The Federal government reaction to the Covid outbreak in early 2020 included massive monetary stimulus, Federal government spendathons and Biden’s green energy policies have resulted in a sizzling 8.5% inflation rate (update on Monday morning).

The problem is that The Federal Reserve is far behind the inflation curve with their target rate at only 2.5%. And The Fed’s balance sheet remains near $9 TRILLION in assets held.

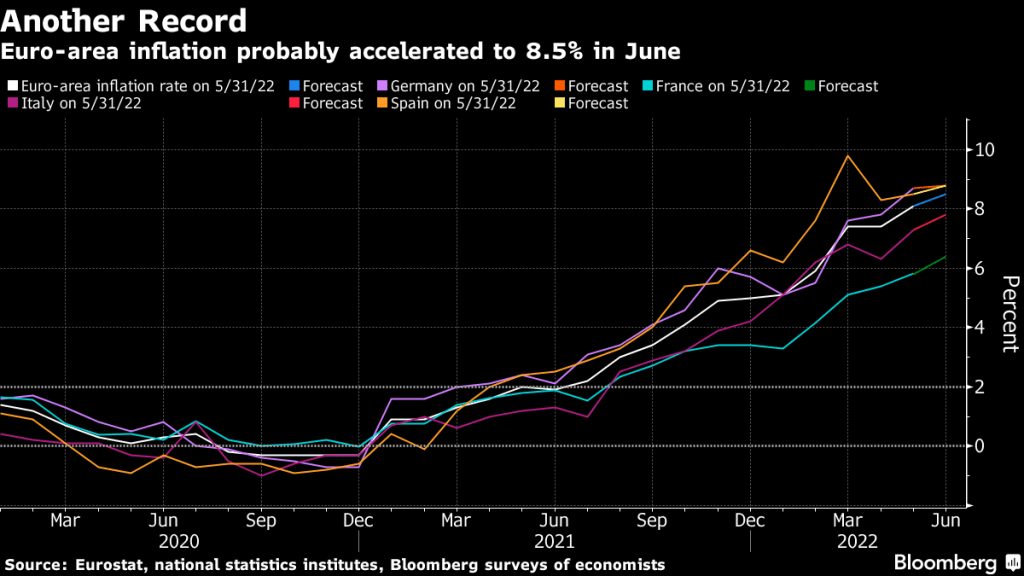

In Euroland, we are seeing a similar problem (Frankfurt, we have a problem!). The Eurozone inflation rate is at 9.1% while their version of The Fed Funds Target rate is only 0.75%, a large catch-up gap.

If we look at the Taylor Rule for the US using headline inflation, we see that The Fed needs to raise their target rate to … 21.72% to crush inflation.

In Euroland, the problem is similar. At 9.10% inflation, the ECB will have to raise their version of The Fed’s target rate to 16.80% to combat inflation. As if that will happen in either the US or Euroland.

On a different note, is it my imagination or does US Democrat Senate candidate from Pennsylvania John Fetterman look like the alien from the flick “Battleship”?

Thanks to Federal Reserve increases in their target rate, the 30-year mortgage rate has risen above 6%.

What drives me crazy about The Fed is their failure to removed monetary stimulus following the financial crisis of 2008 when they dropped their target rate to 25 basis points (0.25%) and began assets purchases (orange line). The Fed raises their target rate only once during Obama’s Presidency but then raised rates 8 times after Trump was elected President.

Now we are seeing The Fed NOT shrinking their balance sheet in a meaningful way. However M2 Money growth YoY (green line) has slowed to 5.2%.

While it is a good thing that The Fed is FINALLY reducing some of the monetary stimulus in place since 2008, the bad thing is that mortgage rates are rising rapidly.

The Fed’s quantheads are predicted to resume easing in March 2023.

As inflation burns the US middle class and low wage workers, The Federal Reserve reaffirmed at Jackson Hole that they are the NEW Smoky The Bear (only The Fed can fight inflation fire!) But of course, Federal spending and energy policies can drive up prices too.

