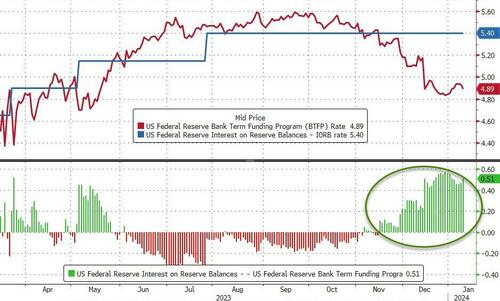

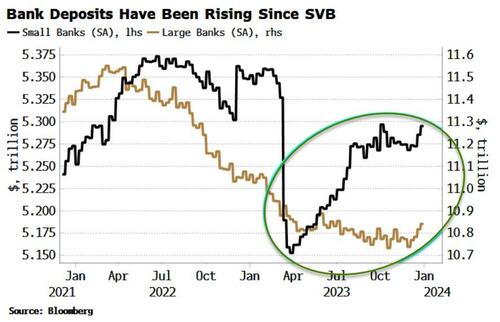

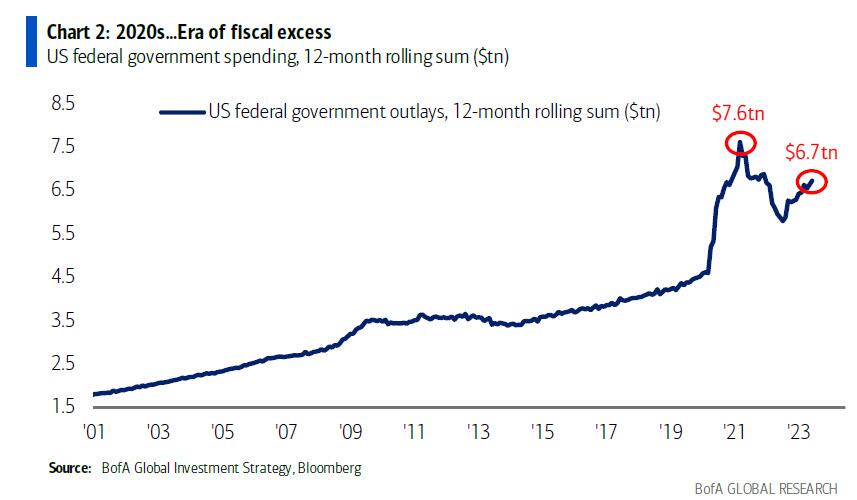

Biden and Congress continue their massive spending spree, mostly on themselves and their donors, creating a massive Debt Star capable of unfathomable economic destruction. This will require massive money printing to fund the US Debt Star.

