The Fed will annouce a pause at today’s FOMC meeting, so don’t look for mortgage rates to do much today.

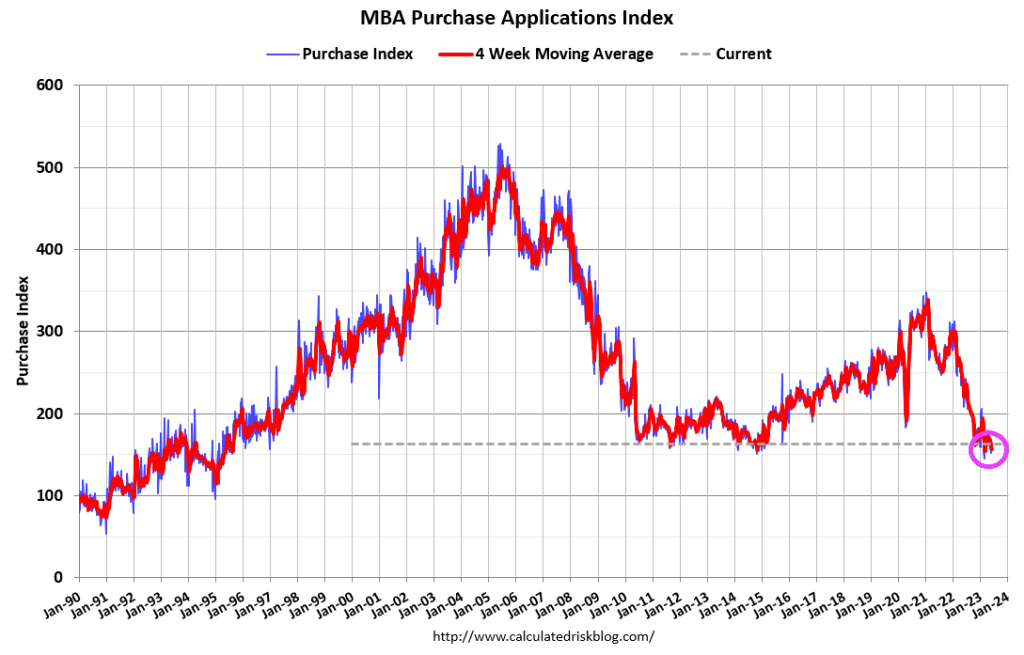

Mortgage applications increased 7.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 9, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 7.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 18 percent compared with the previous week. The Refinance Index increased 6 percent from the previous week and was 41 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 8 percent from one week earlier. The unadjusted Purchase Index increased 17 percent compared with the previous week and was 27 percent lower than the same week one year ago.

Mortgage rates declined for the second straight week, with the 30-year fixed rate decreasing to 6.77 percent. Mortgage applications were up over the week, but remained well below levels from a year ago.

Joe Biden’s new nickname is “The 5 Million Dollar Bribe Man.” Sort of like Steve Austin.

Okay, Joe Biden was generally regarded as the dumbest member of the US Senate and mean-spirited (I won’t repeat podcaster Joe Rogan’s opinion of Biden). Now we realize how brazenly corrupt Biden is (taking bribes from China and Ukraine to influence American poliicies). Not only is Biden an attrocious human being, but his policies have damaged the US middle class terribly thanks to inflation.

