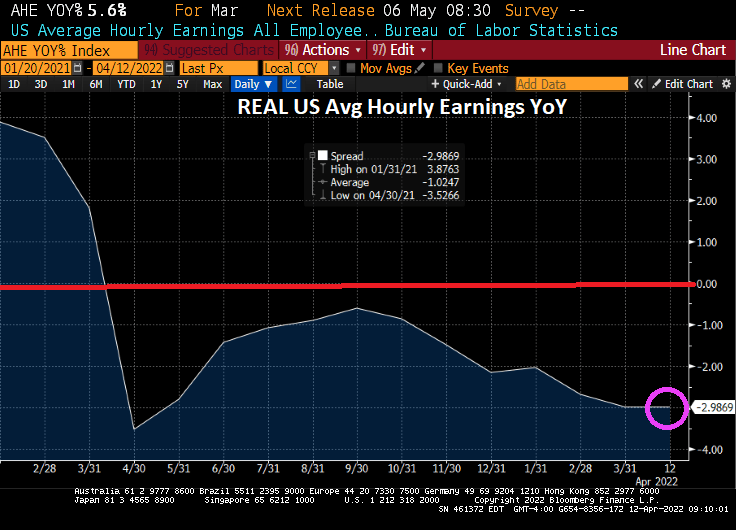

US real average weekly earnings growth YoY is down to -3.60%. That is the lowest since 2007 and is worse than The Great Recession and financial crisis of 2008.

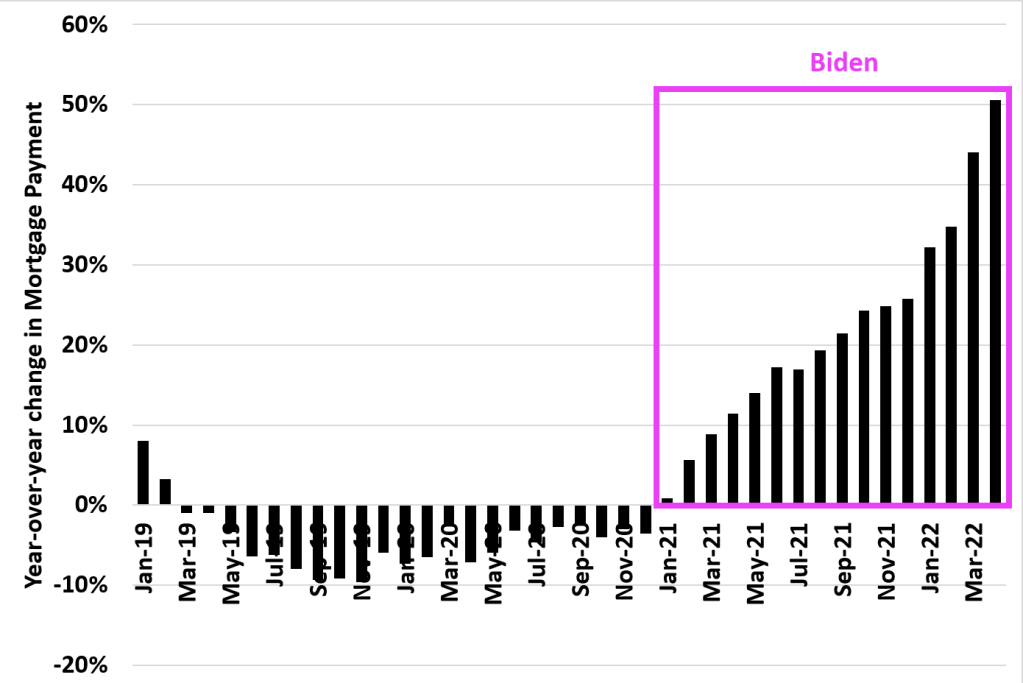

And look at this chart of mortgage payments under Biden. The US was actually experiencing DECLINING mortgage payments YoY in 2019 and 2020. But under Biden’s leadership, mortgage payments have increased by 50% making housing even MORE unaffordable for the middle class and lower-income households.

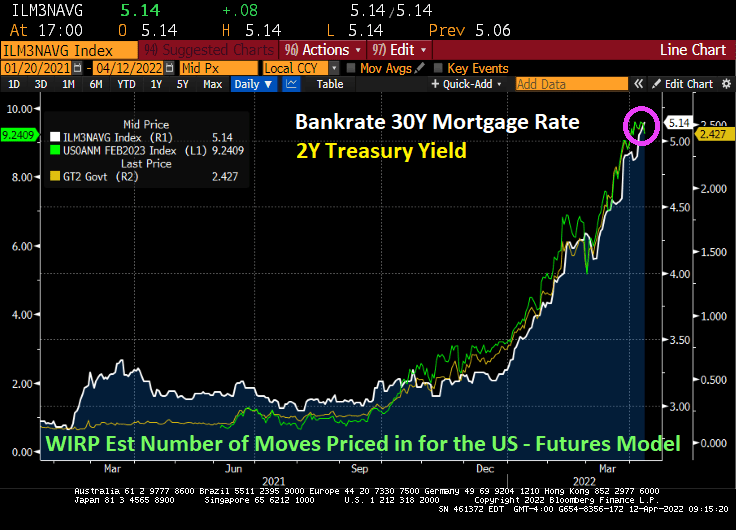

And now for something kind of scary. The US today suffered a 12 basis point decline in the 2-year Treasury yield, generally a bad sign for the economy. As if we needed more bad news for today.