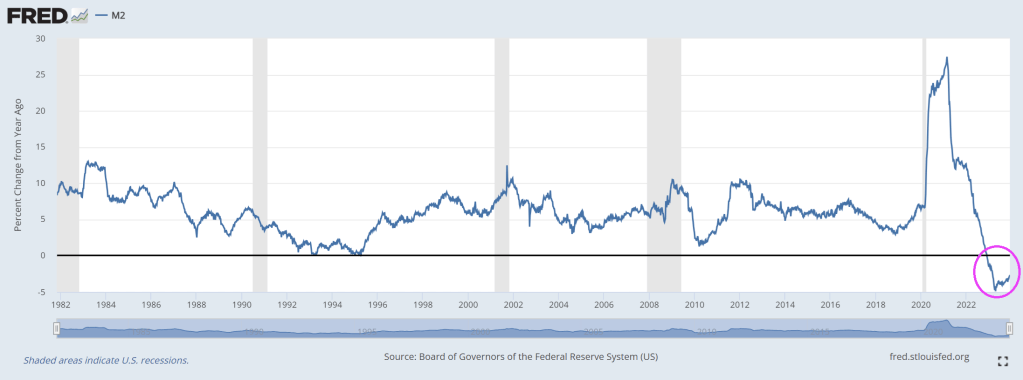

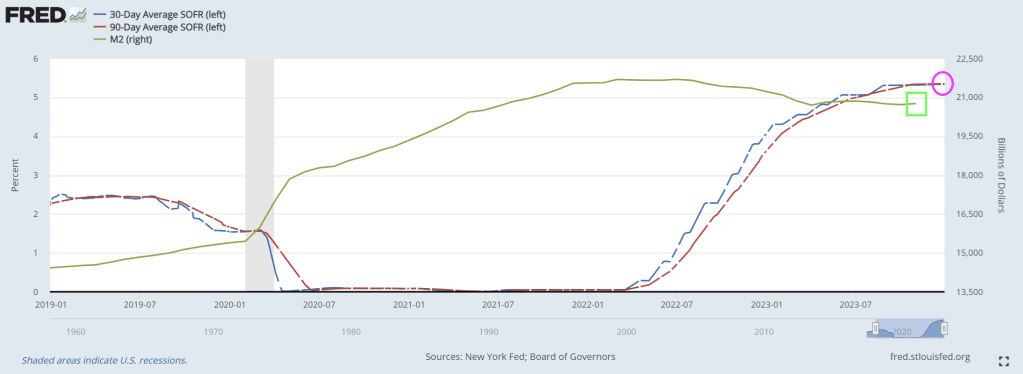

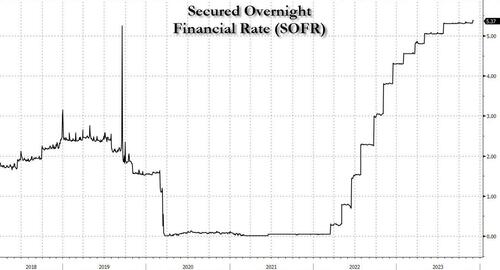

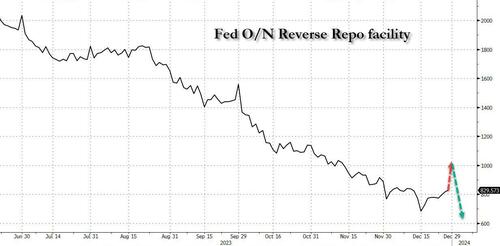

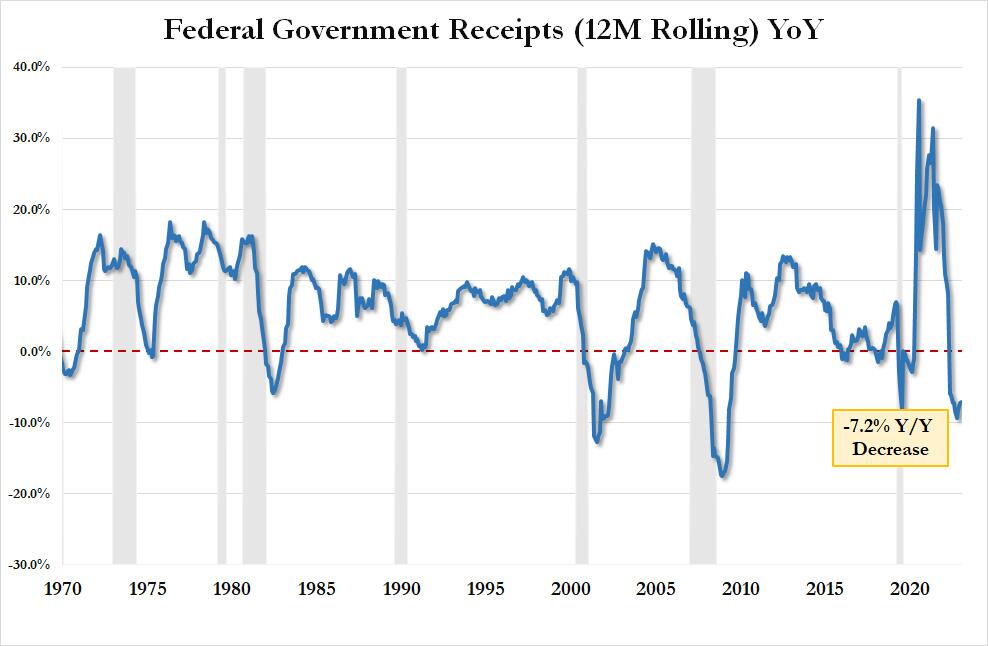

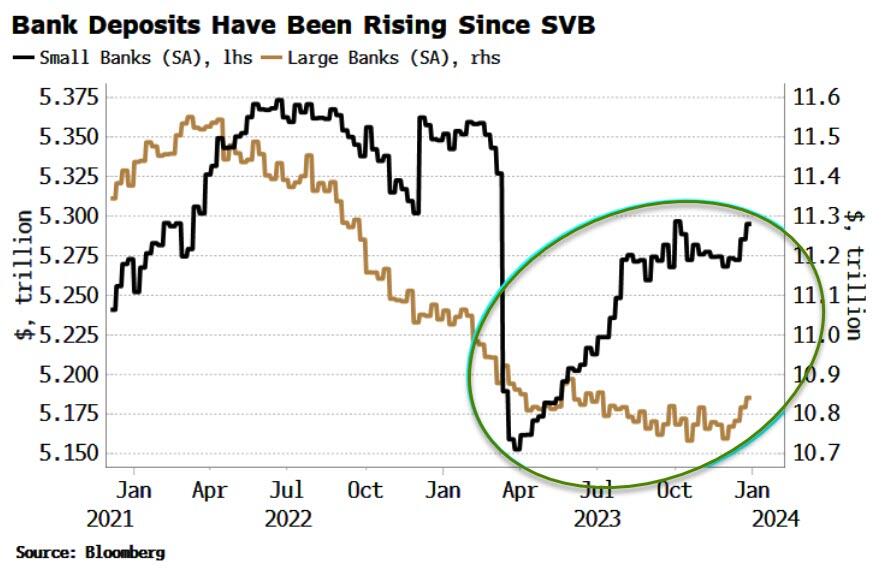

But as of today, M2 Money growth is negative as is bank credit growth.

But all this is about to change.

