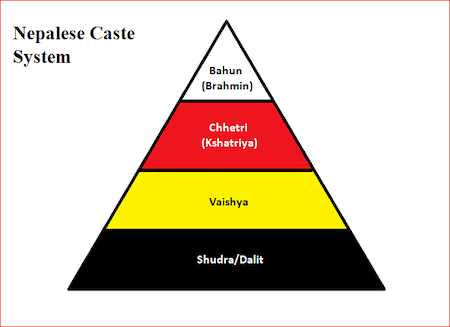

The Federal Reserve has created America’s version of India’s caste system. At the top of the neo American caste system are bankers and the political donor class. The top 1%. The other 99% are losing ground to the Brahmin Banker Class.

In 1913, Woodrow Wilson and his progressives promised that the Federal Reserve would avert both depressions and inflation, while preventing the wealthy from controlling America’s financial markets at the expense of the poor, the new untouchable class.

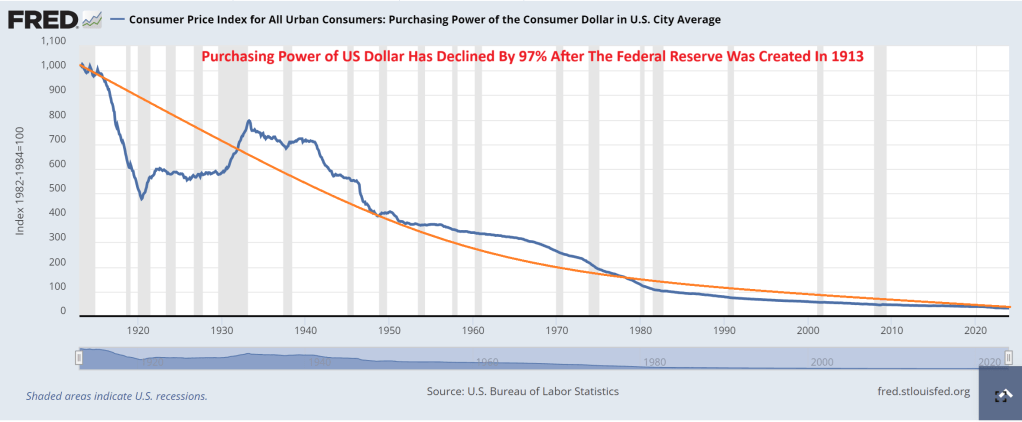

More than a century later, it’s clear that was all a lie, and the Fed has helped create a permanent American underclass (political untouchables). The Fed was designed to transfer wealth from the American people to the government, mostly through the hidden tax of inflation. But this process has prevented countless American families from being able to save and get ahead, because their savings are constantly losing value.

