The ADP National Employment Report SA Private Nonfarm Level Change printed this morning confirming what most of us already knew … the US economy is slowing if not already in recession.

The ADP jobs added grew by only 132k in August as The Fed’s M2 Money growth slowed.

Since The Federal Reserve and Federal government overstimulated the economy when Covid surfaced in early 2020, The Fed’s balance sheet expanded to near $9 TRILLION which helped existing home sales median price YoY hit 25.2% in May 2021 but falling to 10.8% YoY in July 2022 as The Fed tightened rates.

It will be a monetary inferno if The Fed decides to actually unwind its $9 trillion balance sheet.

Mortgage application volume dropped and remained at a multi-decade low last week(back to 1997), led by an 8 percent decline in refinance applications, which now make up only 30 percent of all applications. Purchase applications have declined in eight of the last nine weeks, as demand continues to shrink due to higher rates and a weaker economic outlook.

Mortgage applications decreased 3.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 26, 2022.

The unadjusted Purchase Index decreased 4 percent compared with the previous week and was23 percent lower than the same week one year ago.

The Refinance Index decreased 8 percent from the previous week and was 83 percent lower than the same week one year ago.

Just wait for The Federal Reserve to start unwinding its enormous balance sheet!

US home price growth is decelerating as The Federal Reserve let’s some of the air out of the monetary tires.

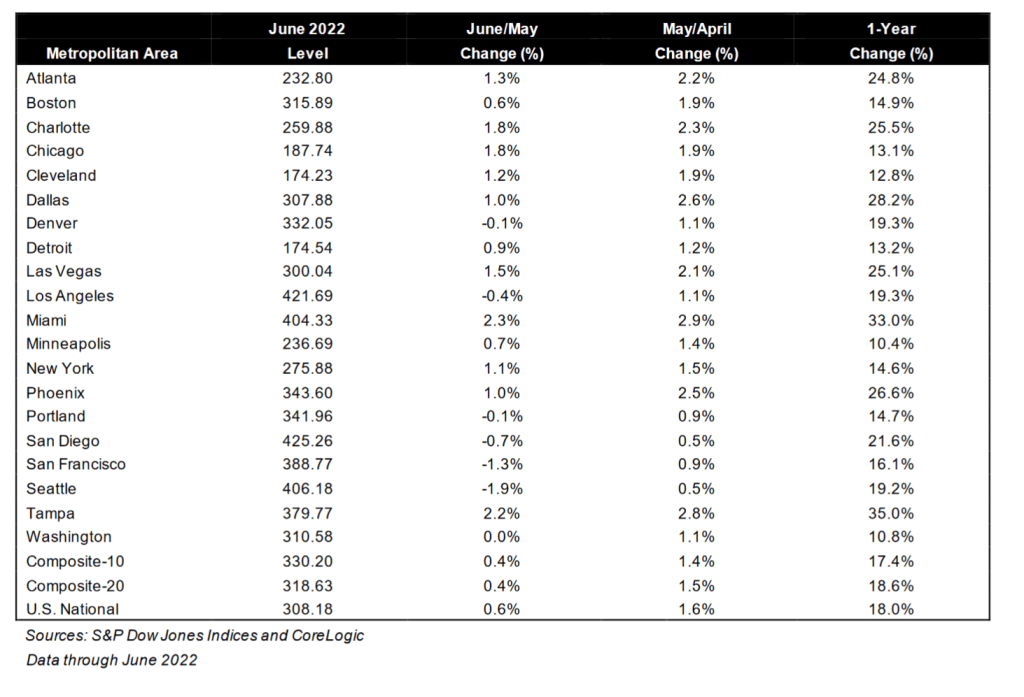

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported an 18.0% annual gain in June, down from 19.9% in the previous month. The 10-City Composite annual increase came in at 17.4%, down from 19.1% in the previous month. The 20-City Composite posted an 18.6% year-over-year gain, down from 20.5% in the previous month.