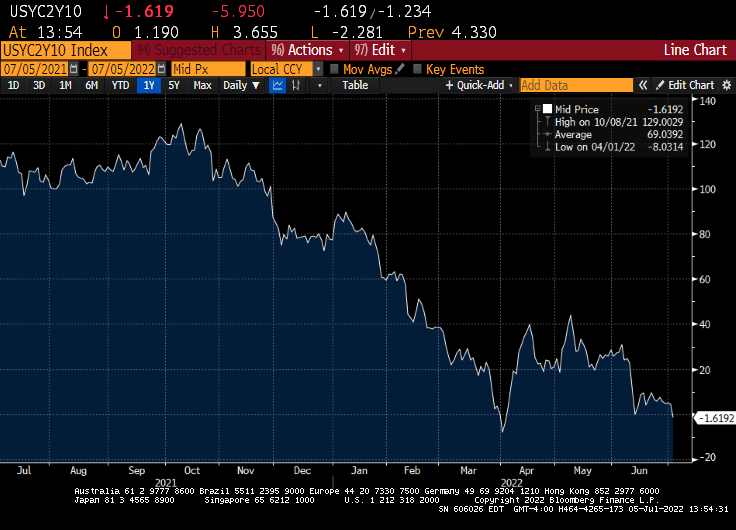

Having said that, the 2-year Treasury yield and 30yr mortgage rate are rising rapidly.

The Fed is trying to cool demand by raising rates after lax monetary policy since late 2008.

While the US 2-year Treasury yield is up only slightly today, the Eurozone is seeing their 2-year sovereign yields spiking by 11-15+%.

Face it. The Biden Administration has little interest in trying to increase the supply fossil fuel energy which would anger his “green” base (like building more refineries or allowing for more crude oil and natural gas exploration). So, the burden of “inflation fighting” falls on the frail shoulders of The Federal Reserve.

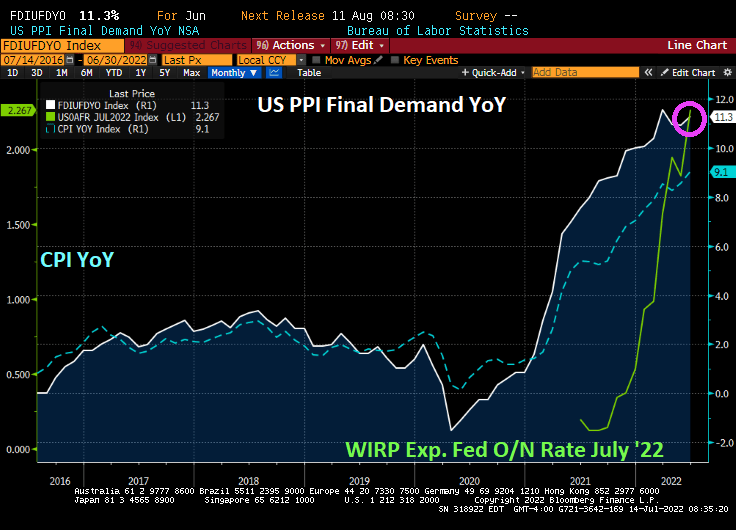

Given today’s US Producer Price Index Final Demand prices rising +11.3% YoY in June, it seems that The Fed has not been able to extinguish the “Tower of Inflation.” But, Fed Funds Futures are pointing to a near 100 basis point (or 1%) increase in The Fed Funds target rate at the July 27th Fed Open Market Committee (FOMC) meeting.

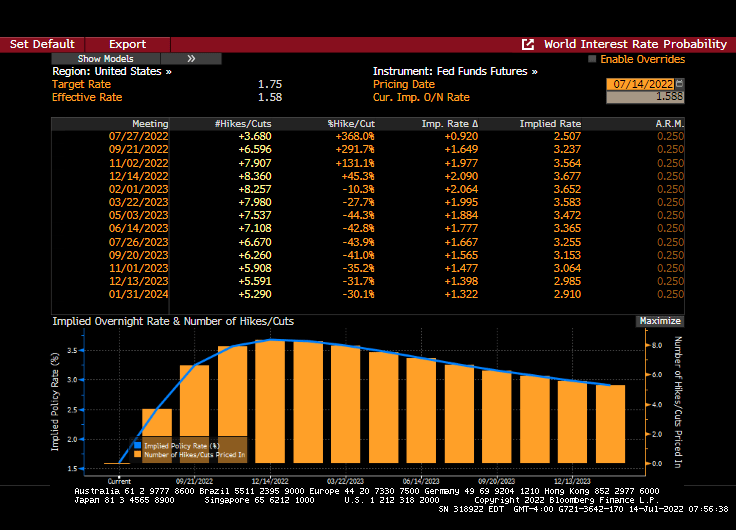

The Fed Funds Futures Data points to a +0.920 (almost 1%) increase at the July 27th FOMC meeting. Followed by rate cuts.