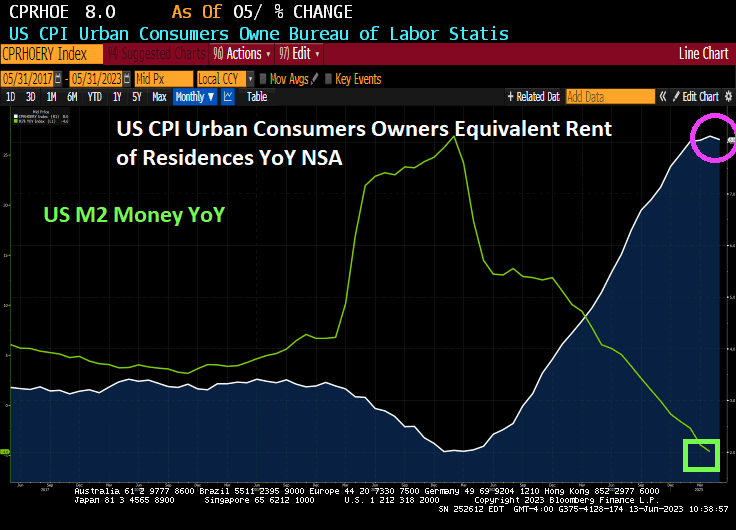

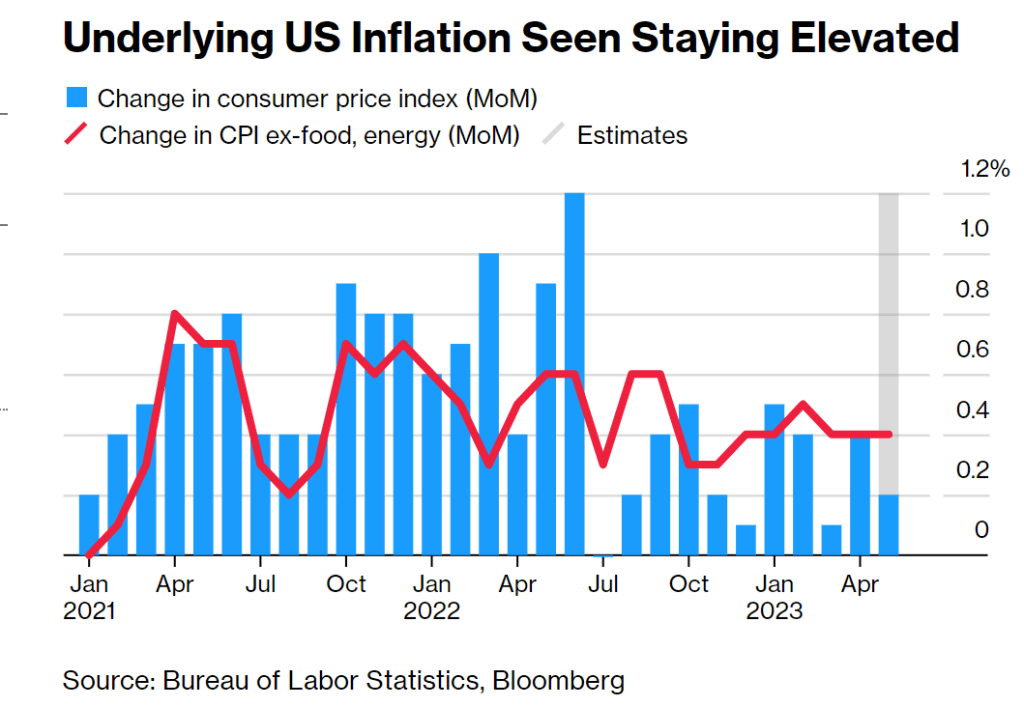

Tomorrow is the Federal government’s inflation report. As it stands today, overall inflation is slowing as M2 Money growth crashed. Core inflation remains persisitently high (white line), rent is still getting worse (orange dotted line at 8.1% YoY. What about food? Online food prices are up 8.2% YoY.

Shopping online is a good place to find cheaper computers and appliances, but grocery prices are still rising at a fast clip.

Prices of consumer goods sold online fell 2.3% in May in the US, the ninth consecutive month of declines and the biggest drop since the pandemic started, according to data from Adobe Inc. That was mainly due to steep decreases in discretionary categories.

Essential items like food, pet products and personal care, however, are seeing persistent inflation. Online grocery prices increased 8.2% from last year — although the pace of inflation has been abating since peaking at 14.3% last September.

Americans have been shifting more of their discretionary purchases to services over the past year, cutting spending on items for the home.

Online prices for appliances were down 7.9% in May from last year, the largest drop in digital-prices data from Adobe going back to 2014. Online prices for computers slumped 16.5% and electronics were down 12%.

The Adobe Digital Price Index was developed with the help of Austan Goolsbee before he became president of the Federal Reserve Bank of Chicago this year. The gauge analyzes one trillion visits to retail sites and more than 100 million items to track price changes.

Yes, Biden and Congress have levied a devastating tax on Americans. Rent and food are two of the largest household expenditures and they are up 8.1-8.,2% YoY.

Federal Reserve policymakers are about to take their first break from an interest-rate hiking campaign that started 15 months ago, even as they confront a resilient US economy and persistent inflation.

The Federal Open Market Committee on Wednesday is expected to maintain its benchmark lending rate at the 5%-5.25% range, marking the first skip after 10 consecutive increases going back to March of last year. While officials’ efforts have helped to reduce price pressures in the US economy, inflation remains well above their goal.

