The US economy got beaten to a pulp by the Chinese Wuhan Covid virus outbreak in early 2020. The Fed intervened with massive money printing along with massive spending by Congress and the Administration. Result? 40-year highs in inflation and a Fed counterattack in terms of rate hikes.

The result of Fed rate hikes? Failing regional banks trying to cope with duration extention and scared depositors. And then we have the St Louis Fed Financial Stress index reaching its highest level since the Covid outbreak of early 2020. And with that, bond volatility is higher than that found during the Covid crisis.

With the expectation of MORE rate hikes, the 10-year Treasury yield jumped 12 basis points.

The architect of The Fed’s “too long for too long” is also the US Treasury Secretary, Janet Yellen.

As The Fed attempts to fight inflation, rates are rising. Consequently, deposits are all commercial banks are falling.

The Fed just released its weekly commercial bank data dump showing deposit inflows/outflows.

Two things to note:

1) This is for the week up to 3/15/23 (which includes the SVB collapse but nothing more)

2) ‘Large Banks’ includes the top 25 banks (which means SVB was among that group, hence, we get no indication of SVB rotation flows)

The overall data shows that domestic commercial banks saw over $98 billion in deposit outflows (seasonally-adjusted) that week to just over $17.5 trillion (8th straight week of aggregate outflows).

Source: Bloomberg

That is the largest (seasonally-adjusted) outflow since April 2022 (tax-related?) as we suspect much of that flowed into money-markets. Deposits have been on a steady decline over the past year or so, falling $582.4 billion since February 2022.

There was a notable rotation however with the large banks seeing deposit inflows of $117.9 billion on a non-seasonally-adjusted basis (the biggest weekly inflow since Dec 2021).

Small banks, on the hand, saw a massive $111 billion outflow (non-seasonally-adjusted)…

Source: Bloomberg (note different scales)

That is the largest weekly outflow ever (by multiples) and drops ‘small bank’ total deposits to the lowest since Sept 2021…

Source: Bloomberg

Bear in mind this data does not include the last 10 days, where we have US regional banks all tumbling further and Yellen offering no guaranteed deposits, FRC stock collapse amid bailouts (though that will skew the data due to that $30bn infusion), and the fear of Credit Suisse’s collapse.

Will banks start to compete for deposits? (Well not the biggest ones, for sure)…

The Federal Reserve never died. In fact, The Fed is growing its balance sheet again. Why? A slowing economy and weakness in the banking sector (thanks to inflation and the Fed trying to get inflation back to 2%.

And the banking fiasco keeps rolling, particularly in Europe where Credit Suisse has been in the news for failing and now my former employer, Deutsche Bank (aka, The Teutonic Titanic).

Deutsche Bank AG became the latest focus of the banking turmoil in Europe as ongoing concern about the industry sent its shares slumping the most in three years and the cost of insuring against default rising.

The bank, which has staged a recovery in recent years after a series of crises, said Friday it will redeem a tier 2 subordinated bond early. Such moves are usually intended to give investors confidence in the strength of the balance sheet, though the share price reaction suggests the message isn’t getting through.

“It is a clear case of the market selling first and asking questions later,” said Paul de la Baume, senior market strategist at FlowBank SA. “Traders do not have the risk appetite to hold positions through the weekend, given the banking risk and what happened last week with Credit Suisse and regulators.”

Deutsche Bank slumped as much as 15%, the biggest decline since the early days of the pandemic in March 2020. It was the worst performer in an index of European bank stocks, which fell as much as 5.7%. Crosstown rival Commerzbank AG, Spain’s Banco de Sabadell SA and France’s Societe Generale SA also saw steep drops.

The widespread declines undermine hopes among authorities that the rescue of Credit Suisse Group AG last weekend would stabilize the broader sector. Central banks from the Federal Reserve to the Bank of England this week raised interest rates once again, keeping their focus on inflation amid hopes that the worst of the financial turmoil was past.

All week, regulators and company executives have sought to reassure traders about the health of the banking industry. Deutsche Bank management board member Fabrizio Campelli said Thursday that the government-brokered takeover of Credit Suisse by UBS is “no indication” of the state of European banks.