Highest inflation in 40 years, worst wage growth since 2007 and rising mortgage payments. We will need all the luck we can get.

With 8.5% YoY inflation, REAL average hourly earnings growth fell to -3% YoY.

And with The Fed intent on extinguishing their part of the inflation, Bankrate’s 30Y mortgage rate rose to 5.14%.

Energy is the biggest culprit (fuel oil up 70.1% YoY) thanks to the double whammy of 1) Russia’s invasion of Ukraine and 2) Biden’s restrictions on oil and natural gas production. Food at home is up 10% YoY.

Here is a colorful chart of MoM growth in prices.

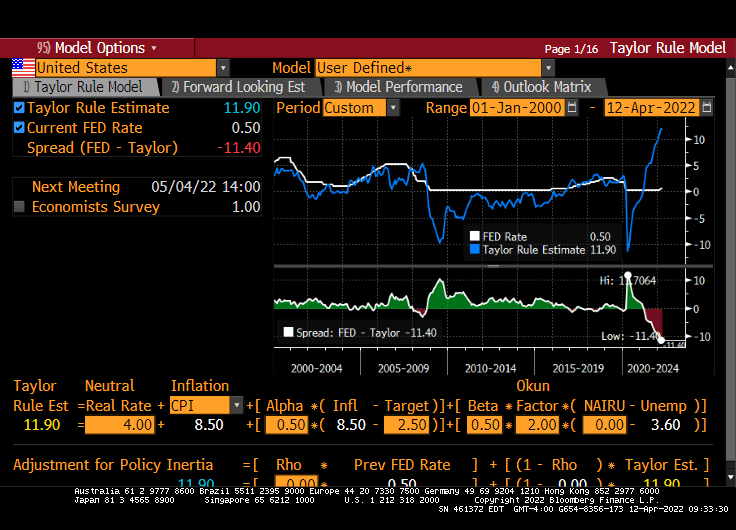

The Taylor Rule model now says that The Fed Funds Target Rate should be 11.90%. Hence, Fed Stimulypto is still in place with the signal that rates will increase.

How about WTI Crude and Brent Crude soaring over 4% today?

Once again, the Four Horsemen of the Inflation Apocalypse (Biden, Powell, Pelosi, Schumer) overstimulated the economy and financial markets with excessive monetary stimulus (Powell) and excessive Federal spending (Biden, Pelosi, Schumer) where demand soared for products and supply naturally hasn’t caught up.

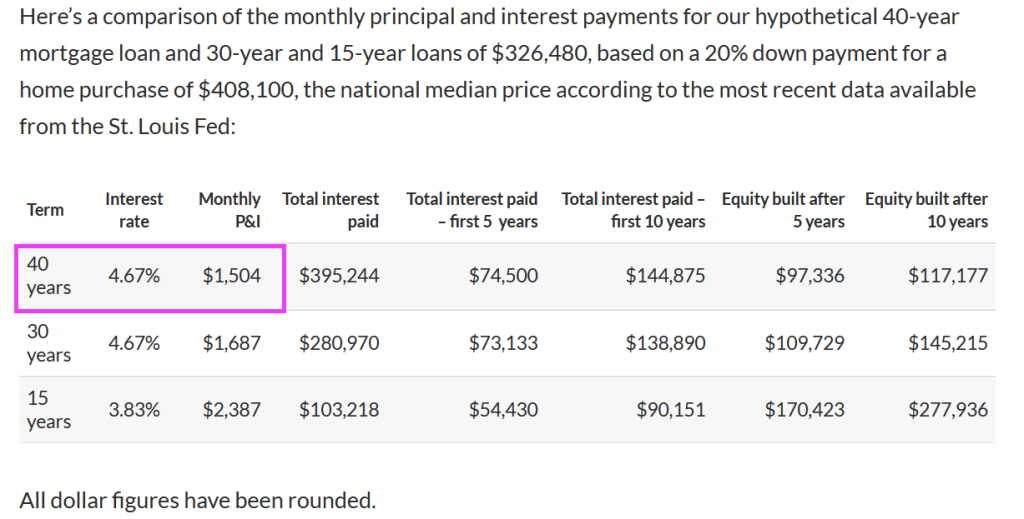

To make a long story short, a 40-year mortgage, by stretching the payment out from 30 to 40 years, means that the mortgage mortgage payment declines from $1,687 to $1,504.

