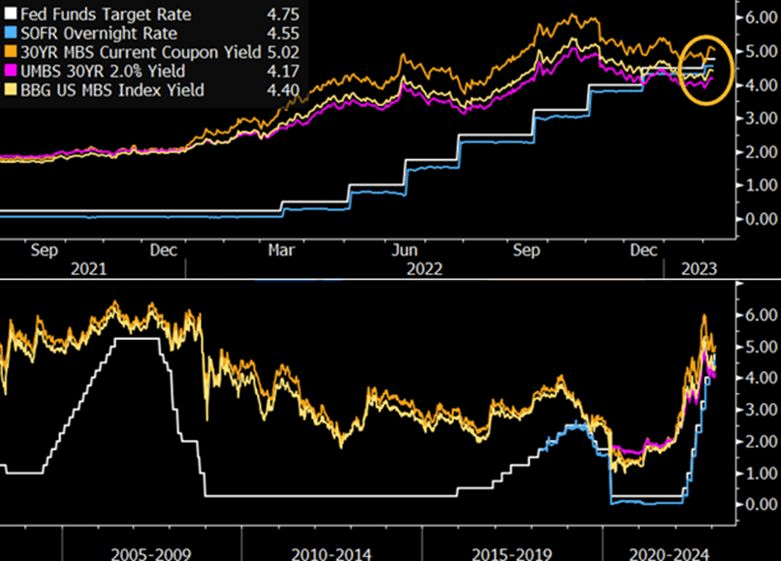

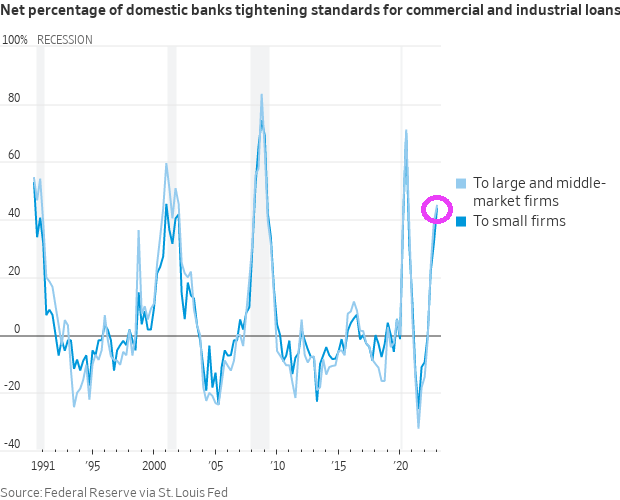

The most recent tightening by the Federal Reserve has pushed the federal funds target rate above mortgage-backed securities yields for the first time in history. Though this poses clear challenges of carry for MBS holders, selective investments in specified pool and collateralized mortgage obligations (CMOs) could provide incremental returns.

Inflation started under Biden, but the massive expansion in money supply (M2) begin with Covid in 2020.

Once this latest spending splurge kicks in, we will see rising inflation again. After all, Biden and Congress have gotten the taste for massive spending bills (like vampires) and spending likely won’t slow down.

