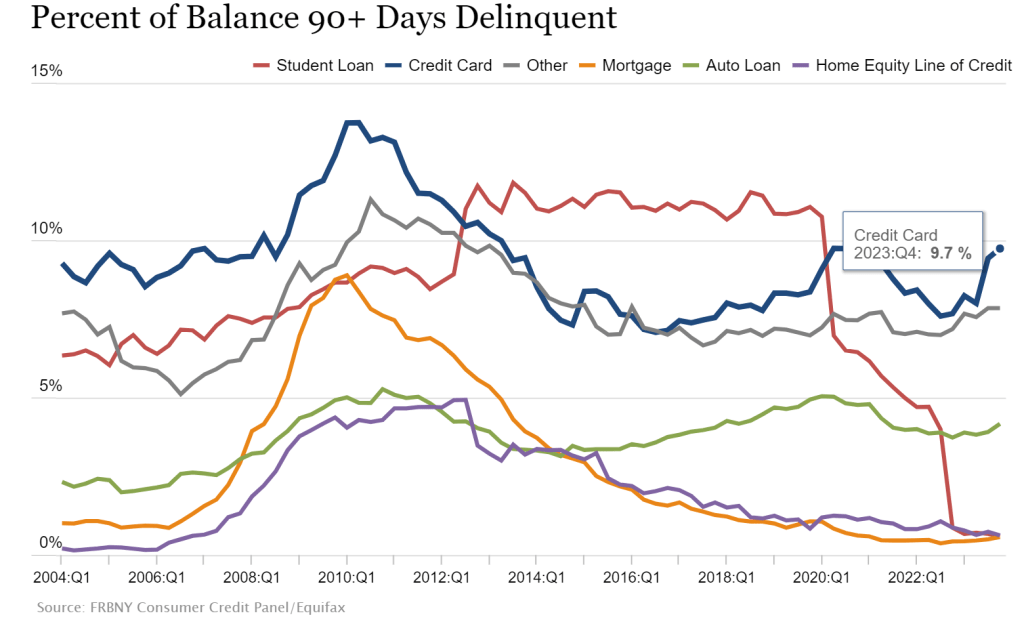

Credit card delinquecies (90+ days) rose to almost 10% in Q4 2023.

Credit card delinquencies surged more than 50% in 2023 as total consumer debt swelled to $17.5 trillion, the New York Federal Reserve reported Tuesday.

Debt that has transitioned into “serious delinquency,” or 90 days or more past due, increased across multiple categories during the year, but none more so than credit cards.

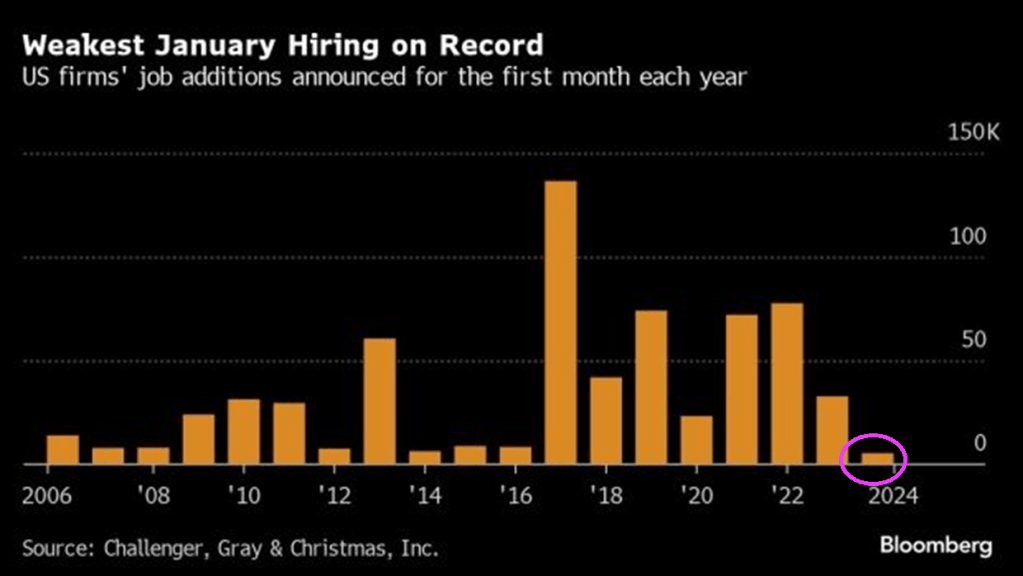

Rising credit card delinquencies combined with the worst job additions in January on record.

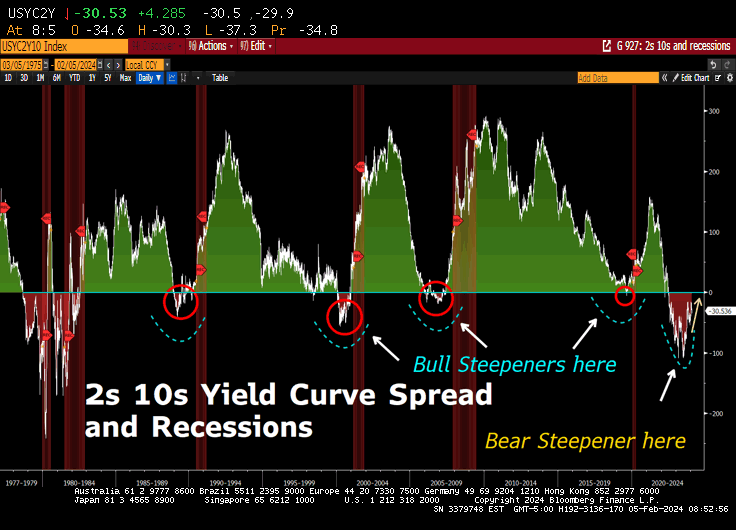

But at least the 10Y-2Y US Treasury yield curve is ALMOST flat (h

Well, the anticipated Establishment, and anti-middle class “Boader Security” bill has been released. It is all about military spending for Ukrainse (of course), grudging spending for Israel and peanuts for the border patrol to MONITOR, not stop the illegal immigrant caravans.

Independent US Senator Kyrsten Sinema told reporters the legislation would secure the US southern border (OMG, that is hilarious!!), including by requiring the Department of Homeland Security to close the border if there are an average of more than 5,000 crossing attempts per day over seven days.

In addition to $20.23 billion for border security, the bill included $60.06 billion to support Ukraine in its war with Russia, $14.1 billion in security assistance for Israel, $2.44 billion to US Central Command and the conflict in the Red Sea, and $4.83 billion to support US partners in the Indo-Pacific facing aggression from China, according to figures from US Senator Patty Murray.

An additional $10 billion would provide humanitarian assistance for civilians in Gaza, the West Bank, and Ukraine.

The US would provide $4.83 billion to support key regional partners in the Indo-Pacific where tensions have risen between Taiwan and China, as well as $2.33 billion for Ukrainians displaced by Russia’s invasion and other refugees fleeing persecution.

Millions for the military to keep Zelensky and his family in mansions while American veterans are homeless. But we expect massive Ukraine funding and the important US border security begins on page 62.

Example: $404,000,000 shall be for Immigration Judge Teams, in16 cluding appropriate attorneys, law clerks, paralegals, court 17 administrators, and other support staff, as well as necessary court and adjudicatory costs, and $36,000,000 shall be for representation for certain incompetent adults pursuant to section 240(e) of the Immigration and Na21 tionality Act (8 U.S.C. 1229a(e)).

What? Homeless vets live on the streets, but Schumer/McConnell want to QUICKLY process illegal immigrants.

Nobody spends other people’s money like Biden and Congress!

$47,500,000 for the procurement and deployment of mobile surveillance capabilities, including mobile video surveillance systems and for obsolete mobile surveillance equipment replacement, counter-UAS, and small unmanned aerial systems; – $25,000,000 for subterranean detection capabilities; – $7,500,000 for seamless integrated communications to extend connectivity for Border Patrol agents; and – $10,000,000 for the acquisition of data from long duration unmanned surface vehicles in support of maritime border security.