Standard Chartered Plc Chief Executive Bill Winters said Friday that while there are still some issues to be addressed, “it seems that the acute phase of the crisis is done.”

The latest moves in Europe follow losses in US banks, which tumbled Thursday even after Treasury Secretary Janet Yellen told lawmakers that regulators would be prepared for further steps to protect deposits if needed.

And apparently bank bailouts never died. They just got relabeled.

And on growing banking fears, the 10-year Treasury yield is down -11.7 basis points.

I feel like I am watching the Star Trek original series episode “The Doomsday Machine” as former Fed Chair and current US Treasury Secretary effectively just guaranteed ALL US bank deposits. Aka, a massive bank bailout. The episode was about a robot space vehicle that destroy planets … and anything in its path. And if it changed course to destroy something, it gradually returned to its original destructive path. Like The Federal Reseve.

But after a few days of declining Treasury yields because of the mess created by Bernanke/Yellen’s too low for too long policies, and the Biden/Congress insane spending, the US Treasury 2-year yield is up 16.1 basis points.

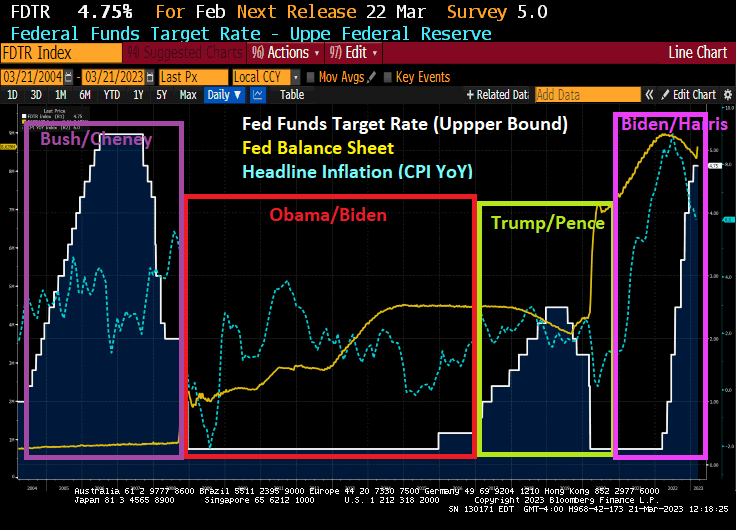

Whether it was politcally motivated to protect Obama/Biden or Obama/Biden’s economic recovery was terrible, The Fed only raised their target rate once before Trump’s election. And then Yellen raised rates like crazy. Only to hand her mess off to Powell who had to drop rates like a rock and massively expand the balance sheet … again … to fight Covid.

Its Gov’t Gone Wild! Insane spending budget by “Sloppy Joe” Biden, Yellen asking Warren Buffet for banking advice (seriously??), a war in Ukraine that America doesn’t seem to actually want to win, etc. But its the banking system where banks are getting crushed by rising inflation and interest rates (but failed to hedge). Sigh.

As I always told my investments and fixe-income students at University of Chicago, Ohio State University and George Mason University, a 10 basis point change in the 2-year and 10-year US Treasury yield is a big deal. This morning, the US Treasury 2-year yield fell -32 basis points while the 10-year Treasury yield fell -14.8 basis points.

At the same time, gold 3.8% and silver rose 4.7% on banking fears.

Debt would hit a new record by 2027, rising from 98 percent of GDP at the end of 2023 to 106 percent by 2027 and 110 percent by 2033. Nominal debt would grow by $19 trillion, from $24.6 trillion today to $43.6 trillion by 2033.

Deficits would total $17.1 trillion (5.2 percent of GDP) between FY 2024 and 2033, rising to $2.0 trillion, or 5.1 percent of GDP, by 2033.

Spending and revenue would average 24.8 and 19.7 percent of GDP, respectively, over the next decade, with spending reaching 25.2 percent of GDP and revenue totaling 20.1 percent by 2033. The 50-year historical average is 21.0 percent of GDP for spending and 17.4 percent of GDP for revenue.

Proposals in the budget would reduce projected deficits by $3 trillion through 2033, including $400 billion through 2025 when it could help fight inflation. The budget proposes $2.8 trillion of new spending and tax breaks, $5.5 trillion of revenue and savings, and saves $330 billion from interest.

