What is the difference between a porcupine and the KC Fed Jackson Hole conference? At the annual Jackson Hole Federal Reserve retreat, the pricks are on the inside! (Source: Clive Owen from “Shoot ‘Em Up” about drivers of BMW cars).

Yes, the elites of The Federal Reserve System will gather at Grand Teton National Park in Wyoming to discuss “Structural Shifts in the Global Economy,” and will be held on Aug. 24-26.

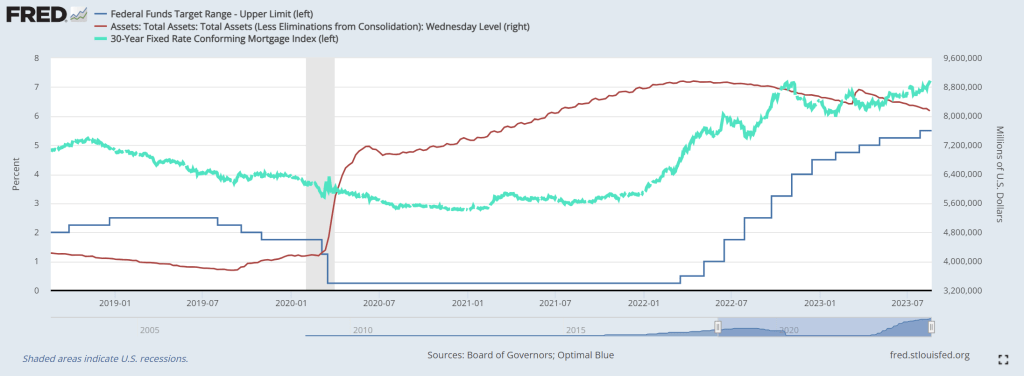

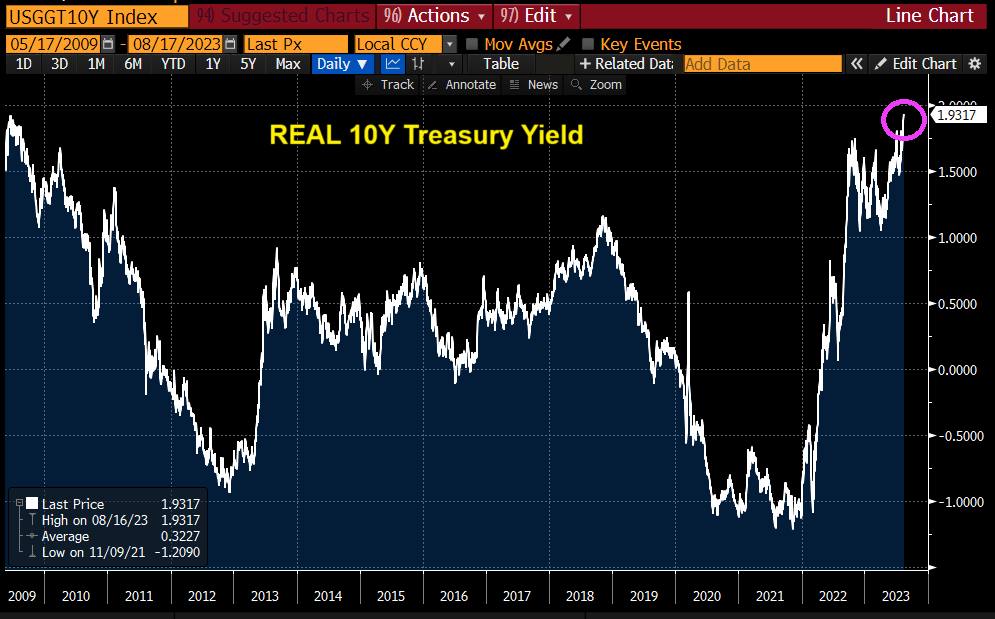

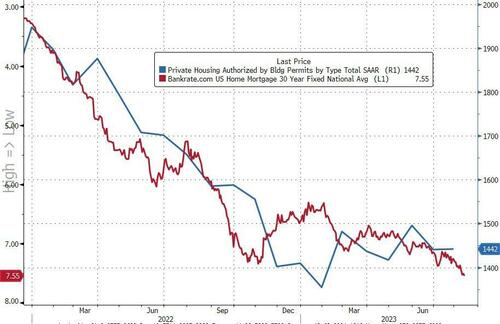