Other than helping the border patrol with surveillance, there are NO FUNDS FOR A WALL and just a lot of gibberish on reporting crossings, but NOTHING TO SLOW THE MIGRANT CROSSINGS.

In other words, it is a BIG DEFENSE SPENDING BILL … for Ukraine and Israel and peanuts for the US border. Child slavery and Fentanyl will continue unabated as will murders by illegal immigrants. Why? Illegals rarely live near Biden, Clintons, Obamas, McConnell, Thune and other frauds in the US House of Lords (aka, Senate).

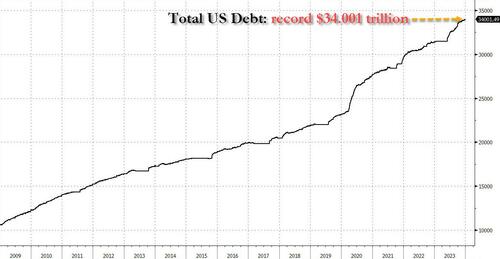

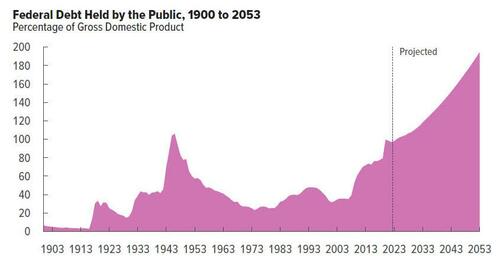

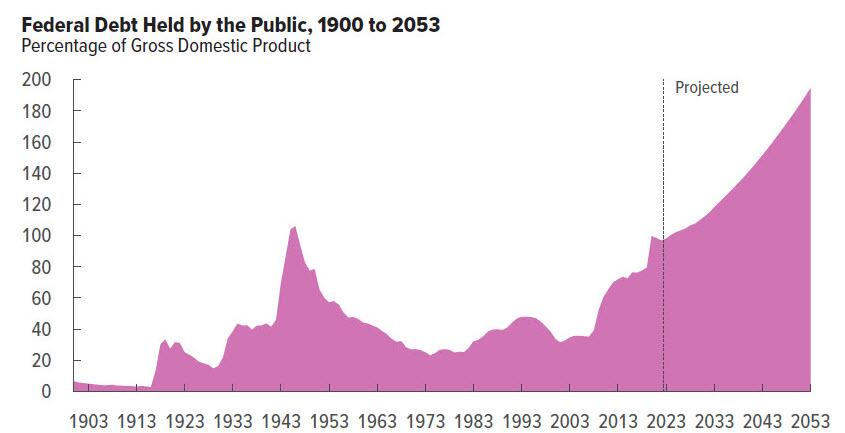

And you wonder why the US is careening off the debt cliff?

The great Will Rogers once said he never met a man he didn’t like. US President Joe Biden and Democrats have never met a spending opportunity they didn’t like (except for US border security, of course).

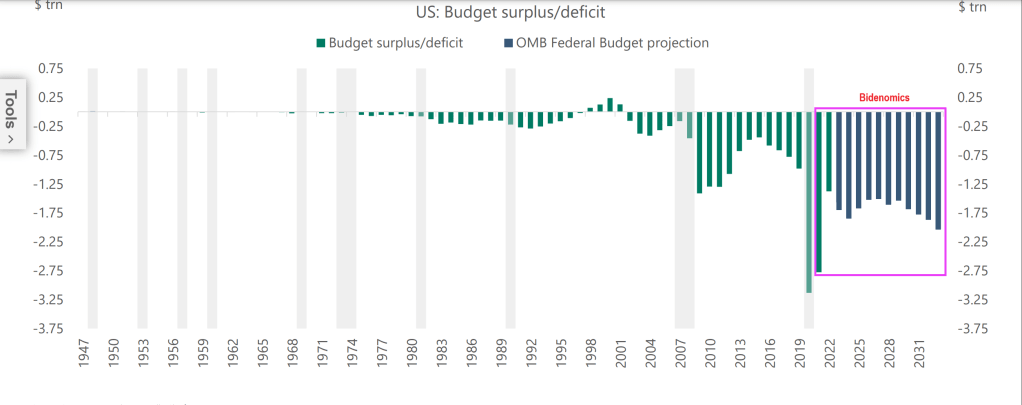

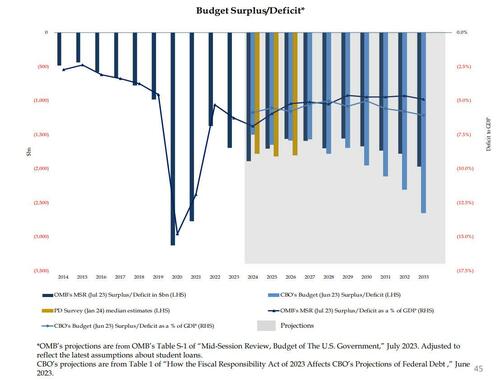

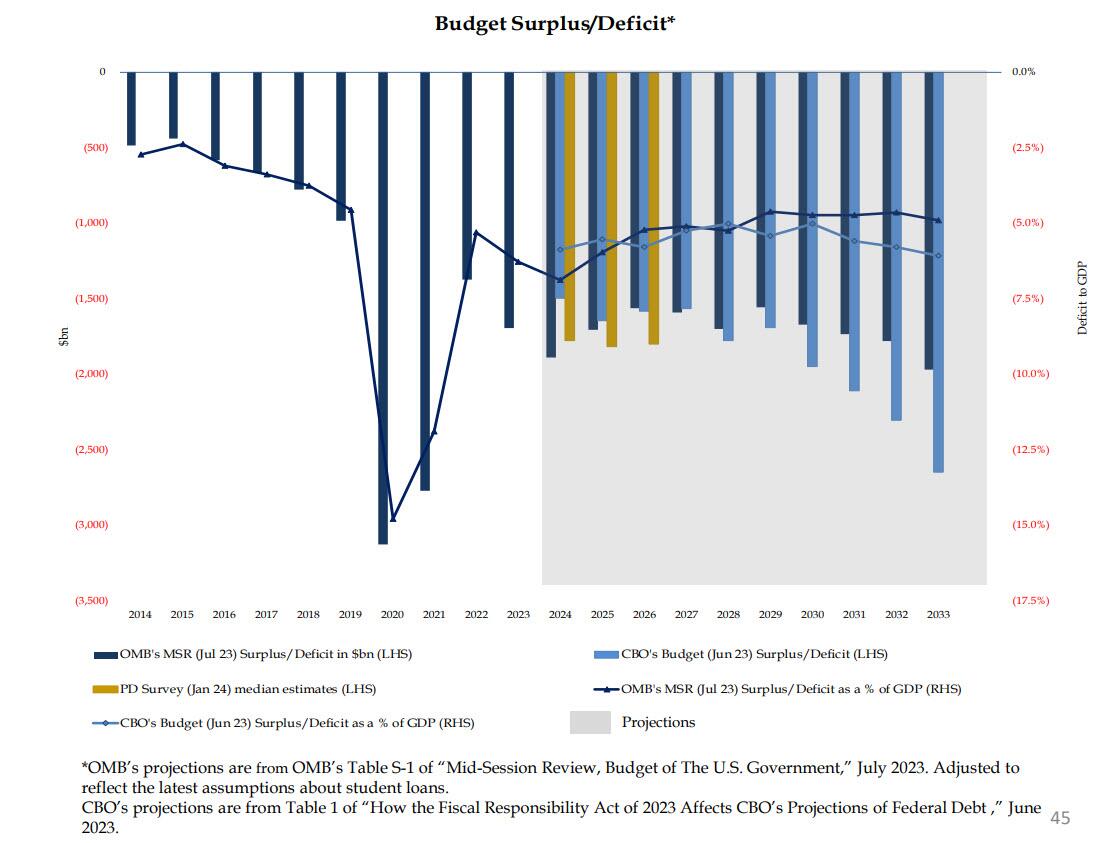

Under “Deficit Joe” Biden, Federal budget deficits have soared! And deficits are projected to grow!

