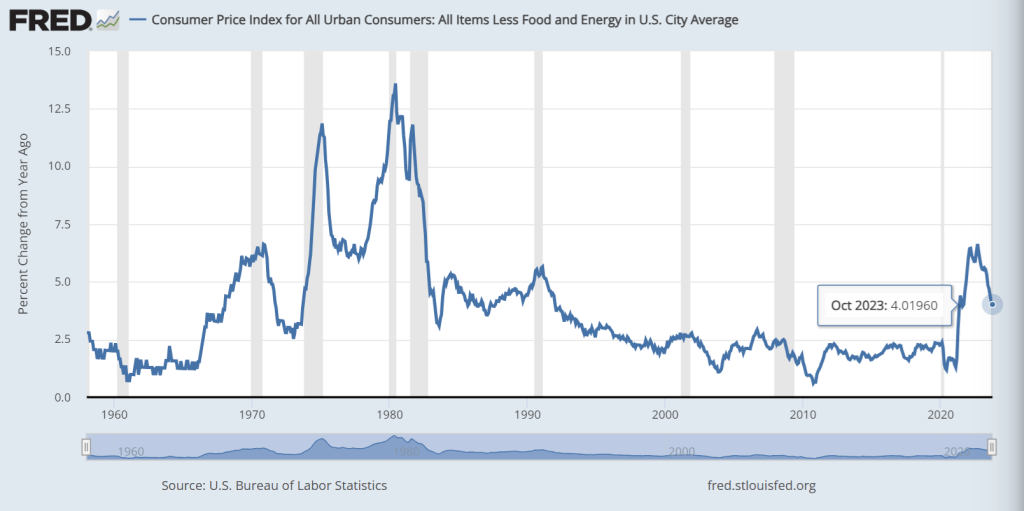

Well, at least core inflation cooled to 4%, twice The Fed’s target rate.

At least The Fed is making progress. But on the housing front, shelter CPI is still up 6.7% YoY while transportation services are up 9.2% YoY. So, as long as you don’t have to rent or go anywhere, inflation looks good!

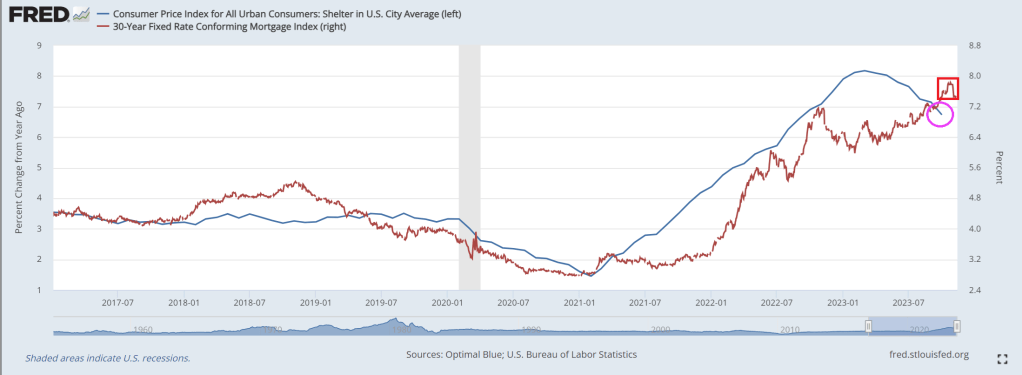

Shelter CPI is over 3x The Fed’s inflation target rate, despite mortgage rates being up 169% under Biden.

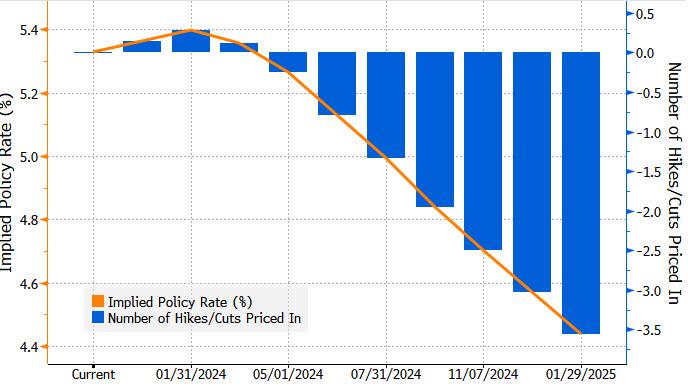

The 10-year Treasury yield cooled to 4.50% as investors see no further action from The Fed … at least until 2024.

Yes, investors forecast big cuts in interest rates in 2024 as the election approaches and The Fed attempts to push our befuddled, nasty Commander-in-Chief over the finish line. Instead of Mean Joe Greene (former Steeler great), we have Mean Joe Biden.

The US economy is still under the thumb of The Federal Reserve. Perhaps The Fed will annouce that the last rate hike was the last time. But you don’t have to be a fortune teller to know The Fed will be cutting rates like crazy as the election approaches.

At least California Governor “Greasy Gavin” Newsom cleaned up The Streets of San Francisco ahead of China’s XIe meeting with President Biden. Here is Biden singing his favorite song about China “If You’ve Got The Money, I’ve Got The Time.”

The Talking Heads at The Federal Reserve keep yammering about persistant inflation (which Yellen kept saying was transitory) and whether or not Fed rate hikes will be necessary to get infation to 2%.