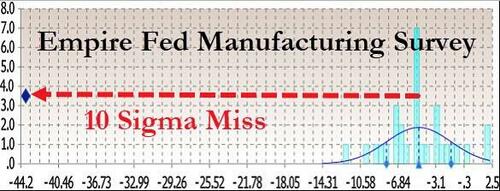

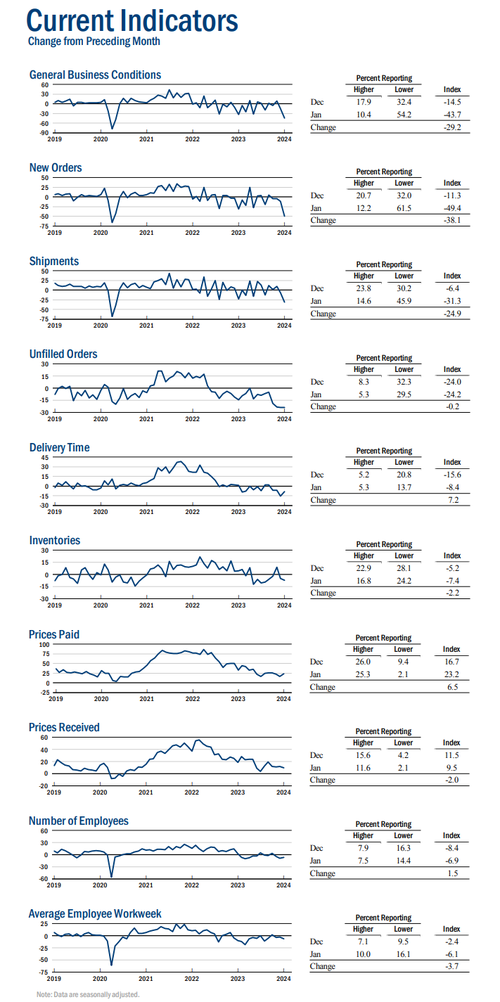

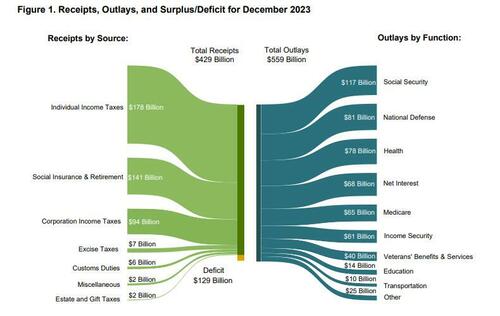

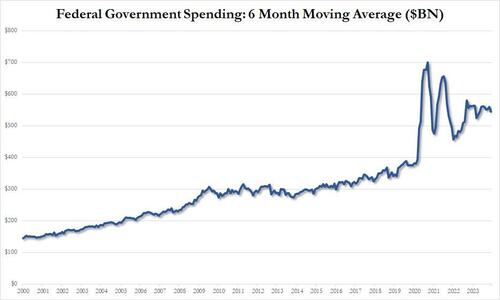

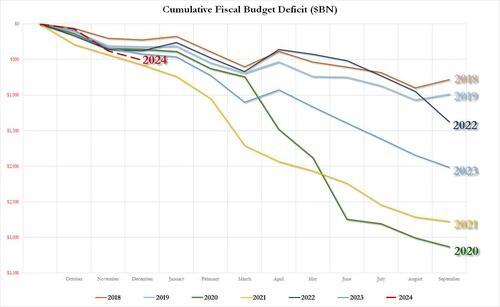

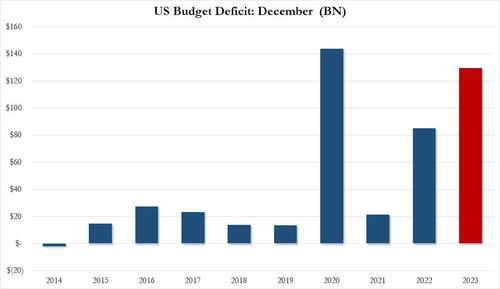

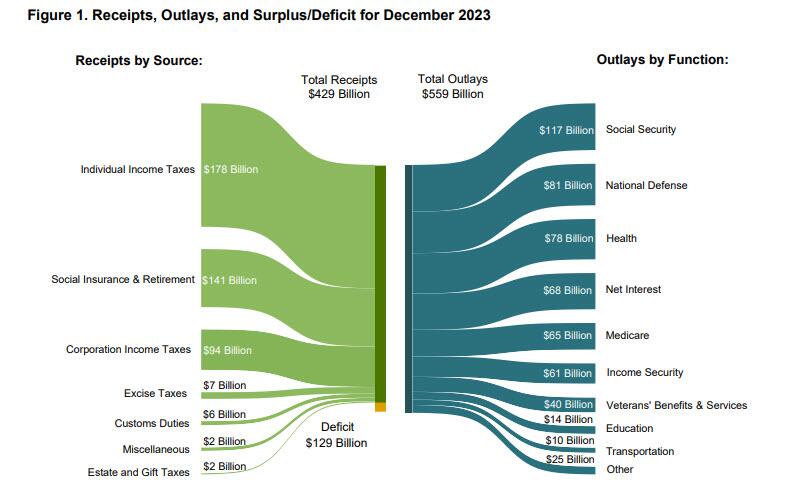

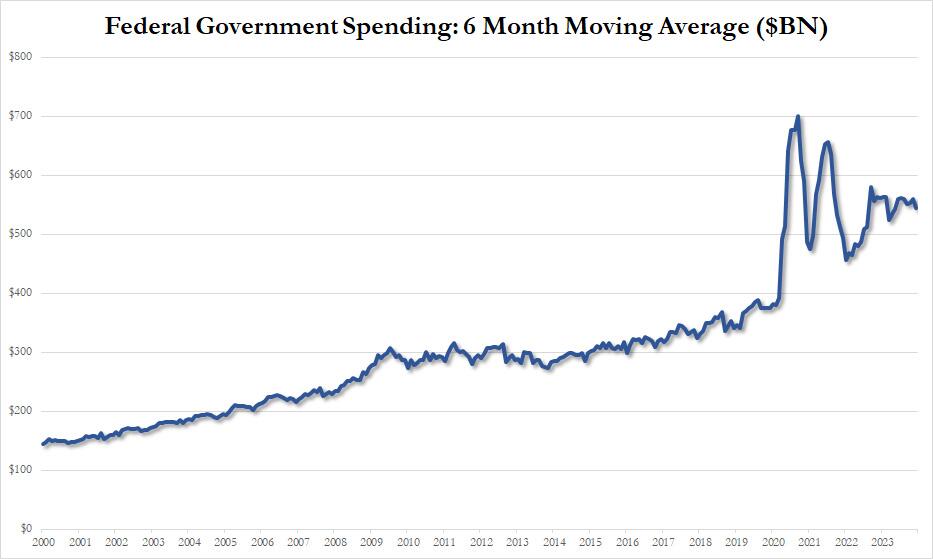

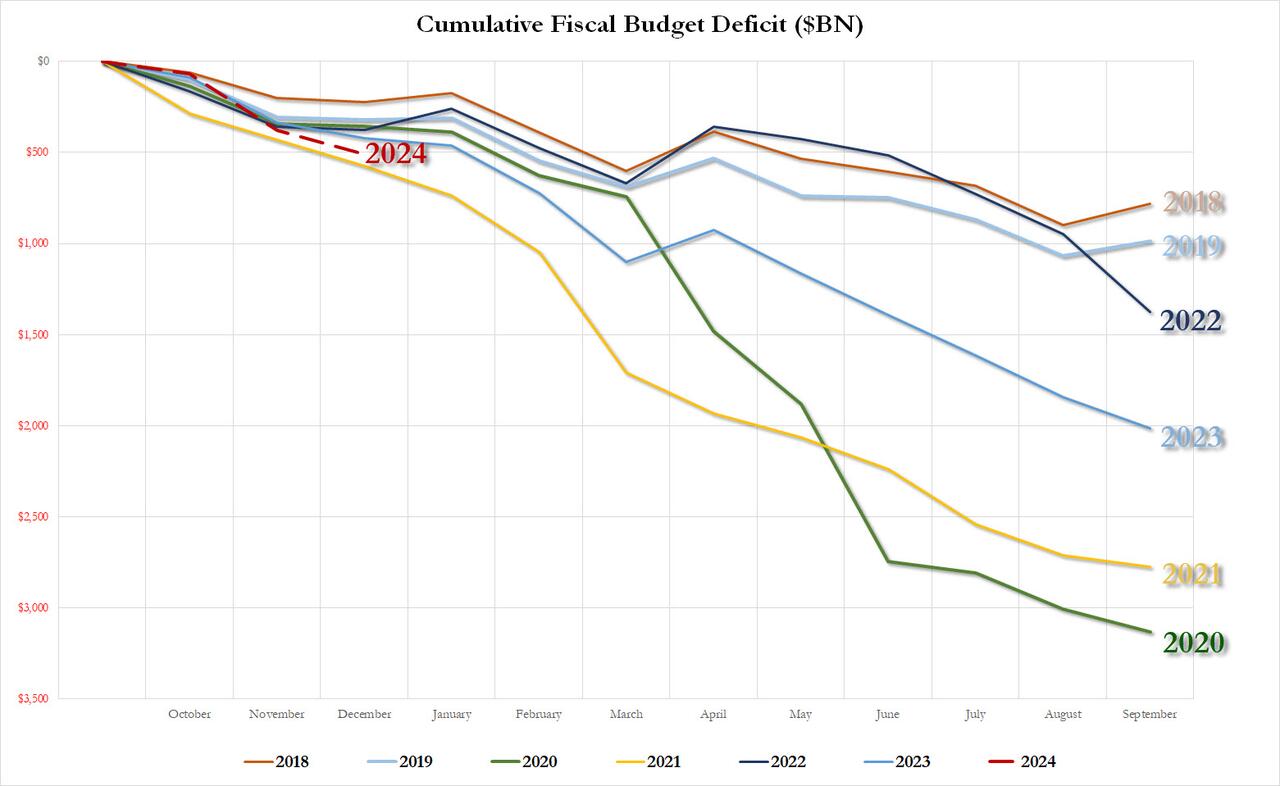

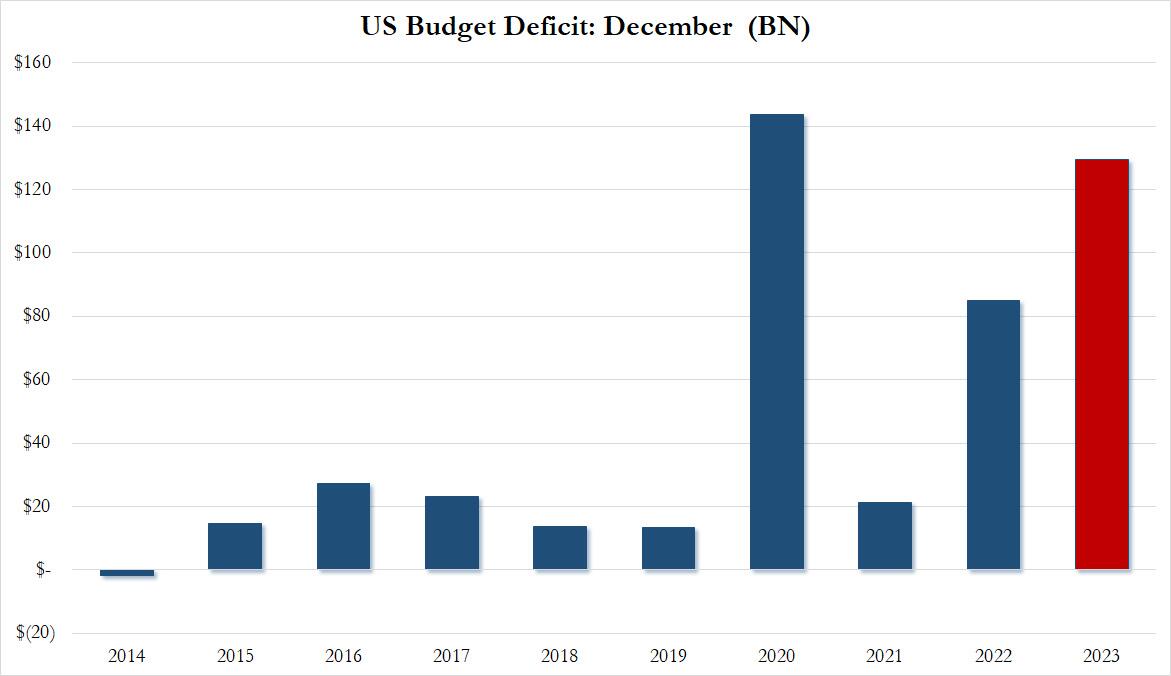

The U.S. federal government published a December deficit of $129 billion, up 52% from the previous year. The private sector recession is clear as expenses