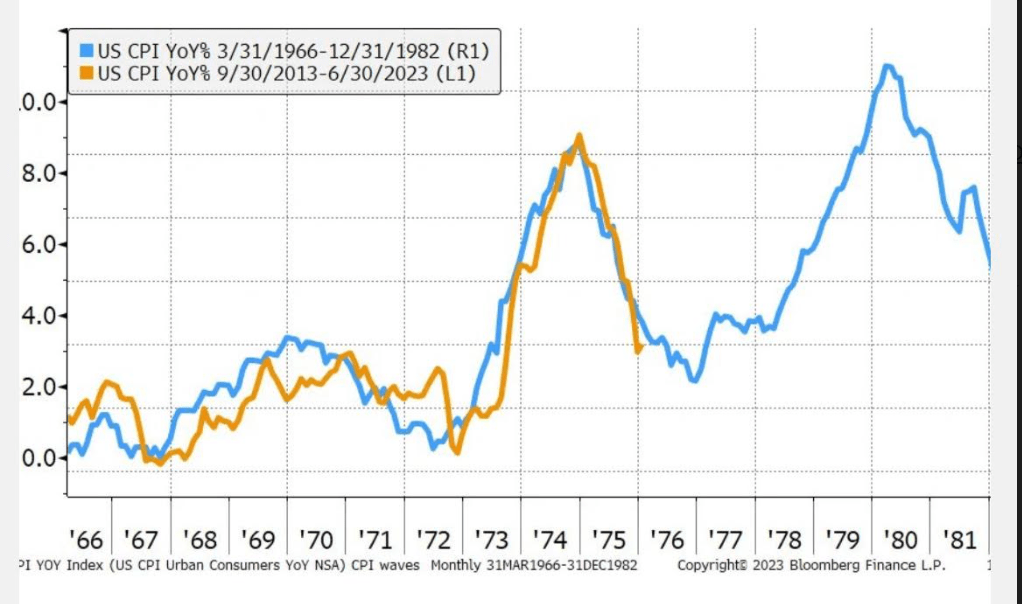

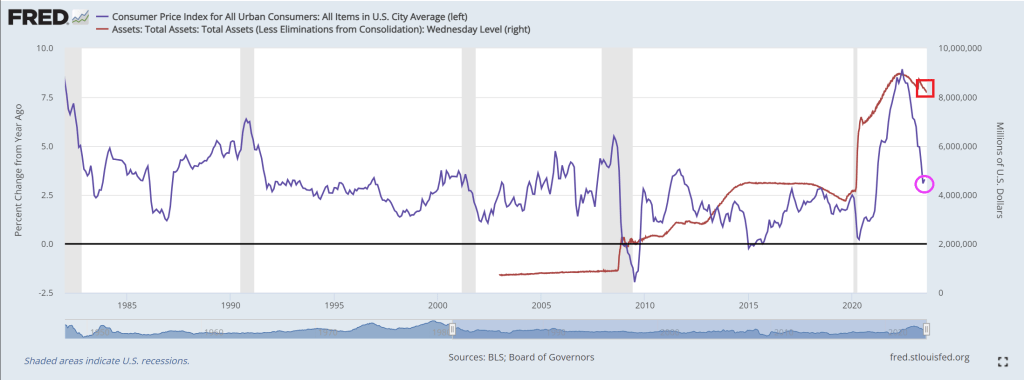

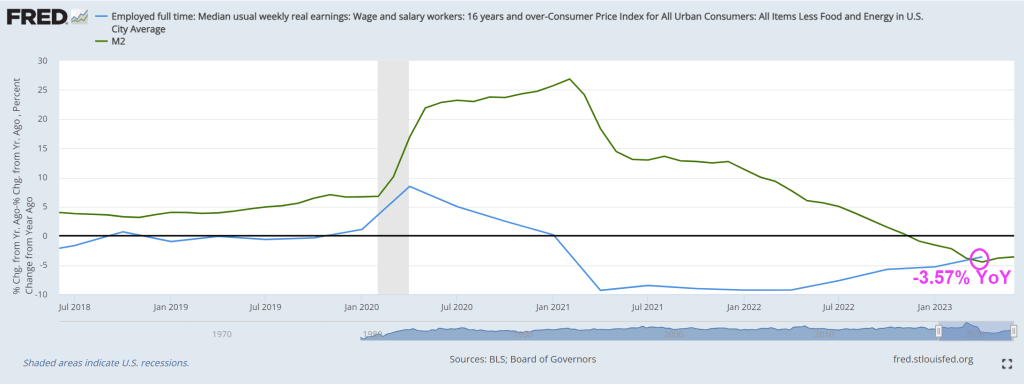

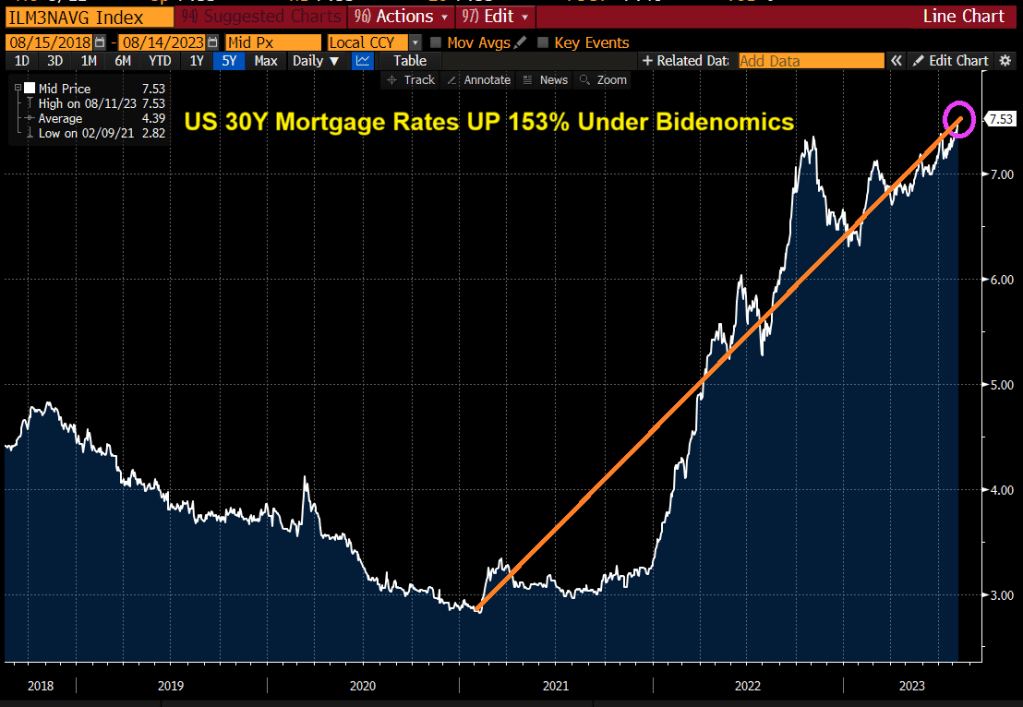

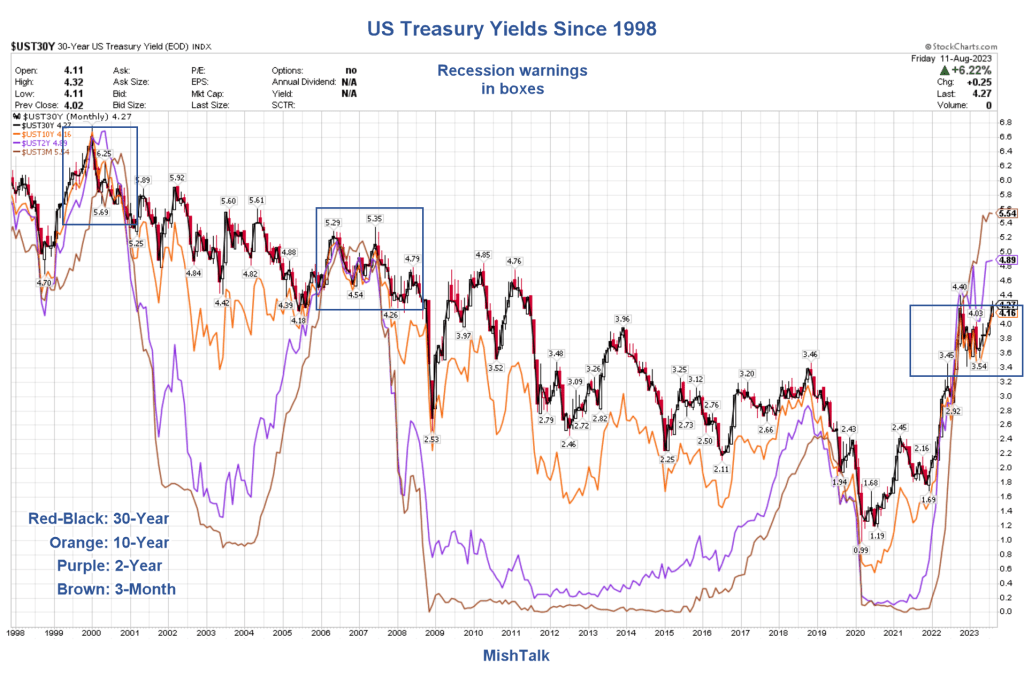

Here is where we sit on Sunday. The 30-year conforming mortgage rate (blue-green line) is over 7% and up 154% under Biden. The Fed’s target rate is now 5.50% (dark blue line) and The Fed still has over $8 TRILLION on its balance sheet. So they haven’t really done all they can do to fight inflation.

Here is a Message From Michael (Snyder). No, not Dionne Warwick’s Message TO Michael.