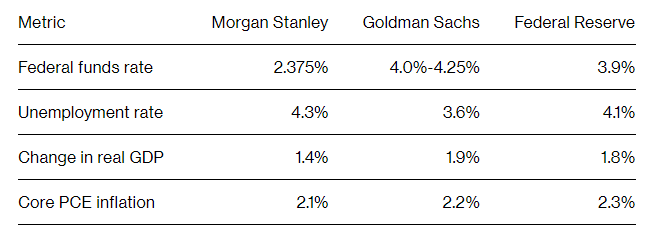

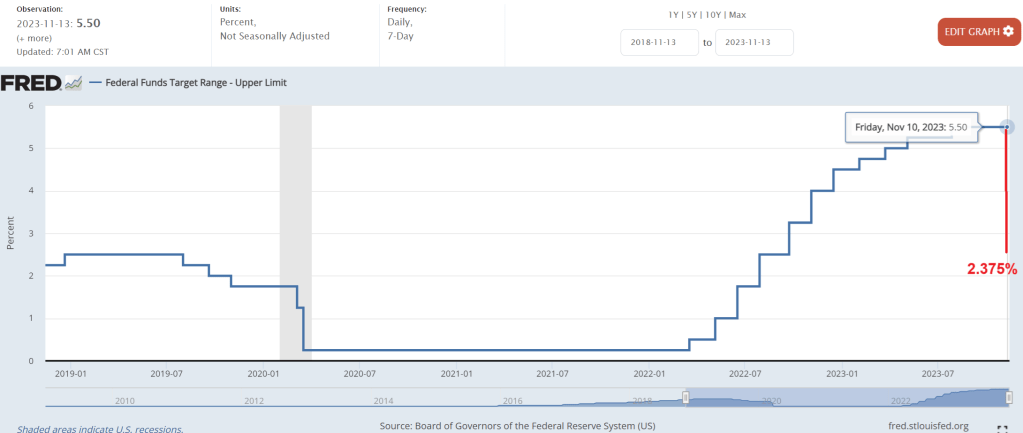

Instead of muddling lectures (like by Atlanta Fed President Rafael Bostic) on Fed tightening to fight inflation, let’s address the elephant in the room (no, not Chris Christie or Hillary Clinton), but Morgan Stanley’s soft landing forecast of a Fed Funds rate cut from 5.50% today to 2.375% in 2024. This is a whopping 215 basis point cut!

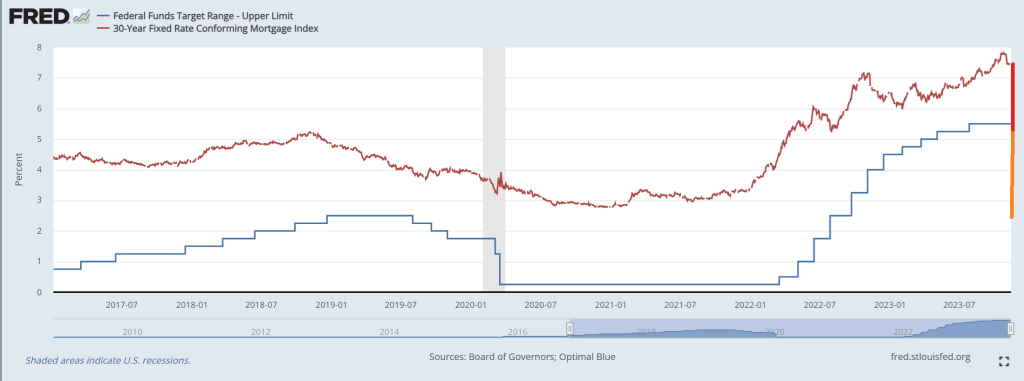

Currently, the spread between the 30-year conforming mortgage rate and The Fed Funds Target rate is 1.981% of 198.1 basis points. While the better spread is the mortgage rate compared to the 10-year Treasury yield, I am going to use Morgan Stanley’s Fed Funds target rate forecast for 2024. Assuming the spread is constant, this results in a mortgage rate in 2024 of … drumroll … 5.50%.

In one sense, a 200 basis point decline in the 30-year mortgage rate would be welcome news to home buyers. On the other hand, Morgan Stanley is forecasting a soft landing and a rise in the unemployment rate to 4.3%, hardly good economic news.

So, fear the talking Fed. They are talking about fighting stubborn inflation while ignoring the slowdown forecast for 2024.

Even eating breakfast under Bidenomics is more expensive. Particularly if you like orange juice like I do. To save money, I am probably going to have to switch to nasty-tasting Tang.

Food CPI is up 3.69% year-over-year. The rate of growth in food prices is slowing. But do I trust BLS data on CPI? Of course not.

Orange juice prices are up 47% under Biden.

And we see that REAL GDP is growing at a slower rate than nominal GDP.

Speaking of Bidenomics, here is an interesting Zero Hedge story on “The Biden-Du Pont Nexus: From A Prestigious Golf Club To A Controversial Child Rape Plea Deal.” What is it with Delaware elites having sex with their children?? And why is NY AG Letitia James prosecuting Donald Trump when there has been no crime while she let’s Epstein’s clients who flew to have sex with minors (used to be illegal) off the hook?

But I feel good! After my breakfast of … Scotch Broth. OJ is just too expensive.

On a amusing or sad note, Biden campaign communications director Michael Tyler’s message to Americans who are worse off economically under Biden: “That’s precisely why we need another four years to finish the job.” OMG! What does “finish the job” mean?? I am afraid to ask.