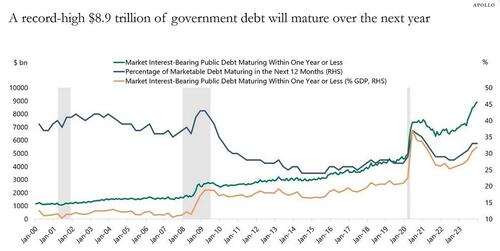

The problem, as Apollo’s gloomy chief strategist Torsten Slok points out, is that this feverish pace will only accelerate further, as a record $8.9 trillion of government debt will mature over the next year.

Meanwhile, the government budget deficit in 2024 will be $1.4 trillion according to the CBO (realistically expect this number to hit $2.0 trillion), and the Fed has been running down its balance sheet by $60 billion per month.

The bottom line is that someone will need to buy more than $10 trillion in US government bonds in 2024. That is more than one-third of US government debt outstanding. And more than one-third of US GDP.

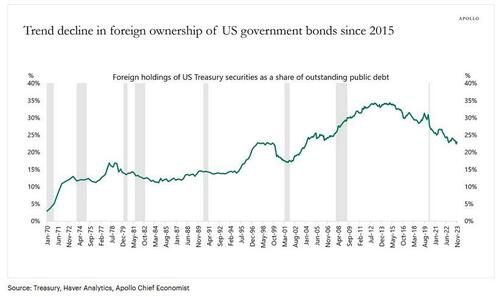

This may be a particular challenge when the biggest holders of US Treasuries, namely foreigners, continue to shrink their share.

More fundamentally, Slok muses, “interest rate-sensitive balance sheets such as households, pension, and insurance have been the biggest buyers of Treasuries in 2023, and the question is whether they will continue to buy once the Fed starts cutting rates.”

(Spoiler alert: no… but that’s what QE is for, and sooner or later, it’s coming back).

Apollo’s latest updated outlook on Treasury demand is below (pdf link).

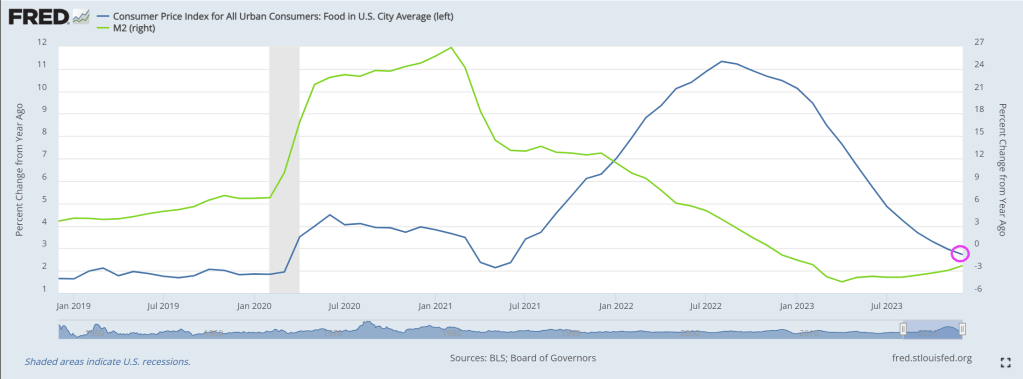

The Biden Administration which motto should be “Make Crime Great Again!” with awful crime in big cities, and millions pouring over the border, not to mention providing jobs for foreign workers and not native born Americans, is likely breathing a sigh of relief as food inflation falling to 2.7% year-over-year, still higher than pre-Covid levels under Trump. But at least food price inflation is slowing as The Fed’s money stimulus recedes.

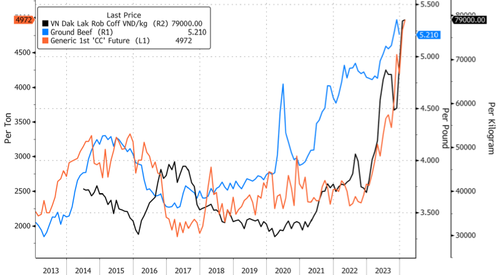

Cocoa prices climbed to a 46-year high this week in New York as concerns about dry conditions across West Africa could reduce yields for the Ivory Coast, the world’s largest producer of cocoa beans, ahead of the mid-crop in April.

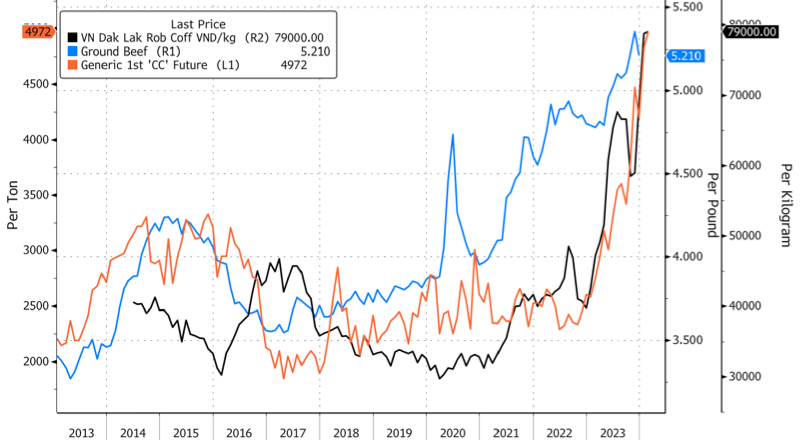

In the US, a rapidly shrinking cattle herd, now at the lowest levels in seven decades, has pushed the supermarket price of beef to a record of $5.21 per pound. Rising food prices are the central bank’s worst enemy.

To end the week, breakfast lovers will be disappointed to learn robusta bean prices in Vietnam, the world’s largest producer of the bean, are absolutely out of control.

Local robusta prices in Vietnam hit a record on Thursday, topping nearly 80,000 per kilogram.

“That’s threatening to push prices in London up further, even after the benchmark capped its own all-time high this week at $3,336 a ton,” Bloomberg said, adding the surge in prices was primarily due to farmers “hoarding” the bean.

To recap this week, cocoa bean, beef, and robusta bean prices have been marching higher.

More bad news for Biden. Even though overall food inflation has receded, voters have long memories.

“Progress on inflation has brightened the economic picture despite a slowdown in hiring and pay. Wages adjusted for inflation have improved over the past six months, and the economy looks like it’s headed toward a soft landing in the U.S. and globally,” says Nela Richardson, Chief Economist, ADP.

ADP National Employment Report

The ADP National Employment Report shows Private Sector Employment Increased by 107,000 Jobs in January; Annual Pay was Up 5.2%

Job Switching Payouts

Year-over-year pay gains for job-stayers reached 5.2 percent in January, down from 5.4 percent in December.

For job-changers, pay was up 7.2 percent, the smallest annual gain since May 2021.

Median Change in Annual Pay (ADP matched person sample) Job-Stayers 5.2%, Job-Changers 7.2%

ADP Notice

January’s report presents the scheduled annual revision of the ADP National Employment Report, which updates the data series to be consistent with the annual Quarterly Census of Employment and Wages (QCEW) benchmark data for March 2023. In addition, this revision introduces technical updates, namely, in re-weighting of ADP data to match QCEW data. The historical file was updated to reflect these revisions.

Notice Translation

ADP revises its data to match annual BLS data from March of 2023. The BLS will do the same in its annual revisions.

The BLS does not even back adjust the numbers so its historical record is bogus. And despite being incredibly lagging, the Fed makes key decisions on the data.

