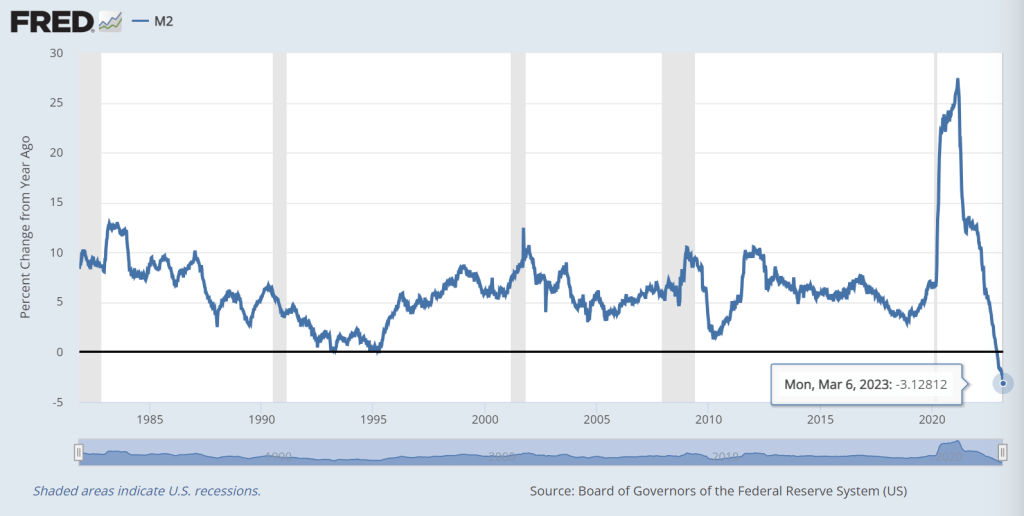

America’s mega bank, The Federal Reserve, is slowing M2 Money growth so rapidly that it looks like it is depthcharging the US economy.

Inflation in the US has been booming since 1) Biden attacked fossil fuels, 2) The Fed’s overresponse to Covid (+27.48% YoY on February 22, 2021 near the beginning of Biden’s Reign of Error). and 3) out of control Federal spending under Biden, Pelosi and Schumer.

Fed Funds Futures point to two more Fed rate hikes before The Fed drop rates like a depthcharge. This depthcharge will help create a rekindling of asset bubbles.

The Taylor Rule suggets a Fed Funds Target rate of 11.77 while the current target rate is only 5%. This is called “leading from behind.”

Here is The Fed monitoring the US economy in order to decide on firing more financial torpedos!

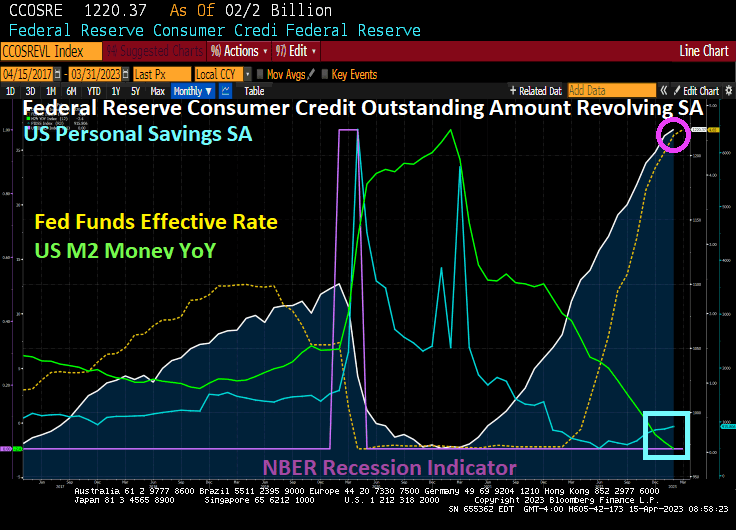

Of course, what is really troubling is that credit card useage is soaring as The Fed hikes interest rates to combat inflation … caused by Janet Yellen and The Fed keeping rates near zero for too long under Obama. Then we have Biden fighting fossil fuels and Congress spending like drunken sailors in port. All together? Consumers turn to credit cards to cope and their personal savings are dwindling.

How to protect yourself against out-of-control Fed money printing? Gold is up over $2,000.

