As the Biden Administration touts “affordable housing,” we are seeing the 30-year mortgage rate rise above 7% as The Federal Reserve fights inflation … caused by the Biden Administration. Meanwhile, US home prices are falling.

The Biden Administration launched a war on domestic energy production, resulting in crude oil prices rising 74% under Biden and regular gasoline prices rising 62.4%.

As Biden pleaded with OPEC to increase oil production, he was embarrassingly rejected. Hence, West Texas Crude Oil prices have begun to rise again along with gasoline prices (pink box).

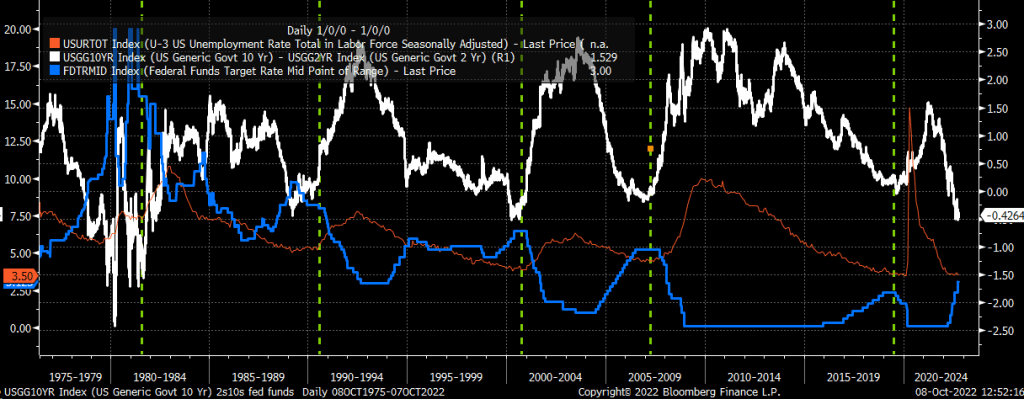

How about unemployment and the 10yr-2yr yield curve?

Yesterday, I told my family “The good news is that Rotolo’s Pizza tastes even better reheated in the morning. The bad news? I ate the only two piece left.”

Which brings me to the September jobs report. The good news is that 263k jobs were added to the US economy. That means 10,521k jobs have been added in the 21 months under Biden! (Bear in mind that 12,100k jobs were added in the 7 months under Trump following the Covid economic shutdown, yet no media outlet trumpeted that accomplishment).

The bad news? While nominal average hourly earnings grew by 5% YoY, when I subtract Bidenflation from that number I get -3.06% growth. Or should I say that REAL wages are shrinking under Biden.

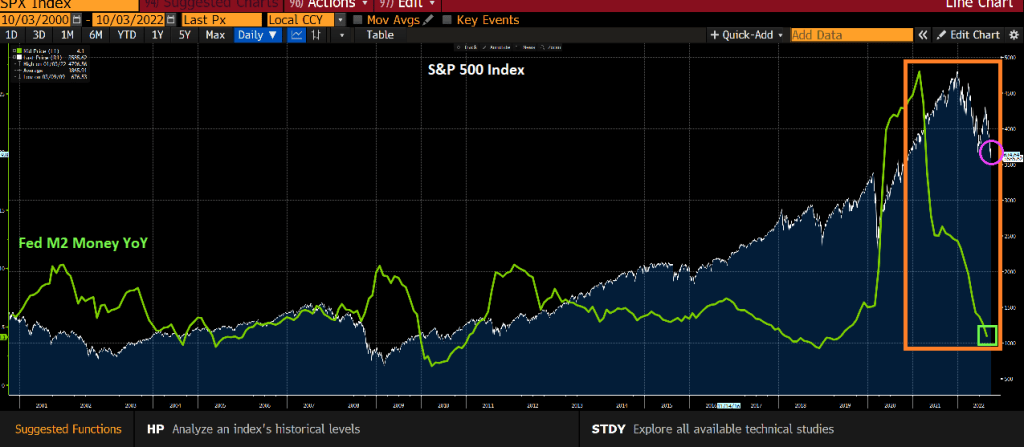

Now for the “Biden Miracle” of jobs being added. Here is a chart of NFP jobs added (white line) against M2 Money and headline inflation. Both The Fed and the Federal government pumped trillions into the economy leading to the highest inflation rate in 40 years. Once governments stopped with their Covid shutdown nonsense, jobs would return regardless of who was President. BUT Federal spending and Fed money printing went off the rails in early 2020.