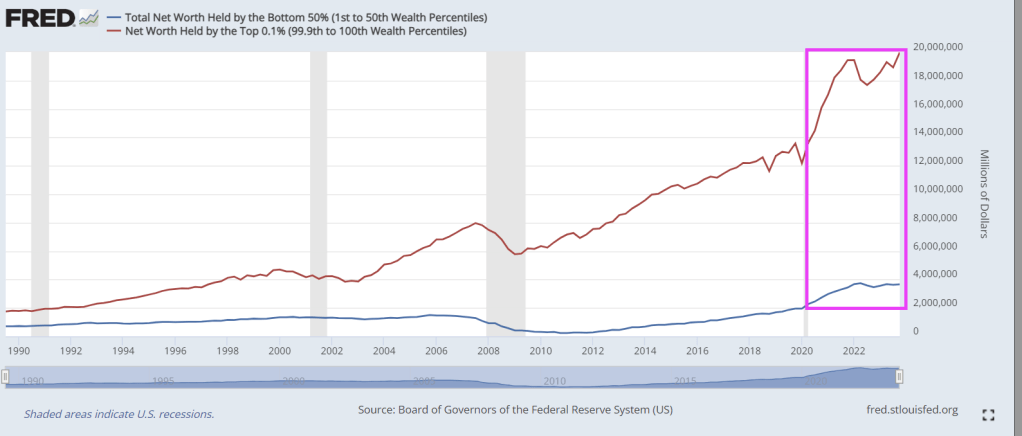

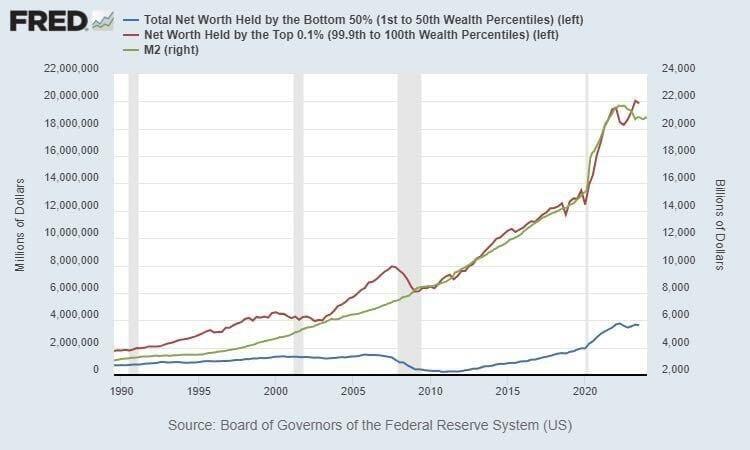

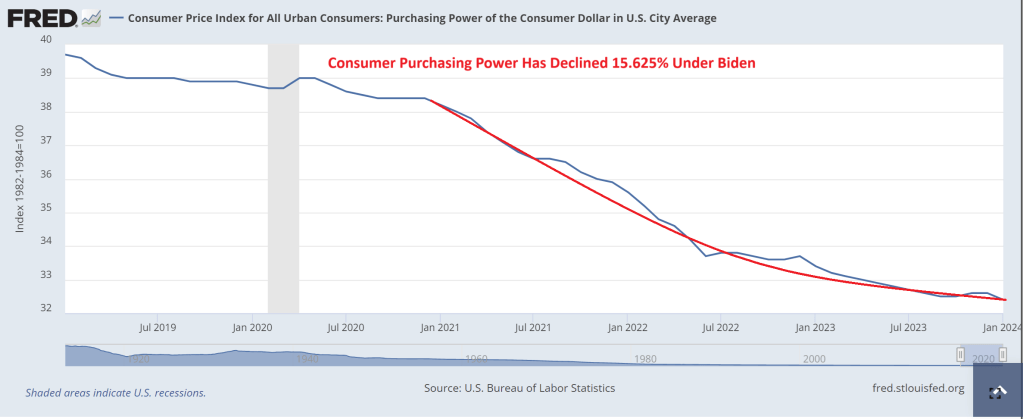

As you can see, the Brahmin Banker class (top .1% of net worth) are beating the socks off the bottom 50% of the new American caste system. This problems has greatly accelerated under Biden’s Reign of Error.