Job Openings Rise in December But Quits Tell the Real Story

There’s lots of meaningless chatter yesterday about job openings. However, actions speak louder than openings.

This report comes after Fed Chair Jerome Powell said “No Sugar Tonight” as in no expected rate cuts. That is, until it becomes obvious that Biden will lose the election, THEN The Fed will start cutting rates like crazy.

An example of the trash that Biden and Democrats are importing from Latin America, Africa and China. Among other sewers. I am sure that employers are lining up to hire this guy. … NOT! Correction: Biden may appoint this creep to his cabinet with the other losers.

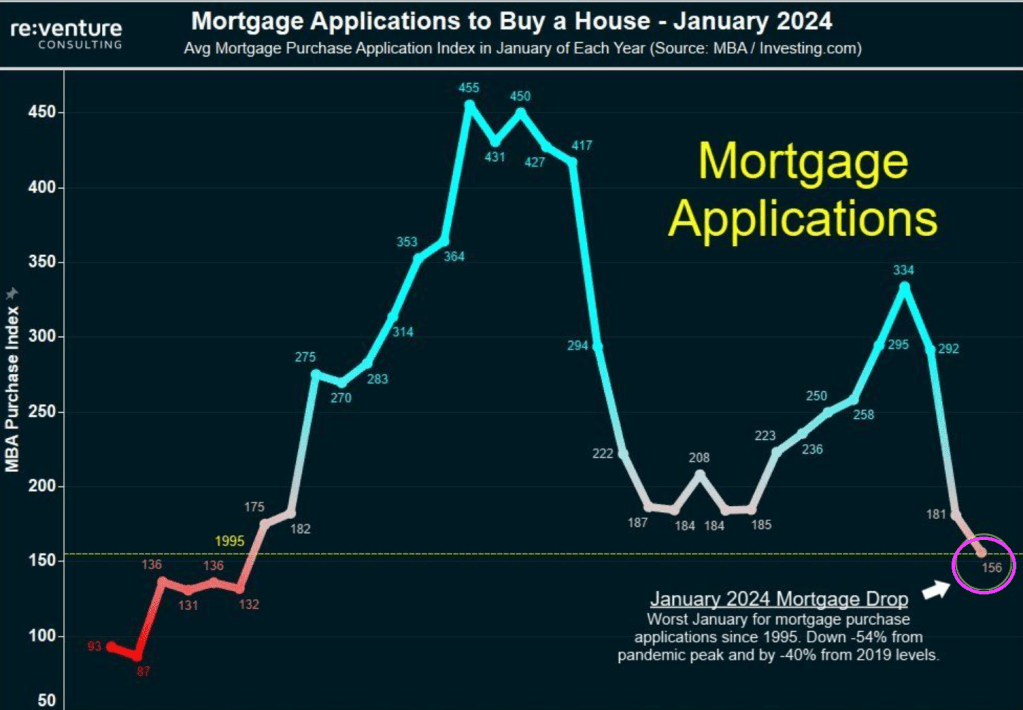

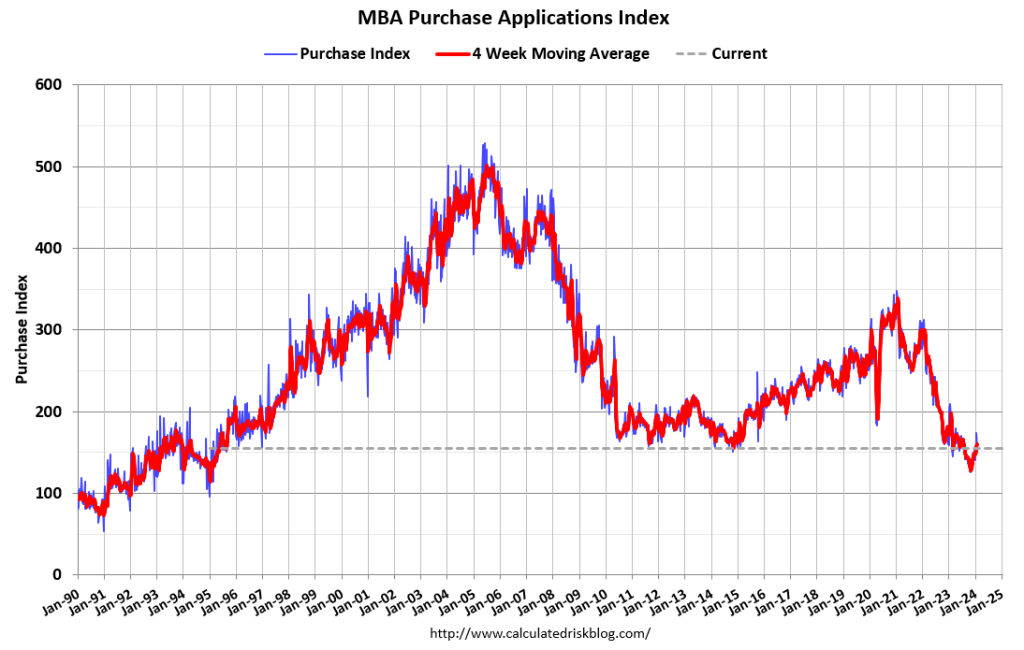

Yikes! Bidenomics is a disaster! MBA mortgage purchase applications are down 54% from Pandemic Peak. I was going to play “The Wreck of the Edmund Fitzgerald” by Gordon Lightfoot and rename it “The Wreck of The US Economy.”

Mortgage demand fell to a new 30-year low in January 2024, down 54% from the pandemic peak. Mortgage demand is down 14% over the last year and 40% from pre-pandemic levels.

Mortgage applications decreased 7.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending January 26, 2024. Last week’s results included an adjustment to account for the MLK holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 7.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 8 percent compared with the previous week. The Refinance Index increased 2 percent from the previous week and was 3 percent higher than the same week one year ago. The seasonally adjusted Purchase Index decreased 11 percent from one week earlier. The unadjusted Purchase Index increased 6 percent compared with the previous week and was 20 percent lower than the same week one year ago.

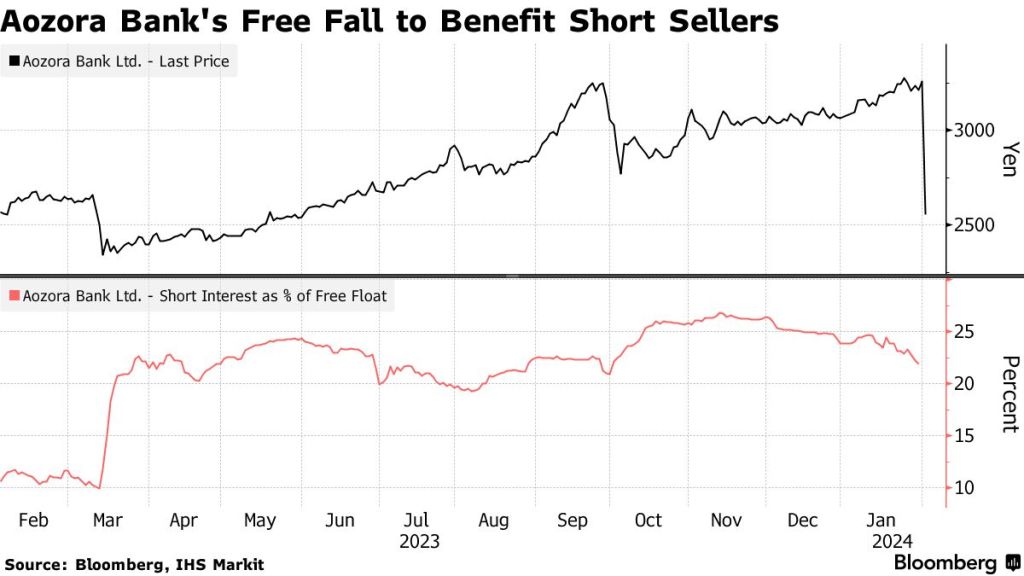

Like rows of falling dominoes, Aozora Bank, the 16th largest in Japan by market value, saw its shares plunge by 20% on Thursday after reporting a net loss of 28 billion yen ($191 million) for the fiscal year. This was in stark contrast to its earlier projection of a 24 billion yen profit.