continue to rise while tax receipts decline. If we look at the period between October and December 2023, the deficit ballooned to a staggering $510 billion.

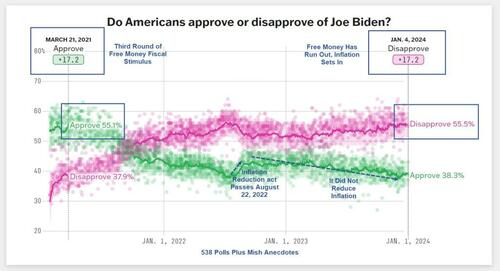

You may remember that the Biden administration expected a significant deficit reduction from its tax increases and the expected benefits of its Inflation Reduction Act.

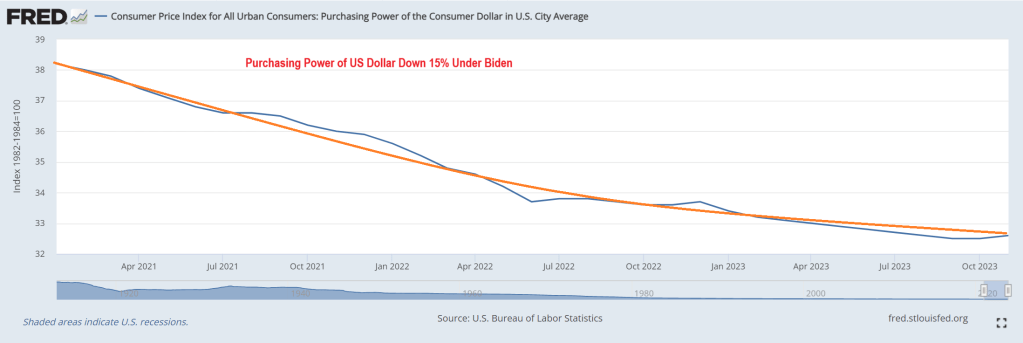

What Americans got was a massive deficit and persistent inflation.

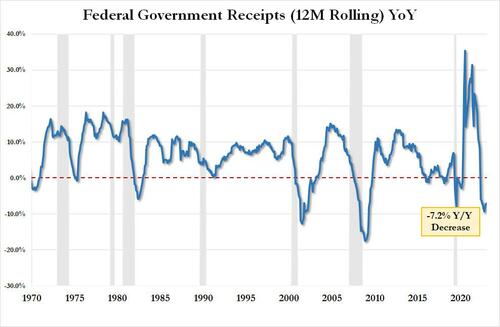

According to Moody’s chief economist, Mark Zandi, the entire disinflation process seen in the past years comes from exogenous factors such as “fading fallout from the global pandemic on global supply chains and labor markets, and the Russian War in Ukraine and the impact on oil, food, and other commodity prices.” The complete disinflation trend follows the slump in money supply (M2), but the Consumer Price Index (CPI) should have fallen faster if deficit spending, which means more consumption of newly created currency, would have been under control. December was disappointing and higher than it should have been.