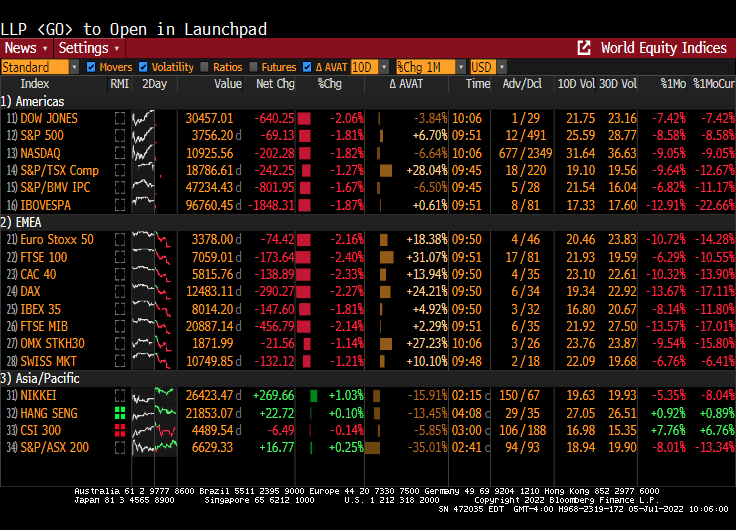

And with the fear of a near 100 basis point increase, today’s stock markets are a sea of red.

It is up to Fed Chair Jerome Powell and policy error brigade to extinguish price increases caused by 1) bad Biden energy policies and 2) too much spending by Biden and Congress. It is like trying to wave-down the Super Chief train with a cigarette lighter.

Yet, the Frail Fed will try to waive down The Super Chief inflation engine with Fed Fireballs. Aka, rate increases of 100 basis points.

The ECB is planning on a Blitzkrieg Bop, monetary style.

When Lagarde talks about the first line of defense, all I can picture is The Maginot Line in France, a failed defensive line that was easily bypassed by the German Wehrmacht (army).

The European Central Bank will activate the bond-purchasing firepower it’s earmarked as a first line of defense against a possible debt-market crisis on Friday, according to President Christine Lagarde.

Applying “flexibility” to how reinvestments from the ECB’s 1.7 trillion-euro ($1.8 trillion) pandemic bond-buying portfolio are allocated is aimed at curbing unwarranted turmoil in government bonds as interest rates are lifted from record lows to curb unprecedented inflation.

Net buying under a separate asset-purchase program is also set to end on Friday.

In other words, Euro-area inflation has exploded in 2021, just like the USA.

But the US also has an inflation problem caused in part by Covid and the government’s reaction to Covid: economic shutdown and massive Federal monetary and fiscal stimulus. The stimulus is still in play.

The bond market is already anticipating an about-face by The Federal Reserve (implied overnight rate peaking at the March 2023 FOMC meeting, then receding.

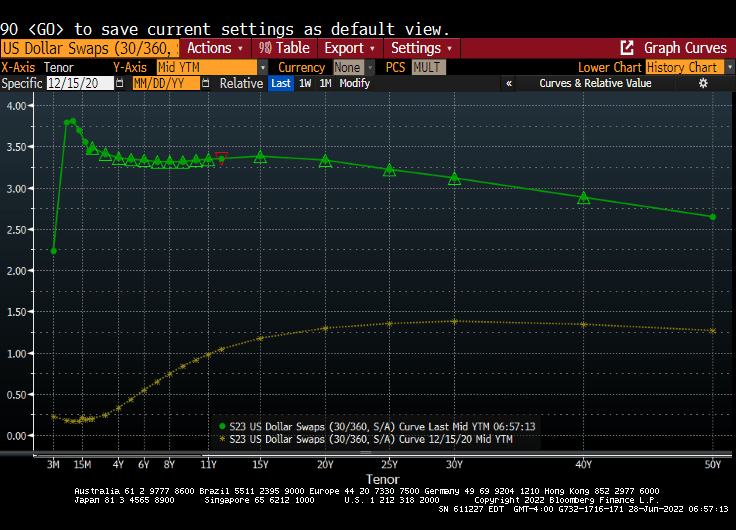

Again, nothing has been the same since the Covid outbreak of 2020 and Fed monetary blitz. Here is the US Dollar Swaps curve before Covid (yellow line) and today’s Fed-enhanced curve (green).

