The US Empire State Manufacturing Survey General Business Conditions, that is. It just crashed and burned (-31.3) in August, the lowest reading since The Great Covid Shutdown and before that The Great Recession.

The inverted US Treasury yield curve (10Y-2Y) is beginning to make sense.

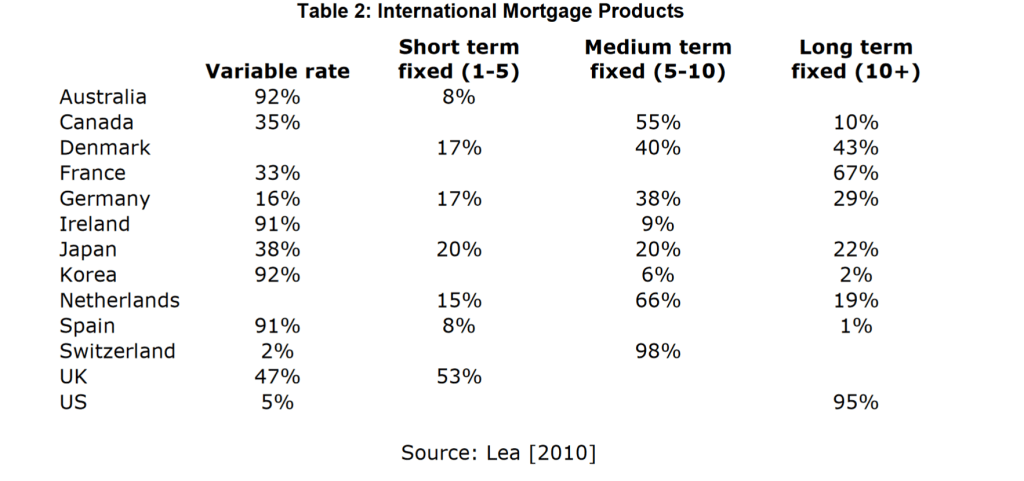

Mike Lea and I wrote a paper entitled “Do We Need The 30yr FRM (Fixed-rate Mortgage)”. We argue that millions of Americans would benefit from an adjustable-rate mortgage like the 5/1 ARM for a host of reasons.

One good reason for a 5/1 ARM is the fact that it 134 basis points less expensive than the 30yr fixed-rate mortgage.

Mortgage rates have risen dramatically with the expectation of Fed rate tightening (green line).

Yes, there is a “fear factor” built in the 30r FRM (“OMG! The mortgage market will collapse without the 30yr FRM!!!!) Hogwash. Or malarkey, as Joe Biden likes to say. The mortgage market actually see the US join the rest of the world in having adjustable-rate mortgage being the predominant mortgage product.

US ARM share peaked at 10.8% in June 2022 before retreating to 7.4% as the 30yr mortgage rate retreated.

Fannie Mae’s Home Purchase Sentiment index has declined from 81.7 shortly after Biden was sworn-in as President to a meager 62.8 in July 2022.

Of course, mortgage rates have risen quite rapidly and home price growth remains elevated as The Fed still has not trimmed its balance sheet as promised.

The US housing market is simply unaffordable for millions of Americans. To illustrate the problem, here is a chart of the Case-Shiller National home price index less CPI YoY graphed against Average Hourly Wages less CPI YoY.

The gap between the REAL national home price index YoY and REAL US average hourly earnings YoY is near the largest since 1988. Inflation is making matters far worse since REAL average hourly earnings growth continues to decline.

The only thing positive to say is that REAL home price growth YoY is lower now than at the peak of the 2005 home price bubble that burst catastrophically.

Another “positive” is that the REAL 30-year mortgage rate has fallen to -3.23%. At the peak of the house price bubble in June 2005, the REAL 30-year mortgage rate was +2.58%. THAT is one big difference between the pre-2008 recession and today’s impending recession.

Here is your weekend update on Treasury and Mortgage markets.

The current US Treasury 10Y-2Y yield curve just slipped further into reversion at -40.299 basis points, screaming impending recession. Oddly, The Federal Reserve has been leaving its balance sheet of Agency Mortgage-backed Securities (MBS) in tact (green line).

On the mortgage front, Bankrate’s 30-year mortgage rate index rose to 5.60% while the affordability-friendly 5/1 Adjustable Rate Mortgage (ARM) rate rose to 4.21%.

Currently, a 5/1 ARM borrower can save 139 basis points over the traditional 30-year mortgage rate.

After mortgage rates topped 6%, they settled back down with the global economic slowdown, but are on the rise again.