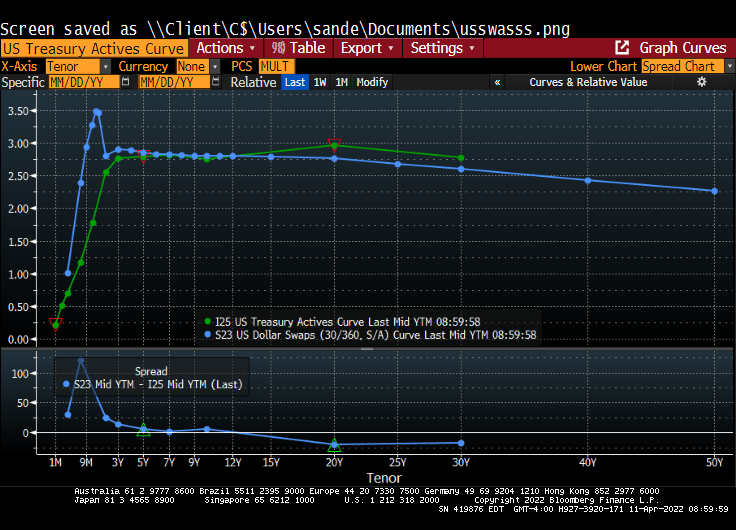

Given that the US Treasury yield curve only goes out to 30 years, lenders (and Fannie Mae and Freddie Mac) will have to use the US Dollar Swaps curve to price mortgages. And since the swaps curve is downward sloping, we could see 50-year mortgages at a lower rate than 30-year mortgages, ceteris paribus.

But with The Fed planning on taking away the monetary punchbowl, mortgage rates are rising making housing even more unaffordable.

But most things are not equal. The 40-year mortgage results in a slower paydown of the mortgage, increasing the lender’s exposure to property value declines. A 50-year mortgage would even be worse.

But the real problem with the 40-year mortgage is that it can lead to even MORE unaffordable housing. Yes, going from 30-year to 40-year mortgages lowers the mortgage payment, but a 40-year mortgage could increase the demand for housing. And since we already have soaring home prices since Covid (thanks to Fed monetary policy AND Federal government stimulus), we could actually see a worsening of the housing bubble). Particularly since REAL average earnings are declining.

What a mess that has been created by the government’s pursuit of “affordable housing.” Ideally, the Federal government could help raise household earnings through lowering of Federal tax rates, but the Biden Administration wants to raise taxes. Alternatively, lenders (and Fannie Mae and Freddie Mac) could lower lending standards (e.g., lowering required credit scores), or reduce downpayments to 0%. Lowering credit standards and reducing required downpayments are also inflationary and pose serious potential problems with default risk.

Not to mention that a 40-year mortgage increases the duration risk for owner’s of the 40-year mortgage.

And don’t forget that local governments frown on multifamily (apartment) construction (the Not In My Backyard [NIMBY] problem contributing to rising housing prices.

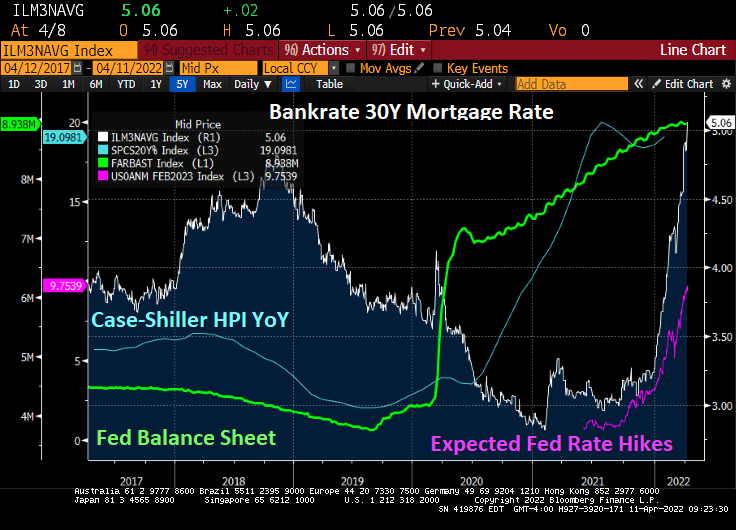

As the US Treasury 2-year yield hits 2.507% (up from 0.128% when Biden was installed as President) and the number of Fed rate hikes over by February 2023 hits 9.6, Bankrate’s 30-year mortgage rate breached the 5% mark at 5.04%.

