Official estimates from the Congressional Budget Office (CBO) show that, since January 2021, legislation signed by President Biden has set in motion a record $3.37 trillion in new spending. And for all that spending, we get a pathetic 1.1% QoQ growth rate?

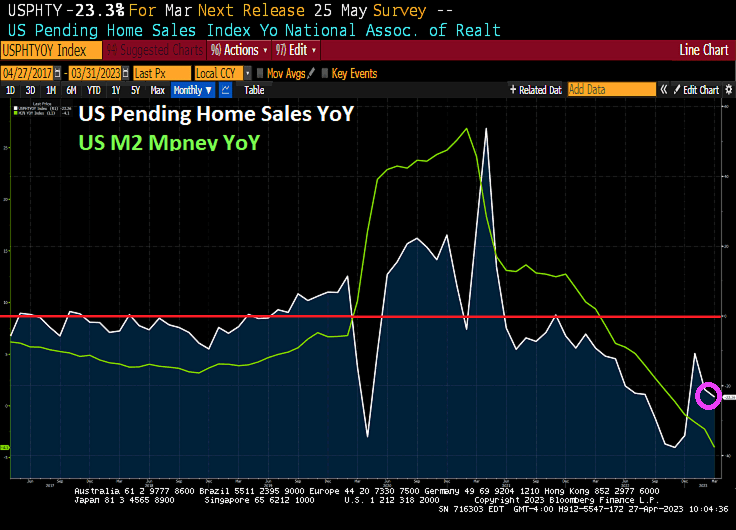

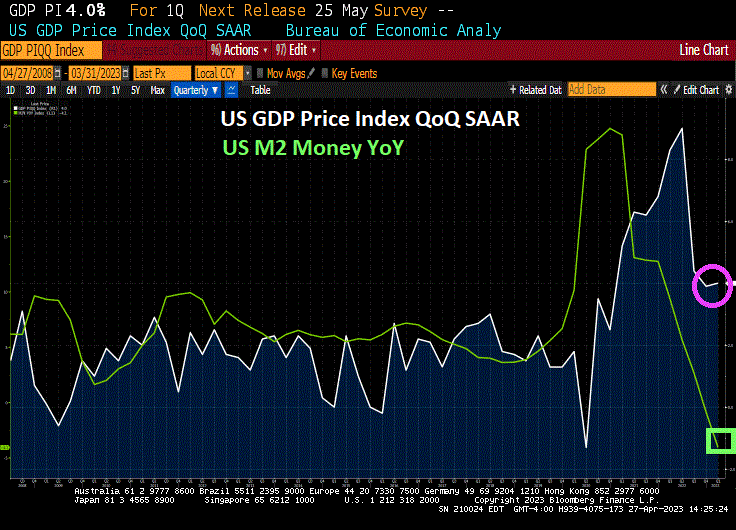

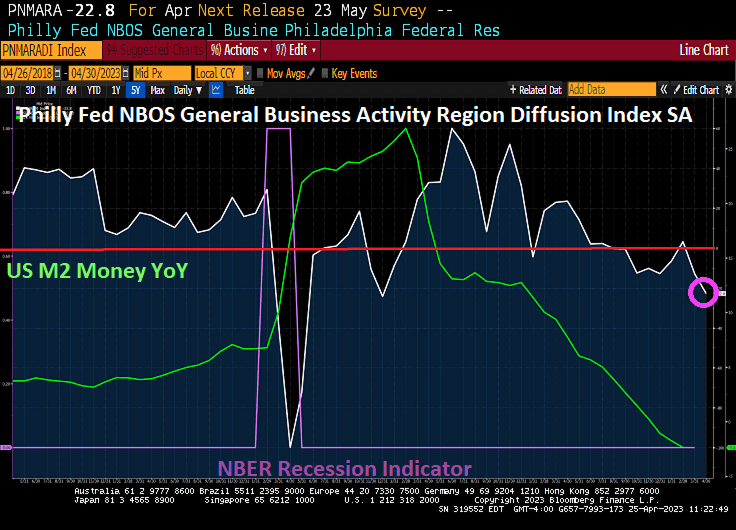

Inflation continues to be 4% QoQ despite M2 Money growth collapsing.