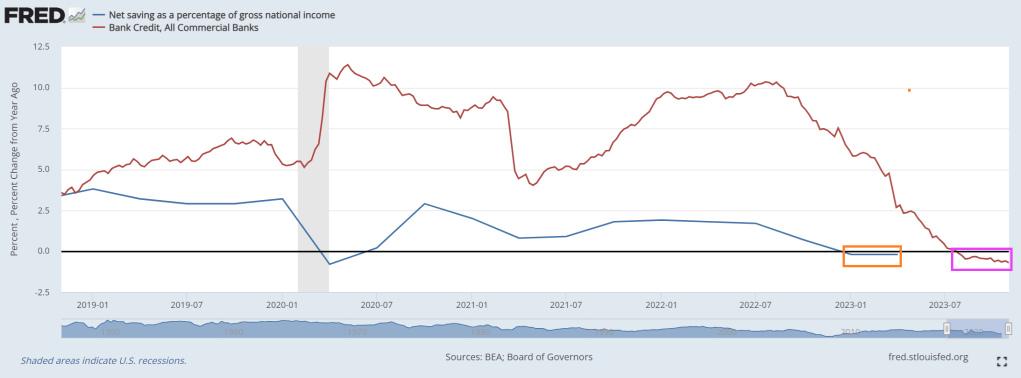

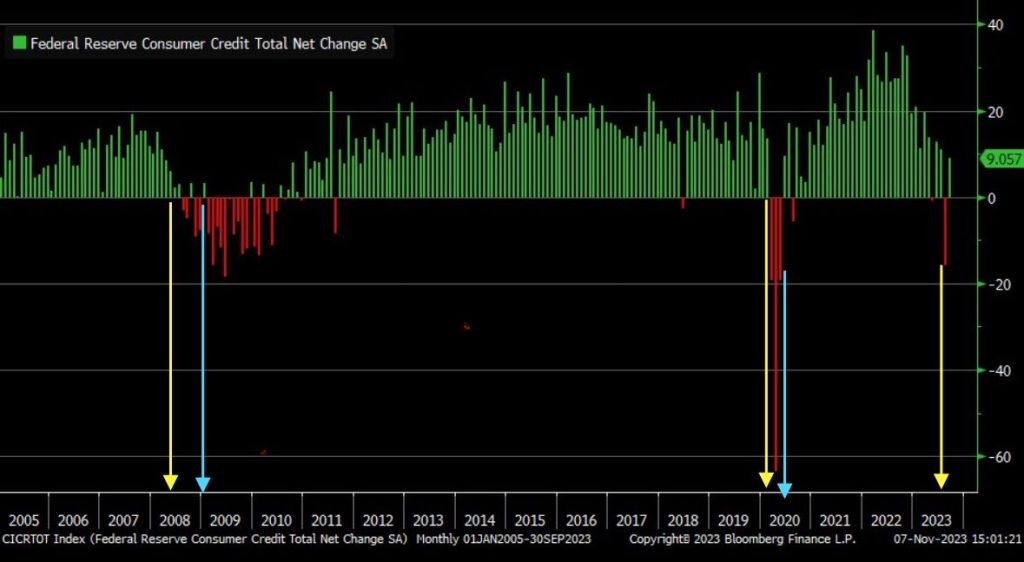

Where we currently sit is … bank credit growth is in the red (15th straight week of negative growth) and net savings as a percentage of gross national income has seen negative growth YoY for 2 consequtive quarters.

September marked the largest consumer credit drop since May 2020, signaling a significant recession warning.

And with Bidenflation (or Yellenflation) and The Fed’s counterattack, we are seeing bank stocks losing relative to the tech sector.

Proshares Bitcoin (BITO)’s assets have nearly doubled in the past 30 days.

Yes, the Three Stooges (Biden, Yellen, Powell) have put the US on a highway to hell!

Conforming mortgage rates have actually dropped -34 basis points since hitting a local high of 7.81% on October 19, 2023. Unfortunately, mortgage rates are still up 169% under Biden and his signature Bidenomics. Even worse, home prices are up 33% under Bidenomics making housing even more unaffordable.

While real weekly earnings growth finally turned positive in 2023, growth is already slowing again as The Fed’s balance sheet slowly declines.

Under Bidenomics, with its high inflation rate and crushing negative wage growth, consumers are draining their savings and living on a prayer …. and consumer credit to cope.

What is worriesome in the transition rates (like current to 90-days delinquent) Credit cards (blue) and auto loans (red).

A closer look at credit card delinquency rates on a year-over-year (YoY) basis, showing the fastest growth in delinquencies since the Covid economic lockdowns.

Then we have commercial real estate delinquencies are now the highest the have been since 2013.

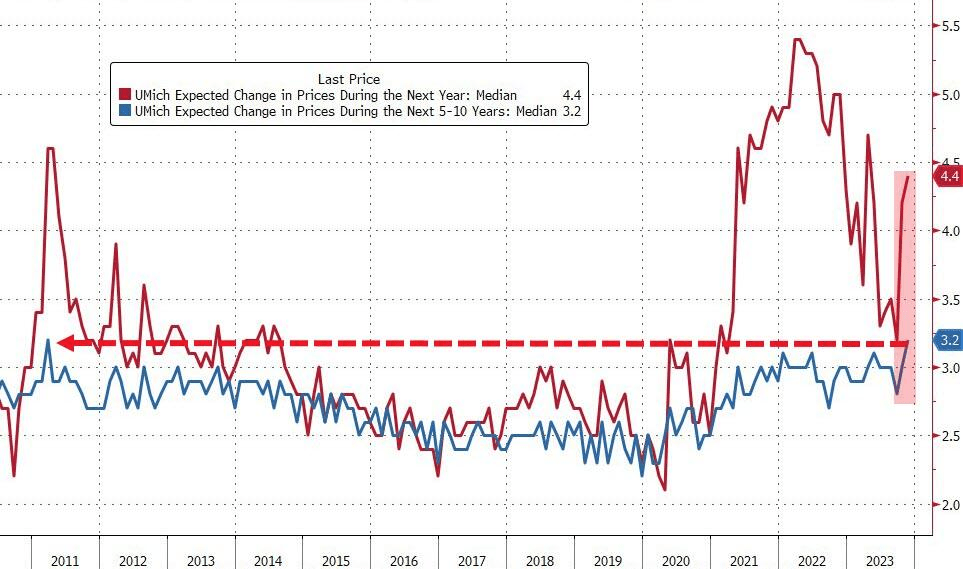

Meanwhile, University of Michigan consumer sentiment about inflation spiked to 4.4%. That is the highest medium-term inflation expectation since 2011.

Has anyone considered the impact of Biden/Mayorkas’s open southern border with Mexico? Other than the crime, stress on existing services like healthcare, schools and Social Security. But where will the 8 million illegal immigrants reside? Well. the Biden Administration has an answer: throw money at it! This time, $45 billion to convert empty office space to homes. Not just for illegals, but for anyone.

