The Covid outbreak in early 2020 (from which I came close to dying) resulted in legendary Fed stimulus and Federal government spending. But as The Fed attempts to cool inflation by slowing M2 Money printing and raising The Fed’s target rate, we are seeing the lowest personal consumption expenditures print under Biden’s reign of error, a measly 1%.

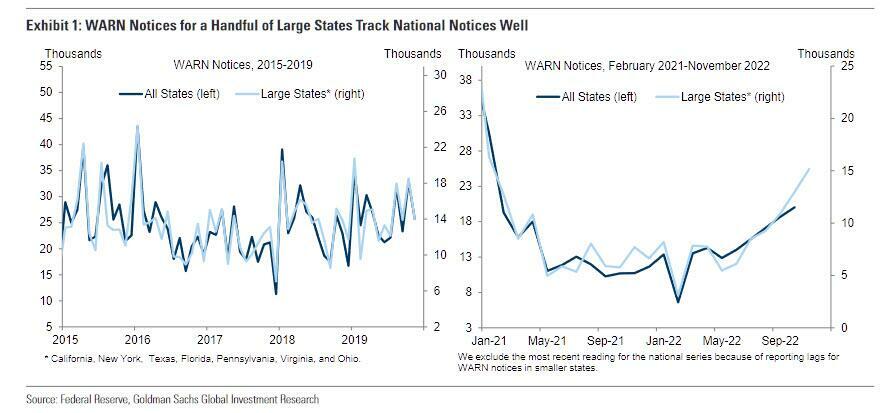

On top of the dismal revision to the Q4, we are seeing WARN notices increasing, particularly for large states. Worker Adjustment and Retraining (WARN) Notices are picking up which points to unemployment claims soon rising and a deterioration in the jobs market, posing a risk to stocks.

Biden’s reign of error continues with horrible policies. With the help of Congress.

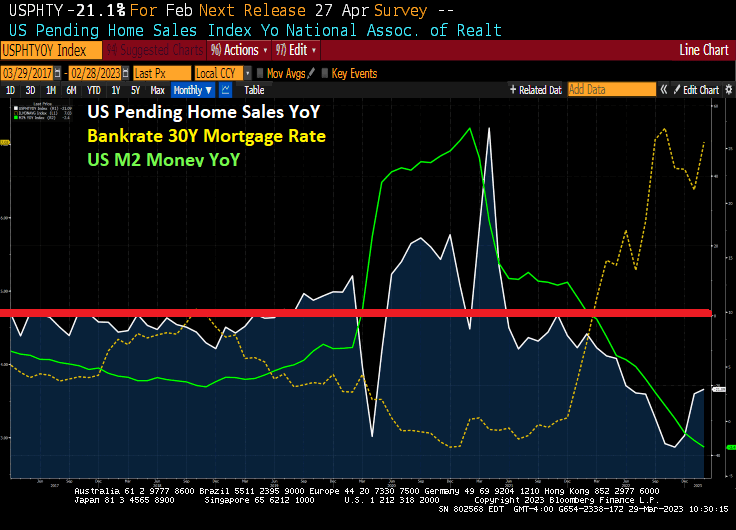

Pending home sales grew in February for the third consecutive month, according to the National Association of REALTORS®. Three U.S. regions posted monthly gains, while the West declined. All four regions saw year-over-year decreases in transactions.

The Pending Home Sales Index (PHSI)* — a forward-looking indicator of home sales based on contract signings — improved 0.8% to 83.2 in February. Year-over-year, pending transactions dropped by 21.1%. An index of 100 is equal to the level of contract activity in 2001.

More notably, the YoY growth rate has been NEGATIVE for 20 of the last 21 months. And 15 straight months.

Biden’s energy policies + insane Federal spending = inflation = Fed slowing M2 Money growth. Hence, pending home sales YoY is down -21.1%.

Well, the regional banking crisis has one positive outcome: mortgage rates dropped -46 basis points since last week. The result? Mortgage demand increased 2.9 percent week-over-week (WoW). Although I don’t recommend banking incompetence by bank management and “regulators” as a strategy to increase mortgage demand.

Mortgage applications increased 2.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 24, 2023.

The Market Composite Index, a measure of mortgage loan application volume, increased 2.9 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 3 percent compared with the previous week. The Refinance Index increased 5 percent from the previous week and was 61 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 2 percent from one week earlier. The unadjusted Purchase Index increased 2 percent compared with the previous week and was 35 percent lower than the same week one year ago.

The rest of the story.

We need a doctor to fix this mess, just not Dr. Yellen or Dr. Jill.

The US economy got beaten to a pulp by the Chinese Wuhan Covid virus outbreak in early 2020. The Fed intervened with massive money printing along with massive spending by Congress and the Administration. Result? 40-year highs in inflation and a Fed counterattack in terms of rate hikes.

The result of Fed rate hikes? Failing regional banks trying to cope with duration extention and scared depositors. And then we have the St Louis Fed Financial Stress index reaching its highest level since the Covid outbreak of early 2020. And with that, bond volatility is higher than that found during the Covid crisis.

With the expectation of MORE rate hikes, the 10-year Treasury yield jumped 12 basis points.

The architect of The Fed’s “too long for too long” is also the US Treasury Secretary, Janet Yellen.