Source: Bureau of Labor Statistics, Bloomberg

Investors’ focus will be on the Fed’s quarterly dot plot in its Summary of Economic Projections, which is expected to show the policy benchmark rate at 5.1% at the end of 2023.

By contrast, markets are pricing in the possibility of a quarter-point hike in July followed by a similar-sized cut by December, and some Fed policymakers have emphasized that a pause in the hiking cycle shouldn’t be seen as the final increase.

Fed Chair Jerome Powell, who’ll hold a press conference after the meeting, has suggested he favors a break from hiking to assess the impact both of past moves and of recent banking failures on credit conditions and the economy. His commentary will be scrutinized for hints of the committee.

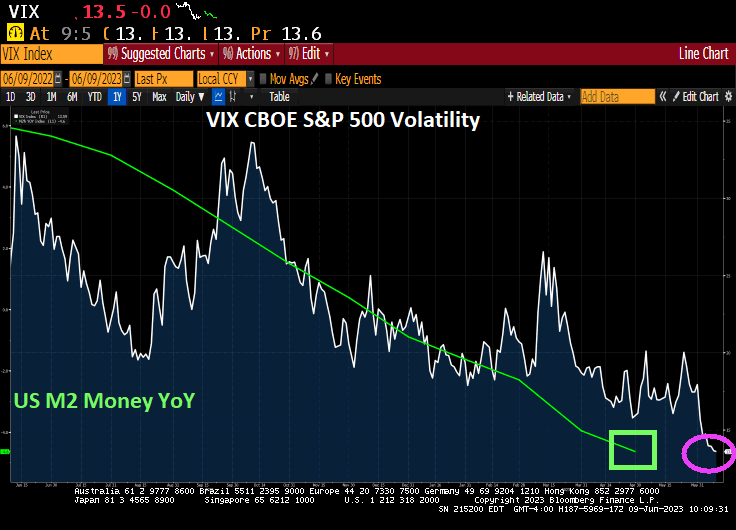

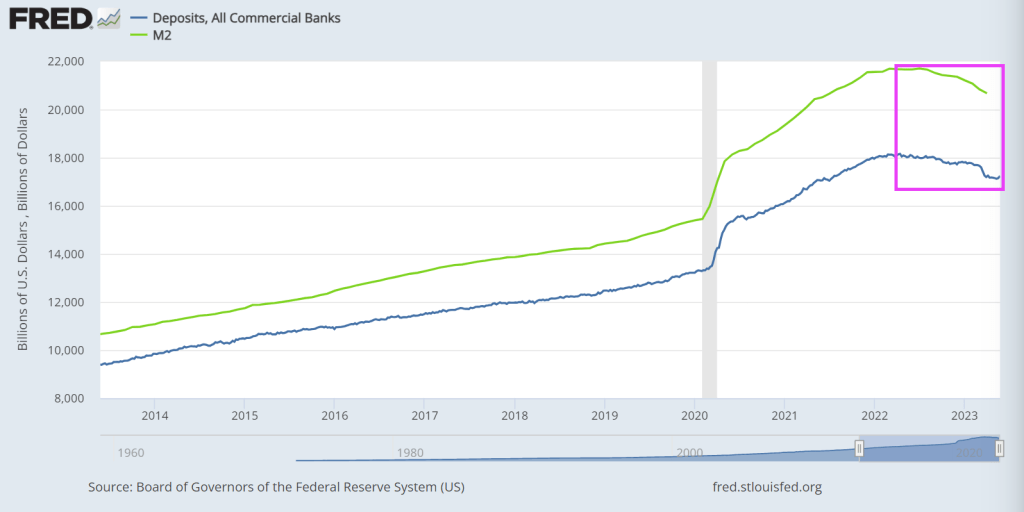

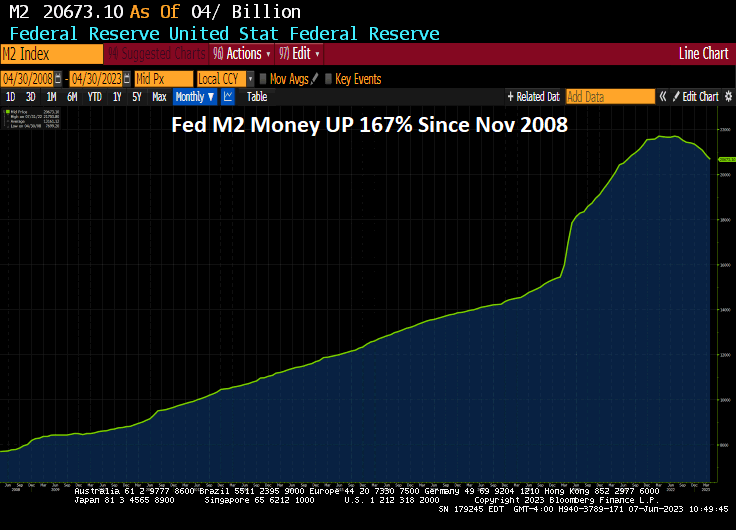

Remember, there is still over $8 TRILLION in Fed assets held sloshing around the economy. The Fed never really removed the excess liquidity and it continues to stoke asset bubbles.

Bear in mind that The Fed is pausing at 5.25% Fed Target Rate, while the Taylor Rule suggests rate hikes to 10.12%. So, Foul Powell is pausing at just over the half way mark.

Of course, Biden’s and Congress’ massive spending spree is causing inflation, and The Fed has no control over Biden/Congress irresponsible spending.