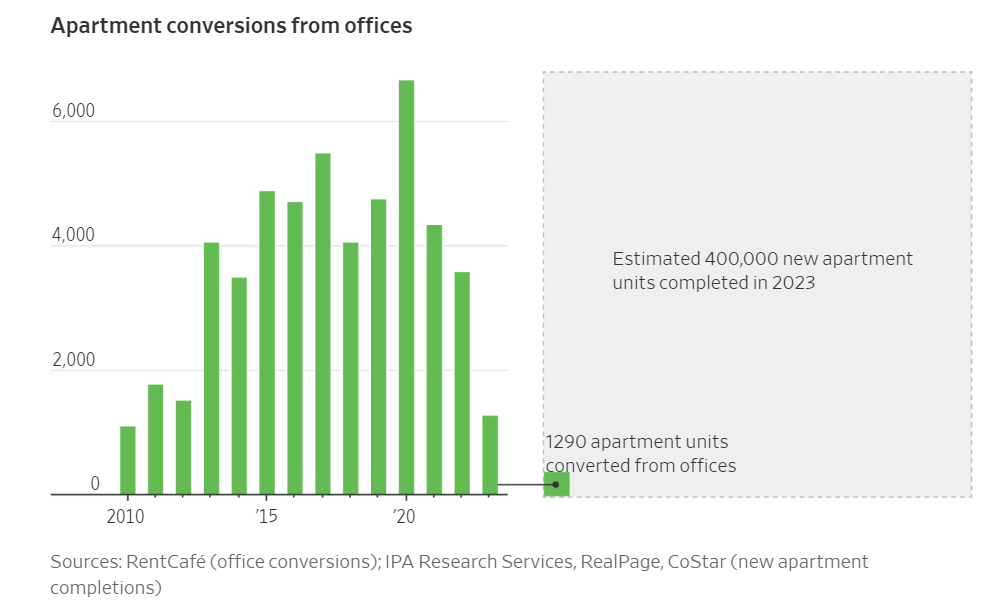

Cities hoping to convert emptying office buildings into apartments are running into financing issues, stagnating rental markets and other challenges that are bottling up their efforts.

Developers last year created just 3,575 apartment units in the U.S. through office conversions, according to an analysis by rental listing site RentCafe. That amounts to less than 1% of all apartments built that year through new construction.

Federal and local governments are also trying to give conversions a boost. The White House said last month that it was updating guidance for existing grants and spending programs to make billions in federal dollars available for these projects. It also said it would seek the conversion of more government-owned properties into housing.

Some cities, such as Washington, D.C., New York and San Francisco, are also taking steps to encourage more conversions. Tax incentives and faster approvals are “rocket fuel” for these projects, said Sheila Botting, a principal at commercial property brokerage Avison Young.

Even so, the process has always been fraught with difficulty and few office buildings are natural candidates. Conversions are easiest in older, lower-quality and mostly empty buildings with small floors. But less than 1% of office space in the biggest U.S. cities ticks those boxes, according to Avison Young.

In significant ways, the conversion process is getting even harder now. Slowing rent growth might make apartment conversions less attractive to investors, if the trend persists into next year. Asking rents for apartments have fallen 1.2% nationally over the past 12 months, according to rentals website Apartment List.

Projects Not Economical

Without massive subsidies these projects are not economically feasible. Many aren’t even with massive subsidies.

In downtown Dallas, developer Wolfe Investments seeks to convert an 18-story, 1950s office tower into residential apartments, but has recently been fighting off foreclosure from its lender, Thistle Creek Partners, court records show.

Developers of One Camelback, a 200,000-square-foot office building in central Phoenix, are trying to convert it into what would be one of the city’s most expensive rental-apartment properties. A website advertises $8,000-a-month apartments, with floor-to-ceiling windows and crystal-clear views of nearby mountains.

But the developers, Sagamore Capital and partners defaulted on a loan of about $70 million. The project’s lender, Delphi Financial Group, has moved to foreclose. An auction of One Camelback is set for later this month, according to documents filed in Maricopa County, Ariz.

Biden Throws $45 Billion in Federal Funds to Convert Offices into Homes

Questions abound. Assume you can convert offices into homes, who wants to live in them? Is a tear down cheaper?

The government has 1,500 office buildings nationally and leases on almost 200 million square feet of additional space that it does not need. Instead of canceling leases and selling the real estate, it’s going to convert them into clean energy spaces.

With enough subsidies, developers will try nearly anything. Then when the projects fail, the developers ask for more money.

How is this Being Paid For?

Taxpayers of course. But Biden is funneling $45 billion from clean energy incentives in the ridiculously named Inflation Reduction Act (IRA) into housing conversions.

You might also be wondering what this has to do with clean energy, and the answer is nothing. The questions keep piling up and I have answers.

What’s Really Going On Here?

Biden is hoping to spread the IRA dollars around to buy more votes.

But to do so, he is taking money away from his other pet projects to fund the idea of the moment. His idea of the moment is to do something about the price of rent.

