In honor of Wolfgang Peterson who passed away yesterday, the Director of the classic WWII movie “Das Boot!” …. ALARM!

Sales of previously owned US homes fell for a sixth straight month in July in the latest indication of how high borrowing costs and waning demand are propelling the housing market’s rapid decline. In fact, existing home sales fell -19% YoY in August.

Contract closings fell 5.9% in July to an annualized 4.81 million, the weakest since May 2020, figures from the National Association of Realtors showed Thursday. The median estimate called for 4.86 million in a Bloomberg survey of economists. Sales fell 22.4% from a year ago on an unadjusted basis.

The nearly 26% decline in previously owned home sales since January marks the steepest six-month plunge in records back to 1999 and underscores a housing market that’s reeling from elevated mortgage rates and prices. The industry is also experiencing a slowdown in construction, and more buyers are backing away from deals.

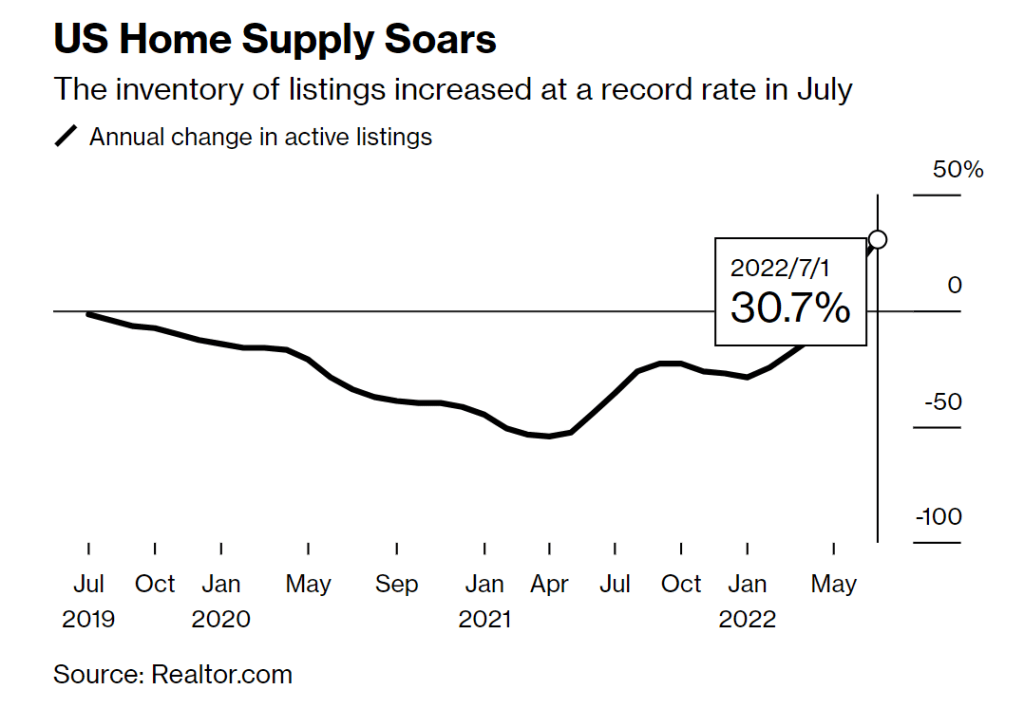

Weaker demand has led to a pickup in inventory, which may help to cool home prices in coming months.

The median price of existing home sales growth fell to 10.55% YoY as M2 Money growth slows.

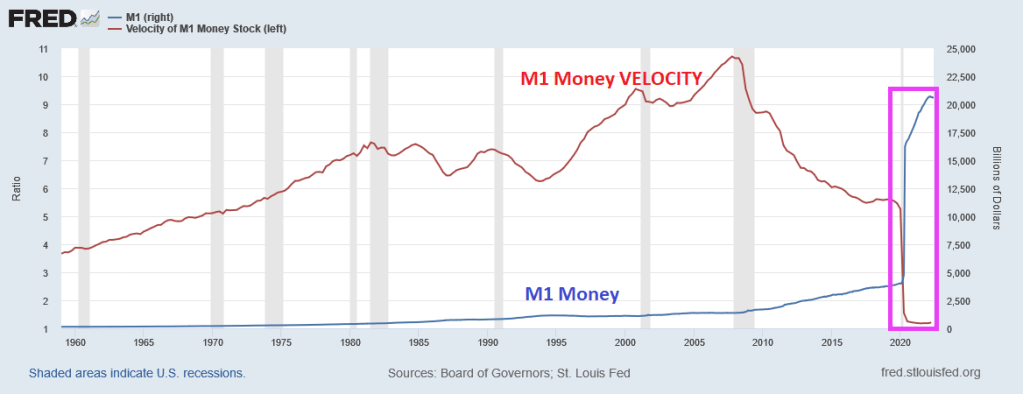

Its all about The Federal Reserve.

You must be logged in to post a comment.