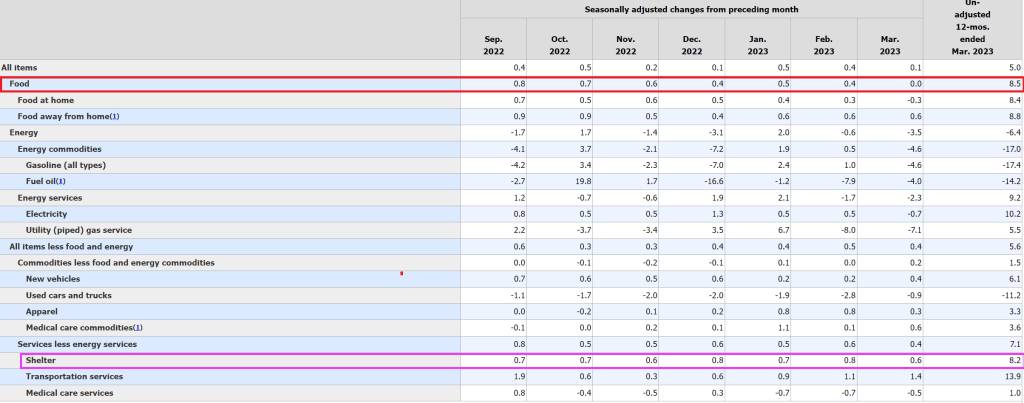

US Producer Price Index (PPI) final demand YoY fell to 2.7% in March as The Fed withdraws its massive monetary stimulus.

Final demand MoM fell -0.5% in March. But the interest number is CORE PPI ex food and energy actually down but at 3.6%. So, CORE PPI final demand growth is higher than the aggregate.

Do I detect a trend in US continuing jobless claims?

At least Biden is in Belfast Ireland making his usual gaffes, telling outrageous lies and looking totally lost. As usual. He can do less damage to the US by being in Ireland.

US Core inflation keeps rising despite The Federal Reserve slowing M2 Money growth and raising The Fed Funds Targget rate as The Fed plays catch up from Janet Yellen’s “Too Low For Too Long” monetary policies under Obama. And she was … negligent.

US Core Inflation (Core CPI YoY) rose to 5.6% in March despite The Fed cranking up their target rate and rapidly withdrawing M2 Money.

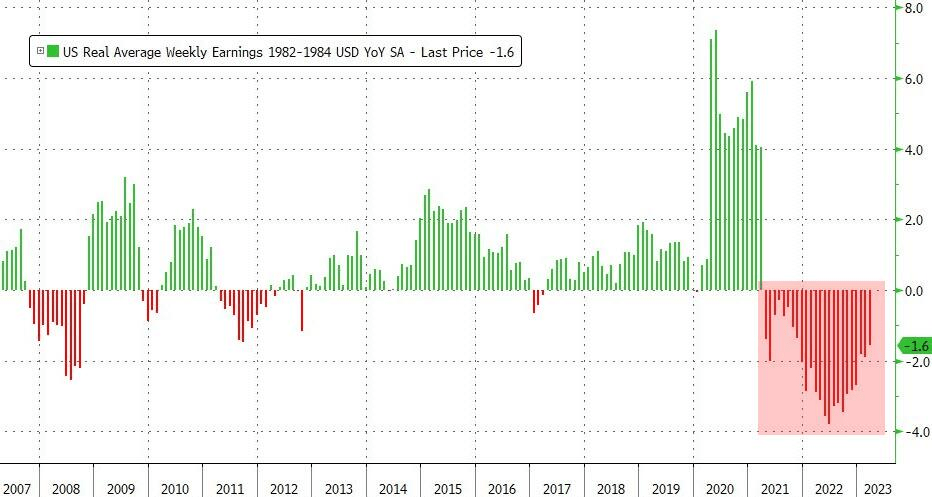

How about REAL wages? Real average weekly earnings growth has now been negative for 24 straight months.

One reason that core inflation is still rising is that The Fed still has not raised rates sufficiently. According to the Taylor Rule, the Fed Funds Target rate should be 11.77% based on core inflation of 5.6%. Hey, The Fed isn’t even half way there. It is like the Doolittle Raiders in World War II dropping their bombs 100 miles off the Japanese coast well short of their target.