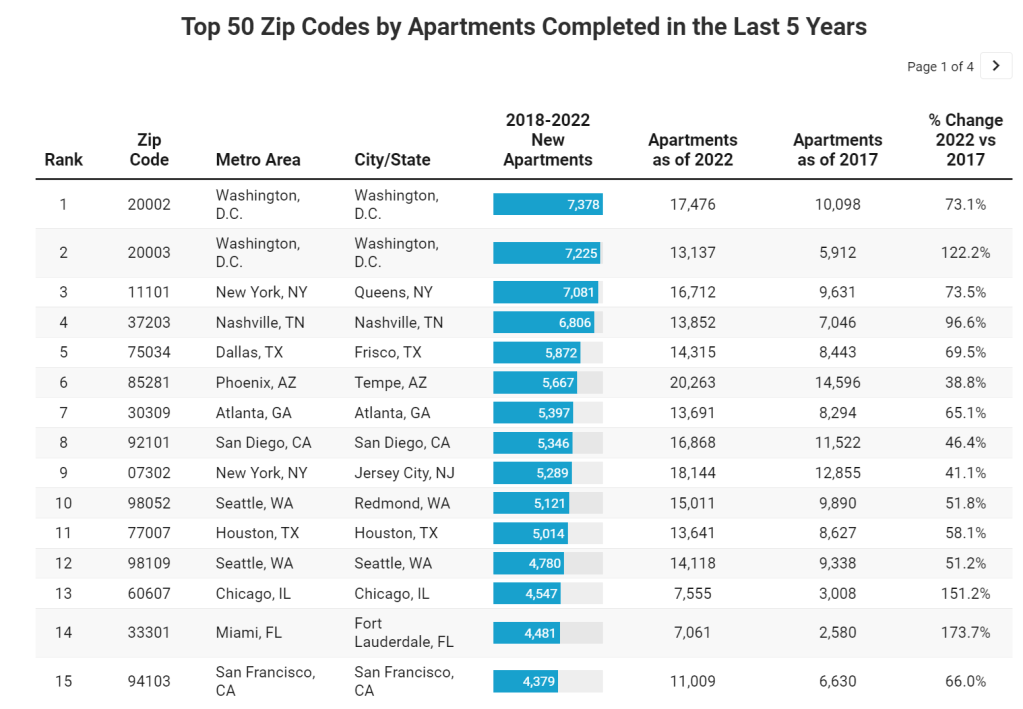

According to RentCafe, Washington DC had two zip codes that led the nation in apartments completed in the last five years (up to 2022).

Why is the private sector doing so few conversions? THAT is the right question. The answer? Office-to-housing conversion is hard and the demand may not be there. But with 8 million illegal immigrants having crossed the border, Biden has to do something. So Biden steps in with $45 billion to convert empty office space to homes. And I have to ask: is this a shadow wealth transfer to large Democrat-controlled cities as an apology for the havoc caused by Biden/Mayorkas open border policy?? Just asking!

So if an idea is really bad and won’t work, like solar power in areas with limited/spotty sunlight or wind turbines in areas with little/sporadic wind, Federal and State governments are always on stand-by to do something really stupid. Like rent control, which creates even worse distortions.

