The elite class “economists” (aka, cheerleaders) are meeting at Jackson Hole, Wyoming this week. But while they are planning our future, the revision to the miserable Q2 Real GDP report came out this morning.

So, the second pass at measuring Real GDP produced a slightly better number (-0.6% vs -0.9%).

But the GDP PRICE index revision worsened from 8.7% to 8.9%. Look at REAL personal consumption (yellow line) as M2 Money growth slows.

Let’s see how things go at The Fed party at Jackson Hole, Wyoming. It is appropriate for The Fed to hold their party/meeting at Jackson Hole (Teton County) since it has the highest concentration of wealth per household than any other county in the nation.

At The Fed continues to tighten to fight inflation, pending home sales in July crashed and burned. That is, pending home sales fell -22.5% in July as M2 Money growth slowed

If I was still teaching at Ohio State or Chicago, I would ask the students if they see the relation between M2 Money growth and pending home sales.

US mortgage applications just hit the lowest levels in 22 years, January 2000 as The Federal Reserve continues monetary tightening to combat Bidenflation.

Mortgage applications decreased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 19, 2022. The Refinance Index decreased 3 percent from the previous week and was 83 percent lower than the same week one year ago.The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 21 percent lower than the same week one year ago.

MBA mortgage applications just declined to their lowest level in 22 years (January 2000) as The Fed has begun raising rates to fight inflation caused by 1) excessive monetary stimulus since late 2008, 2) Biden’s green energy policies driving up transportation costs, 3) distortionary Federal spending (e.g., Covid relief, infrastructure bills and now green energy/IRS spending by Biden/Pelosi/Schumer).

Here is the data summary for the latest MBA applications report.

Fed Chair Jerome Powell shrinking The Fed’s balance sheet.

Dear Mr. Fantasy, play us a tune, something to make us all happy (like hitting 2% inflation WITHOUT crashing the economy). Do anything take us out of this gloom (caused by The Fed, Biden’s energy policies and Federal spending). Sing a song, play guitar, Make it snappy. Or in the case of housing, make it crappy.

(Bloomberg) — Federal Reserve Bank of Richmond President Thomas Barkin said the central bank was resolved to curb red-hot inflation, even if that meant risking a US economic recession.

“We’re committed to returning inflation to our 2% target and we’ll do what it takes to get there,” Barkin said Friday during an event in Ocean City, Maryland. He said that this could be achieved without a “tremendous decline in activity” but acknowledged that there were risks.

“There’s a path to getting inflation under control but a recession could happen in the process,” he said.

The US central bank hiked interest rates by 75 basis points in July for the second straight month as policy makers tackle inflation that’s running near 40-year highs. Fed officials speaking in recent days have said more rate increases are needed, but they are still deciding how big to move at their next policy meeting.

St. Louis Fed President James Bullard, one of the most hawkish policy makers, on Thursday urged another 75 basis-point move while Kansas City’s Esther George struck a more cautious tone.

Well, The Fed (aka, Der Kommissars) let the monetary stimulus blow out of control since 2000.

With the 2001 recession, The Fed crashed the target rate (white line) causing home price growth (blue line) to soar. Then The Fed decided that the economy was overheated and cranked up their target rate. This sudden rise in The Fed’s target rate helped to slow/crash housing prices. Resulting in … a frantic decrease in the target rate (late 2007- late 2008) and the adoption of asset purchases of Treasury Notes/Bonds and Agency Mortgage-backed Securities in late 2008.

The Bernanke/Yellen “loose as a goose” policies from late 2008 to Feb 2018 created a total mess. Bernanke/Yellen raised the target rate only one before Trump was elected President, and 8 times AFTER Trump was elected. And Yellen’s Fed began to let the balance sheet shrink a bit before Covid struck in early 2020. And with Covid came another massive expansion of The Fed’s Balance Sheet WHICH HAS NOT YET BEEN WITHDRAWN (despite Fed talking heads saying it would be reduced).

Here we sit with The Fed NOW trying to extinguish inflation (yellow line) by raising their target rate (white line) but NOT shrinking the balance sheet (orange line).

Wonder why this is a horrible homeless problem in the US, particularly in California? While Stanford University has an excellent study of the causes of California’s homeless problem, there is another cause of homelessness … The Federal Reserve’s insane monetary policies since late 2008. The Case-Shiller National Home Price Index is 65% higher in May than during the calamitous home price bubble of 2005-2007, helping to exacerbate the homeless problem.

One of the many problems created by the reckless Bernanke/Yellen/Powell monetary policies is the M2 Money Velocity is near an all-time low making a return to “easy money policies” far more difficult.

I won’t post any photos of the homeless encampments in Los Angeles since it is very sad. But here is a photo of the Dunder-Mifflin paper company “office” on Saticoy Street. The point is that thanks to The Federal Reserve’s loose monetary policies, housing is unaffordable for millions of households forcing many to live on the streets.

Figure 2: Median Rent for a Two-Bedroom Apartment, California, 2022

And a point of trivia. The Office’s Charles Miner (played by the GREAT Idris Elba) was allegedly hired from Saticoy Steel. The Dunder-Mifflin paper company site was on Saticoy Street in sunny LA, not Scranton PA.

Good luck to The Federal Reserve in combating inflation without causing a recession.

