Undun. The Fed’s balance sheet, that is.

For all the focus on whether the Federal Reserve is about to pause its interest-rate hikes, there’s another critical policy decision sure to draw plenty of attention come Wednesday: What the central bank does with its massive pile of bond holdings.

The banking-sector turmoil that has only appeared to deepen, combined with a previous increase in funding pressures, has left financial markets keenly attuned to what the Fed will say about its $8.6 trillion balance sheet.

Until this month the stash had been shrinking as part of the Fed’s efforts to return it back to pre-pandemic levels. But now it has started to expand again as the Fed acts to bolster the banking system through a slate of emergency lending programs. Its latest step came Sunday, when it moved with other central banks to boost US dollar liquidity.

Some say financial-stability concern may spur policymakers to dial back the runoff of its bond portfolio, a process known as quantitative tightening that’s designed to drain reserves from the system. Still, others argue that even if the Fed does pause its rate increases, the central bank’s overarching goal of taming inflation means it’s unlikely it will signal any shift this week in efforts to shrink the holdings of Treasuries and mortgage-backed debt. The one exception, they note, would be if stress in the banking sector were to become much more severe.

The Fed’s move to backstop US banks “clearly expands the Fed’s balance sheet,” said Subadra Rajappa, head of US rates strategy at Societe Generale SA. If usage of the Fed’s liquidity facilities is “small and contained they probably continue QT, but if the take-up is large then they probably stop as it then starts to raise concerns over reserve scarcity.”

The fate of the Fed’s portfolio is a subject of debate after the collapse of several US lenders led the central bank to create a new emergency backstop, known as the Bank Term Funding Program, which it announced March 12. Banks borrowed $153 billion from the Fed’s discount window — lenders’ traditional liquidity backstop — in the week ended March 15, Fed data show, a record that eclipsed the previous all-time high set during the 2008 financial crisis. They also tapped the new program for $11.9 billion.

The central bank’s various liquidity programs added about $300 billion to the Fed’s balance sheet last week, reversing about half of the reduction the Fed has achieved since the runoff began last June. But some economists say the two programs can work in tandem, with the banking efforts targeting financial stability and QT remaining a steady part of the Fed’s plan to remove the support it provided during the pandemic.

It looks like a 25 basis point increase at the next meeting, then cuts in The Fed Funds Target Rate to 3.820% by January 2024.

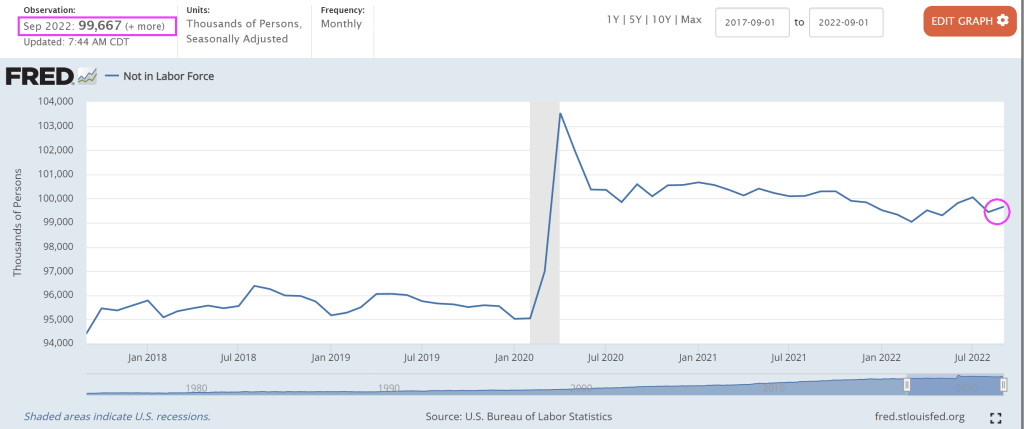

The labor market is still tight. So tight, we get this!!

You must be logged in to post a comment.