The most recent data from on existing home sales show YoY sales in negative territory as The Fed begins in monetary fireball tightening.

St Louis Fed’s Bullard said The Fed is “behind the curve.” Ya think??

The Fed’s minutes from the most recent meeting indicates that The Fed will shedding $95 billion a month from it swollen balance sheet. At almost $9 trillion mostly populated by Treasuries will be the first asset to run-off the balance sheet (there is almost $1 trillion of Treasuries maturing in 2022 and $856 billion maturity in 2023, etc), The Fed plans to shrink the balance sheet while, at the same, raising The Fed Funds target rate from it near zero levels.

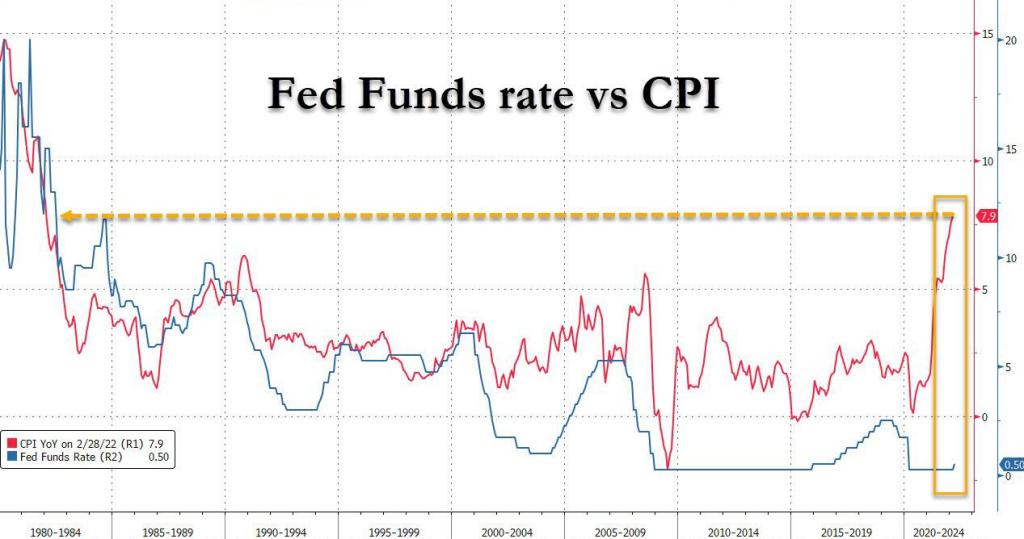

The Federal Reserve has ignoring rules like the Taylor Rule since the financial crisis of 2008-2009, but seemingly are paying attention to the Taylor Rule because of 7.9% inflation. The Taylor Rule is suggesting a 20.42% Fed Funds target while the current target rate is 0.50%. Now THAT would be a real shock to the economy.

Well, the US have gone from “fastest economic recovery in history” to real GDP growth of less than 1% (Atlanta Fed GDPNow for Q1). In addition, the flexible price CPI less food and energy is a whopping 20%.

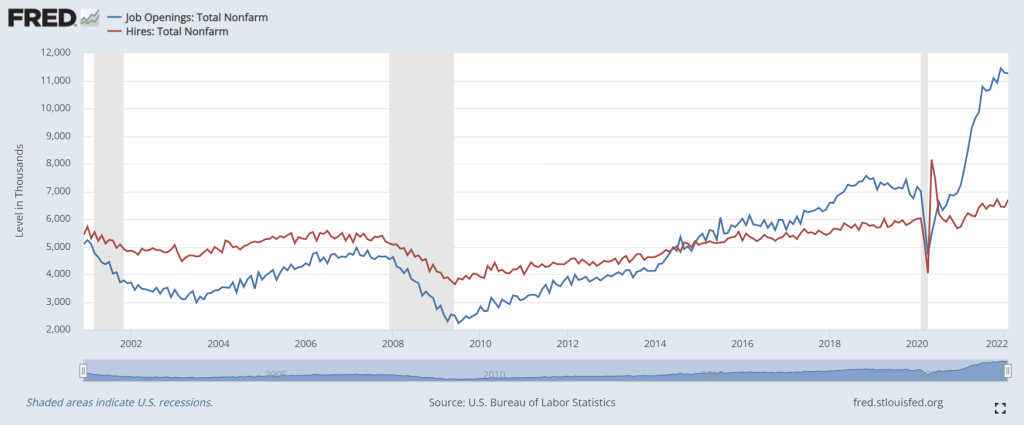

You can see “The Biden Miracle!” in the following chart. Hires (red line) dropped with Covid shutdowns, then spiked when governments opened economies again. Throw in the trillions of Federal government Covid stimulus and trillions in Fed monetary support, the Biden Miracle sees less like a miracle and more like an extremely expensive way to add jobs. But the interesting problem facing the Administration is the massive spike in job openings relative to hires (again, governments opening-up plus Federal Stimulypto).