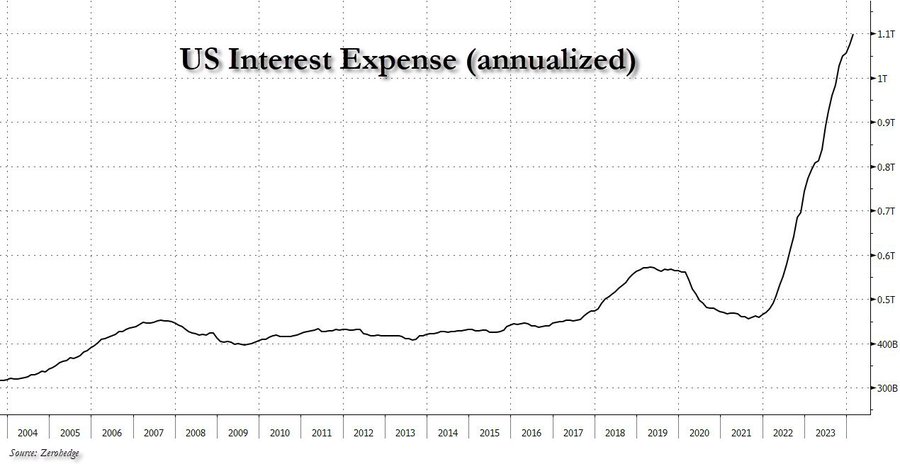

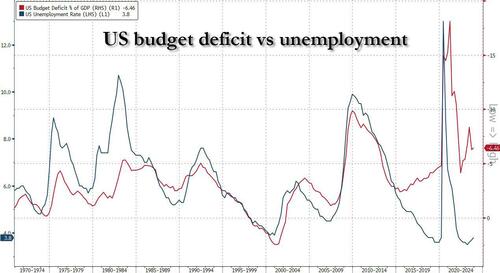

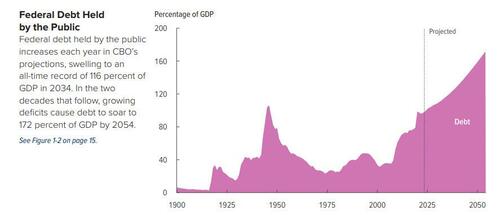

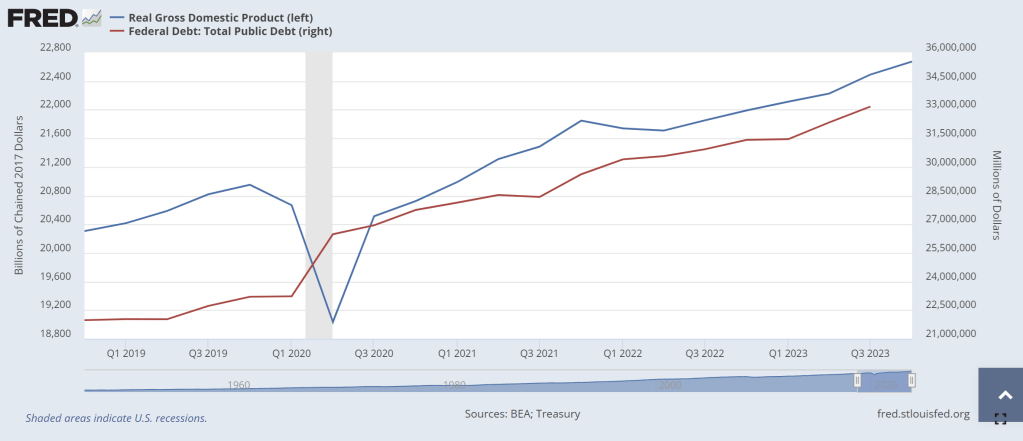

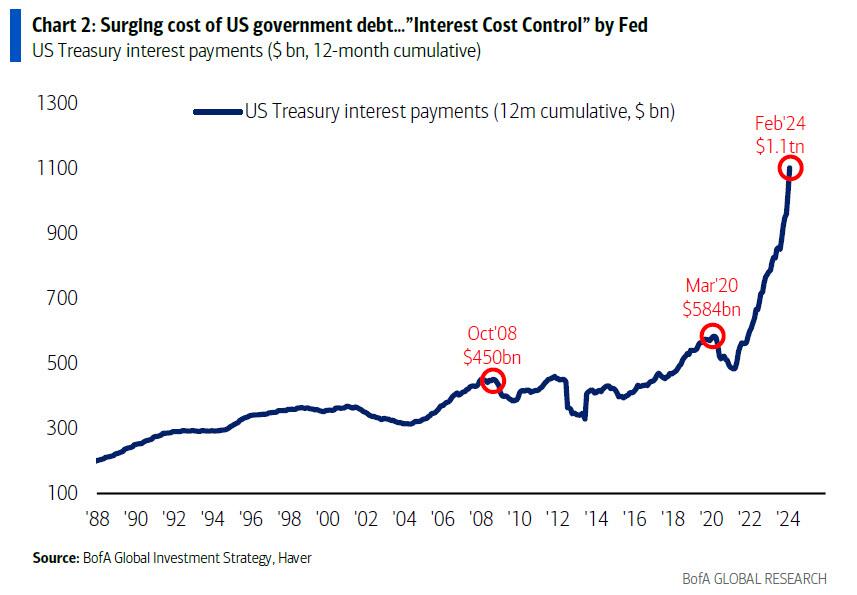

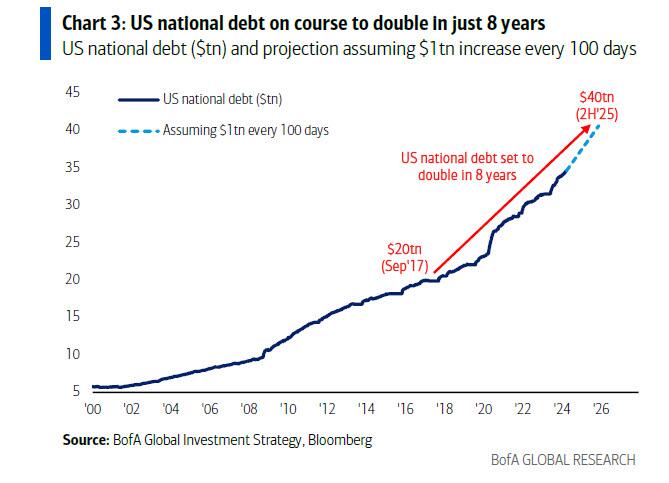

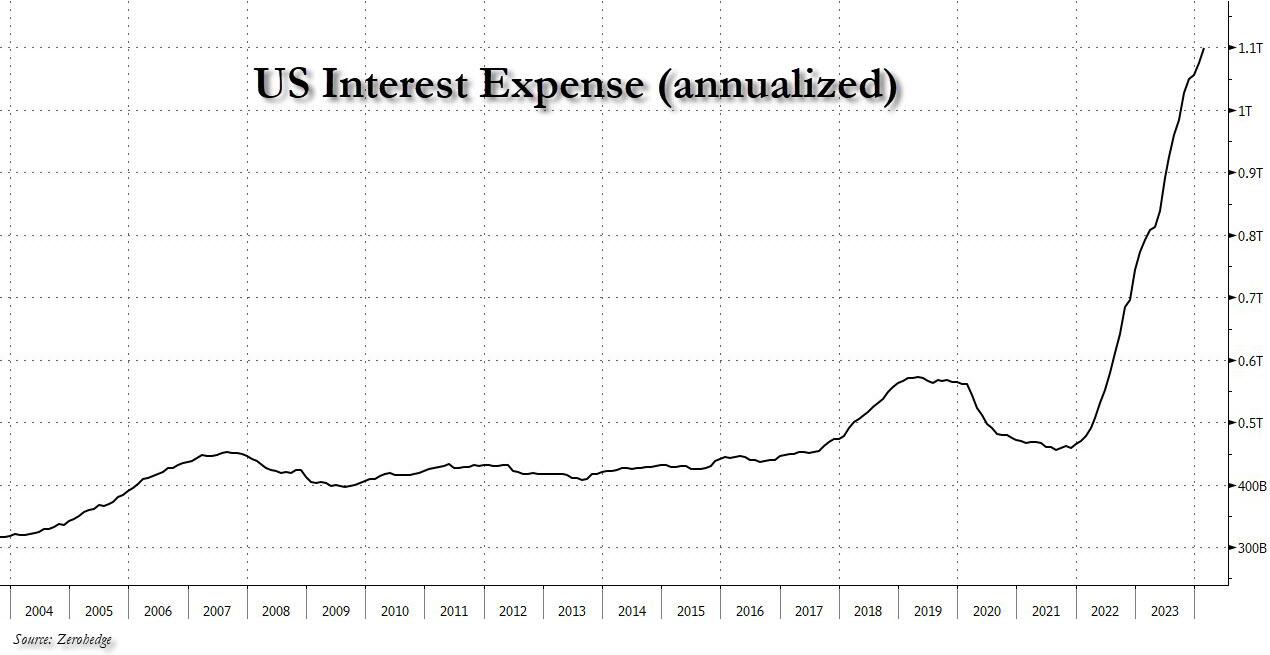

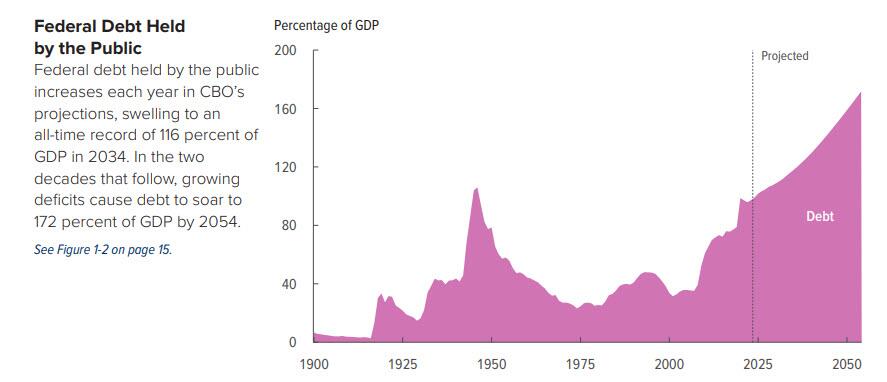

For two decades, the Fed kept interest rates artificially low to help finance massive government spending. When that spending reached unprecedented heights in 2020, the Fed intervened more drastically than ever, creating trillions of dollars and devaluing the currency.

Thus began an unparalleled transfer of wealth that continues to this day, and which has driven a wedge between different groups of Americans.