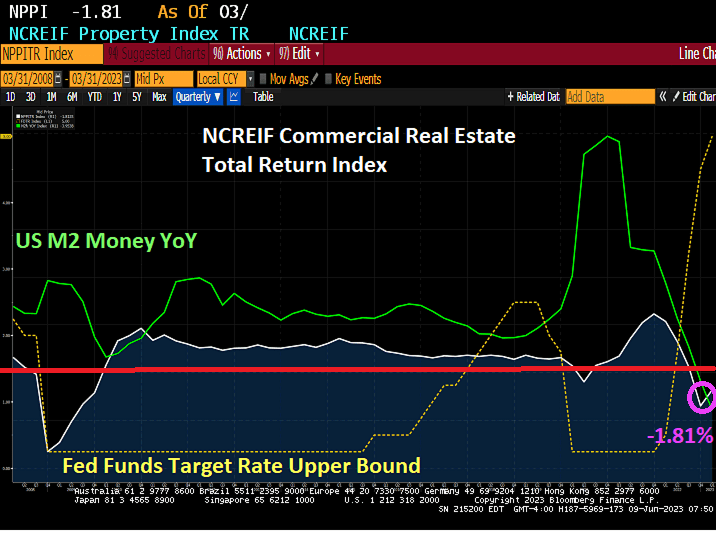

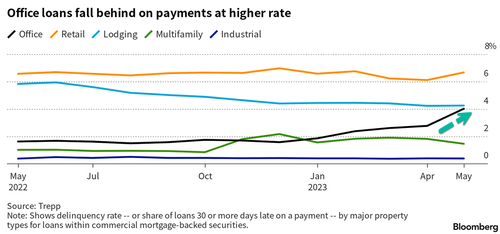

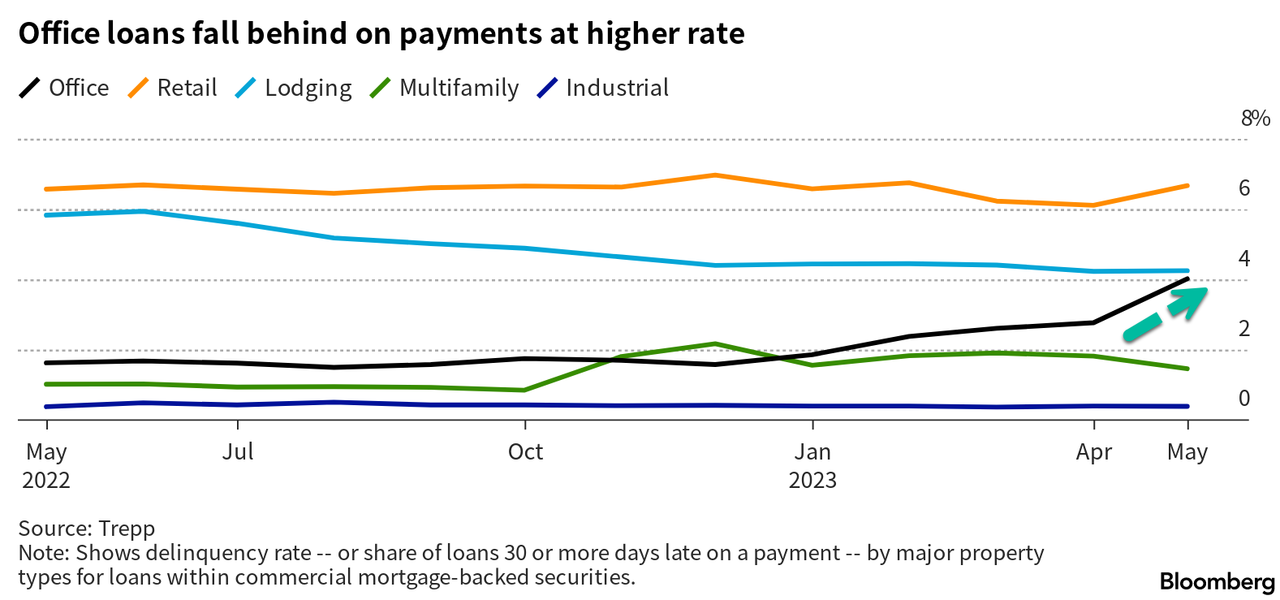

Some structural factors, such as remote work and hybrid work, have doomed the office space segment. This has left empty office buildings scattered across major US cities as the number of landlords falling behind on repayments due to the difficulty of refinancing and high vacancies has hit a five-year high.

According to real estate data firm Trepp, more than 4% of office loans packed into commercial mortgage-backed securities were delinquent in the last 30 days as of May, the highest level since 2018.