Now for a real downer of a chart. Inflation is so toxic that REAL average hourly earnings YoY is down -2.72%. Hardly the best economic growth in history.

Now we have Jerome Powell and The Blackhearts threatening quantitative tightening starting in May. Here is The Fed’s theme song “We love printing money.”

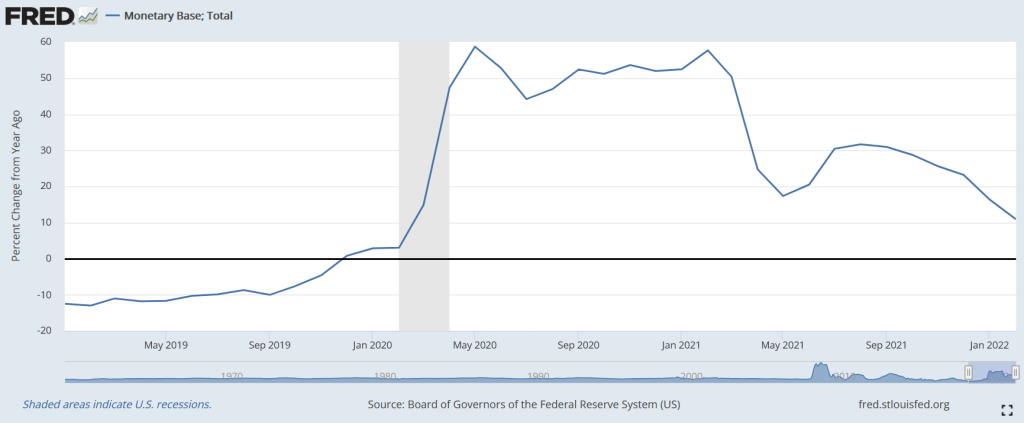

But The Fed is already slowing the growth of monetary base, although this Fed Stimulypto is still growing much faster than pre-Covid.

At least the 10Y-2Y Treasury curve is back above 0 bps as the Atlanta Fed’s GDPNow Q1 forecast falls to under 1%.

Remember, The Fed is planning on shrinking the balance sheet by $95 billion. The Fed’s balance sheet is just shy of $9 trillion. Which is around 1% per month.

With rising expectations of Fed quantitative tightening (QT), residential mortgage rates keep climbing.

Despite a slowing economy teetering on recession and a war raging in Europe, The Fed is tightening monetary policy. Allegedly to fight red-hot inflation.

Stablecoin refers to a new class of cryptocurrencies which offer price stability and/or are backed by reserve asset. In recent times, stablecoins have gained enough traction as they attempt to offer the best of both world’s – the instant processing and security of payments of cryptocurrencies, and the volatility-free stable valuations of fiat currencies.

US Senator Pat Toomey, ranking member of the Banking, Housing and Urban Affairs Committee, announced today legislation to create a responsible regulatory framework for STABLECOINS.

Toomey Announces Legislation to Create Responsible Regulatory Framework for Stablecoins Releases Discussion Draft of the Stablecoin TRUST Act

Washington, D.C. – U.S. Senate Banking Committee Ranking Member Pat Toomey (R-Pa.) today released a discussion draft of legislation establishing a new regulatory framework for payment stablecoins.

“While today stablecoins facilitate trading with cryptocurrencies, tomorrow stablecoins could be widely used in the physical economy. They have the potential, among other things, to speed up payments and automate transactions,” said Ranking Member Toomey. “The proposed regulatory framework I’m releasing today will allow this crypto-innovation to continue flourishing while protecting consumers and minimizing potential risks from stablecoins to the financial system. I look forward to receiving feedback on this legislation from my colleagues and stakeholders as Congress continues its work on stablecoin regulation.”

Key Components

· Authorizes three different options to issue payment stablecoins:

o Establishes a new federal license designed specifically for stablecoin issuers;

o Preserves the state-registered money transmitter status for most existing stablecoin issuers; and

o Clarifies that insured depository institutions are permitted to issue stablecoins.

· Protects consumers by subjecting all payment stablecoin issuers—regardless of whether they are a state money transmitter or receiving a new federal license—to standardized requirements, including:

o Disclosures regarding the reserve assets backing the stablecoin;

o Clear redemption policies; and

o Subjecting them to routine audits by registered public accounting firms.

· Provides much-needed clarity that, at a minimum, stablecoins that do not offer interest are not securities.

o Provides a clear regulatory framework for payment stablecoins and rejects the Securities and Exchange Commission’s approach of regulating through enforcement actions.

· Applies privacy protections to transactions involving stablecoins and other virtual currencies.

Background

· In August 2021, Ranking Member Toomey announced he was soliciting legislative proposals to ensure federal law supports the development of digital assets and its underlying technologies while protecting investors.