Tampa, Miami, and Dallas reported the highest year-over-year gains among the 20 cities in June. Tampa led the way with a 35.0% year-over-year price increase, followed by Miami in second with a 33.0% increase, and Dallas in third with a 28.2% increase. Only one of the 20 cities reported higher price increases in the year ending June 2022 versus the year ending May 2022.

While the Case-Shiller National home price index slowed to 18% YoY in June, the median price for existing home sales slowed to 10.55% YoY in July as The Fed’s M2 Money growth YoY slowed to 5.28% and Freddie Mac’s 30yr mortgage rate rose to 5.3%.

Bear in mind that Case-Shiller is lagged compared to the existing home sales numbers. Much like the New York Yankees manager picking the hottest batter in June to start in September. The Yankees traded poor-hitting Joey Gallo to the LA Dodgers to supplement poor-hitting Cody Bellinger.

In any case, as of June 2022, the 20 metro areas covered by Case-Shiller all grew in price in double digits with alligator-infested Tampa and Miami FL in the 30% rate, rattlesnake-infested Dallas is in 3rd place at 28.2%. Phoenix AZ, where I used to live, slowed to 26.6%. Yes, I had rattlesnakes on my property (a nest of Mohave Rattlers) and a large Diamond-backed Rattler behind my house).

Let’s see how housing holds up with more Fed monetary tightening. Fed Chair Powell is predicting “pain.”

As inflation burns the US middle class and low wage workers, The Federal Reserve reaffirmed at Jackson Hole that they are the NEW Smoky The Bear (only The Fed can fight inflation fire!) But of course, Federal spending and energy policies can drive up prices too.

Having said that, the 2-year Treasury yield and 30yr mortgage rate are rising rapidly.

The Fed is trying to cool demand by raising rates after lax monetary policy since late 2008.

While the US 2-year Treasury yield is up only slightly today, the Eurozone is seeing their 2-year sovereign yields spiking by 11-15+%.

It used to be that economists would see two consecutive quarters of negative Real GDP growth and say “recession.” But apparently not economists like Thaler. But at least the Atlanta Fed’s GDPNow real GDP tracker is pointing to weak growth for Q3 at 1.379%.

So, if 1.38% real GDP growth holds up, the US is technically no longer in a recession. So, Thaler would be correct. However, the US Treasury yield curve 10Y-2Y (blue line) remains inverted and the Conference Board’s Leading Indicators (yellow line) is growing at 0.0% YoY.

And for those expecting interesting news from The Fed’s Jackson Hole conference, I expect Powell to say that The Fed is going to have to jack-up rates to fight inflation (which is crushing the middle class and low wage workers).

Unlike Thaler, I don’t see a strong economy, just a weak economy except for employment (at negative wage growth). And declining savings.

US mortgage applications just hit the lowest levels in 22 years, January 2000 as The Federal Reserve continues monetary tightening to combat Bidenflation.

Mortgage applications decreased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending August 19, 2022. The Refinance Index decreased 3 percent from the previous week and was 83 percent lower than the same week one year ago.The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 21 percent lower than the same week one year ago.

MBA mortgage applications just declined to their lowest level in 22 years (January 2000) as The Fed has begun raising rates to fight inflation caused by 1) excessive monetary stimulus since late 2008, 2) Biden’s green energy policies driving up transportation costs, 3) distortionary Federal spending (e.g., Covid relief, infrastructure bills and now green energy/IRS spending by Biden/Pelosi/Schumer).

Here is the data summary for the latest MBA applications report.

Fed Chair Jerome Powell shrinking The Fed’s balance sheet.

The National Association of Realtors’ Homebuyer Affordability Index for fixed-rate mortgages is now at the lowest reading since 2006 and the peak of the 2005-2007 housing bubble that burst catastrophically.

The reason? The Federal Reserve, in their attempt to put out the inflation fire (caused by 1) excessive monetary stimulus since late 2008, 2) rampant Federal spending and 3) Biden’s green energy policies, driving up prices.