Dan McNamara, the founder of Polpo Capital Management, told Bloomberg about impending CRE turmoil:

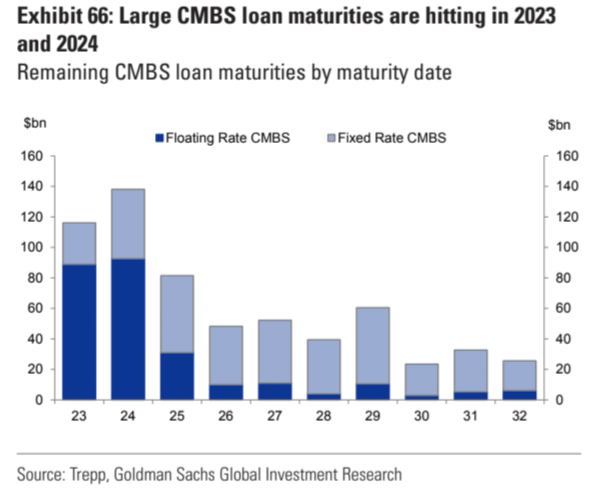

“This is just the tip of the iceberg for office delinquencies as $35 billion in CMBS office loans are scheduled to mature this year and the refinancing market is effectively shut to this asset class.”

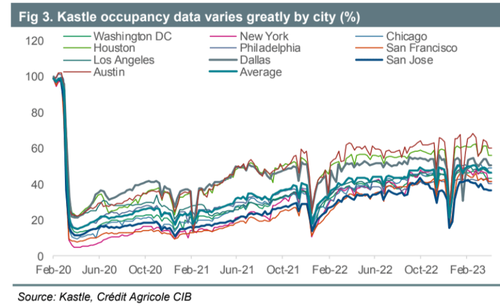

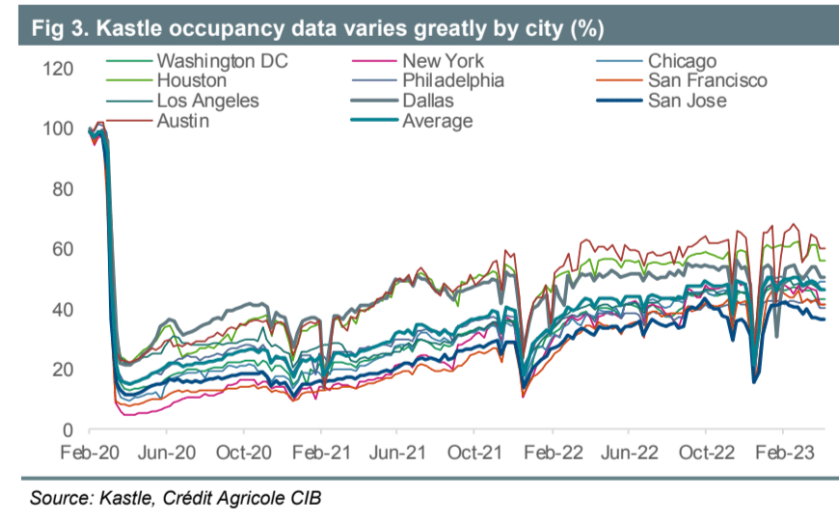

The rise in delinquencies comes as security card swipe data from Kastle shows many workers have yet to return to their desks in major US cities, resulting in high office space vacancies nationwide.