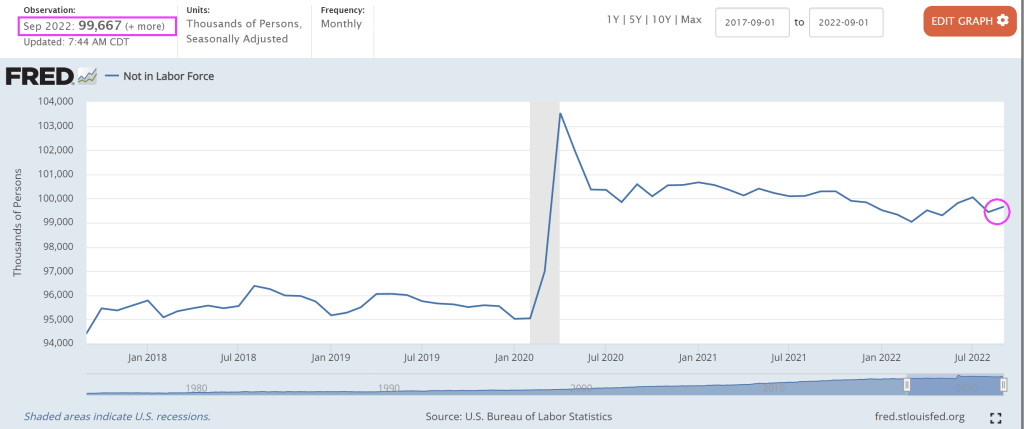

As Paul Harvey used to say, “Here is the rest of the story.” Labor force participation fell in September and the U-3 unemployment rate fell slightly to 3.5%.

But labor force dropouts increased leading U-3 unemployment to decline. The number of people NOT in the labor force grew to nearly 100 million. Nothing has been the same since Covid.

So what will The Fed do? According to Fed Funds Futures data (WIRP), The Fed will keep raising rates until March ’23 then slowly start lowering interest rates again.

And with that “positive” jobs report, The Dow is down almost -500 points and the NASDAQ is down over -3%.

And with Fed tightening, we are seeing a collapse in M2 money supply.