· In December 2021, Ranking Member Toomey released a set of principles to lay the framework for forthcoming stablecoin legislation.

Crytpos in general are having a bad day, with Bitcoin down 4.78% today and Ethereum Classic down 12%.

Toomey’s proposal is a great step forward in the regulation of stablecoin.

The 10-year Treasury term premium, the amount by which the yield on a long-term bond is greater than the yield on shorter-term bonds, remains steeply negative (white line) as The Federal Reserve steps up its attack (aka, monetary tightening). Meanwhile, the 10Y-2Y curve actually rose into positive territory.

Historically, the 10-year Treasury Term Premium declines before a recession.

Meanwhile, 3 month Treasury bill to Overnight Indexed Swaps spread is crashing to the lowest level since 2017.

But with inflation raging at the fastest pace in 40 years, the REAL 10-year Treasury yield remains negative at -5.236% while the REAL 30-year mortgage rate is -3.01%. Both were in positive territory when Biden was installed as President.

Speaking of interest rates, the infamous PIGS (Portugal, Italy, Greece, Spain) are all seeing surges in their 10-year sovereign yields. Sweden, while not a PIG has the largest spike today at 13.8 BPS.

Actually, the biggest spike in sovereign yields occurred in Ukraine where their 2-year yield popped +205.8 BPS. But Lebanon has the highest 2-year yield at 162.29%. Turkey is in third place in the sovereign demolition derby at 23.52%. Sadly, Poland’s 2-year yield is up 16 bps today.

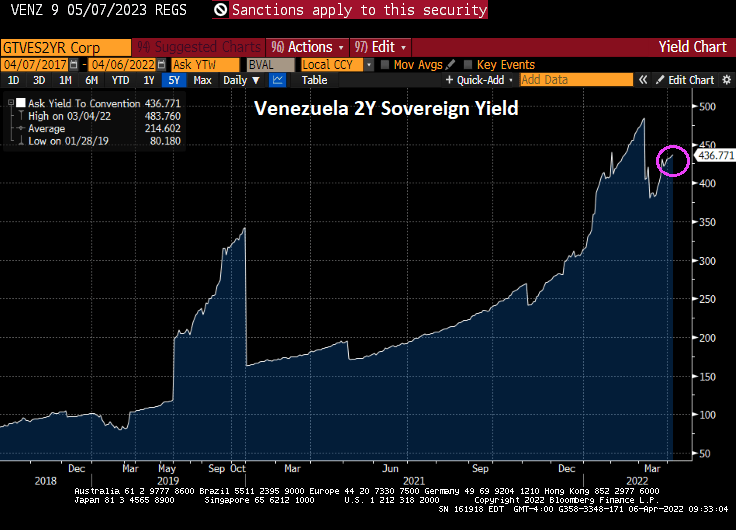

But the winner of the sovereign debt demolition derby is …. drumroll … VENEZUELA! At 436.77%.

I am really surprised that Biden hasn’t adopted Maduro’s fashion sense.

Federal Reserve Governor Lael Brainard said the U.S. central bank will continue to tighten policy methodically and shrink its balance sheet at a rapid pace as soon as May.

Brainard’s hawkish remarks sent bond prices crashing and 10Y bond yields up over 16 bps.

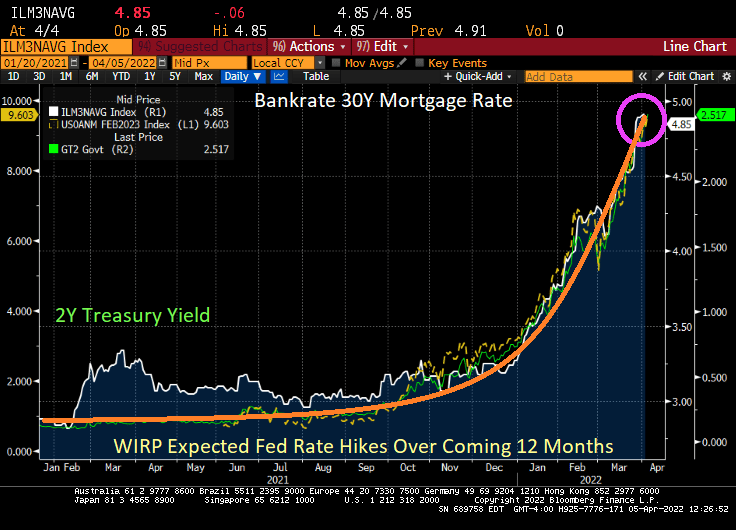

While Bankrate’s 30Y mortgage rate is down slightly today, the surge in the 10Y and 2Y Treasury yields could push mortgage rates above 5% by tomorrow,

Even Europe is feeling Brainard’s wrath. Italian 10Y sovereign yields are up almost 20 bps.