Bankrate’s 30-year mortgage rate index rose to 5.57% after rising above 6% in June 2022. Mortgage rates are up 92% under the team of Biden and Fed Chair Powell as The Fed tries to extinguish the inflation fire cause by 1) excessive Fed stimulus, 2) Biden’s anti-fossil fuel policies and 3) Biden/Congress’ reckless spending.

The Fed still has not shrunk its balance sheet yet and home price growth is still soaring.

The US Treasury 10Y-2Y yield curve inversion just worsened to -38.503, the most inverted since 2000.

Over the longer-term, the US Treasury 10Y-2Y yield curve is the most inverted since 2000. Remember, the 10Y-2Y yield curve inverts prior to a recession.

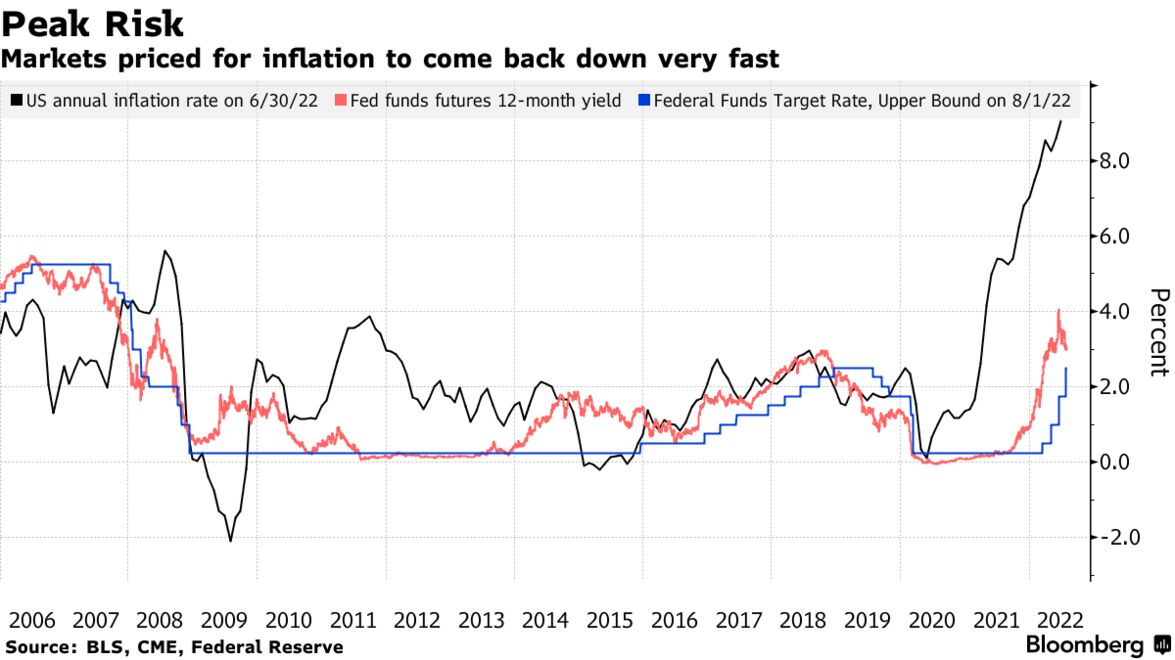

The US economy may need to undergo a deeper and longer recession than investors currently anticipate before inflation can be brought under control, according to Zoltan Pozsar of Credit Suisse Group AG.

Markets expect the surge in consumer prices will soon peak and central banks will become less hawkish, but there’s a high risk that global cost pressures will remain elevated, Pozsar, global head of short-term interest-rate strategy at Credit Suisse in New York, wrote in a client note.

The world is being wracked by an economic war that’s undermining the deflationary relationships that have prevailed in recent decades where Russia and China supplied cheap goods and services to more developed nations such as the US and those in Europe, he said.

“War is inflationary,” Pozsar wrote. “Think of the economic war as a fight between the consumer-driven West, where the level of demand has been maximized, and the production-driven East, where the level of supply has been maximized to serve the needs of the West.” That pattern held “until East-West relations soured, and supply snapped back,” he said.

The result is that inflation is now a structural problem, rather than a cyclical one. Supply disruptions have arisen from the changes in Russia and China, along with tighter labor markets due to immigration restrictions and a reduction in mobility caused by the coronavirus pandemic, Pozsar said.

There’s now a risk the Federal Reserve under Chair Jerome Powell has to raise interest rates to 5% or 6% and keep them there to create a substantial and sustained reduction of aggregate demand to match the tighter supply profile, he said.

‘More Misguided’

Connect the dots on the biggest economic issues.Connect the dots on the biggest economic issues.Connect the dots on the biggest economic issues.

Dive into the risks driving markets, spending and saving with The Everything Risk by Ed Harrison.Dive into the risks driving markets, spending and saving with The Everything Risk by Ed Harrison.Dive into the risks driving markets, spending and saving with The Everything Risk by Ed Harrison.