Mortgage rates in the US have climbed to 6% then backed-off slightly. The good ole Back-off Boogaloo as The Fed attempts to unwind its monetary stimulypto.

The French Maginot Line, easily bypassed by German tanks. The Federal Reserve is the US’s Maginot Line. The Yellenot Line??

Here is Dvorak’s New World Symphony, an appropriate piece the global turmoil that has taken place after Russia’s invasion of Ukraine.

Here is the ratio of the S&P 500 index against the Bloomberg Commodity Price Index. This ratio is plotted against The Federal Reserve’s balance sheet of assets. Notice the decline in the Commodity Ratio in 2022, even ahead of the Russian invasion of Ukraine.

Global currencies, on the other hand, have been really crushed since the Russian invasion of Ukraine. The Japanese Yen, China’s Renminbi and Europe’s Euro relative to the US Dollar are falling due to a variety of reasons. Covid lockdown in China, Japan’s insistence on monetary easing while other Central Banks are tightening and the Euro with Russia threatening nuclear war.

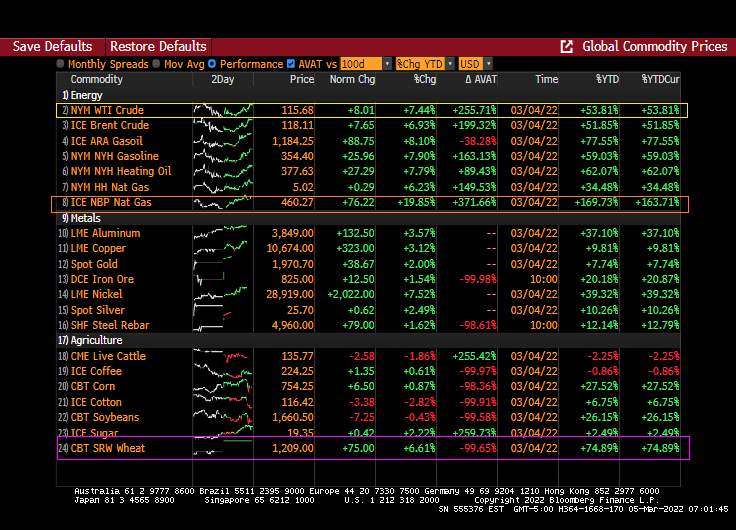

WTI Crude is back to $100 a barrel. Critical metals are down today related to a slowing global economy and wheat is up 2.75%.

Could it be that US Dollar hegemony is nearly over and commodity-backed currencies are the way of the future?

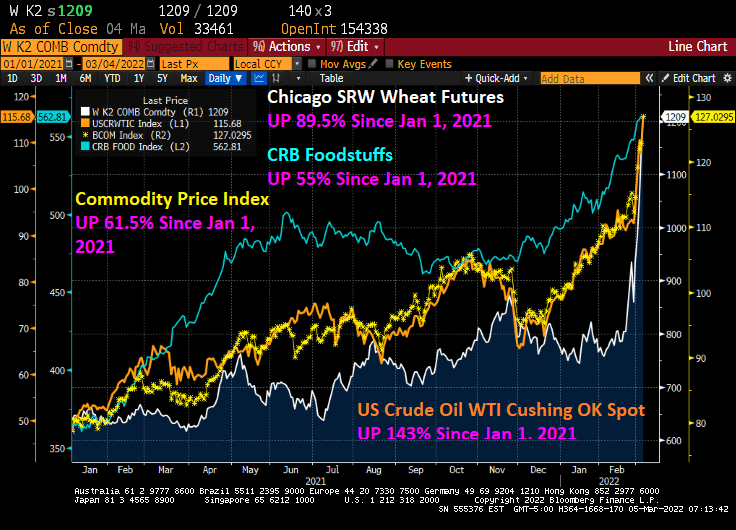

This has been a brutal week for consumers. With the Russia/Ukraine conflict raging and Congress seems determined to not allow for additional oil and gas production, and Biden’s anti-fossil fuel edicts still in place, we are seeing dramatic price increases in wheat (UP 89.5% since January 1, 2021), WTI Crude (UP 143% since January 1, 2021), and food stuffs (UP 55% since January 1, 2021).