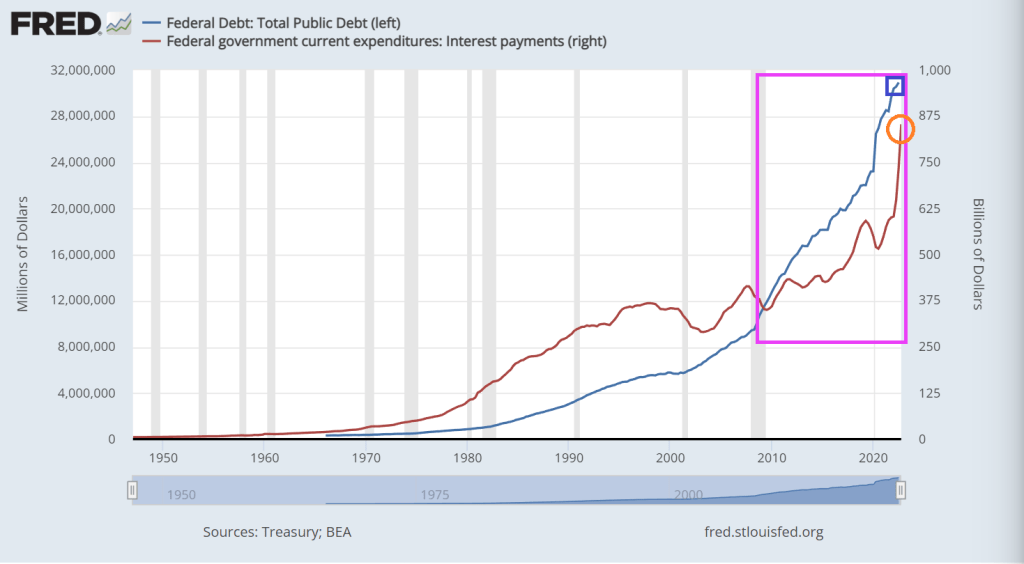

Nothing has been the same since Nancy Pelosi (CA-D) became Speaker of the House in January 2007. In fact, US public debt was at $8.68 trillion when she was handed the gavel and US public debt now sits at $31.55 trillion. That is a whopping 264% increase in the nation’s debt under free-spending SanFranNan. To Pelosi, there is no such thing as too much debt.

To be fair, Pelosi had plenty of help. We had Barack Obama and Joe Biden assume the Presidency in 2009 and in between we had RINOs (Republicans in name only) John Boenher and Paul Ryan as House speakers. In the Senate, the US has had Harry Reid (NV-D), Chuck Schumer (NY-D) and breifly Mitch McConnell (KY-R) as majority leaders. Of course, he had Donald Trump as President for 4 years then a return to the Obama-Biden Presidency with Old Joe as President for the past 2 years.

This chart show how deranged Congress and the Administration became since 2007. On October 3, 2008, President George W. Bush signed the $700 billion Emergency Economic Stabilization Act (EESA) of 2008 after Treasury Secretary Henry Paulson asked Congress to approve a bailout to buy mortgage-backed securities that were in danger of defaulting.

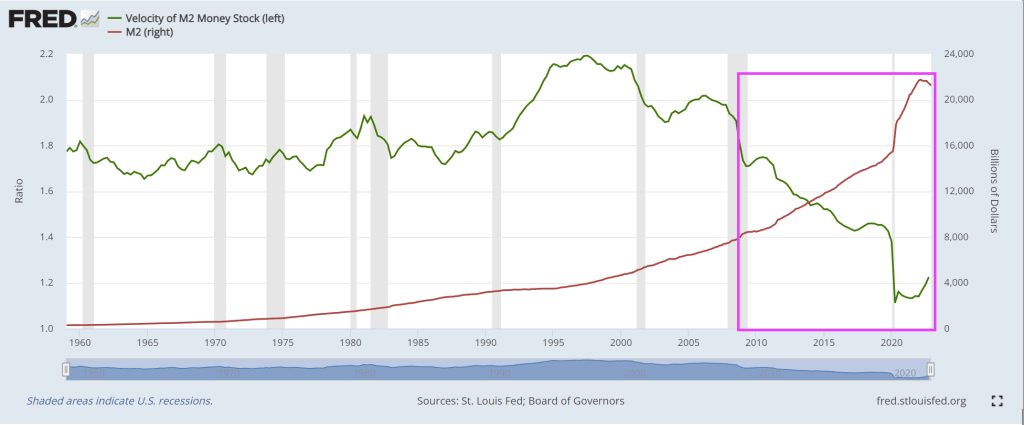

Since 2007, the US has expereienced a housing bubble burst and ensuing financial crisis (2008/2009), then a Covid economic shutdown in 2020 requiring (in the mind of Statists) massive Federal spending in the form of Covid Relief (aka, the American Rescue Plan) for $1.9 TRILLION, then Infrastructure Spending bill for $1 TRILLION, the Inflation Reduction Act (really a green energy spending bill dressed up as an inflation reduction measure) and the infamous pork-laden Omnibus bill. All this Federal spending has driven up M2 Money by 200% since Pelosi first became House speaker.

Look at the chart of M2 Money Velocity (GDP/M2 Money) since Pelosi became House Speaker. It has collapsed.

Pelosi is also notable for her “You have to pass the bill to see what’s in it” speech on the Affordable Care Act and childishly tearing up on camera a copy of Donald Trump’s State of the Union address.

Meanwhile, the US has $181.5 Trillion in UNFUNDED LIABILITIES that will require MORE debt to be issue. Social Security unfunded liability is now $22.46 trillion and Medicare unfunded liability is up to $35 trillion. But if you dare mention “reform” to these massive entitlement boondoggles, President Biden and Senate Majority Leader Chuck Schumer will say “Republicans want to take away your Social Security!” That isn’t what Rick Scott (FL-R) said.