Fed Funds Futures are pricing in one more rate hike (and a small one at that) before they resume cutting rates again.

Between inflation under Biden and The Fed’s counterattack to get inflation to 2%, I call this the Biden Blitz.

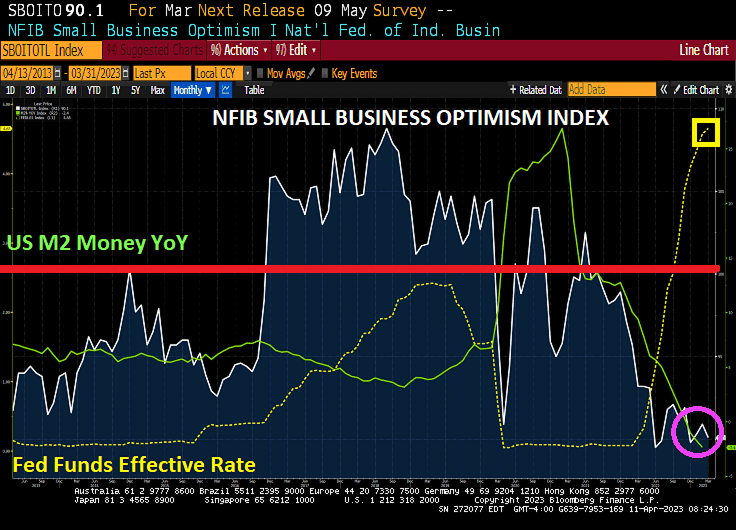

Unlike what the elites in Washington DC think, small business are the cornerstone of the US economy. Unfortunately, small business optimism is getting crushed and just fell in March to a level lower than that found during the Covid economic shutdowns of 2020. HOW is it possible for small businesses to be even less optimistic than it was in April 2002, the nadir of the Covid economic shutdown?

Small business optimism soared in November 2016 after the election of Donald Trump and remained high (above 100) until Covid struck in March 2020. Small business optimism rose above 100 again with the massive money printing by The Fed (green line) and Federal spending spree. But as M2 Money growth slowed, small business optimism hasn’t been above 100 since August 2021. It has been all downhill since then as The Fed started to raise The Fed Funds Target Rate quite rapidly.

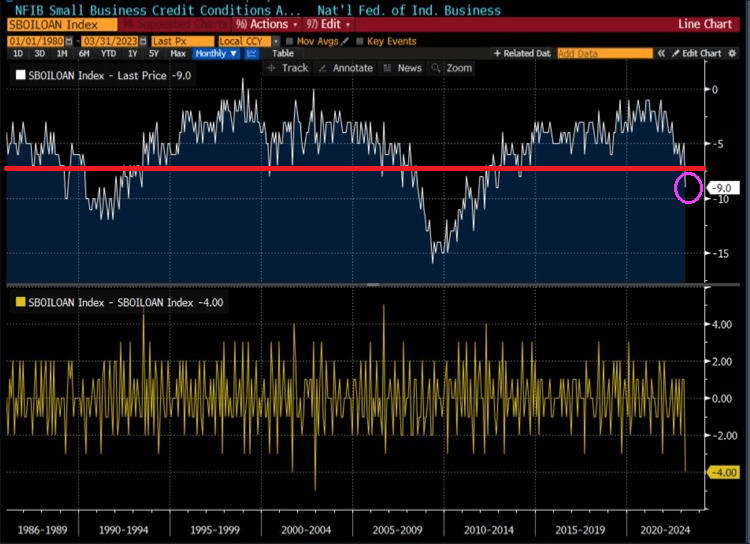

NFIB small business credit conditions are negative at -9.0 and sinking like The Titanic.

Biden is the face of big business (big banks, big pharma, big tech, big defense, big labor unions, big media, etc.). Biden just told Al Roker that he is indeed running for reelection, supported by …. big banks, big pharma, big tech, big defense, big labor unions, big media, etc.

Biden is no longer a President, but an old-time preacher screaming about MAGA Republicans as if they were demons. This is called Blitzkrieg Biden.

I read over the weekend that the Biden Administration was planning to unleash its army of social influencers on us to hype Biden’s economic accomplishments before the Presidential election. I am not one of his preferred social influencers. In fact, the US economy is slippin’ into darkness under Biden.