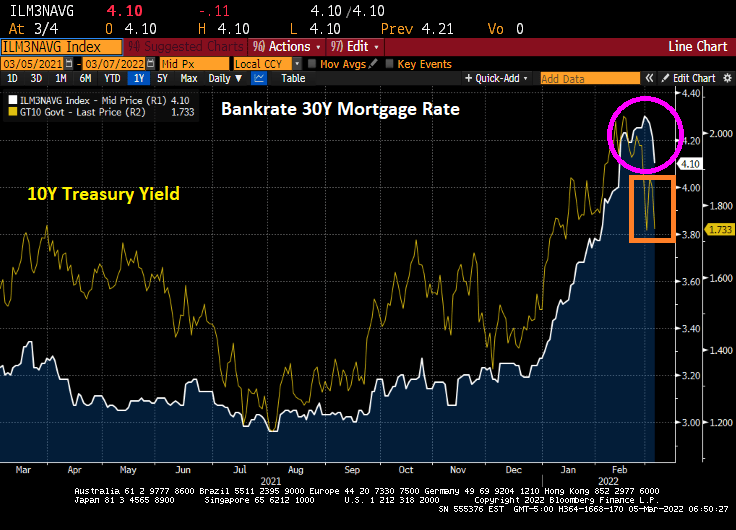

Bankrate’s 30-year mortgage rate has actually been falling the last several days, which is good for prospective home buyers as the 10-year US Treasury Note yield has been declining.

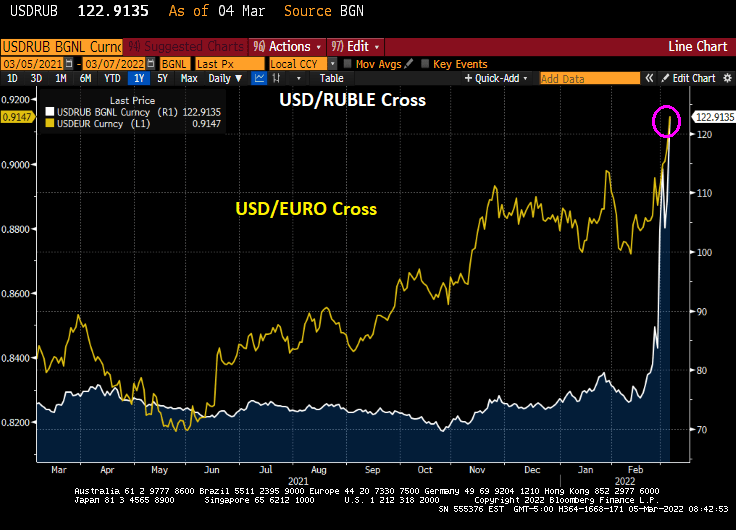

The USD/Russian Ruble cross is skyrocketing and the USD/Euro is doing likewise. Russians visiting the US will find that their trip is suddenly unaffordable (as do many American citizens will its rampant inflation). As Bruce Willis said in “Die Hard,” “Welcome to the party, pal.”

On Friday, the US Treasury 10-year yield declined 11 bps.

And energy prices continue to soar, particularly UK Natural Gas Futures that rose 19.85% overnight.

The US inflation data will be released on March 10th and the consensus is that February CPI inflation will rise to 7.9% YoY.

