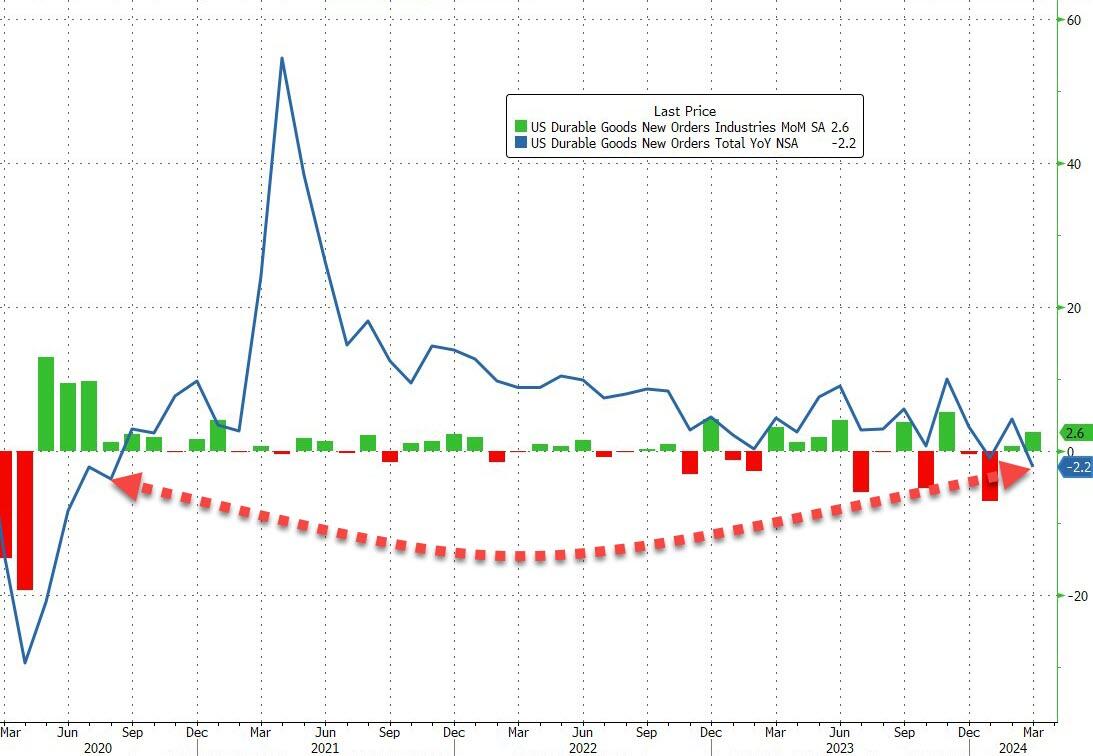

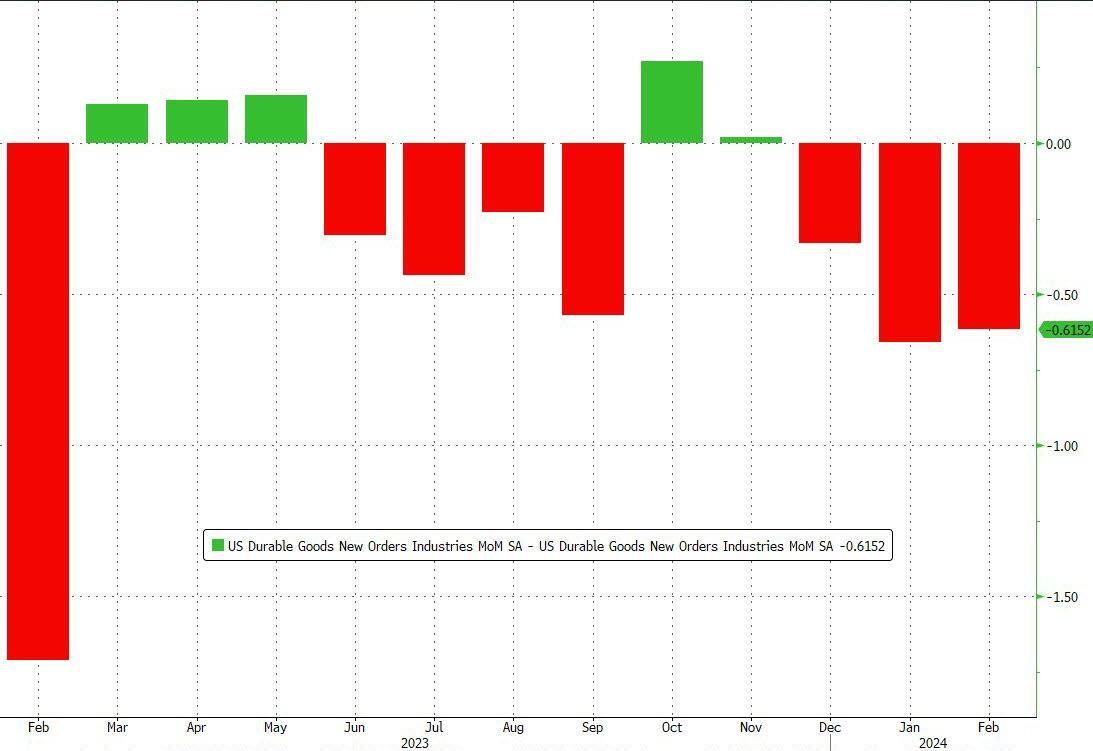

Manufacturer’s Durable Goods New Orders growth peaked in April 2021, thanks in part to M2 Money Growth peaking in February 2021. And its been all downhill since then.