The NASDAQ index is down 300 points on Brainard’s utterance.

Gee thanks Lael from all us wanting to finance the purchase of a house.

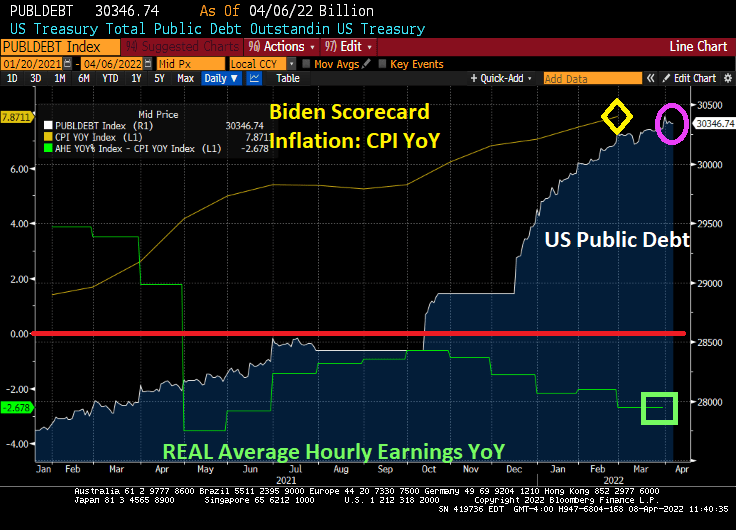

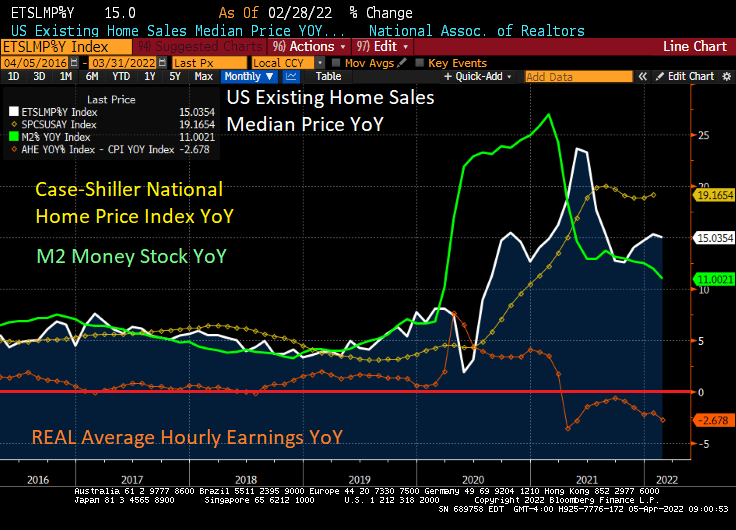

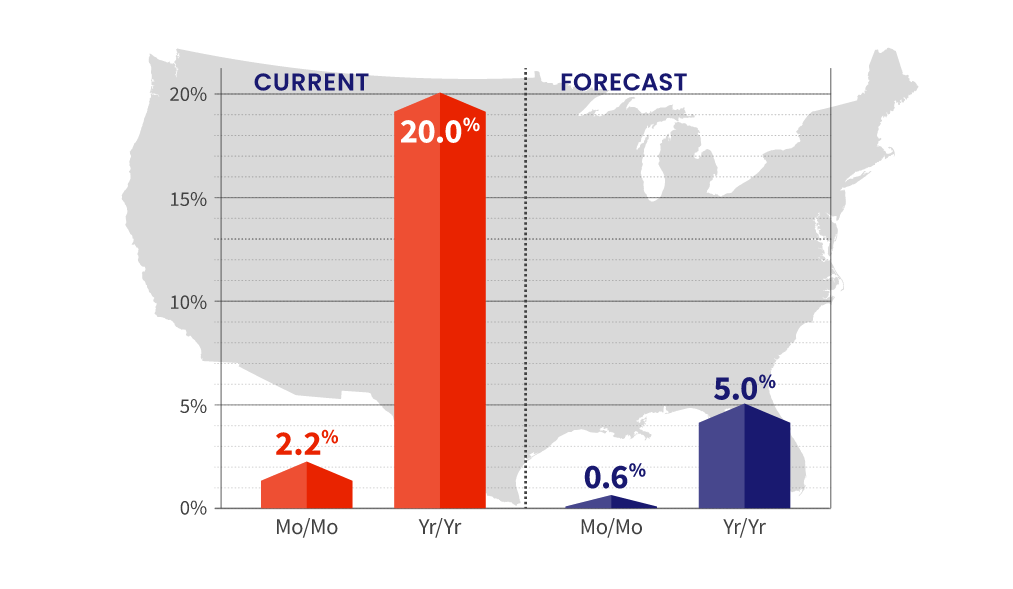

CoreLogic’s Home Price Insights revealed that home prices rose 20% YoY in February despite REAL average hourly earnings declining -2.678% YoY. THAT is euphoria! Or Stimulypto, as I like to call it.