Gross private domestic investment crashed by -12.5% QoQ.

This is Biden’s idea of a strong economy? His lame campaign slogan is “Let’s finish the job!” Please don’t Joe!

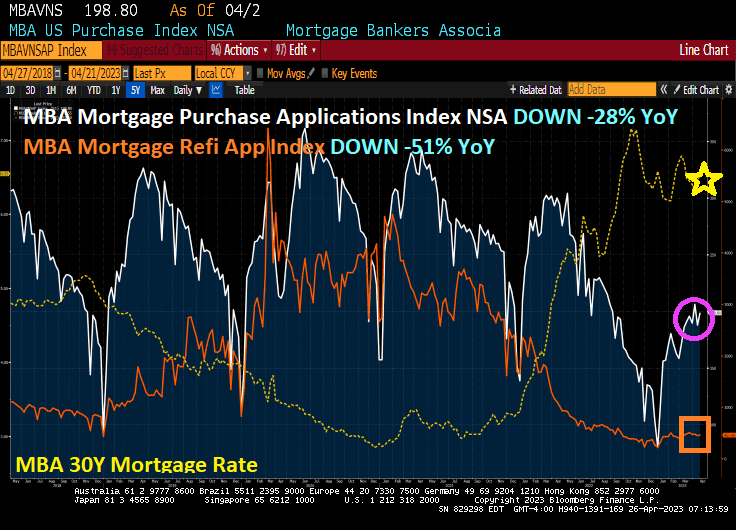

Mortgage applications increased 3.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 21, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 3.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 5 percent compared with the previous week. The Refinance Index increased 2 percent from the previous week and was 51 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 5 percent from one week earlier. The unadjusted Purchase Index increased 6 percent compared with the previous week and was 28 percent lower than the same week one year ago.