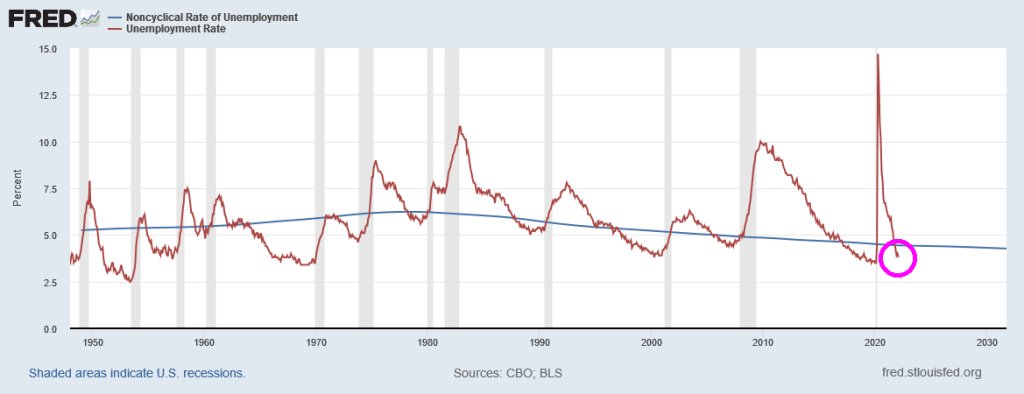

But even the latest unemployment rate report (3.8%) is signalling that The Fed should be raising interest rates since it is lower than the Natural Rate of Unemployment or NAIRU (4.44%).

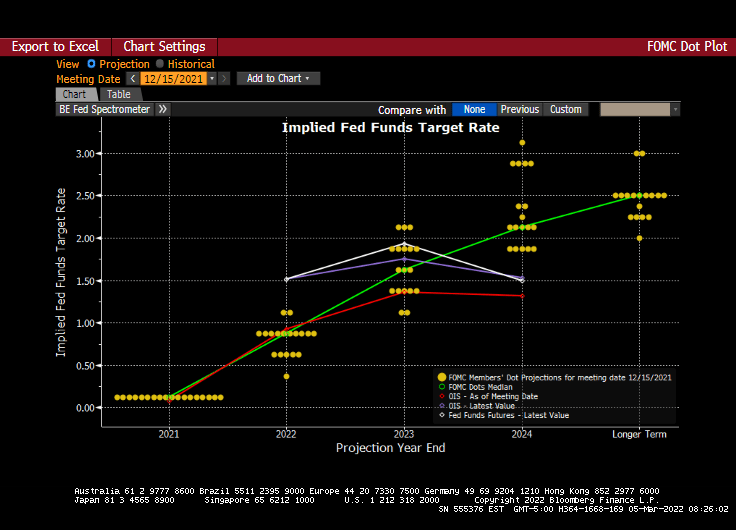

And we have the next Fed policy error on March 16th. The Fed dots plot looks like the glide slope for an aircraft, but the message is that rates will be going up at future meetings.

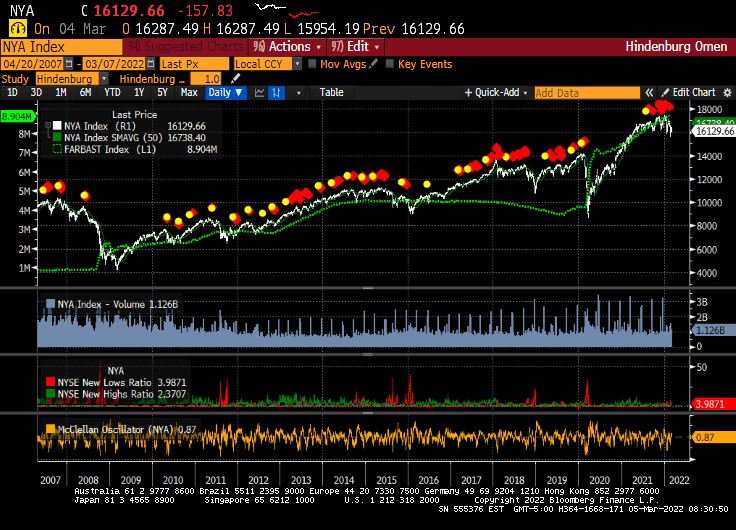

And just for amusement, I present to you the infamous Hindenburg Omen chart that forecast the 2008/2009 stock market correction. Since that correction, the Hindenburg Omen has been flashing “danger” but the only correction was the COVID-linked correction of early 2020. While the Hindenburg Omen is flashing red right now, The Federal Reserve’s balance sheet (green line) has protected against market corrections. Let’s see what happens if and when The Fed decides to remove the epic monetary stimulus.

Its anyone’s guess as to whether The Fed will actually tighten monetary policy.

You must be logged in to post a comment.