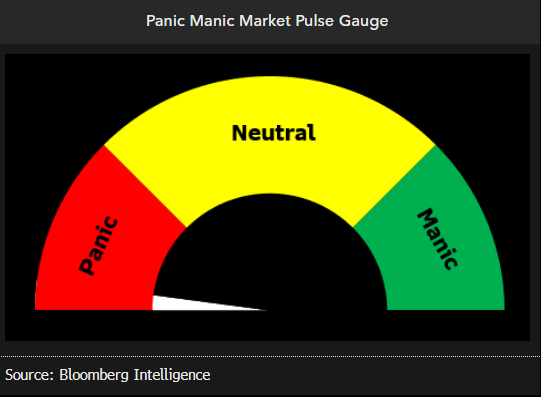

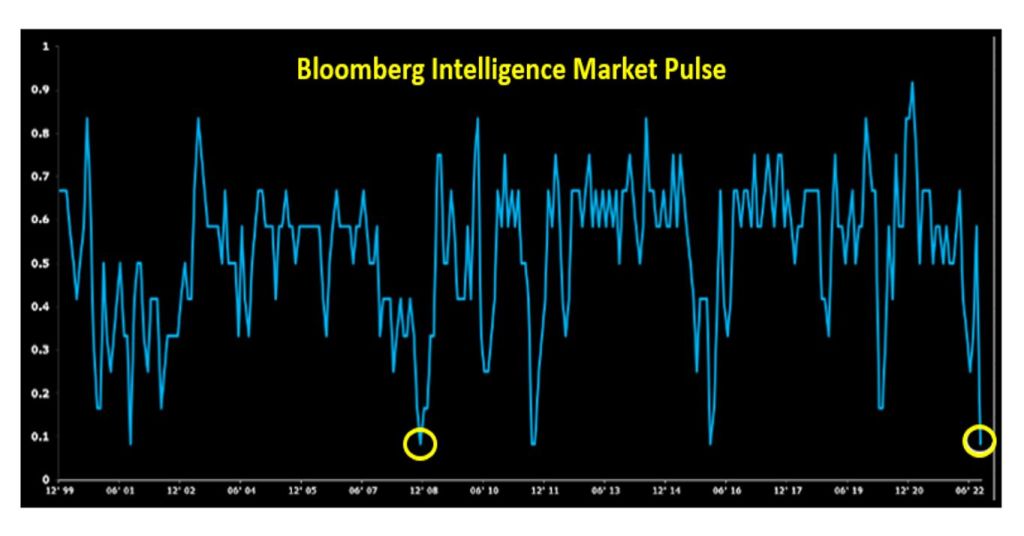

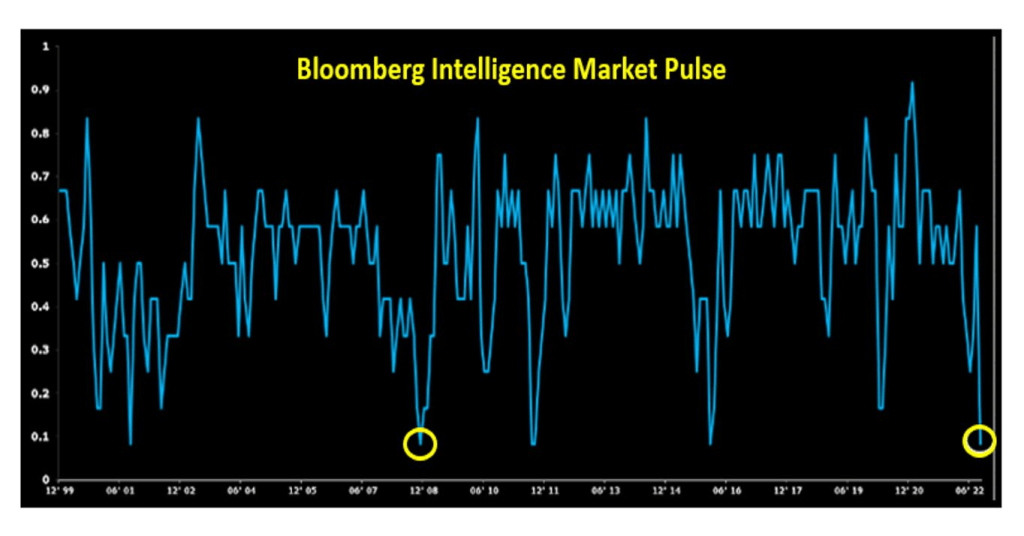

Bloomberg’s market pulse gauge is signalling panic.

The Bloomberg market pulse index quantifies sentiment using 6 factors — price breadth, pairwise correlation, low vol performance, defensive vs. cyclical sector performance, high vs. low leverage performance and high yield spreads.

What do we have? Regular gasoline prices are UP 61.4% under Biden, the strategic petroleum reserve is DOWN -35% before Biden’s latest release of another 10 million barrels. Foodstuffs are UP 50% under Clueless Joe, and heating oil futures are UP 130% under dementia Joe.

And thanks to free-spending Joe, Nancy and Chuckie, US public debt is at $31.1 TRILLION. That is ANOTHER 12% in national debt under the 4 Horsemen of the Economic Apocalypse.

For an additional 12% in national debt (to be paid by our children and grandchildren), we have crippling inflation.

Challenger US Job Cut Announcements for September rose 67.6%, the highest since … Covid-19 outbreak in early 2020. This comes after the JOLTS (job openings) fell the most since … Covid-19.

This index quantifies sentiment using 6 factors — price breadth, pairwise correlation, low vol perf, defensive vs. cyclical sector perf, high vs. low leverage perf and high yield spreads.

In addition to creating the highest inflation rate in 40 years, we are now seeing the highest mortgage rate in 16 years. I feel like we are all on a chain gang.