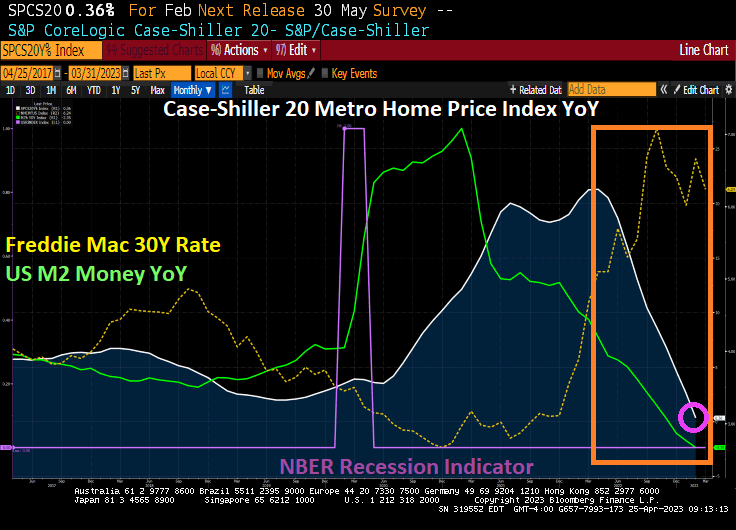

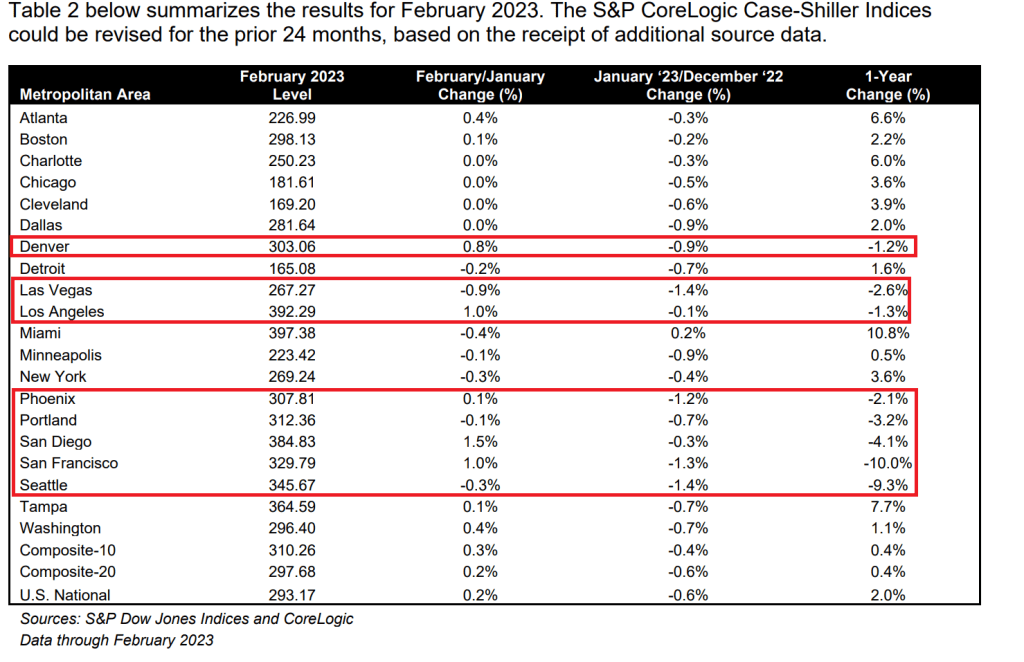

Drifting into darkness, we have the West getting battered with my old hometown of San Francisco leading the pack at -10% YoY with Seattle down -9.3% YoY.

You know things are bad out west when Cleveland, Detroit and Chicago are gaining ground in prices. And Miami was up 10.8% YoY.

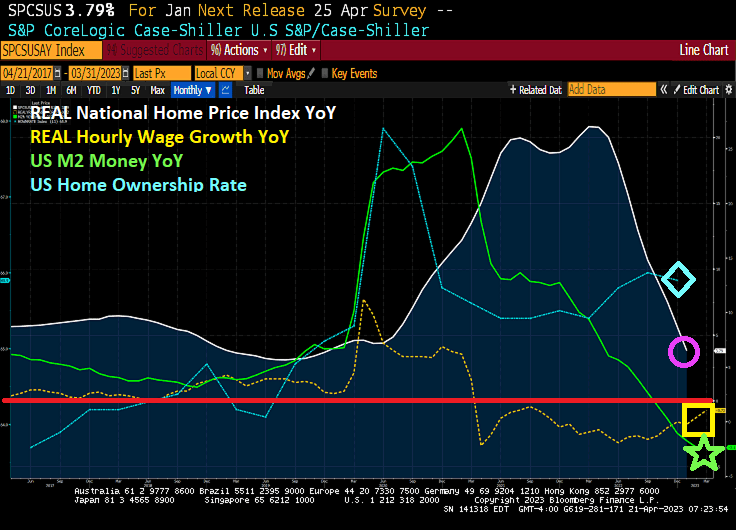

It has been a tough road for the US economy since Covid and Biden’s Reign of Error. For the first time since July 2020 under President Trump, we have finally seen average hourly earnings growth YoY exceed average home price growth YoY.

In REAL terms (after substracting out headline inflation), we see that US housing market is still plagued by 24 straight months of negative wage growth with REAL wage growth still being lower than REAL home price growth.

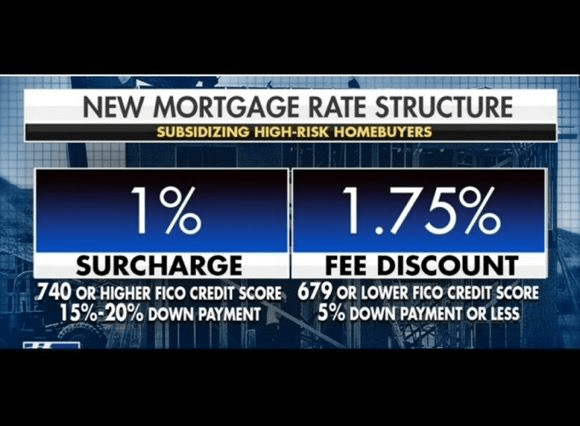

Then we have Biden’s Marxist mortgage model, making those who who saved and showed care in managing their credit score given money to those who didn’t save and are terrible at financial management. Just like taxpayers trusting DC bureaucrats to carefully spend their money.