Unfunded liabilities per citizen is now $542,457. I propose that all illegal immigrants crossing the Mexican border (or Canadian border) per forced to pay their share of unfunded liabilities as an entry fee..

While Congress debates cutting spending (Hint: Childish Biden and Schumer said no to any cuts to spending), the US Debt Star gets closer to completion.

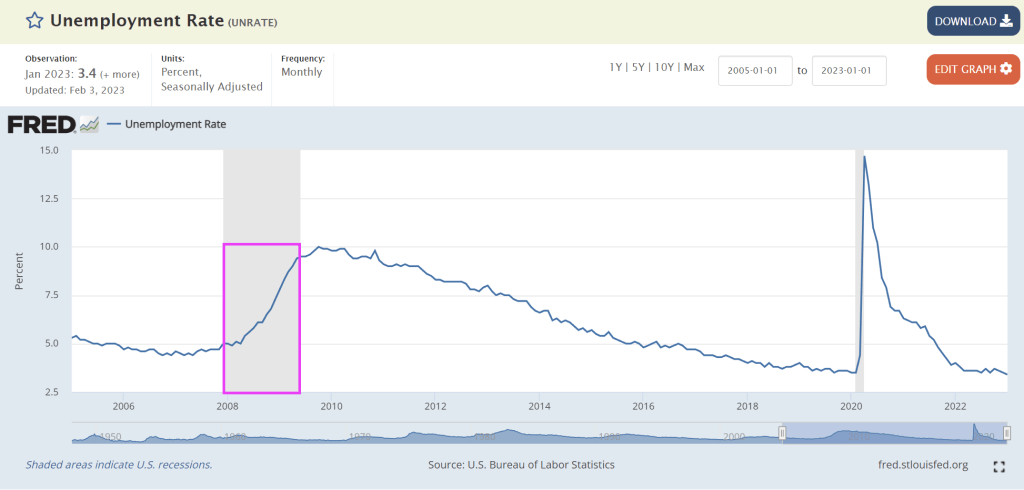

Biden’s State of the Union address saw him bragging about his record job creation (actually, it was the private sector, not Biden than created jobs) and historic unemployment rate. What Biden didn’t mention (along with not discussing the porous Mexican border with fentanyl pouring across or why he failed to shoot down a Chinese spy balloon until after it has passed over numerous military reservation) is that the unemployment rate always hit a low point just prior to a recession.

So, here we sit at 3.4% unemployment. But we also see the US Treasury yield curves (10Y-3M and 10Y-2Y) remaining deeply inverted.

The US Treasury 10-year yield is up 5.5 basis points today.

And Bankrate’s 30-year mortgage survey rate is up slightly today.

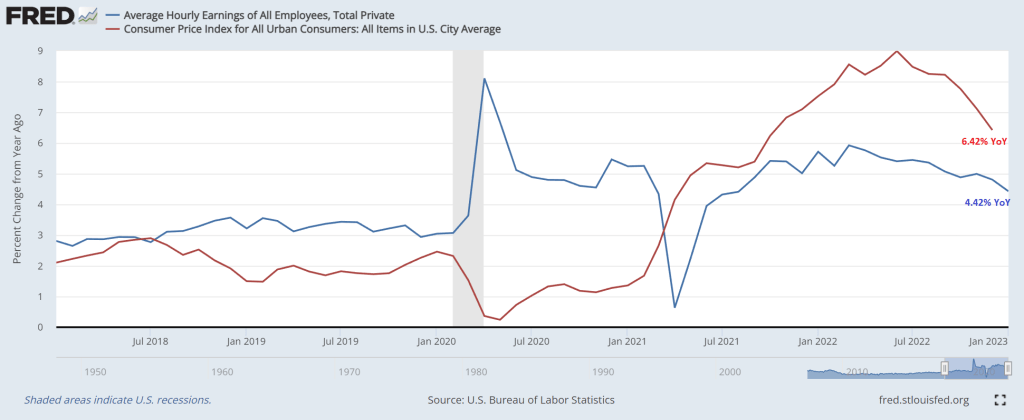

The one statement that Biden made in his State of the Union Address that was factually accurate was that inflation is coming down. Of course, he then blew it by saying he inherited inflation from Trump which was not true. Headline inflation (CPI YoY) was only 1.4% when Biden was sworn-in as President and rose to 9.1% YoY by June 2021 before finally starting to decline.