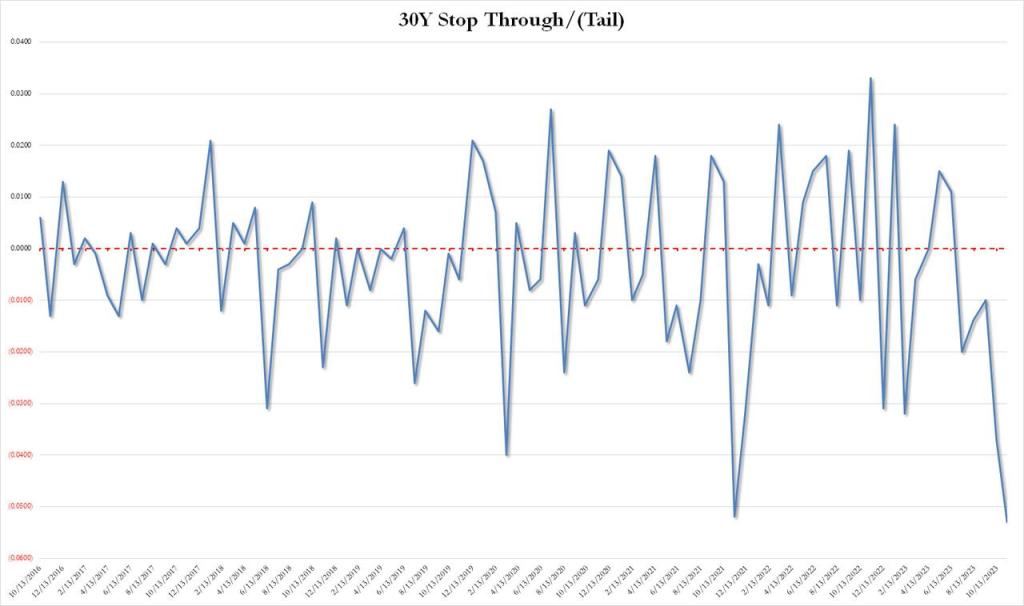

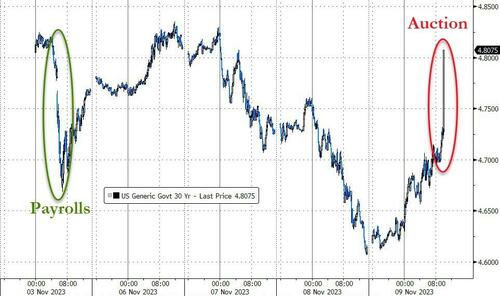

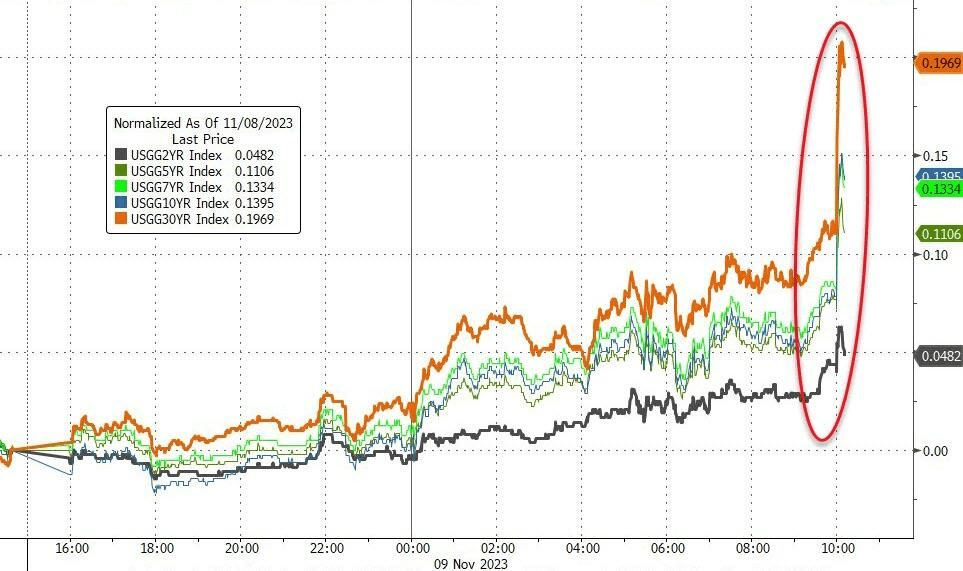

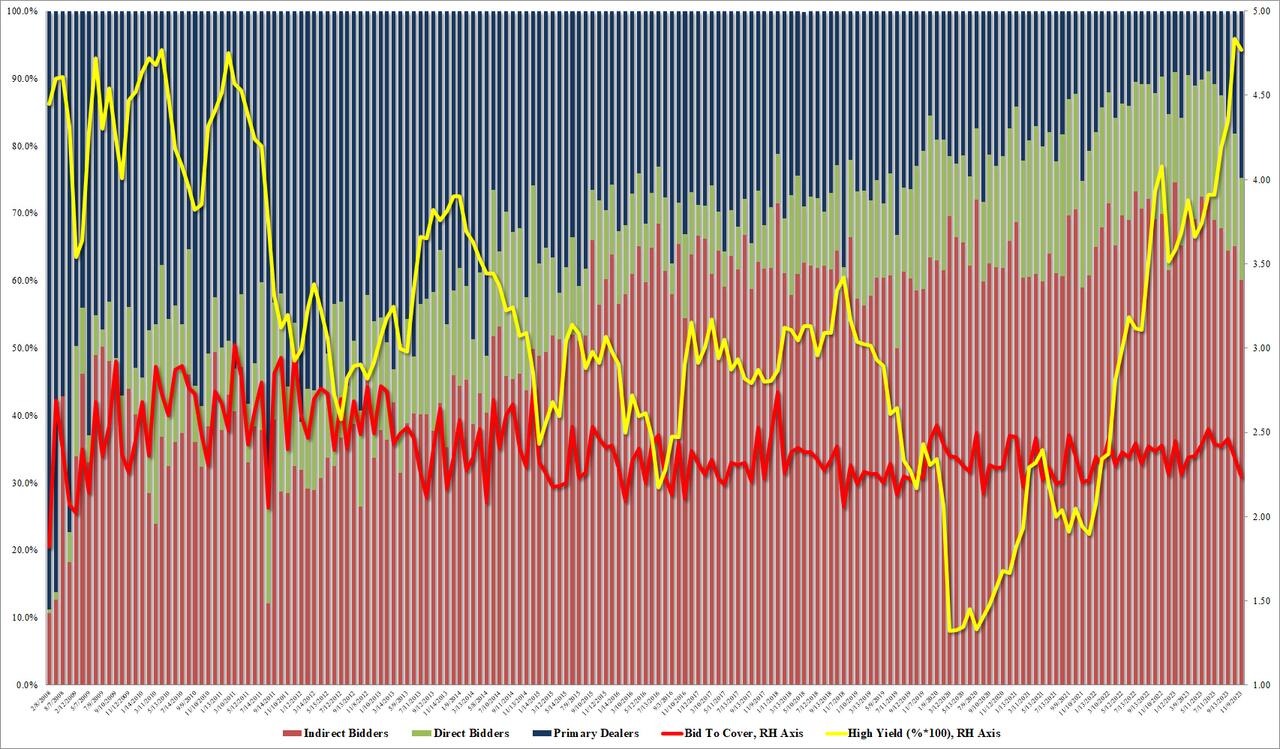

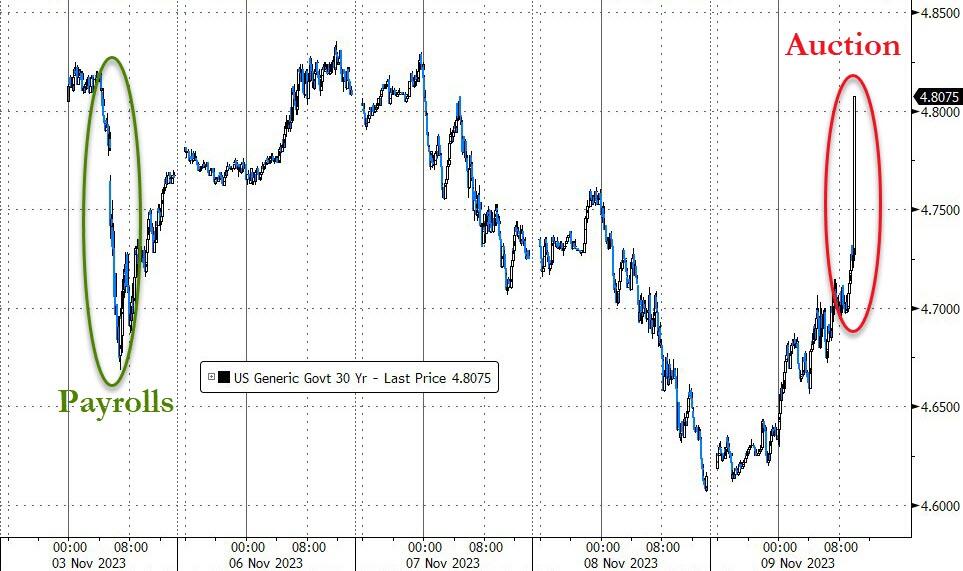

The bond priced at a high yield of 4.769%, which was below last month’s 4.837%, and just shy of the April 2010 high. But more importantly, it tailed the When Issued by a whopping 5.3bps, which was… well… terrible, because as shown in the chart below, this was the biggest tail on record (going back to 2016).