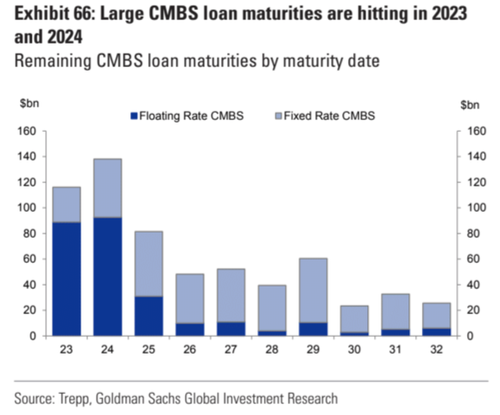

As Goldman pointed out to clients days ago, one major issue is a steep maturity wall of floating and fixed-rate CMBS loans due this year and next. The inability to refinance in these challenging market conditions will likely unleash a tidal wave of defaults in the second half of this year.

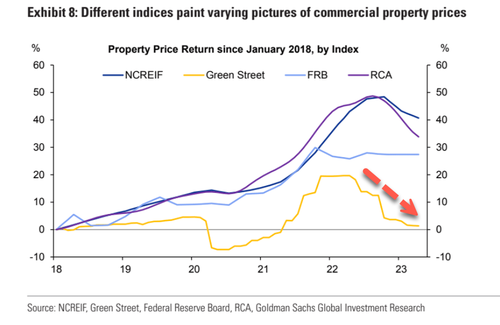

Goldman Sachs chief credit strategist Lotfi Karoui told clients last month, “the most accurate portrayal of current market conditions” is data via the Green Street Commercial Property Price Index, which suggests trouble ahead.

Just how much danger? Karoui believes “Green Street indicates a 25% year-over-year drop in office property values and a 21% drop in apartment property values.”

So the combination of high vacancies, sliding prices, and tightening lending standards is a perfect storm that could ignite an eruption of delinquencies in office loans in the coming quarters.

Treasury Secretary Janet “Too Low For Too Long” Yellen, and former Federal Reserve Chair, is partly responsible for a phenomenon plaguing America: the death of starter homes.

As Mish has discussed, with main markets no longer an option for first-time buyers, Point2 looked at the country’s 100 largest secondary cities for the median price of a starter home and renter households’ median income. Defined as large non-core cities within a metro, these cities used to be fruitful house-hunting grounds for first-time buyers exploring less-expensive options away from main cities. But as it turns out, unaffordability can put a dent in homeownership plans regardless of city type or size.

In 41 of the 100 largest secondary cities in the U.S., renters earn half or less than half of the income they would need to buy a median-priced starter home.

There are no non-core cities in which renters could comfortably make a move toward homeownership: In 10 cities, the necessary income is about triple what they earn.

Would-be buyers in Burbank and Glendale, CA have it worst: They lack 67% of the income they would need in order to make the move from renter to homeowner.

Renters in 9 California cities would need to earn about $100,000 more in order to afford a starter home. Based on the latest renter income figures, starter home prices, and mortgage rates, non-core cities in the LA and San Diego metros are the toughest for first-time homebuyers.

In 15 of the 100 largest secondary cities, renters would need less than 4 months’ worth of extra income to afford the transition to owning a starter home.

Homeownership is within reach in Independence, MO, and Broken Arrow, OK. Those who dream of owning here would need less than one month’s worth of extra income to afford a starter home.

California Tops the List of Worst Places to Look

California has the dubious distinction of having the top least affordable starter home cities.

A starter home, according to the Census Department is priced in the bottom third of homes in the area.

Pomona, CA, is in fourteenth place. The average renter in Pomona makes $49,000 a year and needs to get to $121,000 a year. That’s nearly 2.5 times current salary.

In Burbank, CA, the average renter makes $63,000 year an needs to get to $193,000. That’s over 3 times current salary.