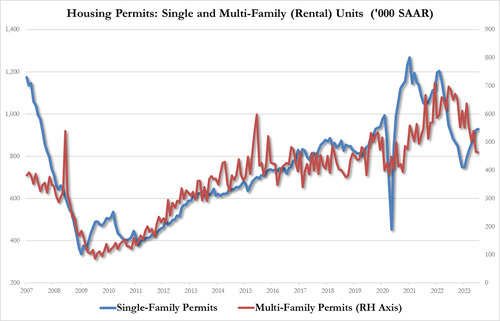

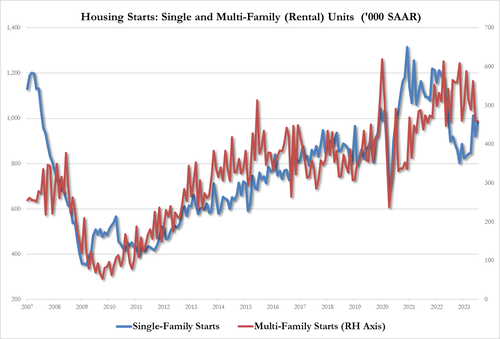

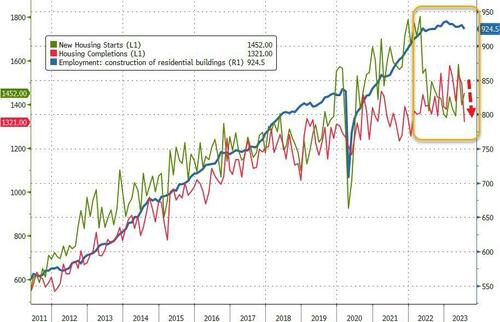

Do you remember what happened in 2008? Many people believe that another historic financial disaster is coming and that it will absolutely devastate the U.S. economy. Earlier this week, I wrote about an investor named Michael Burry that has actually bet 1.6 billion dollars that the stock market is going to crash. He made all the right moves in 2008, and he fully intends to be proven right once again in 2023. Of course current conditions definitely resemble 2008 in so many ways. The residential housing market is so dead right now, and commercial real estate prices are plummeting at a very frightening pace. Unfortunately, officials at the Federal Reserve are making it quite clear that they are not done strangling the economy.

This week, mortgage rates jumped above the 7 percent mark to the highest level that we have seen in more than 20 years…

Mortgage rates surpassed 7% this week, hitting the highest level in more than two decades.