This is life under Joe Biden. Record sovereign risk, record high debt, near 40-year highs in inflation, a hot war in Ukraine with Russia, failure of DOJ/FBI to do anything about the content of Hunter Biden’s laptop, repression of free speech, soaring crime, out of control borders. Should I keep going? It is a disastrous mess created by Obama/Biden and their creepy allies.

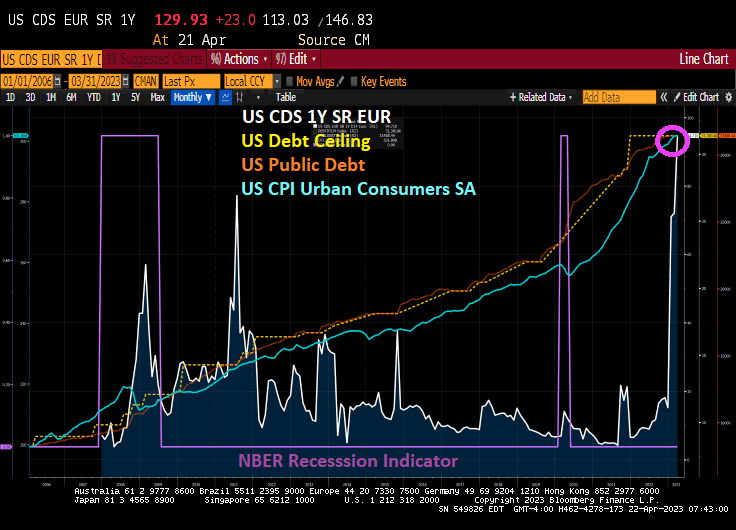

US sovereign risk just hit 130, the highest since CDS was recorded. This alligns with Biden/Congress massive borrow and spend policies where Federal debt has soared to it highest level in history. Inflation, while cooling, remains high.

On the housing front, REAL national home price growth is negative which makes sense since REAL average hourly wage growth has been negative for the last 24 months.

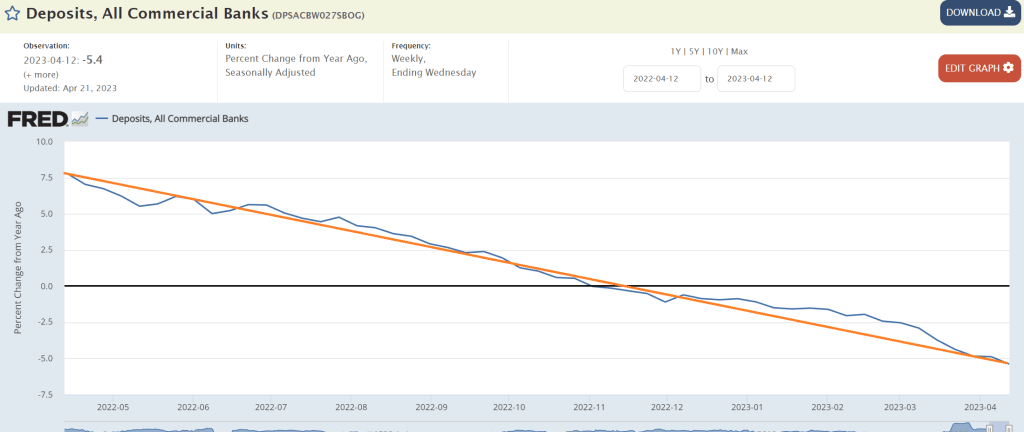

And just over the past year, commericial bank deposits are falling like a paralyzed falcon.

Biden and Obama’s chief hack in the White House, Susan Rice, are burning down the house.

Former Federal Reserve Chair and current Treaury Secretary Janet “The Evil Hobbit” Yellen has created numerous catestrophic messes thanks to Fed policy errors, both at The Fed and now as Treasury Secretary.