Sign up to this newsletter

Pozsar’s warning that inflation will stay elevated puts him at odds with the Treasury market, which rallied last month as investors switched their focus to recession risks from inflation concern. While an economic slowdown typically weighs on consumer prices, the latest annual US inflation reading of 9.1% for June remains far above the Fed’s 2% goal, although the price surge is forecast to slow for the first time in three months to 8.8% in July according to a Bloomberg poll of economists.

The bond market is more misguided now than at any other time this year as traders wager the US central bank will start cutting rates in early 2023, Bloomberg Economics’ chief US economist Anna Wong and her colleagues said this week. Money markets are wagering on almost one percentage point of hikes by year-end followed by a quarter-point cut by June.

“Interest rates may be kept high for a while to ensure that rate cuts won’t cause an economic rebound (an ‘L’ and not a ‘V’), which might trigger a renewed bout of inflation,” Pozsar wrote in his note. “The risks are such that Powell will try his very best to curb inflation, even at the cost of a ‘depression’ and not getting reappointed.”

Speaking of “recession,” the US Treasury 10Y-2Y yield curve has inverted even further to -31.69 BPS.

After breaking the 6% barrier back in June 2022, Bankrate’s 30-year mortgage rate has backed-off to 5.28% despite Federal Reserve rate hikes.

The reason for the decline in the US Treasury 10-year is, amongst other things, a global economic slowdown (partly due to the US and Europe “going green” and cutting the supply of fossil fuel-based energy). Instead of “The Great Reset,” I call it “The Great Economic Suicide.” The 10-year US Treasury yield and Bankrate’s 30-year mortgage rate are declining with declining global GDP.

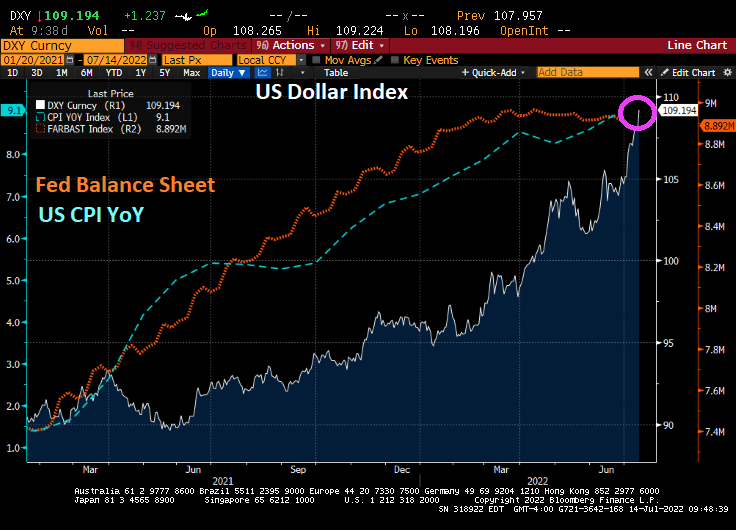

Bear in mind that a strong dollar is a two-edged sword. The US Dollar Index has risen 16% year-over-year, presenting a big hurdle for US firms with business overseas.

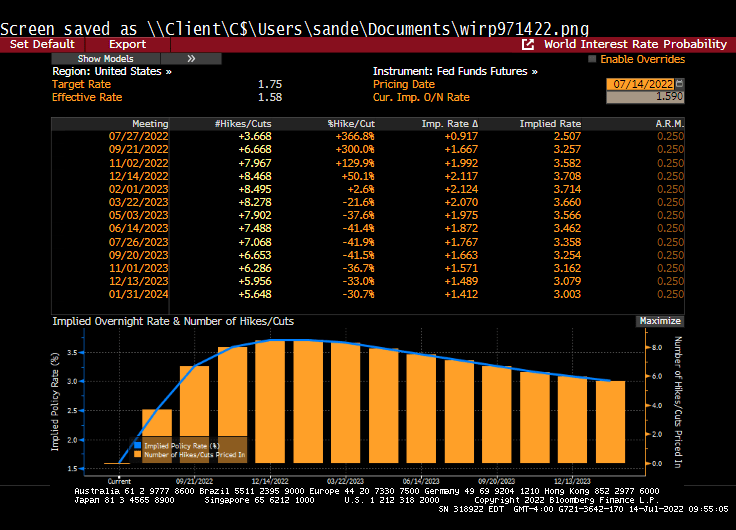

That strength of the greenback will rise until the Fed makes a dovish policy pivot.

And that pivot is forecast to occur at the Feb ’23 FOMC meeting.

You must be logged in to post a comment.