If we compare mortgage rates with the US Treasury 10Y-2Y yield curve, you can see that the yield curve remains inverted (historically a bad sign). This may signal an eventual loosening of monetary policy by March 2023.

The phrase “crossing the Rubicon” is an idiom that means that one is passing a point of no return. Its meaning comes from allusion to the crossing of the river Rubicon by Julius Caesar in early January 49 BC.

Indeed, the US crossed the FISCAL Rubicon in Q4 2012. That is when US Treasury Public Debt outstanding exceeded Real GDP. And the gap has been growing ever since.

In case you were wondering why M2 Money Velocity is so low, it is because the US is in constant crisis management mode as an excuse to spend trillions of dollars …. that generates progressively lower real GDP.

They built this nation on MMT (Modern Monetary Theory) which translates to the Federal government and Federal Reserve just wanting to spend trillions and trillions. Since 2005 (the peak of the housing bubble), the US Federal Reserve has increased the M2 Money stock more than real GDP growth in almost every quarter.

I remember when macroeconomists used to say “Everything is beautiful … as long as M2 Money growth is LESS than real GDP growth.” But we have apparently shifted to MMT when Everything is beautiful as long as there is a crisis and Congress can spend trillions.

Now Biden/Congress are spending billions in trying to reduce inflation (seriously, only in Washington DC would they think that massive spending bills would REDUCE inflation).

Under President Biden, inflation has soared and The Federal Reserve claims that they want to extinguish the inflation fire by tightening monetary policy … resulting in rising mortgage rates. Under Biden, mortgage purchase applications are DOWN -41.5% while mortgage rates are UP 96%.

(Bloomberg)The US mortgage industry is seeing its first lenders go out of business after a sudden spike in lending rates, and the wave of failures that’s coming could be the worst since the housing bubble burst about 15 years ago.

There’s no systemic meltdown coming this time around, because there hasn’t been the same level of lending excesses and because many of the biggest banks pulled back from mortgages after the financial crisis. But market watchers nonetheless expect a string of bankruptcies broad enough to trigger a spike in layoffs in an industry that employs hundreds of thousands of workers, and potentially an increase in some lending rates. More of the business is now controlled by independent lenders, and with mortgage volumes plunging this year, many are struggling to stay afloat.

Please note that mortgage purchase applications are DOWN -41.5% under Biden while mortgage rates are UP 96%.

Margin Calls Many other lenders have seen the value of their loans drop, said Scott Buchta, head of fixed-income strategy at Brean Capital, an independent investment bank. The Federal Reserve has tightened rates by 2.25 percentage points this year in an effort to tame inflation, and 30-year US mortgage rates have surged above 5% for government-backed loans. That’s close to their highest levels since the financial crisis, from around 3.1% at the end of last year.

That’s beaten down the value of home loans made just a few months ago. A mortgage made in January and not eligible for government backing could have traded in early August somewhere around 85 cents on the dollar. Lenders usually try to make loans worth somewhere around 102 cents to cover their upfront costs.

For a lender whose loans dropped to 85 cents, the losses can be debilitating, even if they aren’t realized yet. On top of that, business is broadly plunging. Overall mortgage application volume has plunged by more than 50% this year, according to the Mortgage Bankers Association. These business conditions are spurring banks that provide lines of credit known as warehouses to make margin calls and cut credit.

“The warehouse lenders in this industry seem to be extremely on top of things in this downturn, unlike in ‘08,” said bankruptcy attorney Mark Power, who is representing creditors in the First Guaranty bankruptcy. “They are making margin calls quickly.”

Banks have emergency funding they can tap in times of crisis, which can often allow them to stay afloat in hard times. But not always: emergency financing from the Federal Reserve is usually only available for solvent institutions with a chance of recovering. In the last downturn, so many banks had so many soured loans and struggling assets of all kinds that hundreds failed. Nonbanks went bust as well.

You must be logged in to post a comment.