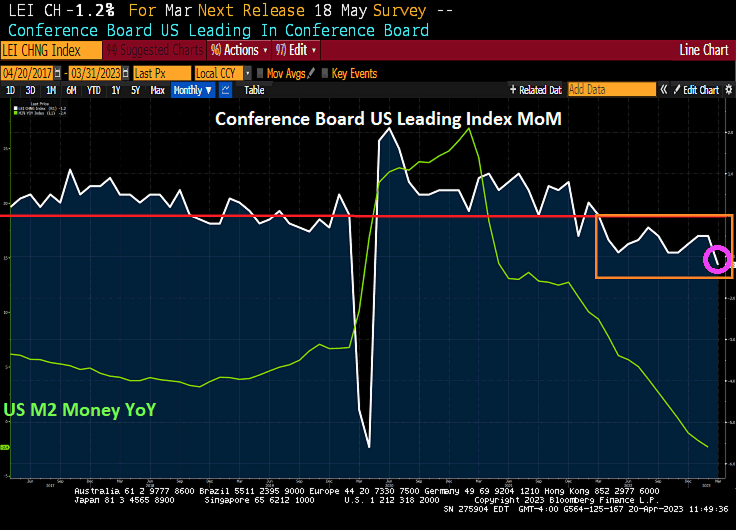

For example, the massive almost hysterical overreaction of The Fed under Powell (following Yellen’s Reign of Error) to the Covid economic shutdowns resulted in a massive surge in M2 Money growth [green line].

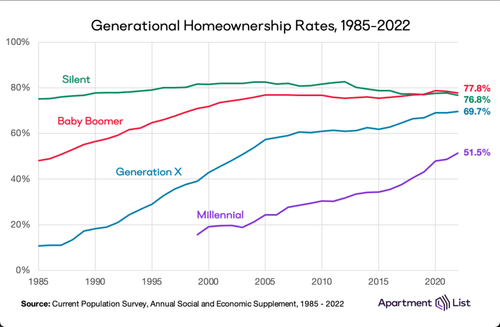

The result? REAL US housing prices soared while REAL averge hourly wage growth was negative for 24 straight months. THAT is the Fed error induced housing policy blunder. But it did increase the US homeownership rate (blue line).

Under the new rules, high-credit buyers with scores ranging from 680 to above 780 will see a spike in their mortgage costs – with applicants who place 15% to 20% down payment experiencing the biggest increase in fees.

“This was a blatant and significant cut of fees for their highest-risk borrowers and a clear increase in much better credit quality buyers – which just clarified to the world that this move was a pretty significant cross-subsidy pricing change,” added Stevens, who is also the former CEO of the Mortgage Bankers Association.

Jeder nach seinen Fähigkeiten, jedem nach seinen Bedürfnissen (German for “From each according to his ability, to each according to his needs” – Karl Marx.

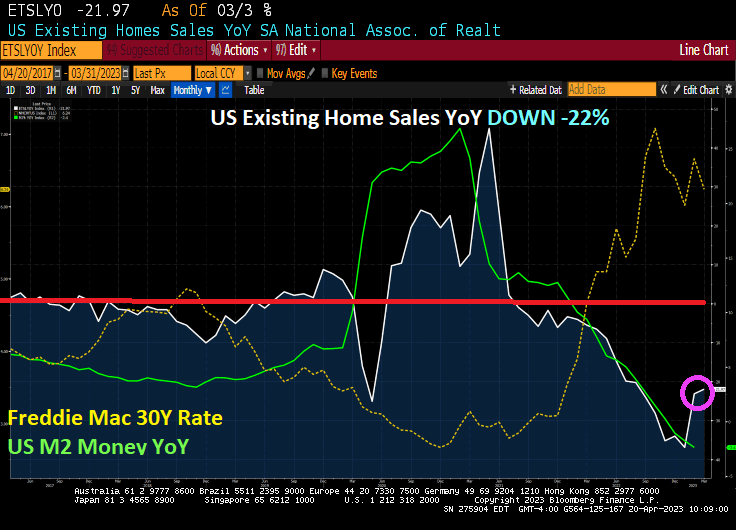

According to the National Association of Realtors, existing home sales fell -2.4% in March from February. And fell -21.97% since the same time last year (YoY).

And the median price of existing home sales fell -0.9% in March, the first negative growth since 2012.

You must be logged in to post a comment.