This is the 8th downward revision of durable goods orders in the last year…

Source: Bloomberg

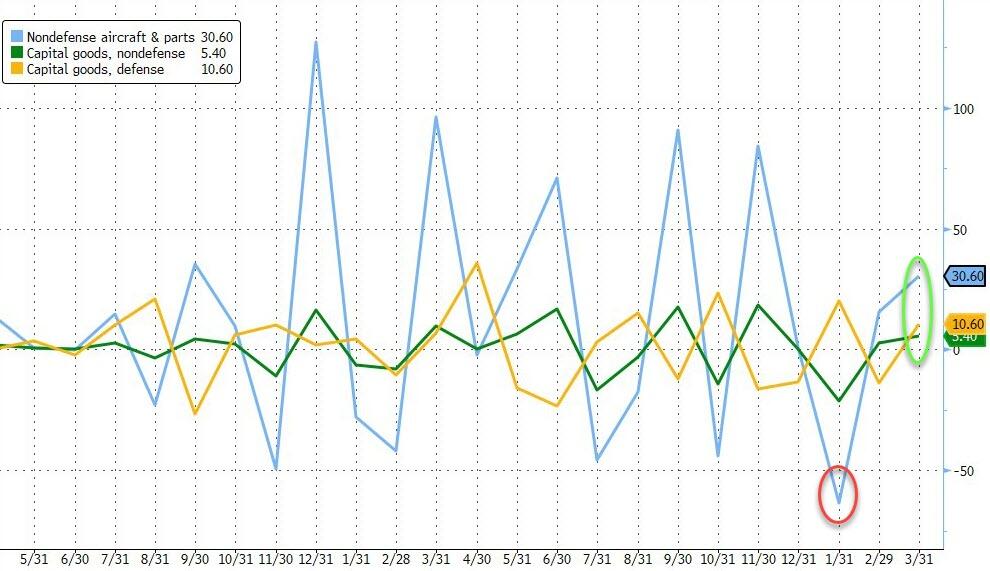

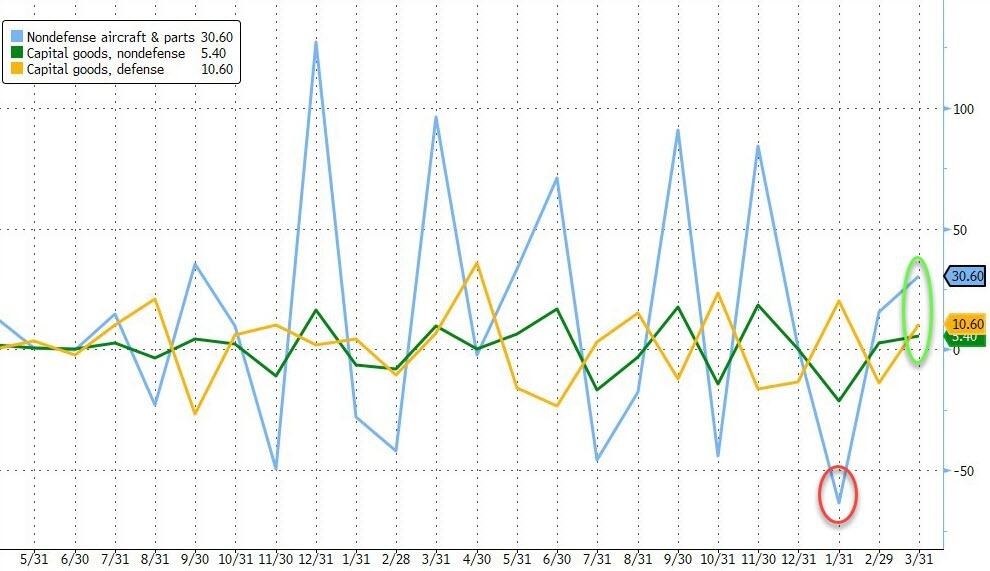

Under the hood, defense and non-defense capital goods orders rose with non-defense aircraft orders surging over 30% MoM…