The average rate on the popular 30-year fixed mortgage increased to 7.09% this week, up from 6.96% the week prior, according to Freddie Mac’s release on Thursday. That’s the highest point since the first week of April 2002 and marks just the third time rates have exceeded 7% since then. The last times were in October and November of last year, when the rate reached 7.08%.

Needless to say, high mortgage rates have been crippling the housing market in recent months.

At the midpoint of this year, existing home sales were down a whopping 18.9 percent from the same time in 2022…

Total existing-home sales1 – completed transactions that include single-family homes, townhomes, condominiums and co-ops – receded 3.3% from May to a seasonally adjusted annual rate of 4.16 million in June. Year-over-year, sales fell 18.9% (down from 5.13 million in June 2022).

There are certainly lots of people out there that would like to buy homes, but thanks to how high mortgage rates have become they simply cannot afford to do so.

Housing has become extremely unaffordable in this country. According to Redfin, the percentage of teachers that can afford to buy a home close to the school where they work has fallen to just 12 percent…

The number of teachers who can afford a reasonably priced home in their school district nationwide has collapsed to just 12%, down from 17% last summer and 30% in 2019, amid the worst housing affordability crisis in a generation, according to data from Redfin.

Redfin’s analysis of median teacher salaries for 2022 across 50 major cities for over 70,000 PreK-12 public and private schools revealed no teacher in San Jose and San Diego could afford homes within “commuting distances” to their respective school, which means home and work are 20 minutes during typical rush hour conditions.

So much damage has already been done.

But apparently officials at the Federal Reserve believe that even more carnage is necessary, because they are indicating that more rate hikes are on the table…

Most Federal Reserve officials signaled during their July policy-setting meeting that high inflation still poses an ongoing threat that could necessitate additional interest rate hikes this year.

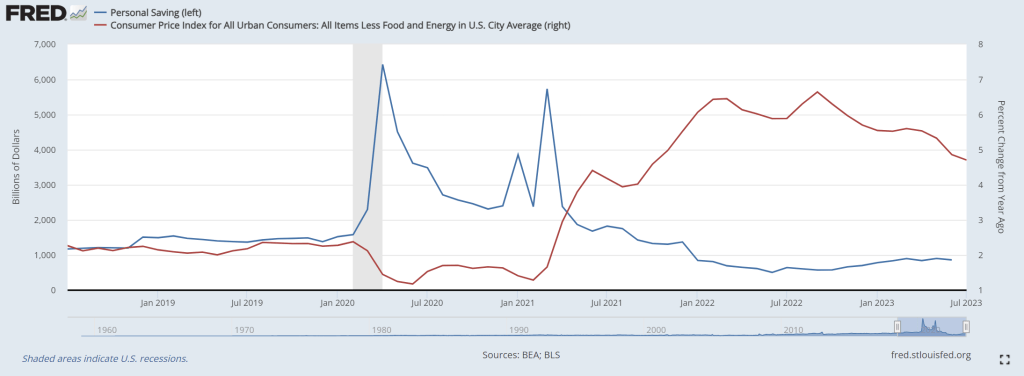

Minutes from the U.S. central bank’s July 25-26 meeting released Wednesday showed that central bank officials observed that inflation remains well above the Fed’s 2% target — and that policymakers need to see “further signs that aggregate demand and aggregate supply were moving into better balance to be confident that inflation pressures were abating.”

No.

Don’t do it.

Even if rates stay at current levels, we are headed for extreme pain.

Raising rates even higher would just be suicidal.

But it looks like they are going to do it anyway, and that could push mortgage rates up to the 8 percent level…

Economists have predicted mortgage rates could go above 8 percent if the economy continues to show signs of strength and the US Federal Reserve decides to raise interest rates again.

Mortgage Rates have not hit such levels since 2000, according to data compiled by Freddie Mac.

Do officials at the Fed actually believe that our system can handle such high rates?

Unless the Fed changes course, the housing market is going to absolutely implode.

And of course the commercial real estate market is already imploding.