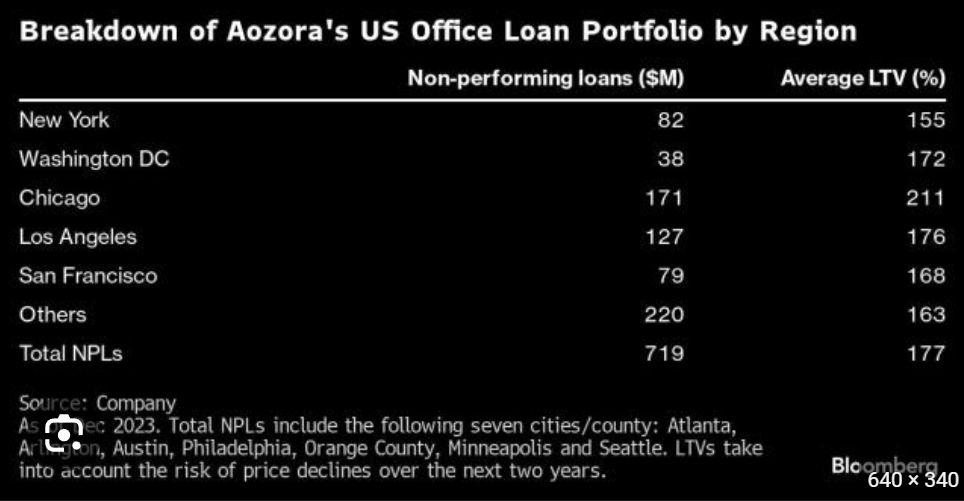

Aozora wrote down the value of its non-performing office loans by 58%, including a 63% reduction in Chicago and between 51% and 59% in New York, Washington D.C., Los Angeles, and San Francisco – all of these cities are plagued with violent crime and controlled by radical Democrats.

In total, the bank’s US office loans were about 6.6% of its portfolio, or approximately $1.89 billion. It said 21 office loans worth $719 million were classified as non-performing, and as a result it increased its loan-loss reserve ratio on US offices to 18.8% from 9.1%.

“It’s a shock,” said Tomoichiro Kubota, a senior market analyst at Matsui Securities Co., adding, “The expectation was the worst was over and that the bank had set aside enough provisions.” Guess not.

Far markets, this was another flashing red warning sign that not only is a tsunami of office loan defaults still on the horizon, but that banks continue to be woefully underprovisioned for the coming bloodbath.

“This is a huge issue that the market has to reckon with,” said Harold Bordwin, a principal at Keen-Summit Capital Partners LLC in New York, specializing in renegotiating distressed properties.

Bordwin said, “Banks’ balance sheets aren’t accounting for the fact that there’s lots of real estate on there that’s not going to pay off at maturity.”

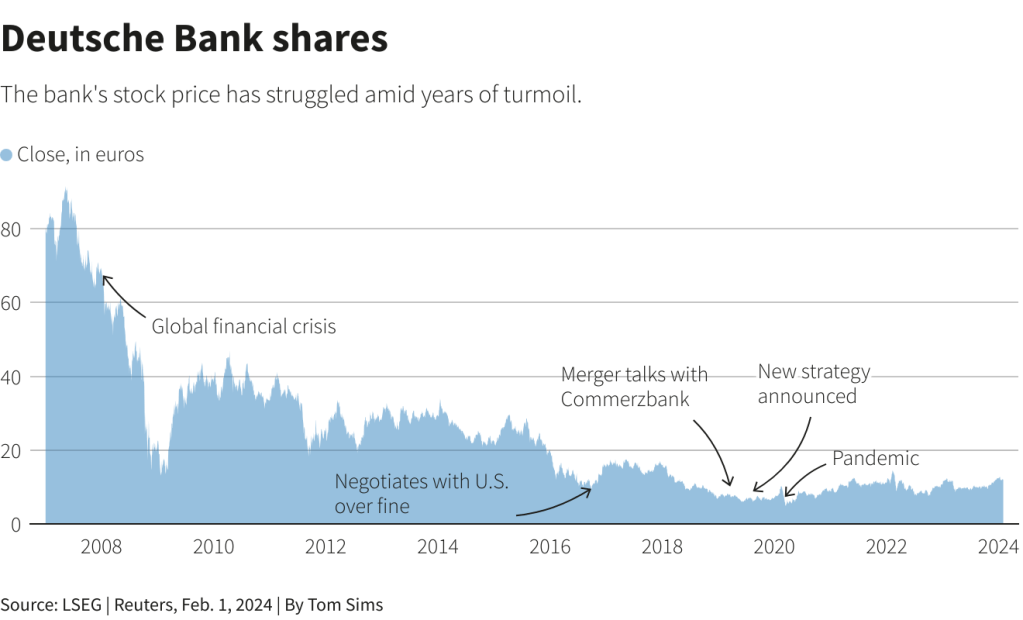

Besides New York Community Bancorp and Aozora Bank, Deutsche Bank noted in fourth-quarter results:

“Interest rate environment remains key driver for refinancing risk and potential [credit-loss provisions] in 2024 especially in office, with further drivers being ongoing sponsor support and expiring rental agreements.”

Fed chair Powell delivered bad news for the CRE world in yesterday’s FOMC meeting, warning that a March rate cut isn’t happening (absent a shock of course). Perhaps most notably, the Fed removed the following sentence from the FOMC statement: “The US banking system is sound and resilient.” Cynics asked why the Fed no longer sees “the US banking system is sound and resilient” – is it a signal of rumblings in the economy near-term, or was it just a lie before, and now that bank dominoes are again falling, will Powell be forced to trot it back out?

Where will this lead? Likely more bank and pension fund bailouts. You didn’t really believe that hype about the Dodd-Frank banking legislation that there will never be another bank bailout did, you??

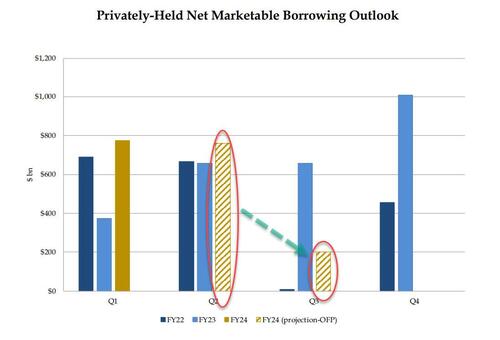

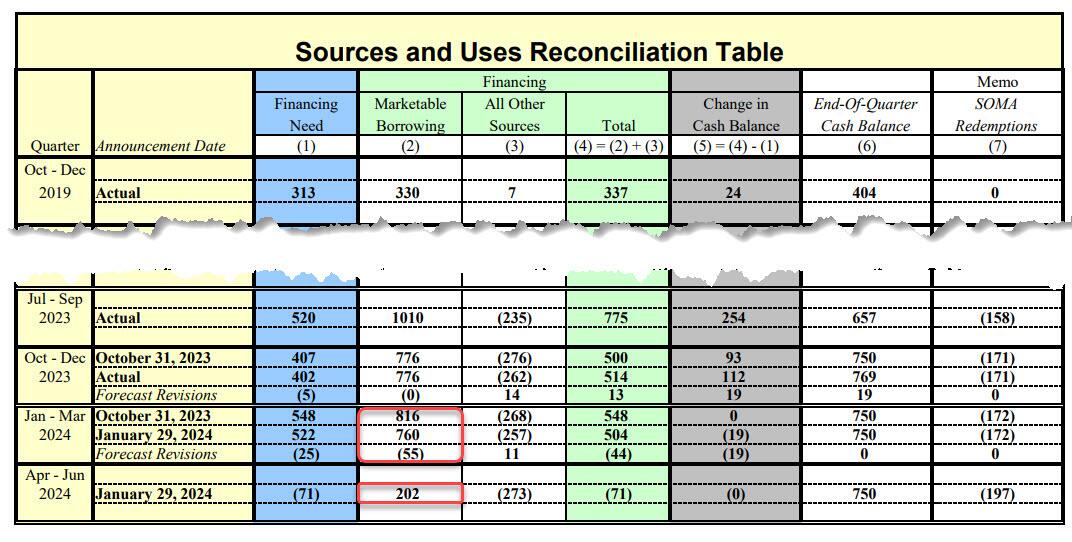

Constitution Avenue in Washington DC is actually becoming Tobacco Road. No, not the dysfunctional family of Georgia sharecroppers during the Great Depression, but the Treasury Borrowing Advisory Committee (TBAC).