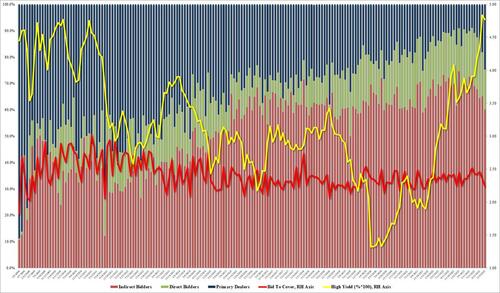

The bid to cover was just as bad: at 2.236 it was the lowest since Dec 2021.

The internals were even worse as foreign bidders (Indirects) tumbled from 65.1% to 60.1%, the lowest since Nov 2021, and with Directs taking down only 15.2%, banks (Dealers) were forced to step up and take the balance, or a whopping 24.7%, double the recent average of 12.7%, and the highest since Nov 2021.

This is a big warning flag because every time we have seen a surge in Dealer takedowns, some sort of Fed intervention – QE or otherwise – has usually followed and we doubt this time will be different.

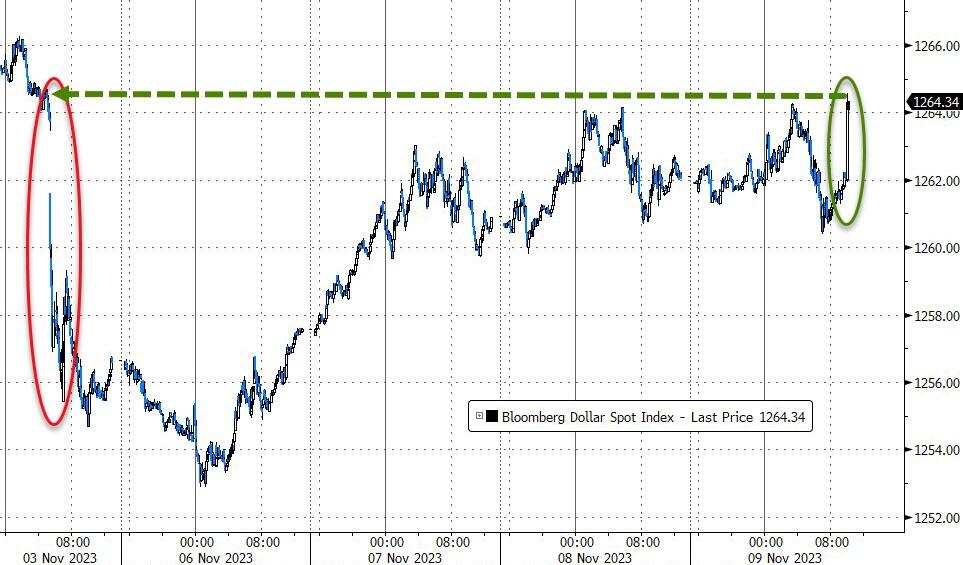

The market reaction to the catastrophic 30Y auction was immediately, sparking a swift and painful response across markets with bonds and stocks hammered lower and the dollar spiking.

Treasury yields – as you would expect – exploded higher, with 30Y Yields back up to pre-payrolls levels…

That is the biggest spike in 30Y yields since March 2020…

But the entire curve is higher in yields…

Stocks tanked…

Regional bank stocks tumbled…

The dollar ripped back up to pre-payrolls levels…

Finally, we note that this ugly auction comes as Treasury Liquidity is evaporating dramatically…

The Fed (and The Treasury) have a problem!! Particularly since the 30Y yield reversed course and is on the rise again.

And at the 10 year tenor, the rate rose to 4.638%.

All together now!!

The Edmund Fitzgerald, symbolic of the US under Biden and Janet Yellen.

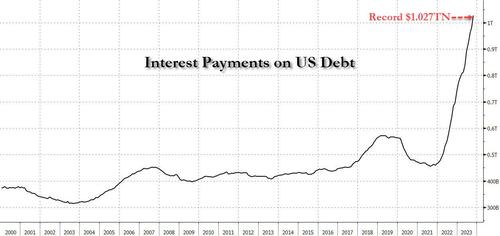

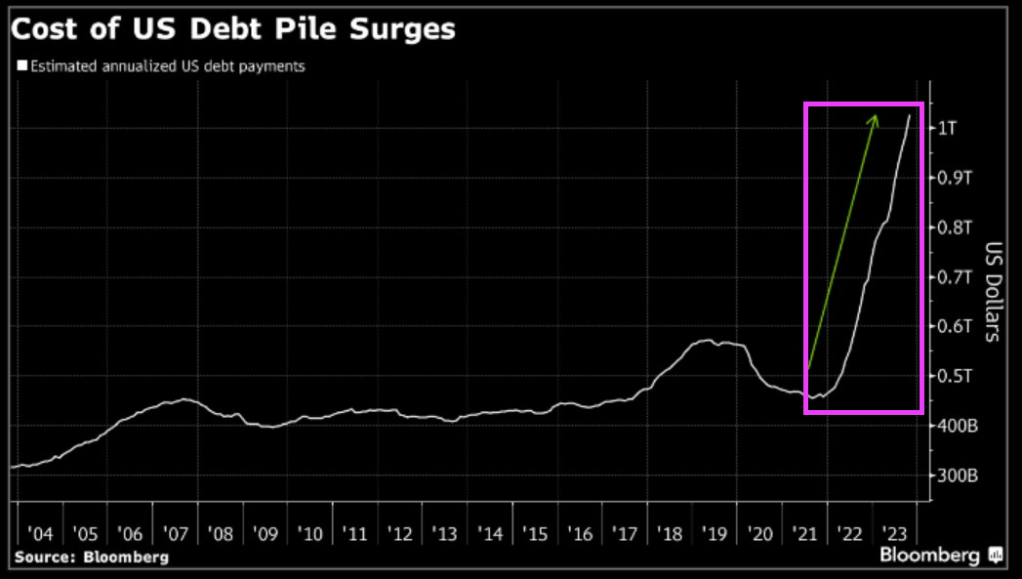

$1.027 trillion in interest is calculated by multiplying the average interest rate on marketable US Treasury debt (which according to the Treasury is 3.096% as of Oct 31) by the $26.003 trillion in marketable US debt (as of Oct 31) which nets off to $805 billion, and adding to this non-marketable debt interest (which as of Oct 31 was 2.884% multiplied by the amount of non-marketable debt which is $7.696 trillion) and which in turn is an additional $222 billion in interest. Add across and you get $1.027 trillion.