Within Grasp

In no market can the average renter make the plunge.

But in Independence, Missouri, or Broken Arrow, Oklahoma, the average renter is respectively just 2% and 5% short of the amount needed for a starter home

Not Shocking

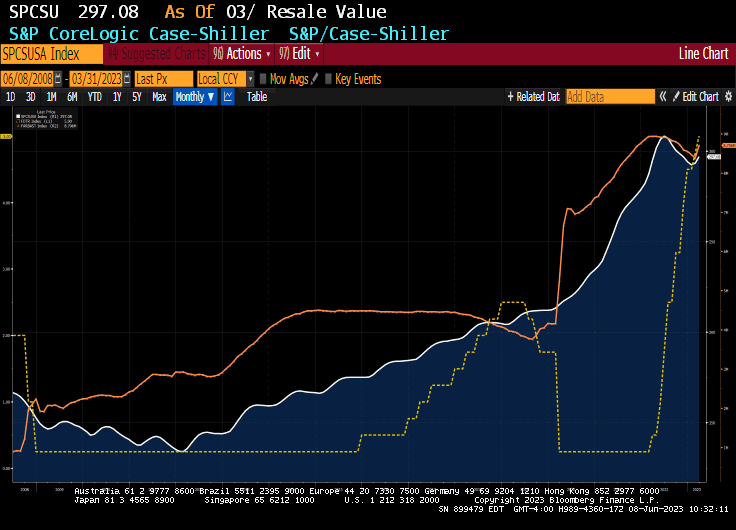

None of this is shocking. It matches one one should expect looking at Case-Shiller home prices and mortgage rates.

The Fed wanted to produce inflation and it did. But for years the Fed did not even see the inflation because the manifestation of inflation was in asset prices, not the price of consumer goods.

Case-Shiller Top City Home Prices Decline From Year Ago for the First Time Since May 2012

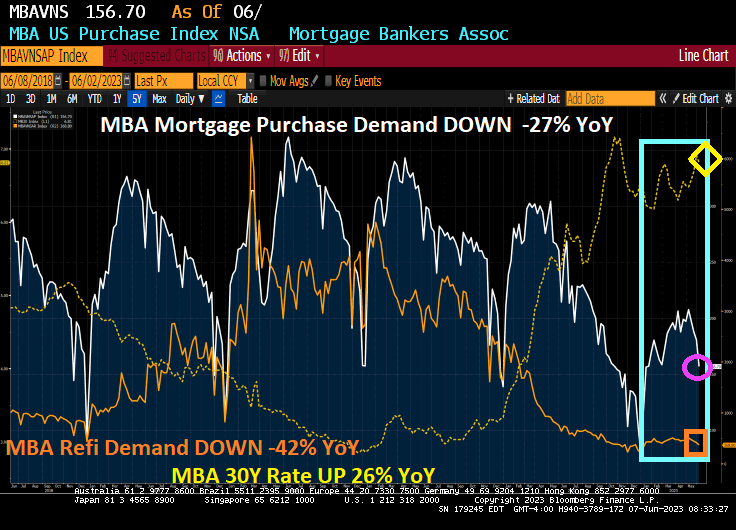

Housing starts, like mortgage purchase demand, remains depressed compared to the housing bubble of the 2000s.

Now, will The anticipated Fed pause in rate hiking help? Not likely. The Fed still has over $8 trillion in monetary stimulus chasing assets. Too much Stimulypto.

One has to wonder about The Feral Reserve. Since The Great Recession of 2008, The Federal Reserve has printed a staggering amount of money (know as QE). There is still about $8.3 TRILLION in monetary stimulus sloshing around the economy.

And M2 Money printing is up 167% since November 2008.

So, despite the talking heads from The Fed and CNBC, etc blathering about Fed tightening, there remains over $8 TRILLION in monetary stimulus chasing asset prices.

Is The Fed ACTUALLY the US economy? Or is The Fed the financing arm of the Democrat party?

Yes, The Fed looks like they are pausing .. rate hikes.

Welcome to the Bidenville Mortgage Depot! Where Bidenflation (caused by idiotic energy policies, crazy Fed money printing and insane Federal spending) has caused The Fed to raise rates crushing the US mortgage market.

Mortgage applications decreased 1.4 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending June 2, 2023. This week’s results include an adjustment for the Memorial Day holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.4 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 12 percent compared with the previous week. The Refinance Index decreased 1 percent from the previous week and was 42 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 13 percent compared with the previous week and was 27 percent lower than the same week one year ago.

