I read over the weekend that the Biden Administration was planning to unleash its army of social influencers on us to hype Biden’s economic accomplishments before the Presidential election. I am not one of his preferred social influencers. In fact, the US economy is slippin’ into darkness under Biden.

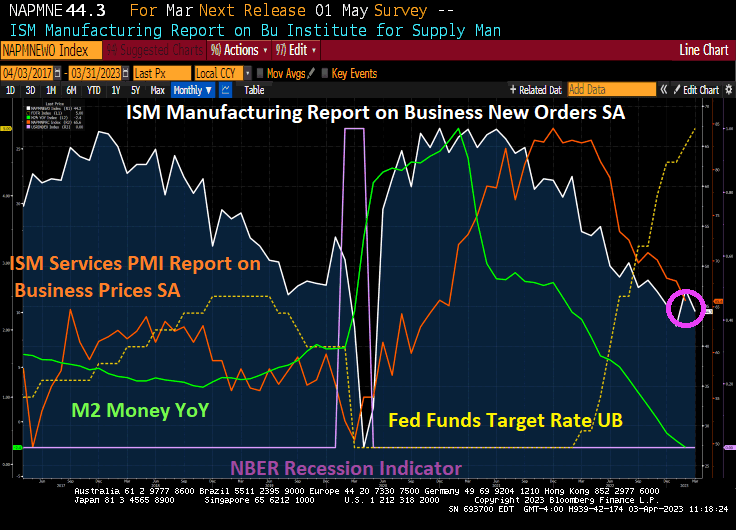

An example is ISM Manufacturing PMI which has declined to a level typically seen in prior recessions.

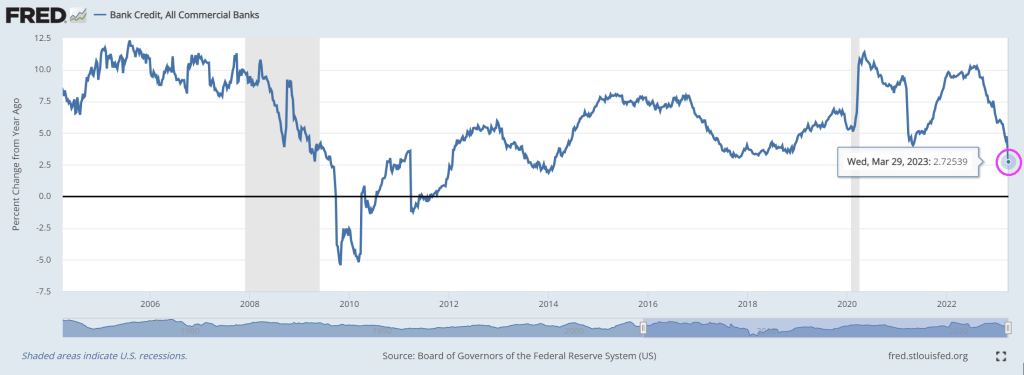

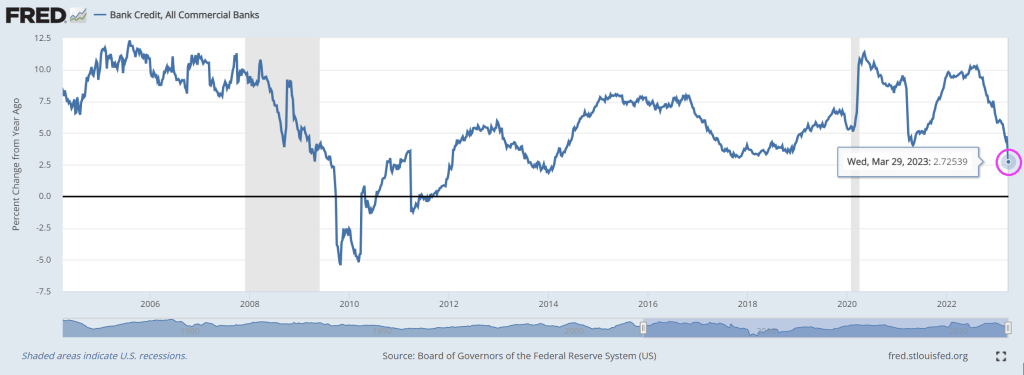

And then we have US bank credit growth which just crashed to the slowest growth rate since 2014.

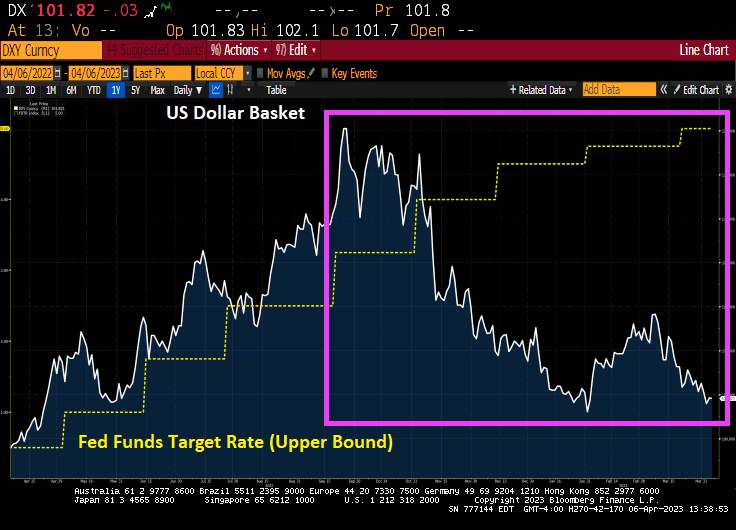

The Fed is returning to rate low-riding as the US economy slips into recession,

You must be logged in to post a comment.