The budget relies on somewhat optimistic economic assumptions, including stronger long-term growth, lower unemployment, and lower long-term interest rates than the Congressional Budget Office (CBO). The budget assumes 0.4 percent growth this year, 2.1 percent growth next year, and 2.2 percent by the end of the decade – compared to CBO’s 0.1 percent, 2.5 percent, and 1.7 percent, respectively. The budget also assumes ten-year interest rates fall to 3.5 percent by 2033, compared to CBO’s 3.8 percent.

And then we have Sloppy Joe and Statist Janet Yellen meeting with mega donor Warren Buffet for advice on dealing with the banking crisis … made by Biden’s energy policy and insane Covid spending by the Administration. And, of course, The Fed’s “too low for too long” monetary policy. What is 92-year old Warren Buffet going to say?

Meanwhile, Fed Funds Futures are pointing to one more rate hike then a series of rate cuts down to 3.737 by January 2024.

All together now. The Fed has been printing too much money for too long and Biden restricts fossil fuel production. Ad in rampant Federal spending and we have INFLATION. Inflation led to The Fed to raise rates. And with rate increases and down go the banks.

Of course, The Fed and Biden Administration will overeact (e.g. offering deposit insurance on ALL deposits above $250,000 creating moral hazard risk). As such, we are seeing gold prices soar by 2% this AM.

In adddition to gold rising 2%, natural gas futures are up 6%

The Silicon Valley Bank failure (along with NY’s Signature Bank) are sending shock waves through the global economy. Not because of the incompetence of bank regulators, but because of the reaction function from the FDIC and Fed.

The 10-year Treasury yield is down -26 basis points in the AM. And the Fed Funds Target Rate is expected to drop to 4.7%.

Its not just the US Treasury yield that declined -26 basis points. European sovereign yields are down too (Germany 10-year is down -32.9 basis points).

Look at the 2-year Treasury yield. Its down -54.6 basis points.

On a sad note, Resident Biden is calling for stricter regulations for the banking industry, already one of the most regulated sectors of the economy. How about less politics and just make them do their ^*T^R jobs!

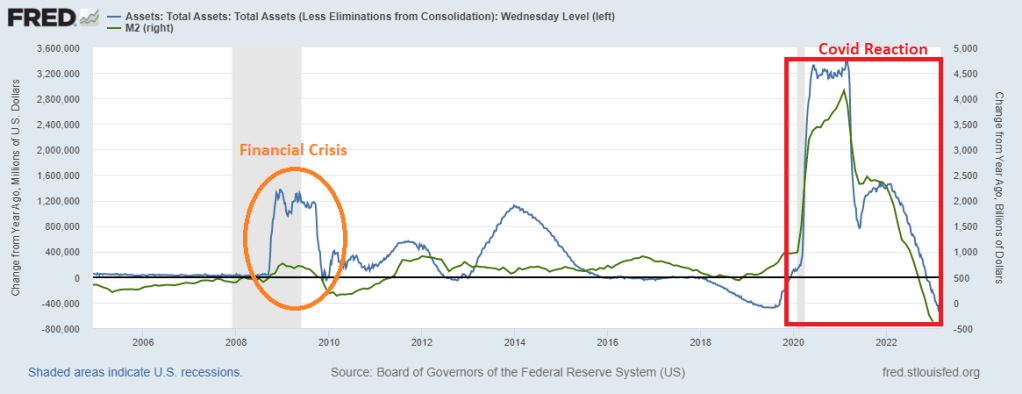

But despite how bad the financial crisis of 2008/2009 was, the growth of Fed assets on it balance sheet (orange oval) paled in comparison to The Fed’s overreaction to the Covid outbreak of 2020. And the government shutdowns and mask mandates.

The good news? The rate of growth YoY of both The Fed’s balance sheet and M2 Money is negative. But it is still startling to see the comparison of Fed reactions to crises.