Source: Bloomberg

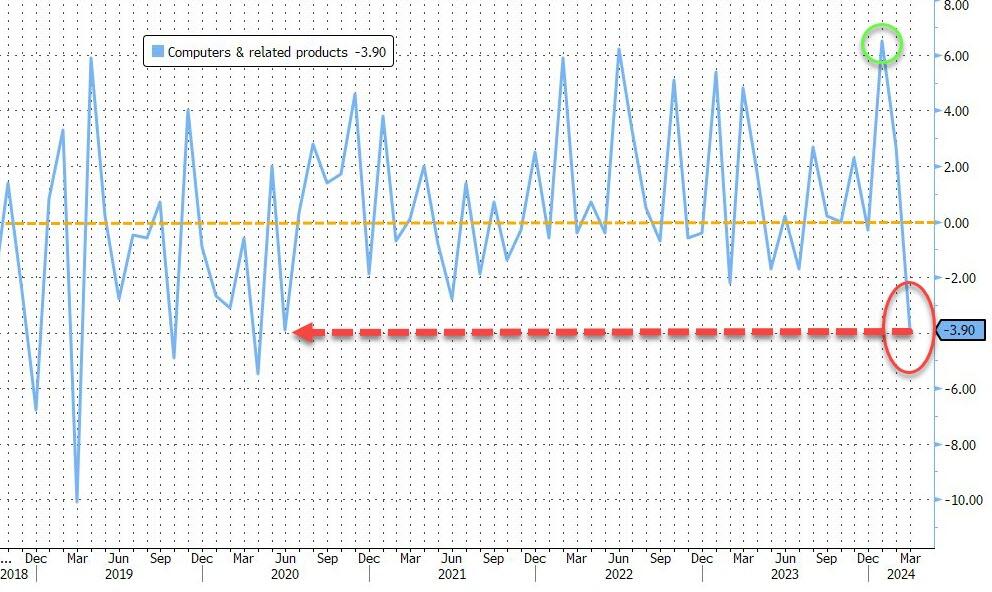

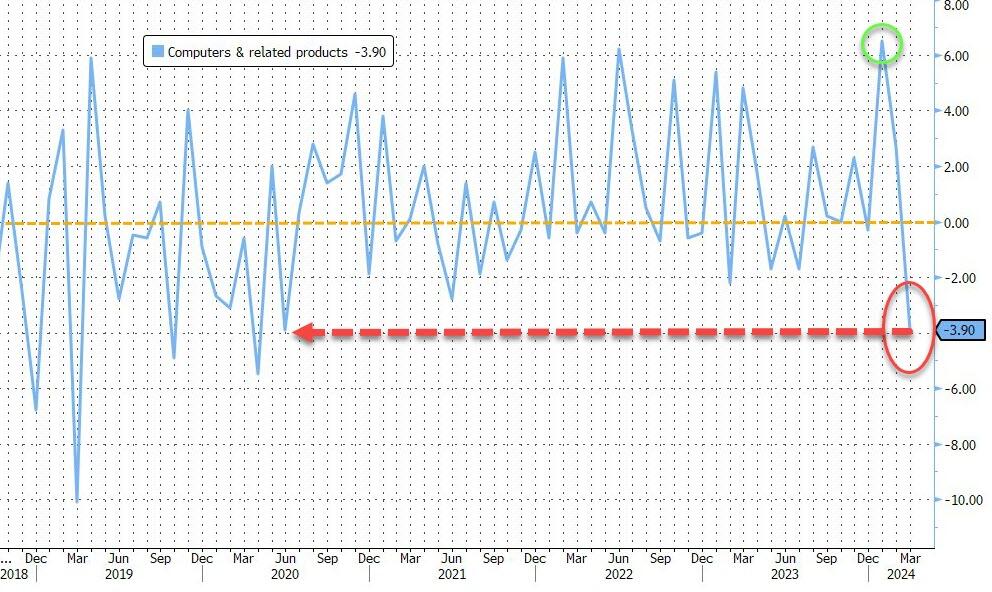

But… it looks like the AI bubble just burst as Computer & related Products orders plunged 3.9% MoM – the biggest drop since COVID lockdowns…