The rest of the story.

The East Palestine Ohio train wreck is symbolic of Biden’s economic programs. I don’t think the Vacationer in Chief (40% of time as President has been on vacation) has been there yet.

But it isn’t just San Francisco. Phil Hall reports that Fitch Ratings reduced its 2023 outlook for the U.S. real estate investment trust (REIT) sector outlook from “Neutral” to “Deteriorating,” citing the tumult in the commercial real estate space.

While Fitch noted that most of its rated REITs “have the capacity to withstand such a slowdown within rating sensitivities [and] those with ample dry powder could capitalize on distressed property sales by weaker capitalized players.” But at the same time, the ratings agency warned that banks – which account for nearly half of the $5.5 trillion commercial mortgage market – saw their lending levels drop by 20% between February and April, with more tightening expected.

“At minimum, this will lead to further contractions in CRE credit, further limiting conditions for property transactions,” Fitch added in its announcement of the outlook reduction, adding that “CRE transaction volume has steadily declined since early 2022 due to the confluence of operating fundamentals pressure, higher interest and capitalization rates, limited buyer financing, and looming recession risk. The rapid jump in rates has resulted in unusually wide value discrepancies between buyers and sellers across most property types and markets, particularly in the struggling office sector. Our forward-looking U.S. equity REIT ratings incorporate assumptions about future property disposition volumes and valuations.”

Fitch predicted the U.S. economy will go into a recession, most likely late in the year – a previous forecast put the downturn at mid-year – and forecasted property performances will vary by sector over the next two years.

“Sectors experiencing strong fundamentals, such as industrial and shopping centers, will likely see some cooling in demand, with tenants showing greater reluctance to lease space, including delaying decisions, resulting in less pricing power for landlords,” Fitch continued. “Tighter lending conditions and weaker economic growth will add to the secular pressures facing some property formats (e.g. office, enclosed malls). The office REIT sector has met, or modestly underperformed, our low expectations during 2023. Leasing volumes have generally underperformed as occupiers add the business cycle to the list concerns and reasons for conservatism, along with secular pressure from remote work. Conversely, the industrial sector, although no longer white hot, continues to deliver above average occupancies and outsized rent growth that have modestly exceeded our projections.”

While Fitch stressed that REITs were “unlikely to directly encounter meaningful stress” based on the recent problems in the banking industry, although it also acknowledged that it did not expect “REITs’ access to unsecured revolvers will be impeded, although facilities up for renewal will likely see higher pricing and some banks have reduced appetites for traditional bank syndicate activities, such as making funded term loans – particularly in hard hit sectors, such as office. We also do not expect meaningful portfolio vacancies caused by bank tenant failures, which are unlikely to be widespread.”

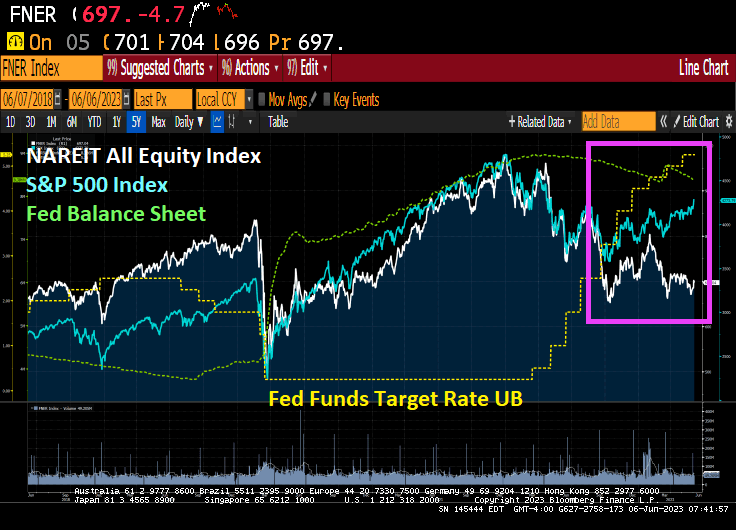

The NAREIT All-equity index has gotten pummelled by the S&P 500 index since The Fed started tightening monetary policy to fight inflation …. that The Fed helped cause in the first place.

Under Biden, the US is beginning to morph into a lawless Socialist sewer like Venezuela. Joe Maduro??

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.