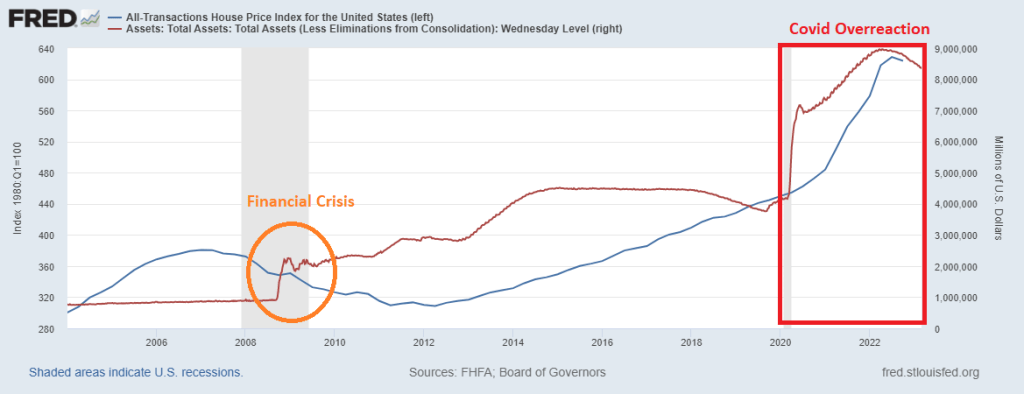

Give The Fed three steps to catch up to the mayhem they created. Particularly in inflation home prices.

What a mess in Washington DC. While House Republicans are at lagerheads with Senate Democrats and Resident Biden over Federal spending cuts, the price of insuring against a debt default just rose to 76.75.

How bad it that? Put it this way. Millions are fleeing Mexico and Guatemala and coming to the US. But Mexico has a lower cost of insuring against a debt default than the USA. And Guatemala is almost as expensive as the USA.

It will all be over soon, according to CDS prices.

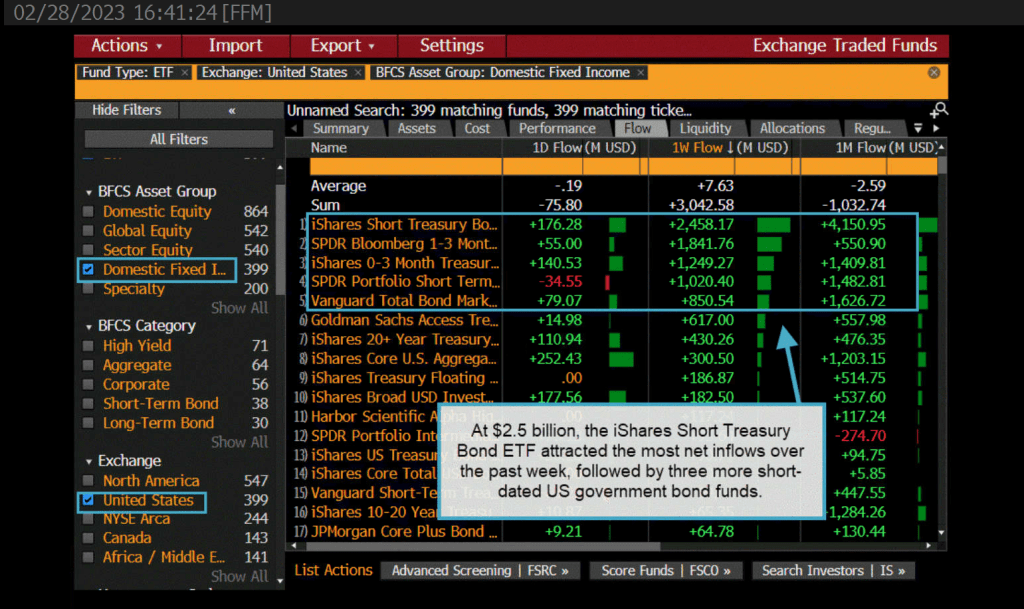

As The Federal Reserve reaffirms their draining of the monetary punch bowl, we are seeing investors flock towards the bond market. Particularly the iShares Short Treasury ETF. $2.5 BILLION to be exact.

Meanwhile, credit ETFs are hammered by record outflows of almost $12 Billion.

The reason why? Inflation remains elevated which is leading The Fed to keep their foot on the monetary brake pedal.

You must be logged in to post a comment.