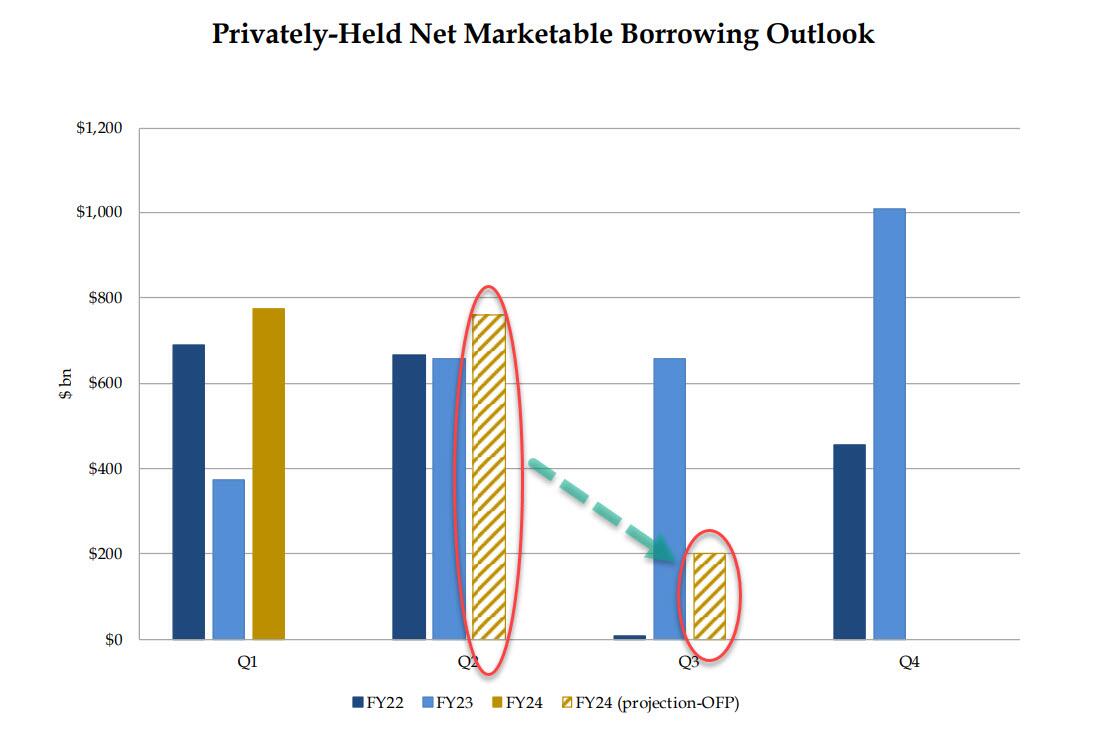

… yields tumbled as this was viewed as an aggressively dovish outlook on the future of i) the US fiscal deficit and ii) the debt needed to fund said deficit. Here is another way of visualizing the US historical and projected marketable debt funding needs:

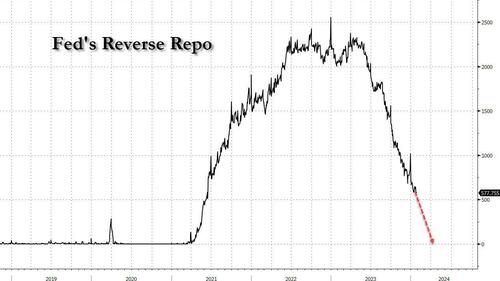

Commenting on this surprise drop in expected borrowing, on Monday we said that “the numbers also mean that the Reverse Repo facility will be fully drained by Q2, and we expect that on Wednesday we will learn that the bulk of the reduction in Q1 and Q2 estimates will be due to sharply lower Bill issuance for one simple reason: there is just no more Reverse Repo cash to buy it all.“

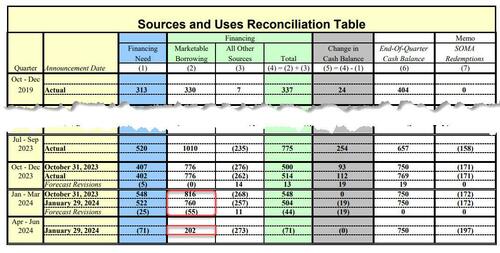

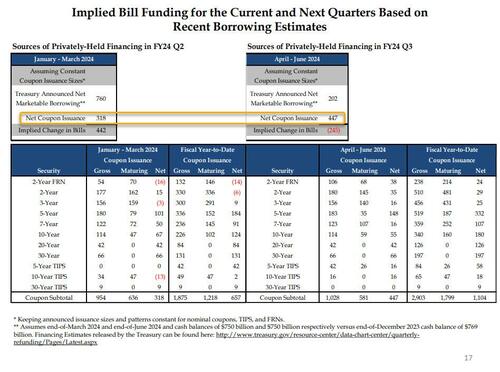

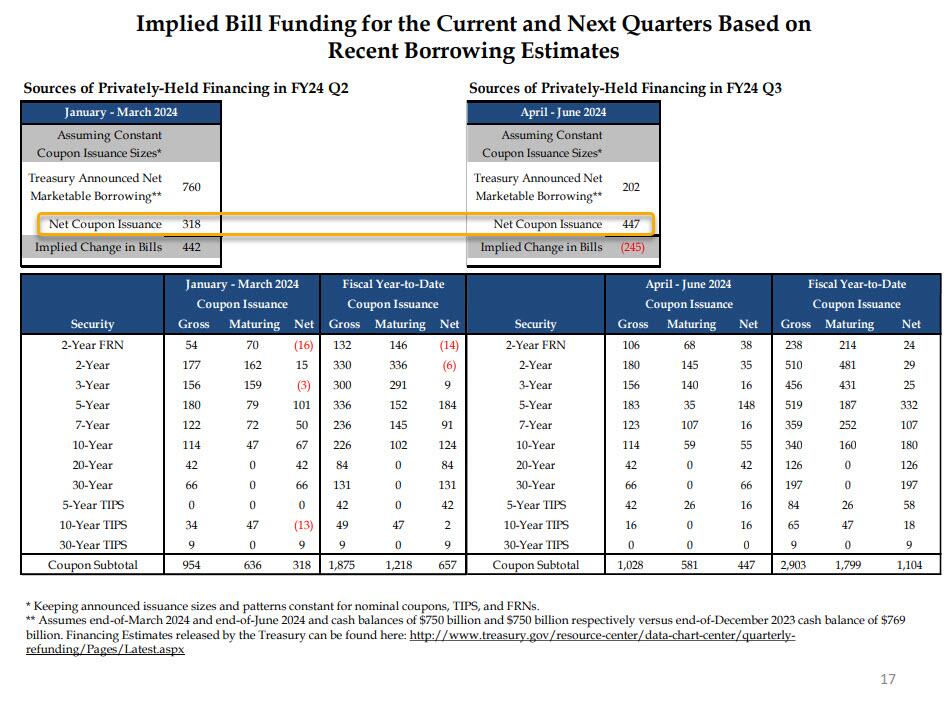

Boy, were we right: earlier today, in the Treasury’s presentation to the Treasury Borrowing Advisory Committee (TBAC) as part of the Quarterly Refunding, Janet Yellen revealed what the composition of this sharp drop in Q2 funding needs would be. As we expected, it was all bills!

