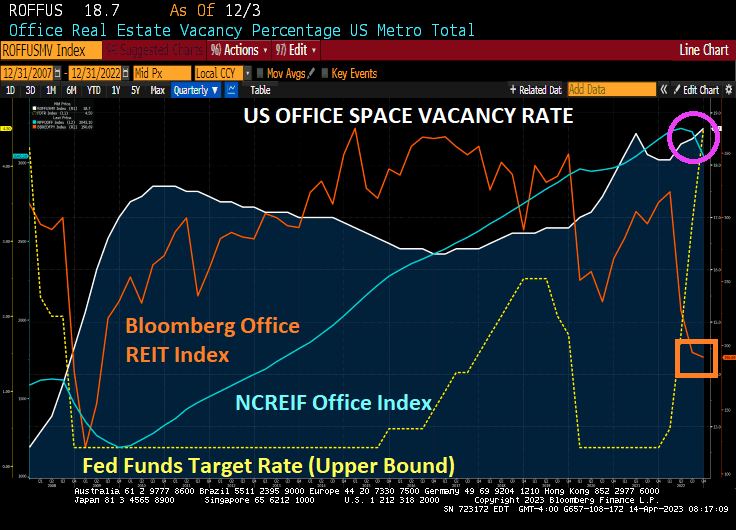

- Office vacancy rate in the US has climbed to 20.2% in 2023

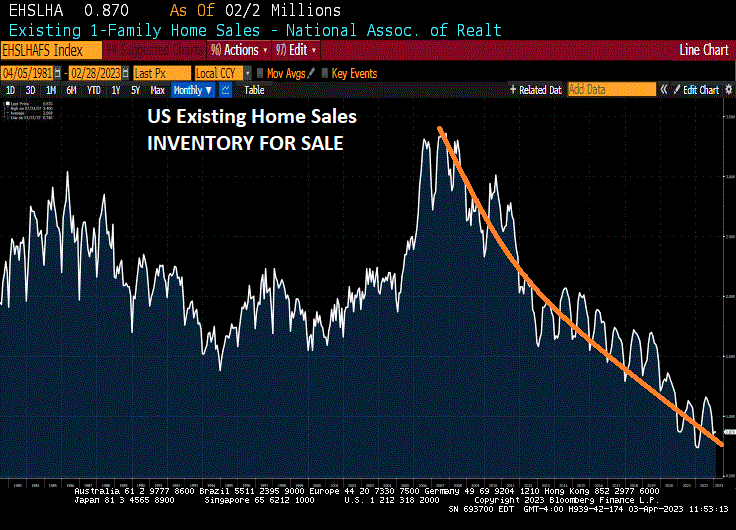

- Financing for residential building is tepid despite demand

The Covid economic shutdowns have a disastrous effect on small businesses as we know. But office space is really getting crushed in terms of vacancy rates. In fact, it is so bad the investor Kyle Bass is suggesting that office space be torn down across the US much in the same way that FDR’s Agriculture Secretary Henry Wallace ordered the mass execution of hogs in order to drive up prices in a deflationary economy.

(Bloomberg) Kyle Bass has some advice for real estate investors: Tear it down.

The founder of Dallas-based Hayman Capital Management says office buildings in cities need to be demolished because demand isn’t returning and it’s impractical to turn most towers into apartments.

“It’s one asset class that just has to get redone, and redone meaning demolished,” said Bass.

The Dallas-based investor shot to fame more than a decade ago betting against subprime mortgages before the US housing collapse. He’s since pushed a series of contrarian investments that have occasionally burned investors such as predicting the collapse of Japanese government debt and Hong Kong’s dollar.

NCREIF’s office index is starting to decline, but Bloomberg’s Office REIT index (orange line) is really showing the pain being felt in the office market. But just wait to see what happens IF the market takes Bass’ advice and starts removing supply to help increase values. Unfortunately, my chart is only up through December 2022 and office vacancies have worsened in 2023 to a mind-boggling 20.2%.

In a classic Bill Lumbergh move (he was the office manager of Initech in Dallas Texas), JPMorgan now requires managing directors return to office 5 days a week and ‘be visible on the floor’ or else face ‘corrective action’.

An additional non-Bill Lumbergh issue is the rising crime in American cities causing companies like Whole Foods to leave their San Francisco (tenderloin district) location because 1) workers feel unsafe and 2) shop lifting is out of control. Even Washington DC where a large number of office building are leased by The Federal government is experiencing a boom in crime (particularly carjackings). And don’t get me started on Chicago (see Hey Jackass! for a Chicago crime map).

The face of micro-managing office managers, Bill Lumbergh. Or is this now JPMC’s CEO Jaime Dimon?

You must be logged in to post a comment.