The United States annual CPI (+3.4%) came above estimates, proving that the recent bounce in money supply and rising deficit spending continue to erode the purchasing power of the currency and that the base effect generated too much optimism in the past two prints. Most prices rose in December, and only four items fell. In fact, despite a large decline in energy prices, annual services (+5.3%), shelter (+6.2%), and transportation services (+9.7%) continue to show the extent of the inflation problem.

The massive deficit means more taxes, more inflation, and lower growth in the future.

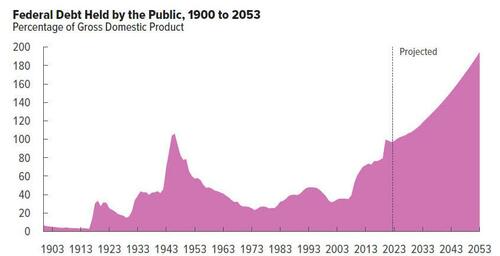

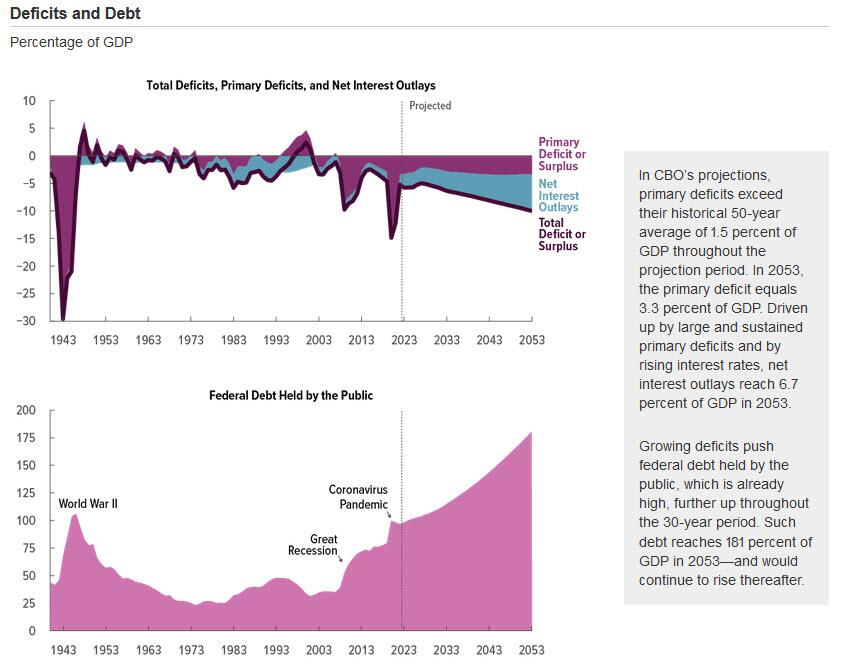

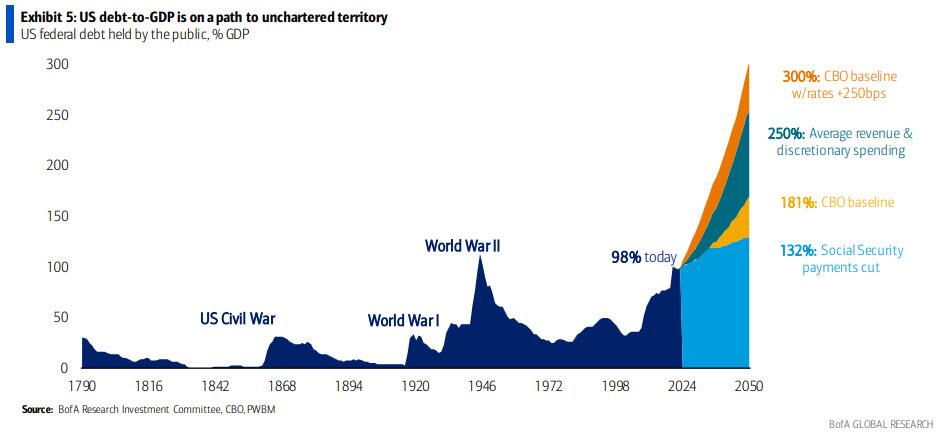

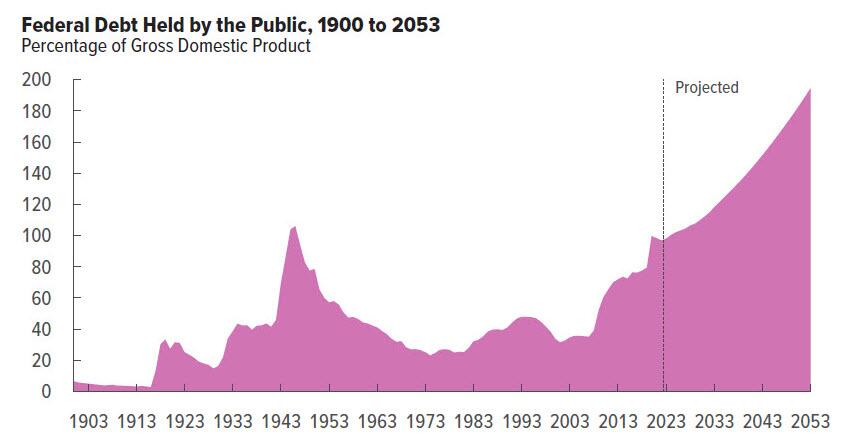