In fact, as the chart below – which we have dubbed the scariest chart in the Treasury’s presentation to TBAC today (link here) – shows, with Bills expected to fund some $442 Billion of the $760BN funding deficit in the Jan-March quarter (the balance of $318BN funded by coupons), in Q2 the Treasury now anticipates a $245BN DECLINE in net Bills outstanding (i.e., not only no incremental Bill funding but a quarter trillion maturity in Bills outstanding). In other words, while we expected a “sharply lower” Bill issuance in Q2, the Treasury is actually expecting a $245BN drawdown in Bills.

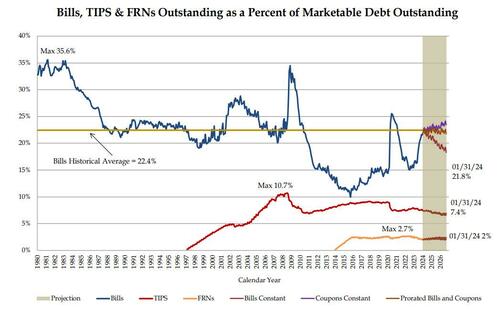

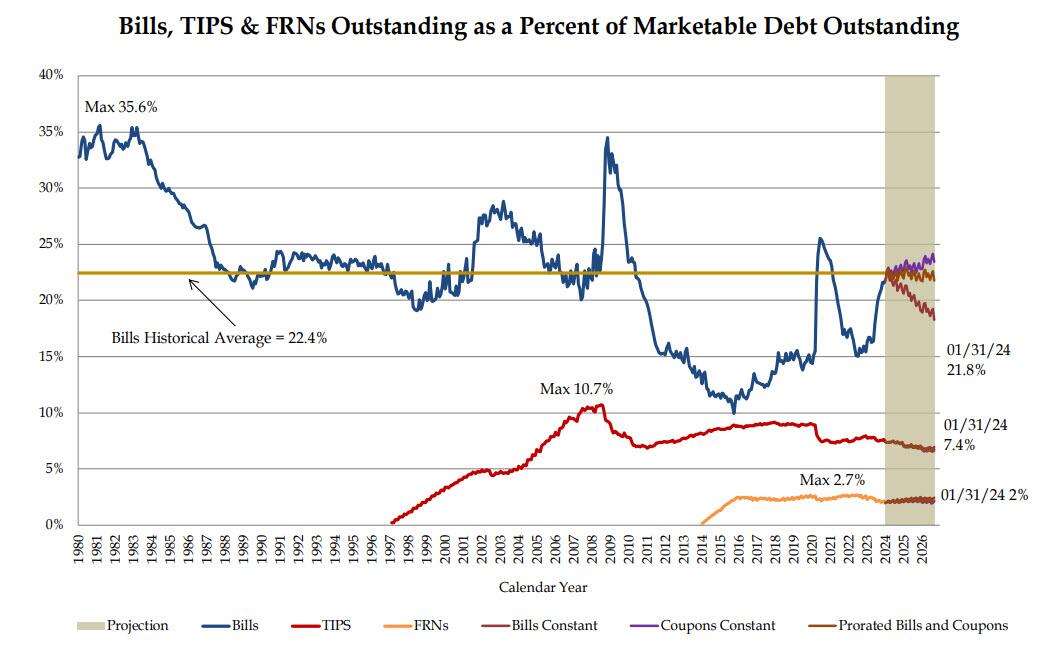

But wait, there’s more: because while the market was expecting some pro rata decline in coupon issuance to go with the slide in net Bills (we were not) in Q2 to justify the sharp drop in long-end yields, it was not meant to be. In fact, just the opposite, because as highlighted in the chart above, net Coupon issuance in Q2 is actually expected to increase by $130BN to $447BN from $318BN in Q1. This is a huge shift in higher duration supply, and is hardly what all those who were buying 10Y bonds on Monday were expecting, and yes, that too was to be expected: with Bills now well above the “comfortable” ceiling of 20% as a percentage of total debt outstanding, the Treasury had no choice but to roll it back, especially since the Reverse Repo is already mostly drained. And sure enough, in its presentation, the Treasury no longer anticipates a flood of Bill issuance in the future.

That’s not all: while the Treasury said it does “not anticipate needing to make any further increases in nominal coupon or FRN auction sizes, beyond those being announced today, for at least the next several quarters”, the TBAC politely disagreed, stating that “it may be appropriate over time to consider incremental increases in coupon issuance depending on how the current uncertainty regarding borrowing needs evolves” (translation: as the need to bribe the population with more fiscal stimmies ahead of November rises, so will borrowing needs).

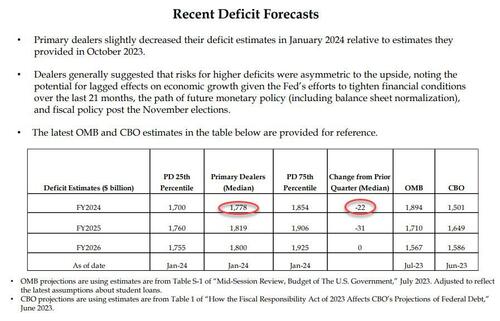

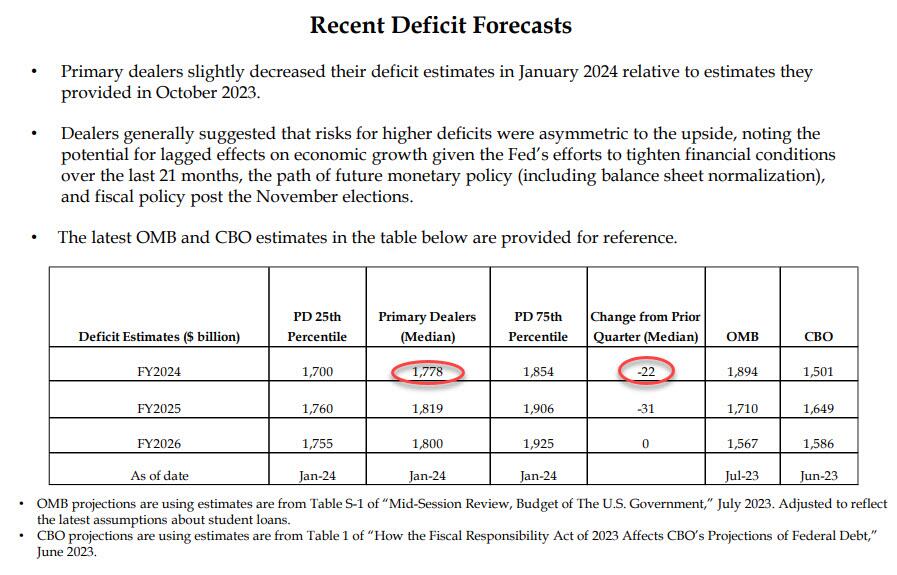

As for any naive expectations that any decline in issuance in structural instead of merely shifting away from Bills to Coupons, we have some more bad news: as the table below confirms, the Primary Dealer estimate of the US 2024 budget deficit dropped just $22BN in the past quarter, from $1.8 trillion to $1.778 trillion, a meaningless change (expect this number to rise sharply as the full brunt of fiscal stimulus in an election year become visible).

As for the bigger picture, well you can listen to either the Primary Dealers…

… or the CBO:

Both reach the same sad conclusion, the same one voiced by Nassim Taleb on Monday when he said that “we need something to come in from the outside, or maybe some kind of miracle…. This makes me kind of gloomy about the entire political system in the Western world.”