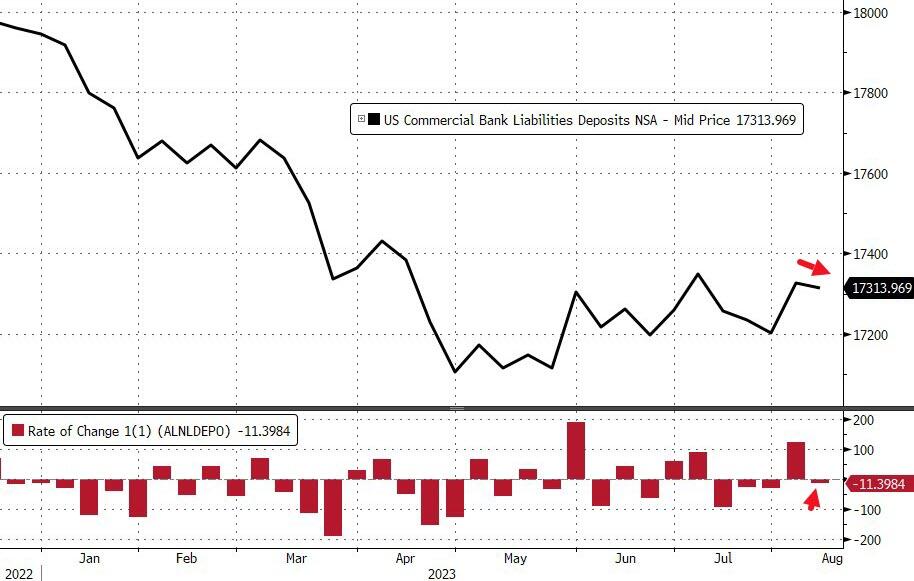

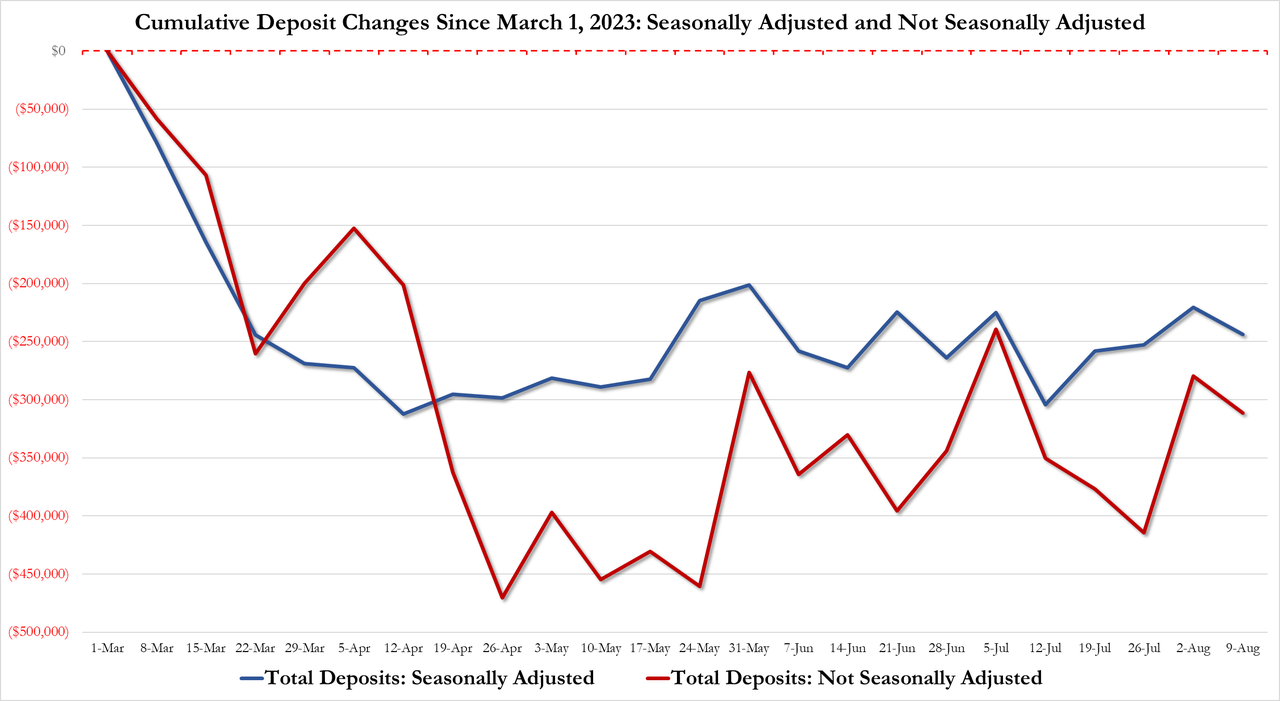

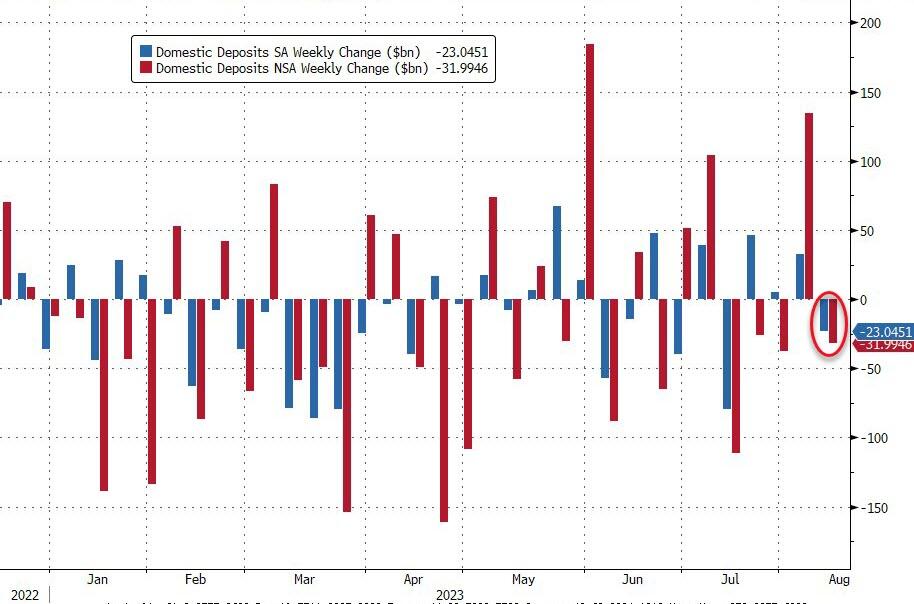

The chaos that is already transpiring is putting an enormous amount of strain on our financial institutions, and Fitch is warning that we could soon see sweeping rating downgrades in the banking industry…

A Fitch Ratings analyst warned that the U.S. banking industry has inched closer to another source of turbulence — the risk of sweeping rating downgrades on dozens of U.S. banks that could even include the likes of JPMorgan Chase

.

The ratings agency cut its assessment of the industry’s health in June, a move that analyst Chris Wolfe said went largely unnoticed because it didn’t trigger downgrades on banks.

In many ways, I feel like I am watching a repeat of 2008.

Officials at the Fed can clearly see everything that is happening, but they just keep insisting on making things even worse.

So I hope that you have been preparing for turbulent times, because things are going to get crazy.

Sadly, the truth is that most Americans are not prepared for tougher times. In fact, one recent survey discovered that 72 percent of Americans are not financially secure…

For many Americans, payday can’t come soon enough. As of June, 61% of adults are living paycheck to paycheck, according to a LendingClub report. In other words, they rely on those regular paychecks to meet essential living expenses, with little to no money left over.

Almost three-quarters, 72%, of Americans say they aren’t financially secure given their current financial standing, and more than a quarter said they will likely never be financially secure, according to a survey by Bankrate.

Many of those people will lose their jobs during this new economic crisis, and because they don’t have any sort of a financial cushion to fall back on many of them will also end up losing their homes.

Delinquency rates are already starting to move higher, and that should deeply alarm all of us.

But what we have experienced so far is just the tip of the iceberg.

So brace yourselves for what is ahead, because this ride is only going to get bumpier from here.

Here is a photo of The DC Economic Strangler, Fed Chair Jerome Powell, riding a wild jackalope in Jackson Home Wyoming.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.