Real estate investment trusts (REITs) are an interesting asset class, allowing investors to purchase shares in large-ticket assets like multi-family properties or shopping centers. But given the changing landscape due to online shopping (aka, the Amazon effect), Covid economic shutdowns, etc., REITs should be having a hard time. But aren’t. How come?

Covid economic shutdowns definitely took its toll on retail shopping centers, as an example. And you can see the plunge in the NAREIT All equity index in early 2020. But the NAREIT All-equity index rallied … until The Federal Reserve started tightening their loose monetary policy. Note that as the implied O/N rate rose (orange line), REIT shares declined.

But as the WIRP implied O/N rate settled (pink box), the NAREIT index began to climb again. It is clear that REITs, like other equities, benefit from Fed easing. But how long will The Fed continue tightening?

As of this morning, The Federal Reserve is anticipated to raise their O/N rate to 3.738% by March 22, 2023. Then begin lowering their target rate … again.

Sadly, REITs, like other equity investments such as the S&P 500 index, are sensitive to The Fed’s easing/tightening. Look for REITs to struggle as The Fed tightens, then rally as The Fed eases again.

Here is the (in)famous Hindenburg Omen. Notice how the Hindenburg Omen alarm bells (yellow and red dots) have been silenced by The Fed. But as The Fed tightens (at least until March ’22), we may see the Hindenburg Omen flashing again. Call it the Powellburg Omen.

The NCREIF property index had a decline in the Covid-outbreak era (early 2020) and you can see a slight slowdown in the NCREIF index as The Fed started tightening to fight inflation.

Today’s US industrial production and capacity utilization numbers showed a nice “steady as she goes” slow decline from previous months, though still positive at 3.90% YoY.

And it is difficult to argue that the US is in a recession when capacity utilization is at 80.27%.

Notice that industrial production growth falls below 0% during a recession and capacity utilization slumps. We are NOT there … yet.

However, M2 Money growth is shrinking awfully fast.

While the US is technically in default (two consecutive quarters of negative GDP growth), it doesn’t FEEL like a recession with 3.90% YoY industrial production growth and capacity utilization above 80%. During the Covid recession in early 2020, industrial production growth YoY had declined to -17.65% and capacity utilization shrank to 64.53%.

Speaking of a recession SIGNAL, the 10Y-2Y Treasury yield curve is SCREAMING impending recession.

The US Empire State Manufacturing Survey General Business Conditions, that is. It just crashed and burned (-31.3) in August, the lowest reading since The Great Covid Shutdown and before that The Great Recession.

The inverted US Treasury yield curve (10Y-2Y) is beginning to make sense.

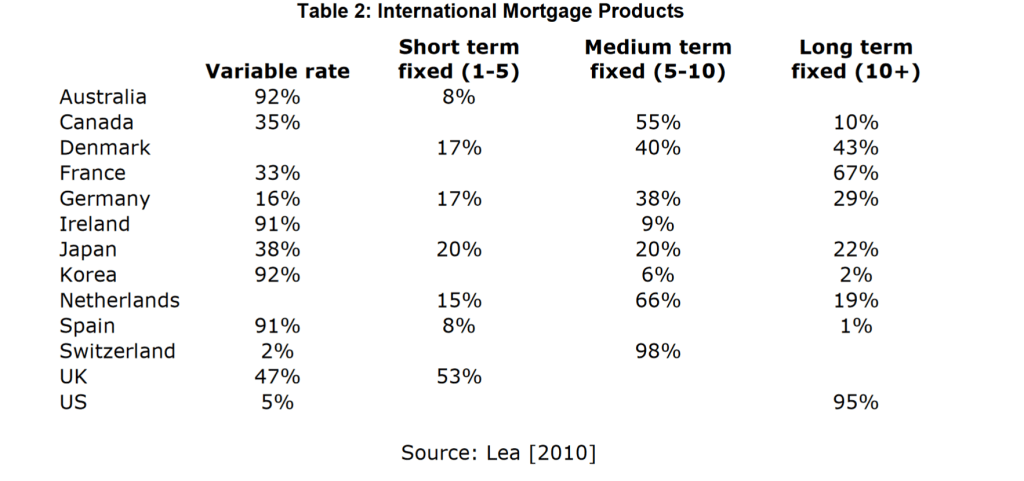

Mike Lea and I wrote a paper entitled “Do We Need The 30yr FRM (Fixed-rate Mortgage)”. We argue that millions of Americans would benefit from an adjustable-rate mortgage like the 5/1 ARM for a host of reasons.

One good reason for a 5/1 ARM is the fact that it 134 basis points less expensive than the 30yr fixed-rate mortgage.

Mortgage rates have risen dramatically with the expectation of Fed rate tightening (green line).

Yes, there is a “fear factor” built in the 30r FRM (“OMG! The mortgage market will collapse without the 30yr FRM!!!!) Hogwash. Or malarkey, as Joe Biden likes to say. The mortgage market actually see the US join the rest of the world in having adjustable-rate mortgage being the predominant mortgage product.

US ARM share peaked at 10.8% in June 2022 before retreating to 7.4% as the 30yr mortgage rate retreated.

Fannie Mae’s Home Purchase Sentiment index has declined from 81.7 shortly after Biden was sworn-in as President to a meager 62.8 in July 2022.

Of course, mortgage rates have risen quite rapidly and home price growth remains elevated as The Fed still has not trimmed its balance sheet as promised.

You must be logged in to post a comment.