Sorry, Nassim, no miracles… just lots and lots of money printing coming.

And speaking of money printing, the fact that Bill issuance is about to grind to a halt in Q2 means that, just as we expected, reverse repo balances will tumble in the remaining two months of Q1…

… bringing it effectively to zero (which means the Treasury’s stock market liquidity pump is now almost drained), at which point the Fed will have to take over and taper QT as the alternative would be draining some $100BN in reserves every month at a time when total Fed reserves are already at the level which Waller hinted may be the infamous LoLCR floor which is a hard constraint at “10-11% of GDP.” The alternative is simple: a stock market crash just months before the November election, hardly the stuff Biden’s handlers or the anti-Trump Deep State would approve of.

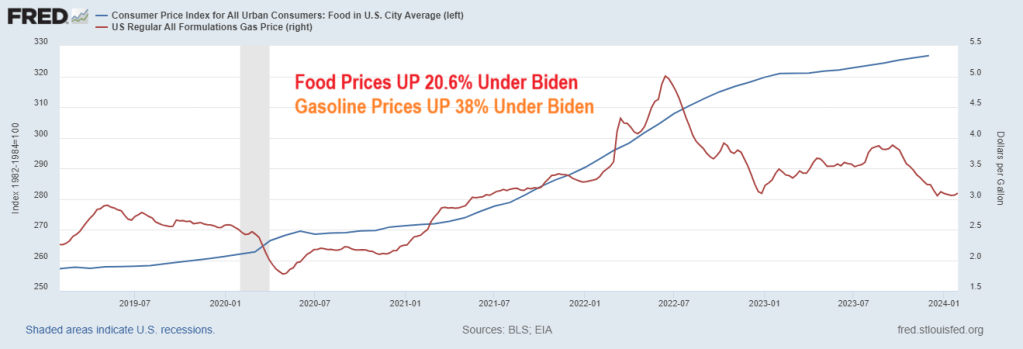

Treasury Secretary Janet Yellen just admitted what the rest of Americans already knew: high prices are here to stay. Example? Food prices (CPI) are up over 20% under Inflation Joe while gasoline prices are up 38% under Clueless Joe.

On the housing front, the Case-Shiller National Home Price Index is up 33.2% under Biden. And Freddie Mac’s 3-year mortgage rate is up 154% under Biden’s leadership (c’mon man! Obama is pulling the strings on Puppet Joe).

For months officials in the Biden administration have falsely claimed prices on everyday goods and services were going down. In reality, they’re getting more expensive at a slower pace.

During a briefing at the White House last week, Press Secretary Karine Jean Pierre had trouble explaining complaints from Biden when he purchased a smoothie that cost $6.

“Last Friday, the president was at a coffee shop in Pennsylvania, and he seemed to be surprised that the smoothie was $6 and how expensive it was,” a reporter asked. “I’m curious. So is the president now realizing the costs that Americans are bearing?”

“So, look, when he went over to you all, to the press corps, he was having a good time, right? And offered, as you know, offered to buy them coffee,” Jean Pierre responded. “There was a big group there, and he made sure everyone got coffee and pastries. So I just want to make that really clear.”

That is wonderful, KJP! The White House Press Corps got free coffee and pastries! Yippee!!!

But the rest of us in America are suffering from Bidenomics and inflation. Like food prices having risen 21% under Biden, gasoline prices UP 38%, home prices UP 33.2% and mortgage rates UP 154%.

A Blackstone-owned Manhattan office tower with a $308 million mortgage is being marketed at a discounted rate of $150 million, representing a 50% reduction. The special servicer, Midland Loan Services, has enlisted Jones Lang LaSalle Inc. to facilitate the sale of the tower at 1740 Broadway. The bundled debt, included in a commercial mortgage-backed security, is marked with a 50% discount. In April, the tower was appraised at $175 million, a substantial 71% decline from its $605 million valuation in 2014 when the mortgage originated.

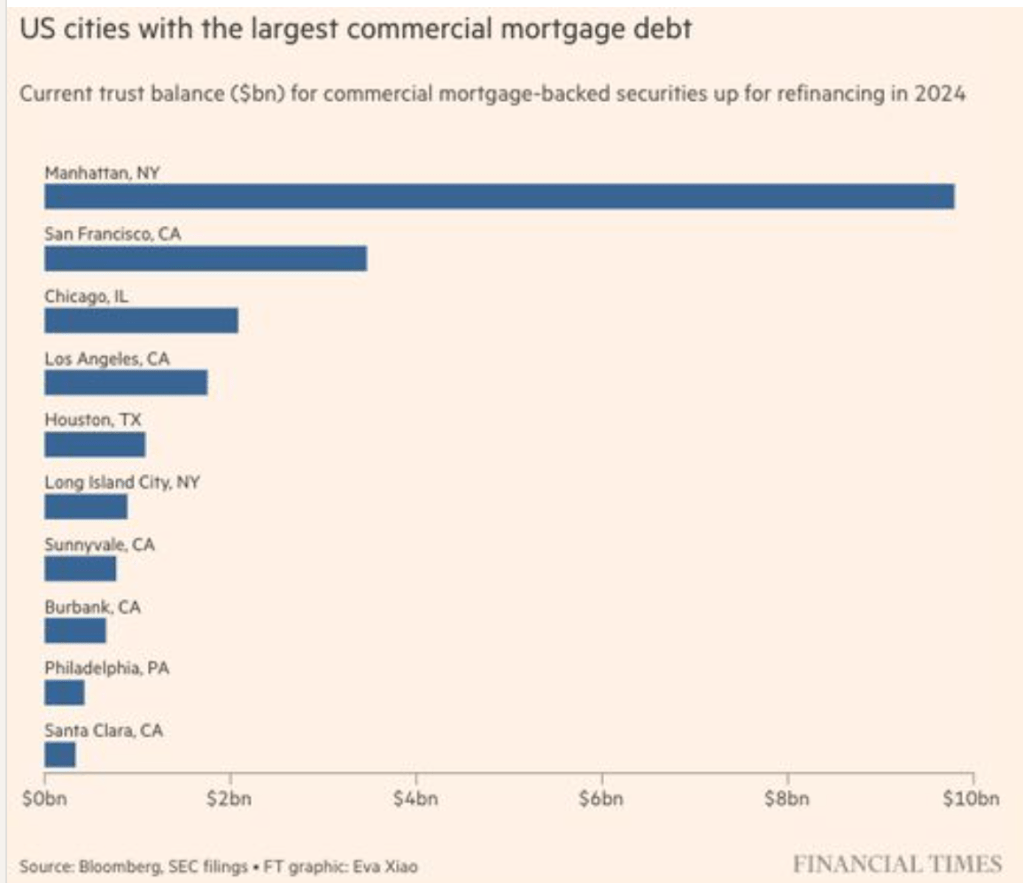

To put this into perspective, a new report by the Mortgage Bankers Association data, shows $117 billion in CRE office debt needs to be repaid or refinanced this year. Much of this debt is concentrated in major cities such as Manhattan, San Francisco, Chicago, and Los Angeles.

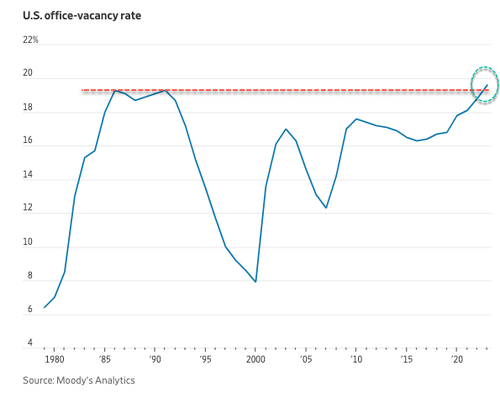

Compounding (or CONFOUNDING) the problem is the near 20% office vacancy rate.

Here is Fed Chair Jerome Powell who replaced now Treasury Secretary Janet Yellen.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.