Source: Bloomberg

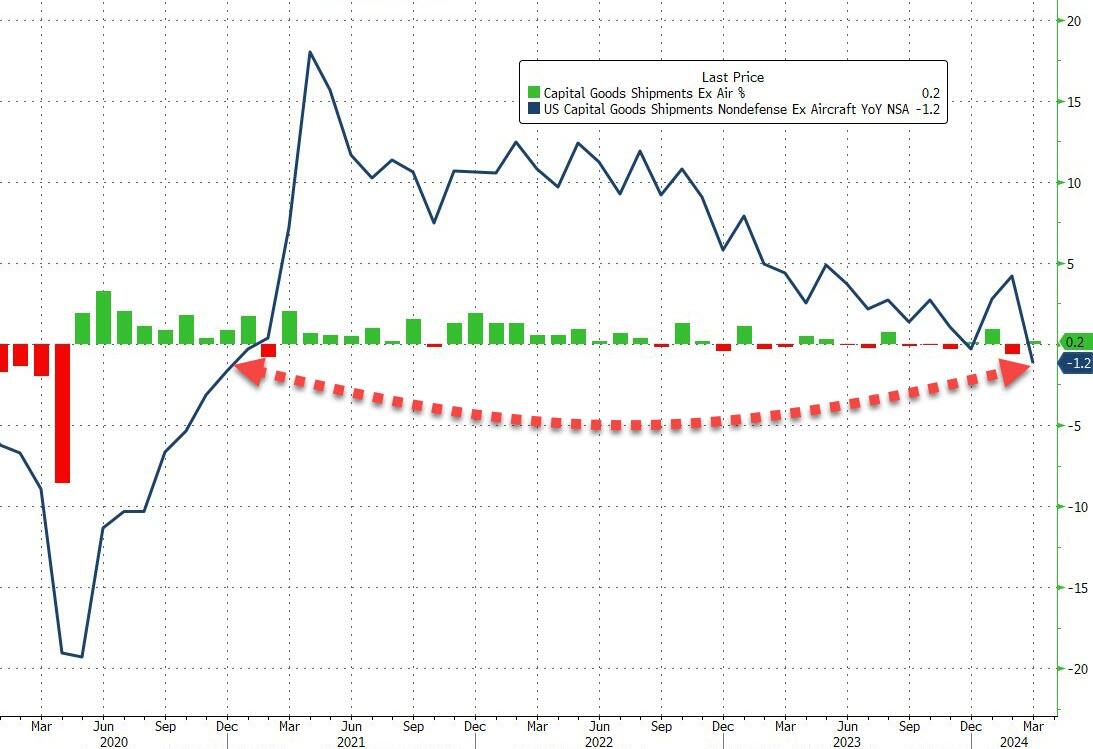

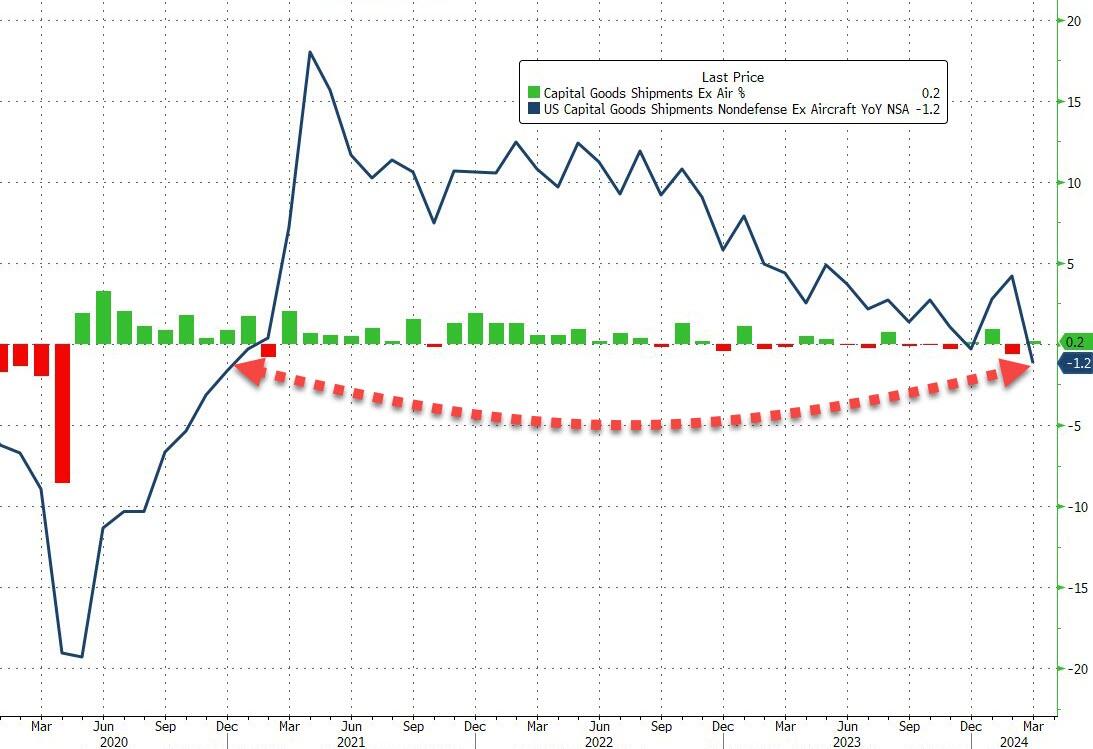

Finally, and more problematically, core capital goods shipments – a figure that is used to help calculate equipment investment in the government’s gross domestic product report – saw only a small 0.2% MoM rise, which left core shipments down 1.2% YoY – the biggest YoY drop since the COVID lockdowns…

Source: Bloomberg

Now that Biden is considering a NATIONAL CLIMATE EMERGENCY granting him 130 War-like powers, I shudder to think for much green spending he will initiate.

Biden: “How many times does Trump have to prove we can’t be trusted?”

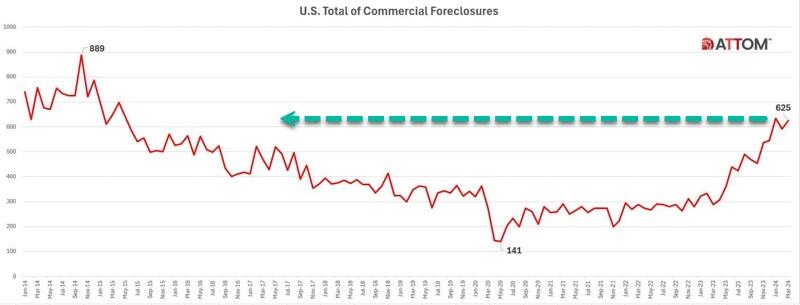

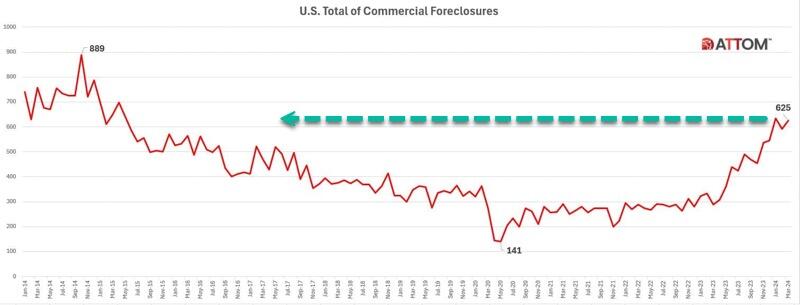

The latest report from real estate data provider ATTOM shows CRE foreclosures topped 625 in March, up 6% from February and 117% from the same period last year.

ATTOM has been tracking commercial foreclosures since 2014. The number of foreclosures is approaching the peak of 889 in October 2014.

“California began experiencing a notable rise in commercial foreclosures in November 2023, surpassing 100 cases and continuing to escalate thereafter,” the report said.

New York, Florida, Texas, and New Jersey also showed increases in CRE foreclosures last month.

Regional banks provide a bulk of the financing for the space. The ongoing mess in the lending space due to tighter conditions adds pressure to the CRE downturn. Banks are expected to set aside more money to cover potential CRE losses.

Last month, Federal Reserve Chair Jerome Powell testified on Capitol Hill, “We have identified the banks that have high commercial real estate concentrations, particularly office and retail and other ones that have been affected a lot,” adding, “This is a problem that we’ll be working on for years more, I’m sure. There will be bank failures, but not the big banks.”

Data from a recent Treasury Department’s Financial Stability Oversight Council (FSOC) warned office vacancy rates have climbed sharply in recent years, reaching a record of 13.1% at the end of 2023.

CoStar analyst Phil Mobley recently noted the “reset in office demand has rocked US markets.”

Morgan Stanley warned earlier this year that office prices could plunge 30% due to sliding demand.

For those wondering why the excess supply of office towers can’t be converted into affordable housing, Goldman also noted that prices must drop 50% for housing conversions to make sense.

Powell has a rolling crisis on his hands. And the goal is to save the fireworks for after the election.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.