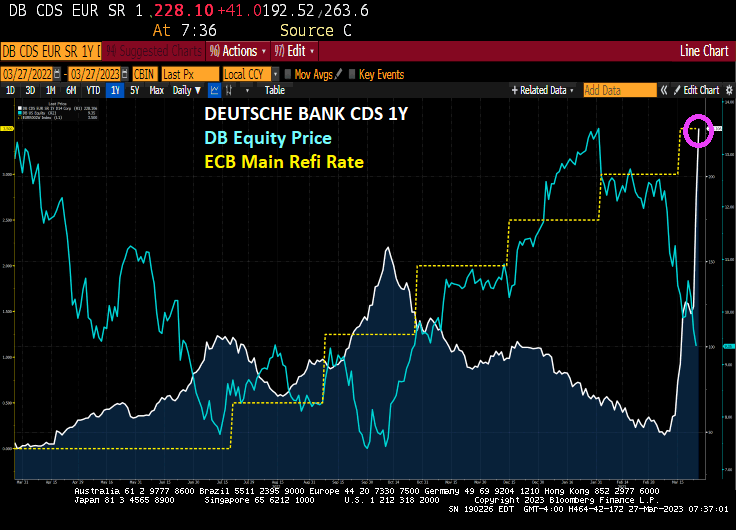

Are central banks like The Federal Reserve and European Central Bank ({ECB) sinking the banks?

Deutsche Bank, Germany’s largest bank (eerily like Germany’s World War II battleship The Bismarck) is seeing a blow out in its 1-year credit default swaps (CDS) as the ECB cranks up it main refinancing rate to fight inflation.

And then we have Deutsche’s Banks gross notional derivatives exposure (Euro 55.6 TRILLLION) dwarfing German GDP (Euro 2.7 Trillion). By a factor of greater than 20! Now, THAT’S a lot of derivatives exposure.

On the bond front (the NEW eastern front), we see the US Treasury 2-year yield rising 17.1 basis points. But European sovereign yields are up double digits as well (except for Italy).

As The Fed attempts to fight inflation, rates are rising. Consequently, deposits are all commercial banks are falling.

The Fed just released its weekly commercial bank data dump showing deposit inflows/outflows.

Two things to note:

1) This is for the week up to 3/15/23 (which includes the SVB collapse but nothing more)

2) ‘Large Banks’ includes the top 25 banks (which means SVB was among that group, hence, we get no indication of SVB rotation flows)

The overall data shows that domestic commercial banks saw over $98 billion in deposit outflows (seasonally-adjusted) that week to just over $17.5 trillion (8th straight week of aggregate outflows).

Source: Bloomberg

That is the largest (seasonally-adjusted) outflow since April 2022 (tax-related?) as we suspect much of that flowed into money-markets. Deposits have been on a steady decline over the past year or so, falling $582.4 billion since February 2022.

There was a notable rotation however with the large banks seeing deposit inflows of $117.9 billion on a non-seasonally-adjusted basis (the biggest weekly inflow since Dec 2021).

Small banks, on the hand, saw a massive $111 billion outflow (non-seasonally-adjusted)…

Source: Bloomberg (note different scales)

That is the largest weekly outflow ever (by multiples) and drops ‘small bank’ total deposits to the lowest since Sept 2021…

Source: Bloomberg

Bear in mind this data does not include the last 10 days, where we have US regional banks all tumbling further and Yellen offering no guaranteed deposits, FRC stock collapse amid bailouts (though that will skew the data due to that $30bn infusion), and the fear of Credit Suisse’s collapse.

Will banks start to compete for deposits? (Well not the biggest ones, for sure)…

The Federal Reserve never died. In fact, The Fed is growing its balance sheet again. Why? A slowing economy and weakness in the banking sector (thanks to inflation and the Fed trying to get inflation back to 2%.

And the banking fiasco keeps rolling, particularly in Europe where Credit Suisse has been in the news for failing and now my former employer, Deutsche Bank (aka, The Teutonic Titanic).

Deutsche Bank AG became the latest focus of the banking turmoil in Europe as ongoing concern about the industry sent its shares slumping the most in three years and the cost of insuring against default rising.

The bank, which has staged a recovery in recent years after a series of crises, said Friday it will redeem a tier 2 subordinated bond early. Such moves are usually intended to give investors confidence in the strength of the balance sheet, though the share price reaction suggests the message isn’t getting through.

“It is a clear case of the market selling first and asking questions later,” said Paul de la Baume, senior market strategist at FlowBank SA. “Traders do not have the risk appetite to hold positions through the weekend, given the banking risk and what happened last week with Credit Suisse and regulators.”

Deutsche Bank slumped as much as 15%, the biggest decline since the early days of the pandemic in March 2020. It was the worst performer in an index of European bank stocks, which fell as much as 5.7%. Crosstown rival Commerzbank AG, Spain’s Banco de Sabadell SA and France’s Societe Generale SA also saw steep drops.

The widespread declines undermine hopes among authorities that the rescue of Credit Suisse Group AG last weekend would stabilize the broader sector. Central banks from the Federal Reserve to the Bank of England this week raised interest rates once again, keeping their focus on inflation amid hopes that the worst of the financial turmoil was past.

All week, regulators and company executives have sought to reassure traders about the health of the banking industry. Deutsche Bank management board member Fabrizio Campelli said Thursday that the government-brokered takeover of Credit Suisse by UBS is “no indication” of the state of European banks.

Standard Chartered Plc Chief Executive Bill Winters said Friday that while there are still some issues to be addressed, “it seems that the acute phase of the crisis is done.”

The latest moves in Europe follow losses in US banks, which tumbled Thursday even after Treasury Secretary Janet Yellen told lawmakers that regulators would be prepared for further steps to protect deposits if needed.

And apparently bank bailouts never died. They just got relabeled.

And on growing banking fears, the 10-year Treasury yield is down -11.7 basis points.

You must be logged in to post a comment.