No, The Federal Reserve still hasn’t removed its staggering monetary stimulus. Notice that M2 Money Stock is still growing at a torrid 11% pace.

20% YoY home price growth in February? CoreLogic has increased their forecast of home price growth to 5%, likely because The Federal Reserve is imitating a sloth in removing its monetary Stimulypto.

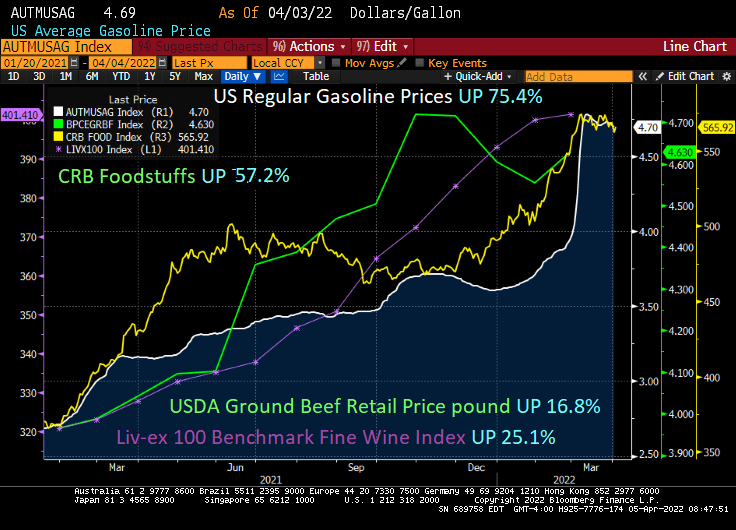

Of course, there are other assets growing at lightning speeds. US Regular gasoline prices are UP 75.4% under Biden. Foodstuffs are UP 57.2% since Biden was installed as President. At least ground beef is only up 16.8% while the fine wine index is up 25.1%.

Speaking of wine,Hitching Post II in Buellton, CA must be suffering from rising food and grape costs too (I highly recommend eating there and using their HP Magic Stuff at home). Not to mention their spectacular wines. Roast artichokes anyone??

Its official! I submitted my resignation from George Mason University effective June 1, 2022. I will miss teaching the students, past and present.

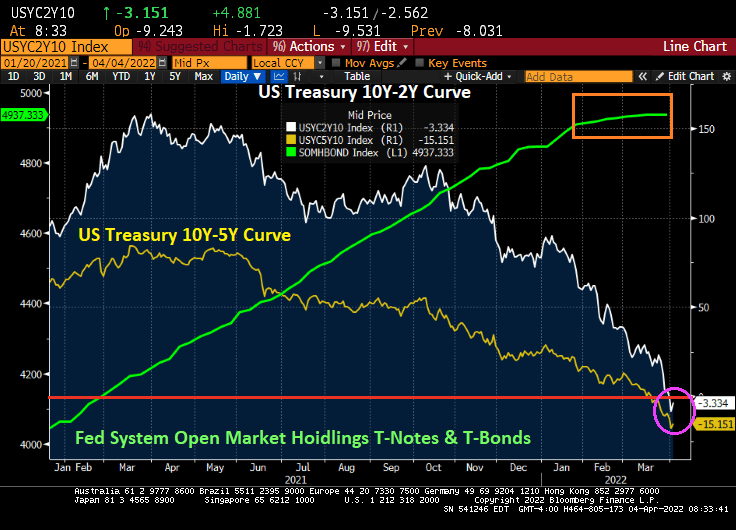

But back to the US Treasury yield curve. It remains in reversion (meaning shorter-term Treasuries have higher yields than longer-term Treasuries, usually a sign of impending recession. The Fed has actually started quantitative tightening (QT) and the growth rate of Treasury note and bond purchases has slowed to a crawl.

Meanwhile, Bankrate’s 30-year mortgage rate rose slightly to 4.91%.

Meanwhile, President Joe “The Big Guy” Biden has ordered carmakers to increase their average fuel economy to about 49 miles (78.8 kilometers) per gallon by 2026. Of course, this is intended to kill-off gasoline-powered autos and make all cars electric or hybrid like the Toyota Prius.

This can be the Democrat’s midterm election slogan: “Making living in the USA unaffordable!”

The middle-class unaffordable Ford F-150 Lightning at nearly $100,000. Thanks Joe!

Alternatively, you can buy a Buick Envision (made only in Shanghai China) with up to 24 city / 31 highway MPG. Well, kiss that baby goodbye under Biden’s new MPG mandate.

You must be logged in to post a comment.