The Congressional Budget Office (CBO) expects an unsustainable path that still leaves a 5.0% deficit by 2027, growing every year to reach a massive 10.0% of GDP in 2053 due to a much faster growth in spending than in revenues. The enormous increase in debt will also lead to extremely poor growth, with real GDP rising much slower throughout the 2023–2053 period than it has, on average, “over the past 30 years.”

Deficits are not a tool for growth; they are tools for stagnation.

Deficits mean that the currency’s purchasing power will continue to vanish with money printing and that the real disposable income of Americans will be demolished with a combination of higher taxes and a weaker real value of their wages and deposit savings.

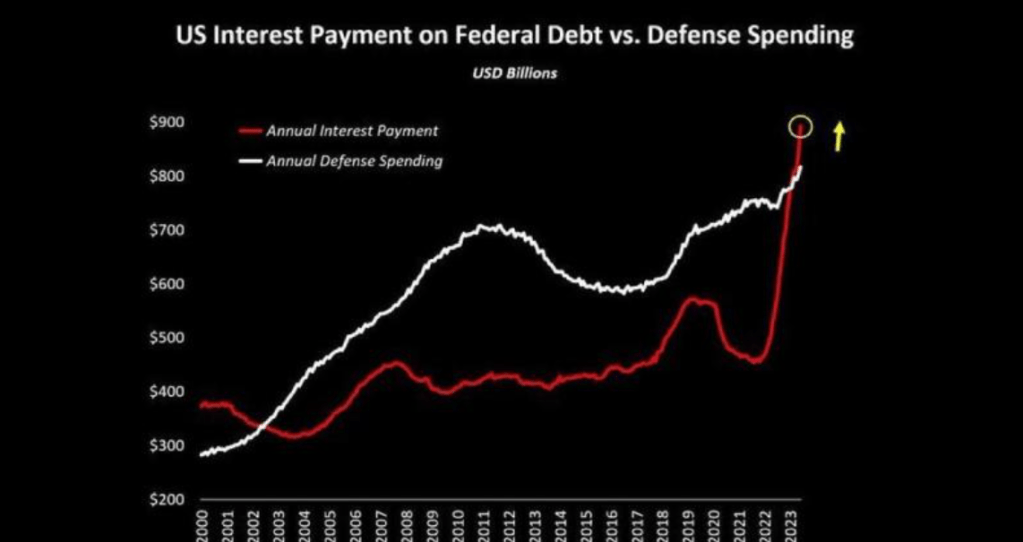

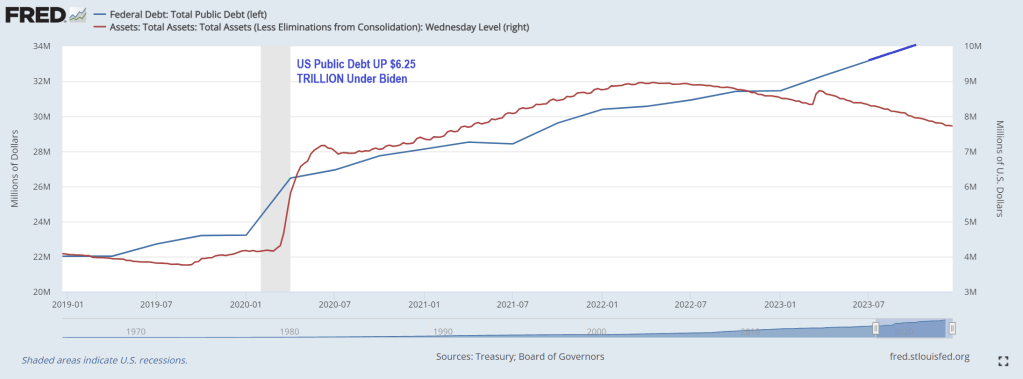

We must remember that, in Biden’s administration’s own estimates, the accumulated deficit will reach $14 trillion in the period to 2032.