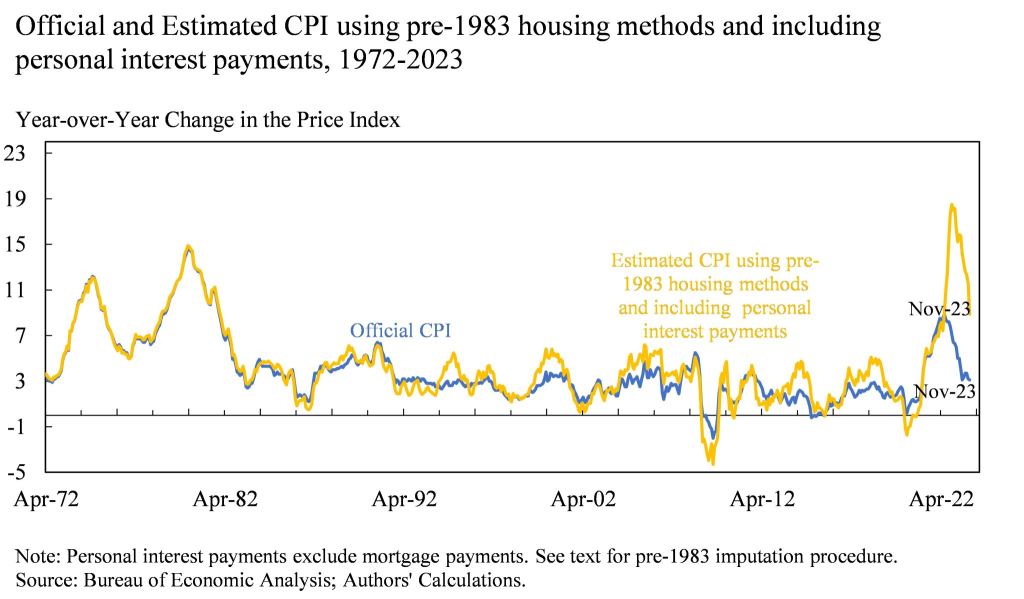

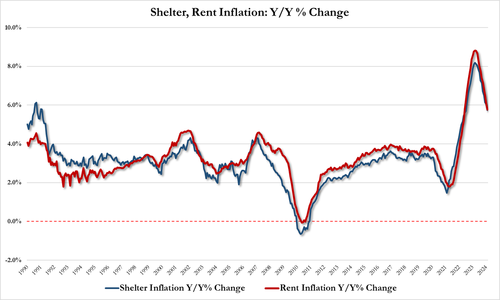

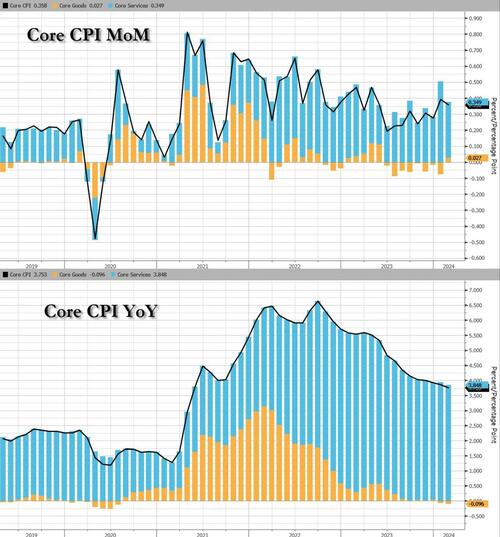

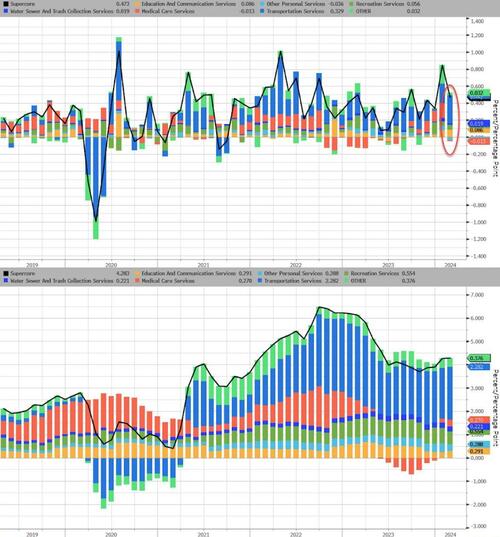

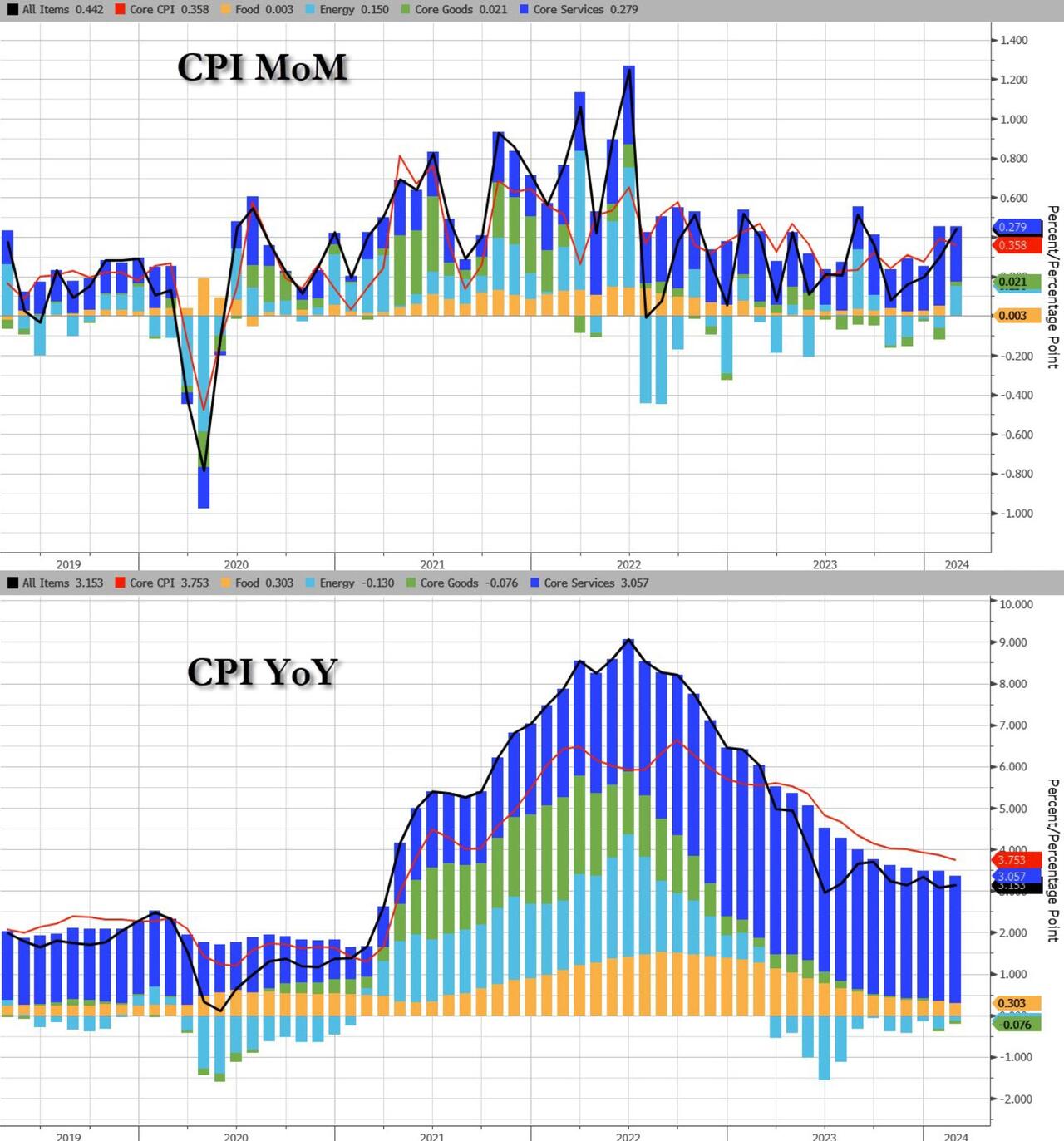

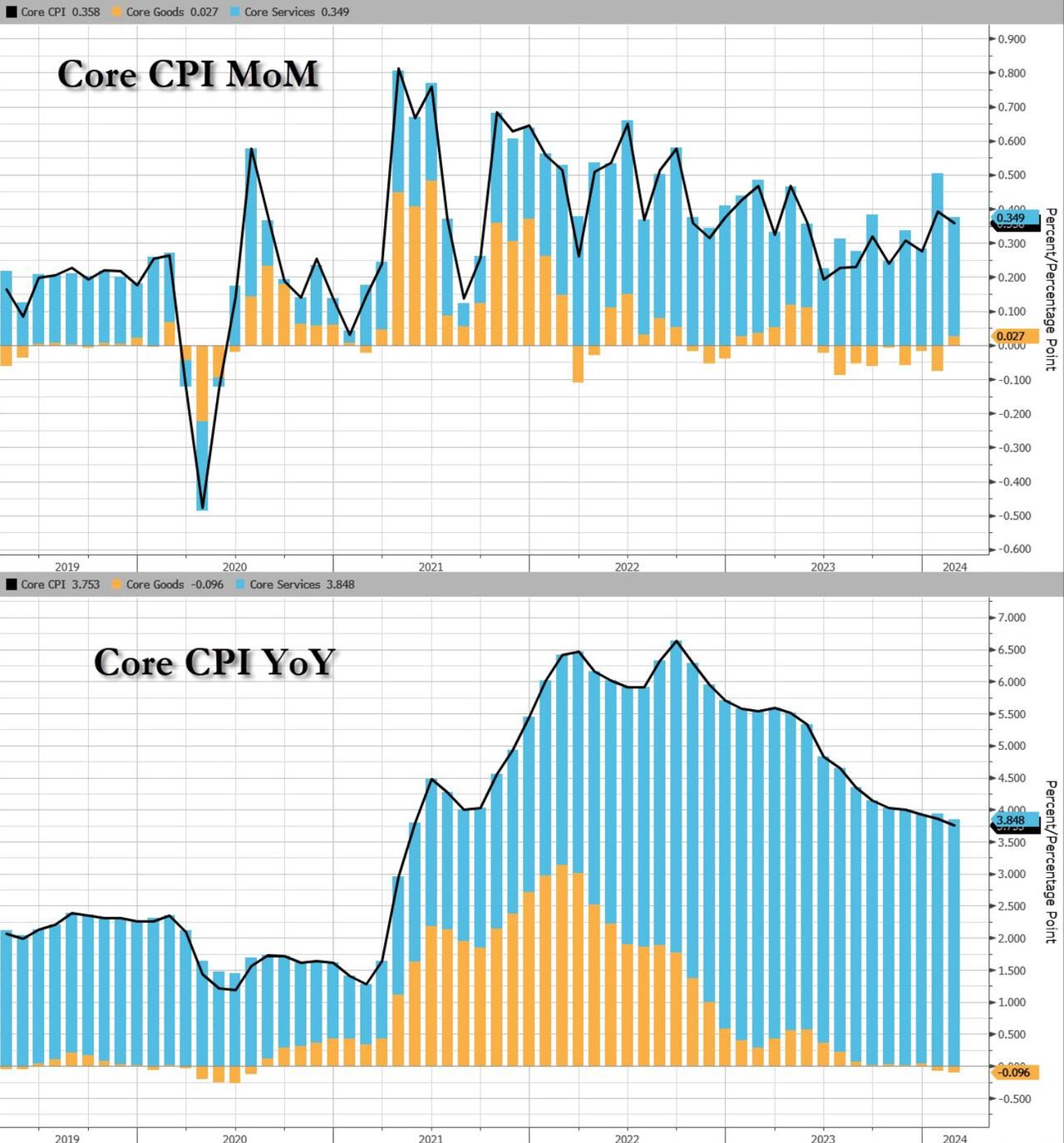

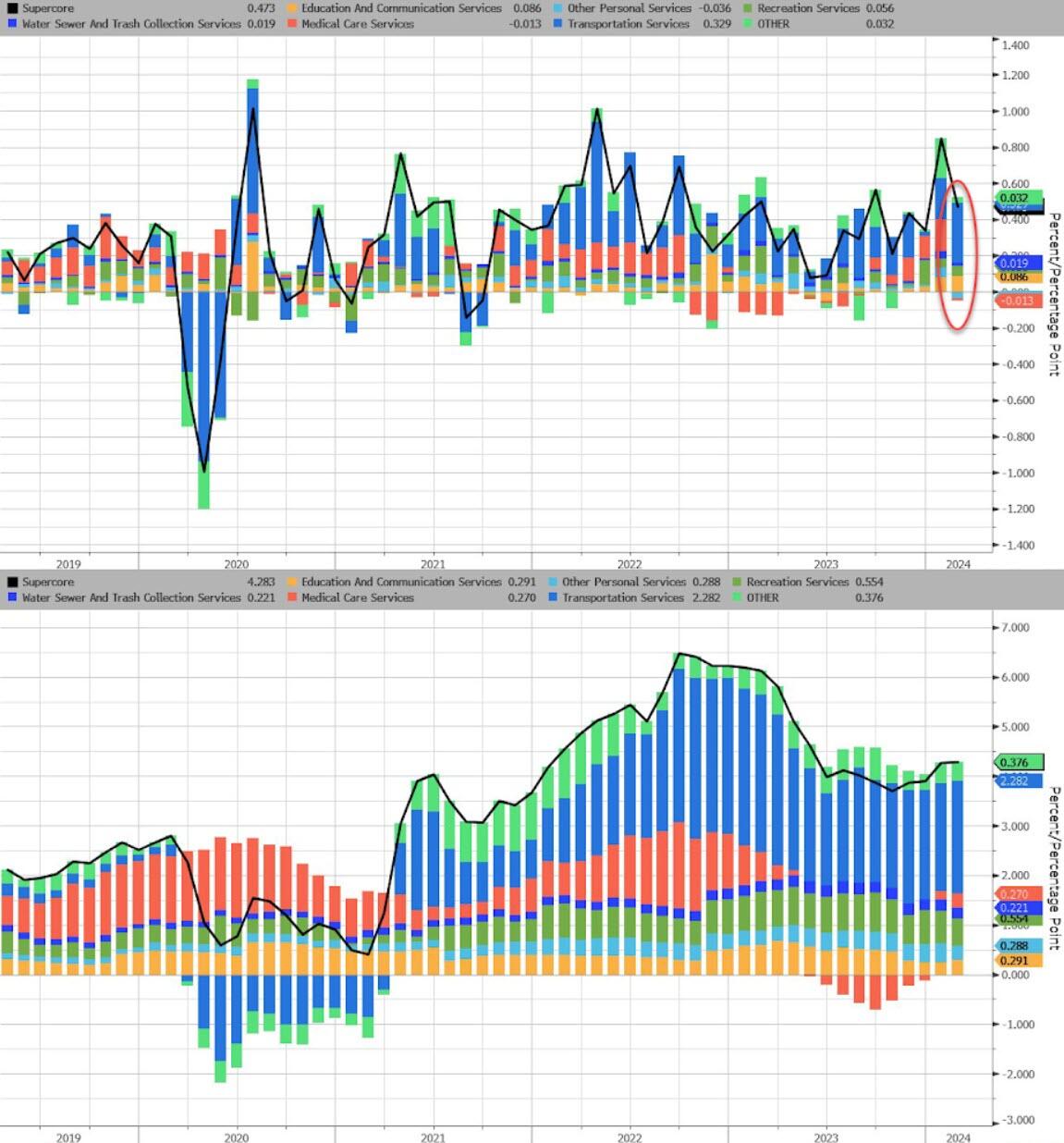

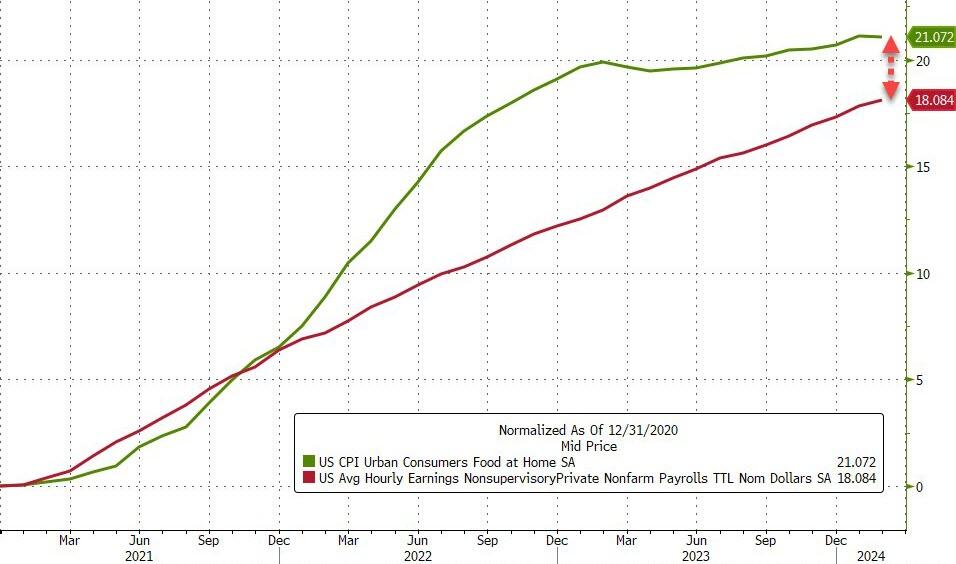

The painful inflation of the last three years has increased prices throughout the economy, distorting the signals that prices are supposed to convey to buyers and sellers. For example, the cost to own a median-price home today has doubled since January 2021, but it’s still the same house.

This phenomenon represents the monetization of housing, where a dwelling becomes a much better store of value than the currency, even if the real value of the house hasn’t improved.

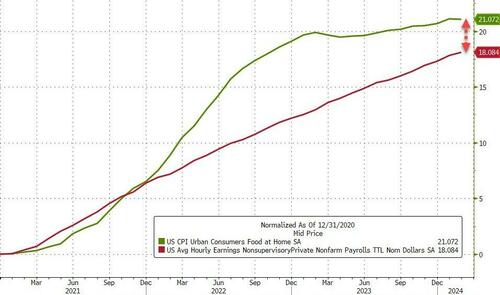

Likewise, Americans’ earnings have increased substantially over the last three years, but not in the most meaningful sense—that is, what they can buy. Instead, the opposite has happened, and today’s larger incomes buy less.