But despite the cooling of inflation (and M2 Money growth), The Fed seems hell bent on increasing their target rate, now forecast by Fed Funds Futures to peak in July 2023 at 5.123% before pivoting.

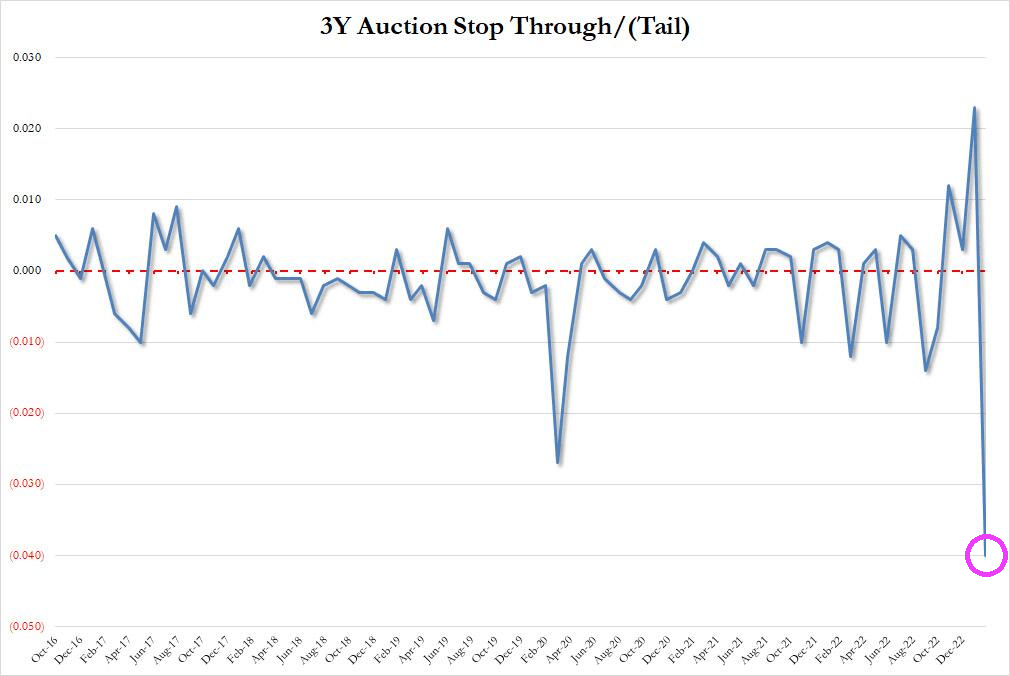

After Jerome Powell raved about the strong US labor market and oddly ignored the staggering crowding-out of US interest payments on its massive debt, the US Treasury’s 3-year debt auction was … a Hinderburg moment.

First, the high yield at today’s auction of 3-year Treasury notes was 4.073%. This occured as the allotment to brokers and dealers collapsed along with M2 Money growth YoY.

Then we have this horrible chart of the 3Y auction stop through, crashing into uncharted waters. A stop-through indicates when the highest yield the Treasury sold in the auction is below the highest yield expected when the auction began – the “when issued” level.

“The U.S. economy added 517,000 jobs in January, more than doubling Wall Street expectations and turning up its nose at prognosticators of an imminent recession. The unemployment rate dropped to 3.4 percent, the lowest level since 1969. Analysts were expecting it to move in the opposite direction, ticking up to 3.6 percent.”

