I feel like I am watching the Star Trek original series episode “The Doomsday Machine” as former Fed Chair and current US Treasury Secretary effectively just guaranteed ALL US bank deposits. Aka, a massive bank bailout. The episode was about a robot space vehicle that destroy planets … and anything in its path. And if it changed course to destroy something, it gradually returned to its original destructive path. Like The Federal Reseve.

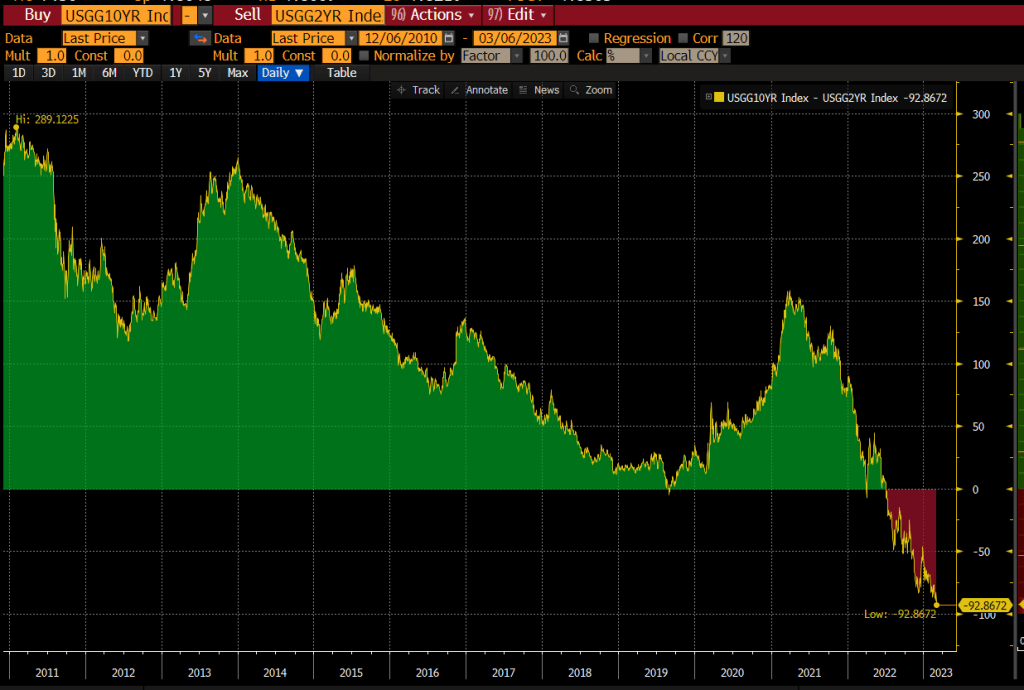

But after a few days of declining Treasury yields because of the mess created by Bernanke/Yellen’s too low for too long policies, and the Biden/Congress insane spending, the US Treasury 2-year yield is up 16.1 basis points.

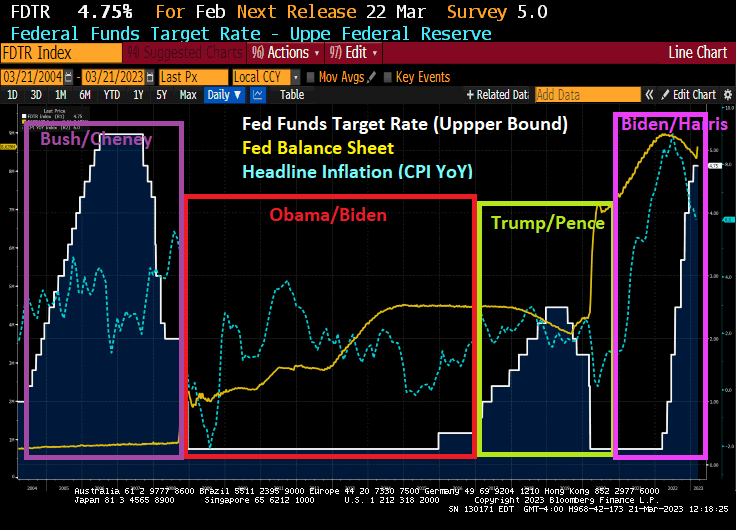

Whether it was politcally motivated to protect Obama/Biden or Obama/Biden’s economic recovery was terrible, The Fed only raised their target rate once before Trump’s election. And then Yellen raised rates like crazy. Only to hand her mess off to Powell who had to drop rates like a rock and massively expand the balance sheet … again … to fight Covid.

The Federal Reserve from a car on Constitution Avenue in Washington DC.

You must be logged in to post a comment.