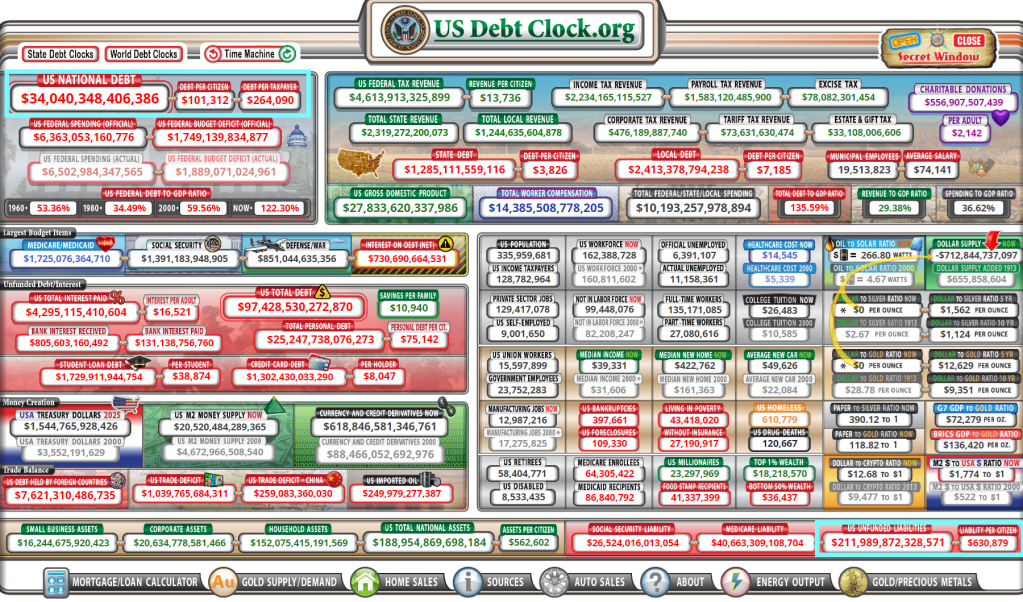

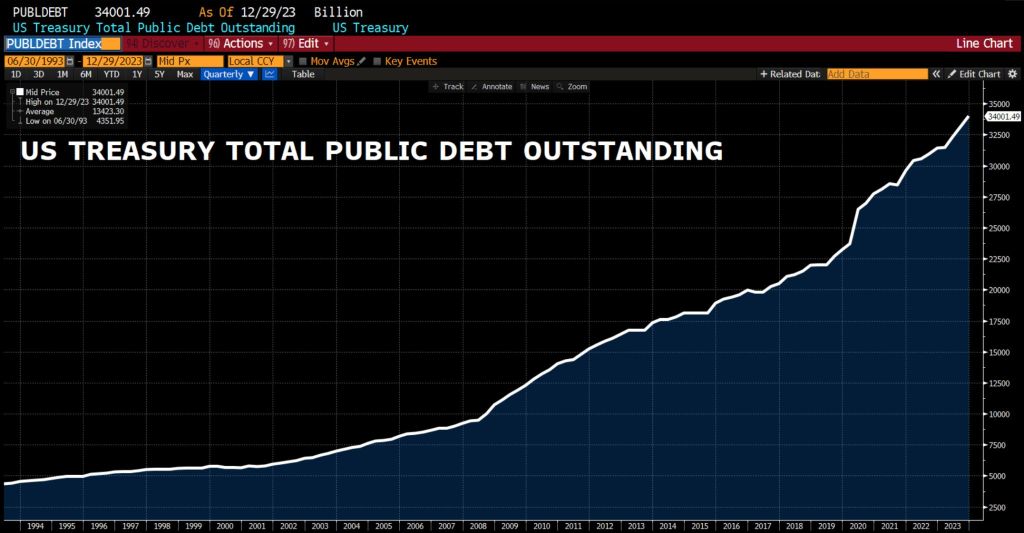

Yes, the US has $34 trillion in national debt and $212 trillion in promises made to keep the 99% quiet while the 1% gut the economy for their own wealth. Think Biden, Clintons, and various Congress Critters who suddenly become millionaires.

The Debt Star was born under Obama and weaponized under Biden/Pelosi/Schumer.

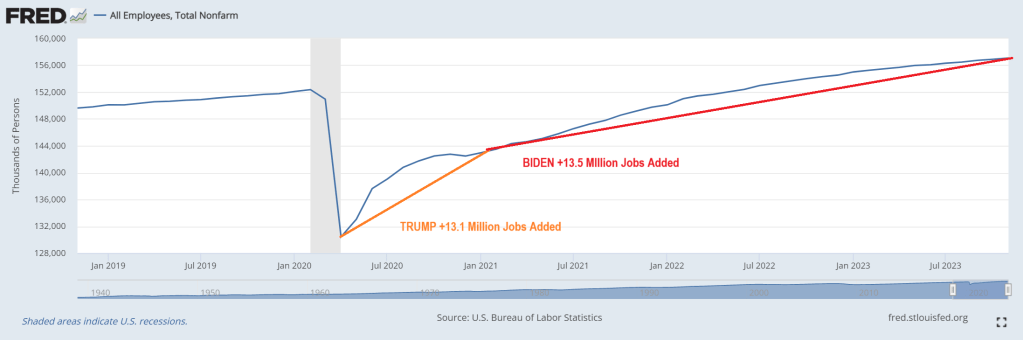

Yes, national debt rose under Trump too. Bear in mind that spending originates in The House and Trump was saddled with warhawks like RINO Paul Ryan and insider trading expert and warhawk Nancy Pelosi.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.