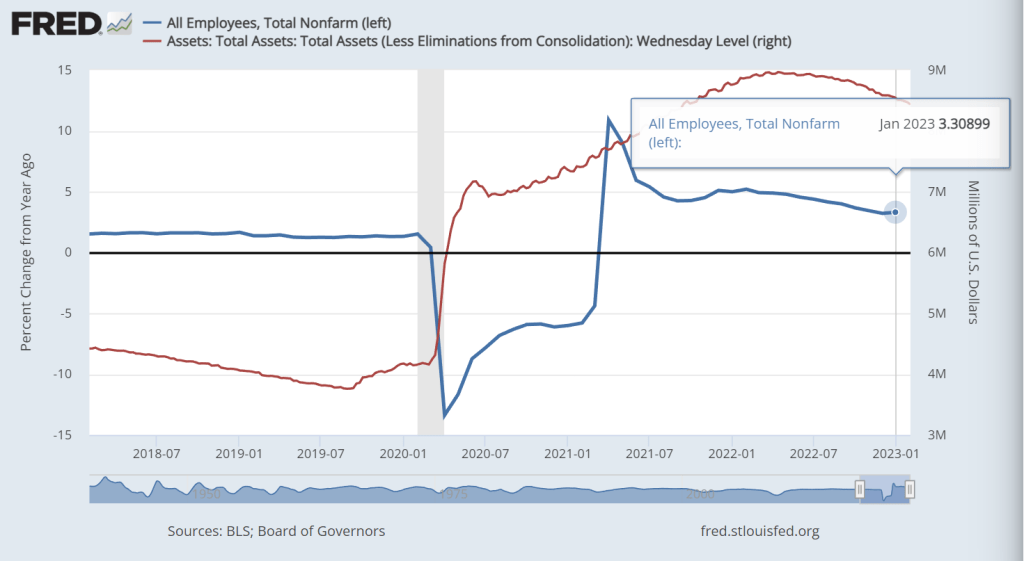

Yes, I was expecting U-3 unemployment to increase to 3.6% as well. What happened? Seasonal adjustments (BLS doens’t provide non-seasonally adjusted data). But the shocking headline (mostly due to seasonal adjustements) was not as surprising if we consider that jobs added in January grew at 3.309% year-over-year. Well, THAT isn’t all that surprising. Particularly since The Fed is slow walking its shrinking of The Fed balance sheet.

And with over 100 MILLION not in the labor force (apparently, the US labor force never really recovered from the Wuhan China virus), the U-3 unemployment rate touted by the media is misleading.

Bear in mind that employment is a LAGGING indicator. For example, the unemployment rate was 4.7% in November 2007 just prior to the beginning of the 2008-2009 Great Recession. So Biden’s bragging about the lowest unemployment rate since 1969 is meaningless in predicting recessions.

So, the January jobs report isn’t as surprising and strong as talking heads screamed about. I wish BLS would release non-seasonally adjusted (raw) data. But since we have a dysfunctional Federal government, I am not holding my breath.

And I wouldn’t consider averrage hourly earnings growth YoY of 4.42% when headline US inflation is 6.42% particularly brag worthy.

Of course, Biden lied about inheriting inflation from Trump. Inflation was 1.28% YoY in December 2020 just before Biden was sworn-in as President. Then again, Biden lies about everything. At least he just refused to comment on the Chinese Spy Balloons.

President Biden had better give his State of the Union Address before the economy worsens any more.