What would have been a decent salary in 2019 is no longer enough to even get by in many places, and it’s certainly not enough to ever fulfill the American dream of homeownership.

A family earning the median household income can afford a median-price home in only a handful of major metropolitan areas in the entire country. In many cities, the cost to own a median price home exceeds the take-home pay from the median household income. Even if you didn’t spend a dime on other necessities such as food, you still wouldn’t have enough for your mortgage payment.

It’s truly a condemnation of the status quo when even those with seemingly high incomes cannot afford a typical house.

Worse, as prices continue marching upward, people can save less, making it harder to accrue a sufficient down payment. Even by the time a family reaches their goal, home prices have increased again, and they’re back on the hamster wheel, trying to save for an even larger down payment.

Meanwhile, inflation is steadily, though silently, taxing away the real value of the family’s savings as they sit in the bank.

This has left countless Americans as perpetual renters, with almost an entire generation of young people giving up on having the standard of living that their parents had. An artificial chasm has been constructed between those who already own capital, like housing, and the remaining Americans who can only borrow such assets, as they do by renting.

Similarly, many of those struggling to afford sharply increased rents are going deeply into debt to keep a roof over their head while those who locked in a mortgage with a fixed interest rate before both home prices and interest rates exploded have shielded themselves from one of the largest drivers behind the cost-of-living increases of the last three years.

Many homeowners could not afford to buy their same home today. The monthly mortgage payment on a median-price home has doubled since January 2021. Thus, even if two families have identical incomes, the one that bought a home three years ago has a nearly insurmountable advantage over the other family trying to do so today.

The Fed’s monetary manipulations have financed trillions of dollars in federal budget deficits, but they’ve also created a permanent American underclass, something antithetical to the Founders’ vision for the country.

Class mobility is at the heart of the American dream, and the Fed has turned it into a nightmare.

I was not comforted when I saw that Biden claims he had no idea who issued an pro-trans Executive Order for a Trans Awareness Day on Easter Sunday. Hey man, you are The President and have no idea who issued Executive Orders????

Here is a photo of Joe Biden with “Doctor” Jill on Easter Sunday flanked by Fed Chair Jerome Powell and Jared Bernstein (whom I once debated in Washington DC).

Update: KJP confessed that it was Obama who created the Trans Day of Awareness back in 2009 (although strangly not enacted until this part Easter Sunday).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.