An example is ISM Manufacturing PMI which has declined to a level typically seen in prior recessions.

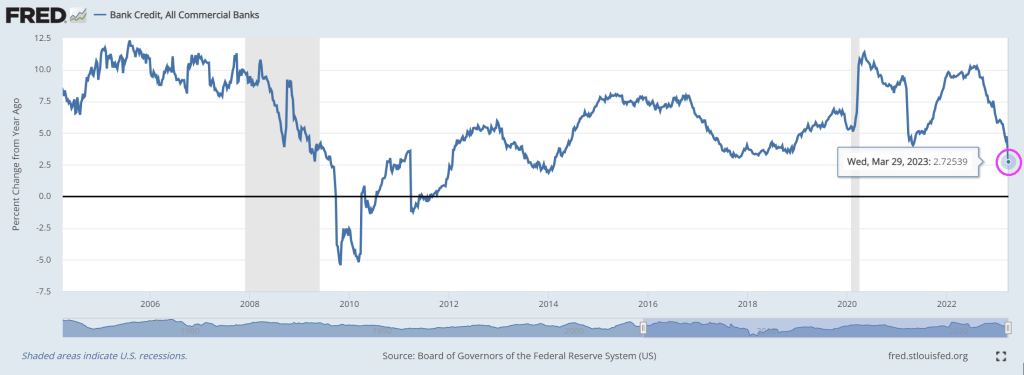

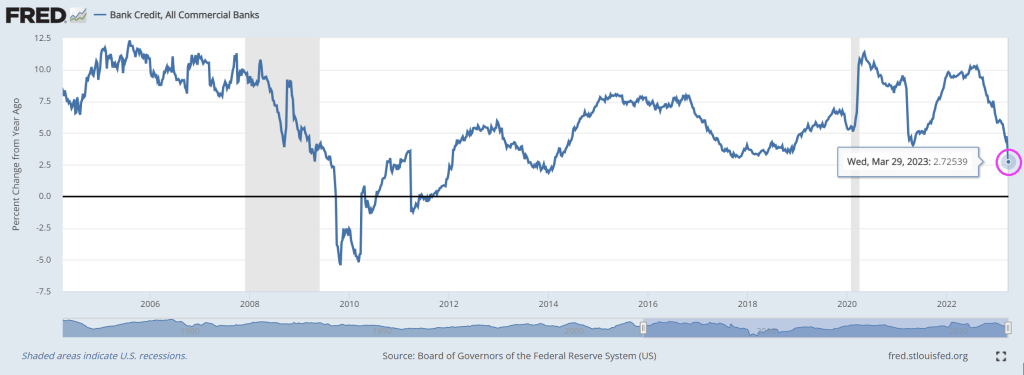

And then we have US bank credit growth which just crashed to the slowest growth rate since 2014.

Inflation started with Biden’s misguided war on US energy, then Biden/Congress helped inflation with an epic spending splurge. The Federal Reserve counterattacked with Fed rate hikes.

Over the past year, The Fed Funds Effective rate has risen and US bank credit has crashed to 2.73% year-over-year.

Do I detect a trend?

Since 2005, the crash in US bank credit is looking like 2008/2009 all over again.

Whether Biden is Cap’n Crunch or Jerome Powell or Janet Yellen, they are all crunching the US economy.

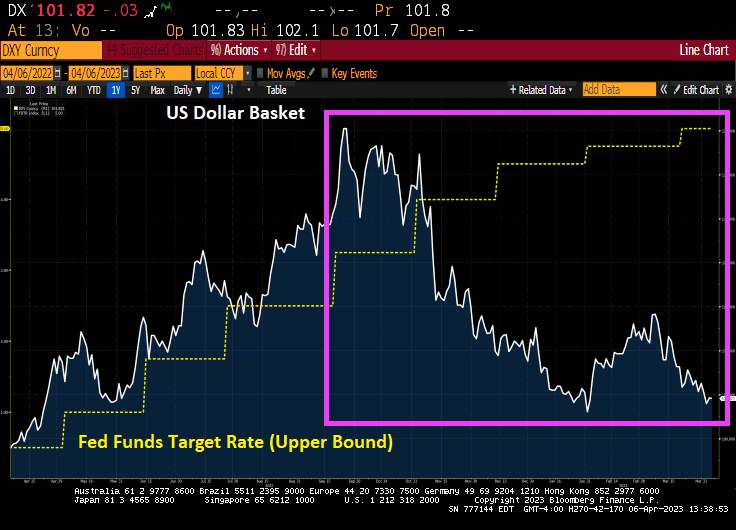

Biden, The Federal Reserve and insane Federal spending are killing King Dollar. Countries that used to use the US Dollar as reserve currency are dumping the dollar like a month old burrito.