(Bloomberg) — US mortgage rates jumped to a 16-year high of 6.75%, marking the seventh-straight weekly increase and spurring the worst slump in home loan applications since the depths of the pandemic.

In fact, mortgage application just fell to the lowest level since May 1997.

The contract rate on a 30-year fixed mortgage rose nearly a quarter percentage point in the last week of September, according to Mortgage Bankers Association data released Wednesday. The steady string of increases in mortgage rates resulted in a more than 14% slump last week in applications to purchase or refinance a home.

Over the past seven weeks, mortgage rates have soared 1.30 percentage points, the largest surge over a comparable period since 2003 and illustrating the abrupt upswing in borrowing costs as the Federal Reserve intensifies its inflation fight.

The effective 30-year fixed rate, which includes the effects of compounding, topped 7% in the period ended Sept. 30, also the highest since 2006.

The Refinance Index decreased 18 percent from the previous week and was 86 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 13 percent from one week earlier. The unadjusted Purchase Index decreased 13 percent compared with the previous week and was 37 percent lower than the same week one year ago.

Here is today’s table of MBA mortgage applications and its ugly.

Unfortunately for the US chain gang, gasoline prices are rising again as the US drains its petroleum reserve. Because, that’s the way … uh-huh … they like.

On the real estate side, Bankrate’s 30-year mortgage rate dropped to 6.85% as the 10-year US Treasury yield drops.

On the home price front, according to the Black Knight Home Price Index (HPI), median home prices fell 0.98% in August, only marginally better than July’s upwardly revised 1.05% monthly decline July. August 2022 marked the largest single-month price declines seen since January 2009 and rank among the eight largest on record. The monthly rate of home price decline is now rivaling that seen during the Great Recession – the question is how long it will continue to do so, and how far off peaks prices will fall.

Now, will The Fed pivot to correct the plunging M2 Money growth?

As I frequently told my investment and fixed-income securities students at Chicago, Ohio State and George Mason University, any 10 basis point change in the US Treasury 10-year yield is significant.

But how about today’s 20 basis point decline in the US Treasury 10-year yield?

The UK’s 10-year yield is down even more at -24.1 basis points. Germany is down -18 bps and France is down -10.3 bps.

Speaking of credit default swaps, Credit Suisse is back to financial crisis levels while UBS and Deutsche Bank are not … yet.

With all the turbulence in markets thanks to the war in Ukraine and Biden’s green energy mandates and spending (not to mention Statists like Klaus Schwab screaming about a Great Reset), I was reminiscing about more simple times.

New CEO Koerner sought to reassure employees in Friday memo

Shares fall to a fresh record low, gauge of credit risk rises

It is like the Lehman Brothers debacle in 2008 all over again.

(Bloomberg) — Credit Suisse Group AG was plunged into fresh market turmoil after Chief Executive Officer Ulrich Koerner’s attempts to reassure employees and investors backfired, adding to uncertainty surrounding the bank.

The stock, which had already more than halved this year before Monday’s sell-off, fell as much as 12% in Zurich trading to a record low that values the firm at less than $10 billion. That was accompanied by a spike in the cost to insure the bank’s debt against default, which jumped to its highest ever.

Koerner, for the second time in as many weeks, had sought to calm employees and the markets with a memo late Friday stressing the bank’s liquidity and capital strength. Instead, it focused attention on the dramatic recent moves in the firm’s stock price and credit spreads, and investors rushed for the exit when trading reopened after the weekend.

One notable difference between 2008 and today is that Credit Suisse’s equity was flying high in June 2007 then crashed a the global banking crisis went into full motion. We then saw Credit Suisse’s credit default swaps soar in early 2009. But today Credit Suisse’s equity is a pale imitation of its former self, but its credit default swap is now higher than it was at its peak in early 2009.

Credit Suisse is now trading lower than its European rival Deutsche Bank (aka, The Teutonic Titanic).

Yes, this brings back sickening memories of the 2008-2009 global financial crisis. Let’s see how The Federal Reserve, ECB and Bank of Switzerland handle this debacle, particularly with M2 Money growth so low.

It appears that we are in another Lehman debacle. Or should I say “Lemur Bros.”

You must be logged in to post a comment.