Naturally, this calculation of estimated real-time interest costs – which is entirely based on Treasury data – is different than what the Treasury actually paid. Interest costs in the fiscal year that ended Sept. 30 ultimately totaled $879.3 billion, up from $717.6 billion the previous year and about 14% of total outlays, however that number is merely lagging what the pro forma print currently is, and will inevitably catch up to it, and then lag on the other side even as pro forma interest payment start dropping (once interest rates plunge after the next QE/YCC is launched).

Fans of exponential functions, we got you covered: the unprecedented surge in both interest rates and interest expense in the past two years means that total US interest has doubled since April 2022 and that’s with the inherent lag in interest catch up – as a reminder, the vast majority of 5, 7, 10 and 30 year debt is still locked in at much lower interest rates, and as such, rates will continue to rise as all of the existing debt rolls into much higher rates over the coming years.

Looking ahead, the staggering surge in both yields and total long-term Treasuries in recent months confirms the government will continue to face an escalating interest bill. As a reminder, we were the first to point out that it took just one month after US federal debt first rose above $33 trillion for the first time, to spike by another $600 billion.

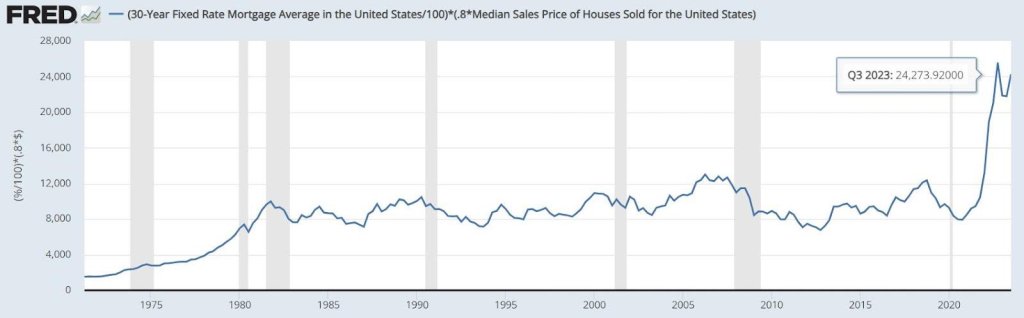

On the personal finance side, annual Interest payments on a 30-year, fixed-rate mortgage before Biden was $8,500, but after Biden it almost tripled to $24,300! That means that annual mortgage interest rose 186% under Biden.

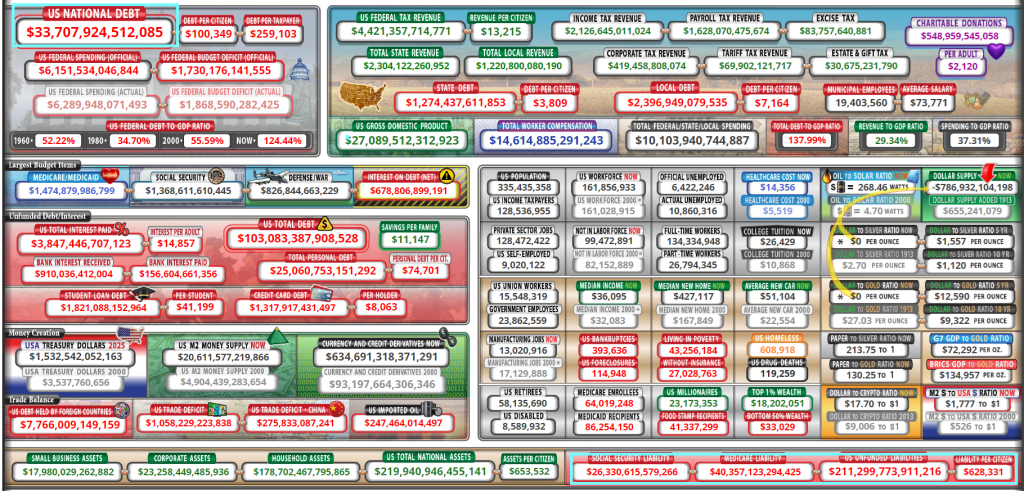

US Federal debt just hit $33.71 TRILLION. And unfunded liabilities (promises from Uncle Spam) are now $211 TRILLION. That is 526% of the the current debt load. Which means either lots of additional debt, higher tax rates or cuts in entitlements.

The cost of US debt continues to soars as The Fed combats Bidenflation.

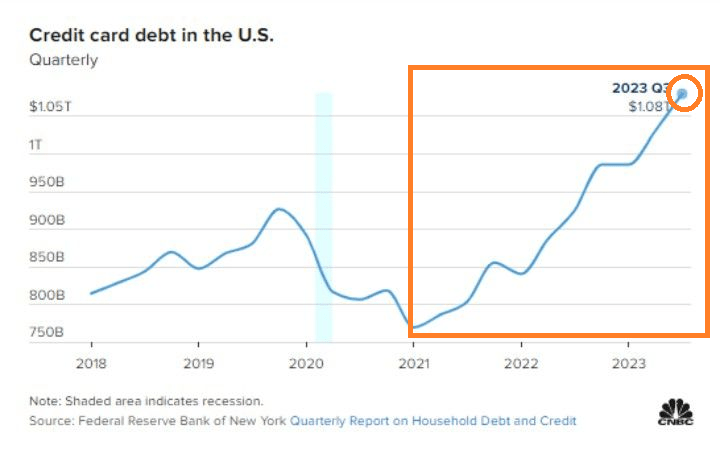

But it isn’t just Federal government debt that is exploding under Bidenomics. Consumer credit card debt has exploded under Bidenomics as consumer struggle with inflation.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.