What countries are dumping the dollar?

A lengthy list of countries are moving away from using the US dollar, which has long been the reserve currency of the world. The following countries are in the process of reducing their dependency on the dollar.

Russia

China

Iran

Brazil

Argentina

Saudi Arabia

UAE

India

The result?

Biden has vacationed 40% of the days he has been President. In his defense, he has probably needed that time to hunt down the classified documents has left strewn around his his home, vacation home, the Penn-Biden Center and Chinatown in DC.

We are truly addicted to gov! Or at least cheap money from The Federal Reserve.

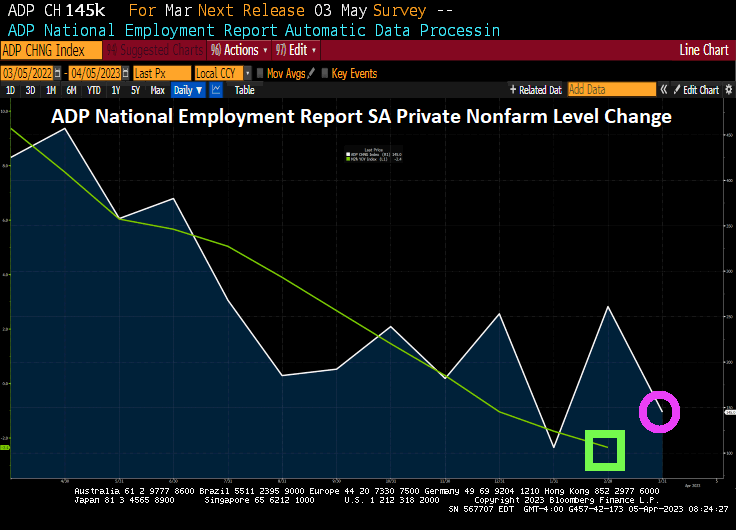

March’s ADP job report shows the US economy only added 145k jobs as The Fed removes its punch bowl. For the moment.

Its simply irresistable for the government to turn back on the printing press.

And then we have domestic banks reporting stronger demand for C&I Loans and real estate loan (for construction and development purposes) slumping to financial crisis lows.

Silicon Valley Bank’s blunders were encouraged by US regulation, went untested by the Federal Reserve and were “hiding in plain sight” until Wall Street and depositors grew alarmed.

That’s JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon’s assessment of the US banking crisis that sent markets careening last month, an episode he predicts is “not yet over” and will be felt for years. He said US authorities shouldn’t “overreact” with more rules.

In his wide-ranging annual letter to shareholders on Tuesday, Dimon described his firm’s aspirations for using artificial intelligence and ChatGPT, weighed in on geopolitics, and provided updates on JPMorgan’s activities in Ohio. This time, many of his sharpest remarks ripped at regulation, including capital rules that pushed banks to binge on low-interest assets that lost value as interest rates shot up.

“Ironically, banks were incented to own very safe government securities because they were considered highly liquid by regulators and carried very low capital requirements,” Dimon said. “Even worse,” he added, the Federal Reserve didn’t stress-test banks on what would happen as rates jumped.

When Silicon Valley Bank’s uninsured depositors realized it was losing money selling securities to keep up with withdrawal requests, they raced to pull their cash. Regulators then intervened and seized it.

Yes. Banking regulators were so focused on credit-exposure of banks (remember the subprime crisis of 2008?) that they really screwed up by having banks load-up on low credit-risk assets that usually have interest rate risk associated with them like Treasuries and mortgage-backed securities (MBS). What could go wrong?

What went wrong was that interest rates rose and unrealized losses on Treasuries and Agency MBS exploded.

Here is a chart of urealized losses on investment securities that banks have accumulated.

Apparently, The Fed and FDIC (and the myriad of Federal and State regulators) sit high on a mountain top and ignore interest rate risk.

You must be logged in to post a comment.