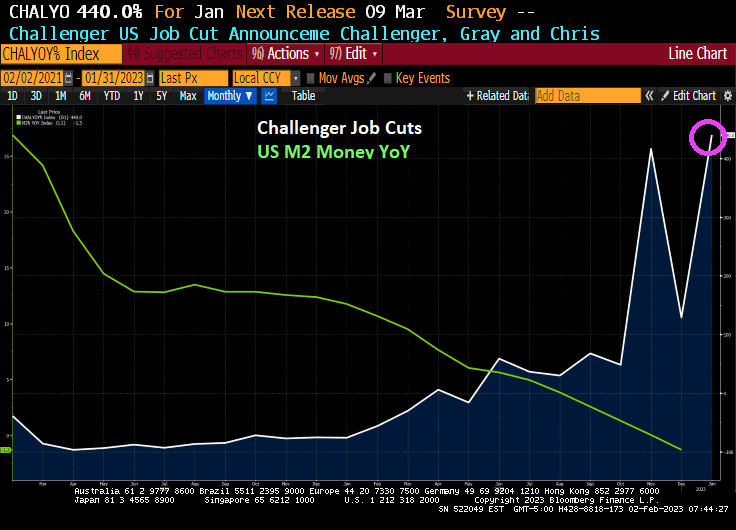

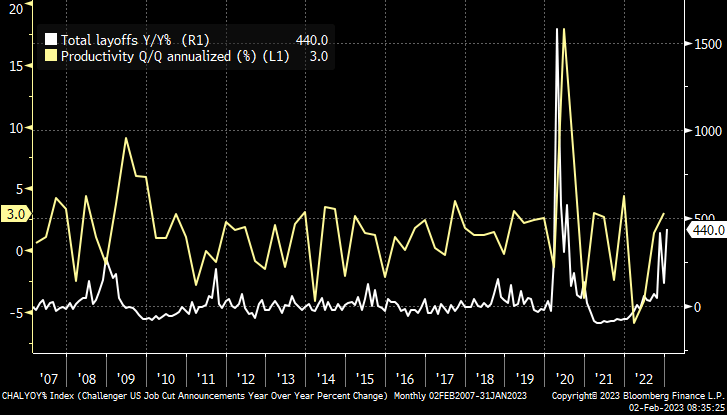

In January, the Challenger, Gray and Christmas jobs cuts index was a doozy. Jobs cuts rose 440%. This is happening as The Federal Reserve keeps its feet on the monetary brake pedal.

The Challenger report shows a big jump of 135.8 percent in layoff intentions to 102,943 in January, up from 43,651 in December and 440.0 percent higher than the 19,064 in January 2022. Many of the job cuts are in the tech sector, but job cuts are now spreading across the economy as a recession looms.

This morning, the US Treasury 10-year yield is down only -3.5 basis points, but it is Europe where the action is. UK is down -16.2 basis points and Italy is down -14.8 bps. UPDATE: US 10Y yield down -5.3 BPS, Italy 10Y down -29 bps.

Today’s GDP report from the BEA reminds me of the Peggy Lee song “Is That All There Is?” Between the massive Fed monetary stimulus since late 2008 (and particularly since Covid in 2020) and all the Federal spending (Covid relief, Inflation reduction, Omnipork spending bill, etc.), US real GDP rose by only 2.9% in Q4 from Q3.

But signs of slowing underlying demand mounted as the steepest interest-rate hikes in decades threaten growth this year.

Gross domestic product increased at a 2.9% annualized rate in final three months of 2022 after a 3.2% gain in the third quarter, the Commerce Department’s initial estimate showed Thursday.

Personal consumption, the biggest part of the economy, climbed at a below-forecast 2.1% pace (forecast was for 2.9%). Again,

The report also showed some signs of stress for American consumers whose wages have failed to keep up with inflation and continued to encourage them to draw down savings accumulated from government pandemic-relief programs. The burden of elevated prices and higher borrowing costs is mounting, pointing to a tenuous outlook for the economy.

A key gauge of underlying demand that strips out the trade and inventories components — inflation-adjusted final sales to domestic purchasers — rose an annualized 0.8% in the fourth quarter after a 1.5% gain.

Core PCE growth grew at 3.9%, but is slowing already as M2 Money growth dies.

Stock-index futures and Treasury yields remained higher and the dollar was little changed after the GDP report and better-than-expected weekly jobless claims. Applications for unemployment insurance dropped to 186,000 last week, the lowest since April.

Recent data show cracks are developing more broadly. Retail and motor vehicle sales data showed households are starting to retrench, the housing market continues to weaken and some businesses are reconsidering capital spending plans.

As the Federal Reserve continues to hike interest rates to ensure inflation is extinguished, housing and manufacturing have deteriorated quickly while industries including banking and technology are carrying out mass layoffs.

The GDP report showed the personal consumption expenditures price index, a key inflation metric for the Fed, rose at an annualized 3.2% rate in the fourth quarter, down from a 4.3% pace in the prior three months. The core index that excludes food and energy climbed at a 3.9% rate compared with 4.7% paces in the prior two quarters. Monthly data for December will be released Friday.

The moderation in price pressures is consistent with forecasts that the Fed will further scale back its tightening campaign next week, when it’s expected to raise rates by 25 basis points. Policymakers boosted the benchmark rate by 50 points in December after 75 basis-point hikes at their previous four meetings.

The world’s largest economy expanded 2.1% last year. In 2021, when demand snapped back from pandemic-related shutdowns, the economy grew 5.9% — the best performance since 1984.

The GDP data showed services spending increased at 2.6% annualized rate in the October-December period, the slowest since last year’s first quarter. Outlays on goods rose at a 1.1% pace, the first advance since 2021.

Business investment slowed sharply after a third-quarter surge. Spending on equipment declined an annualized 3.7%, the most since the second quarter of 2020. Outlays for structures rose at a 0.4% pace.

Let’s hope the BEA isn’t padding the numbers like the BLS was caught doing in the first half of 2022.

Lastly, US Real GDP growth YoY FELL to only 0.95925% as M2 Money growth disappears.

You must be logged in to post a comment.