Martha and the Vandellas said it best: “No where to run, no where to hide.” We are already seeing rioting in the streets.

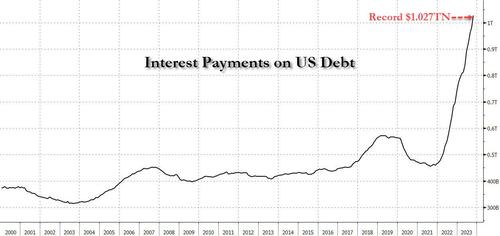

Rubino says, “If the U.S. government is running crisis level deficits, which it is right now, borrowing money and paying interest on it means we are in a financial death spiral…”

“The debt goes up, the interest on the debt goes up and that raises the debt even further, and you just spiral out of control.

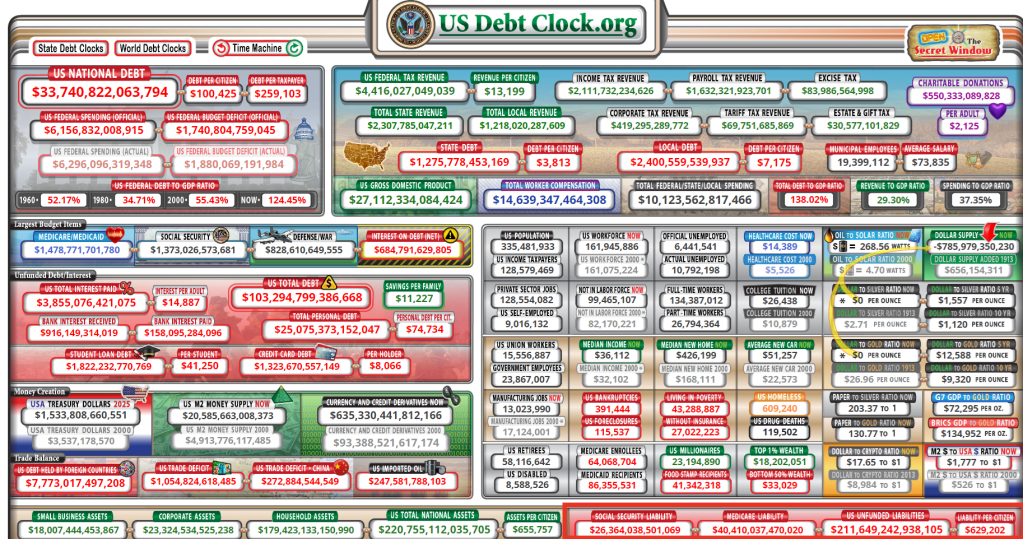

We are there right now. The official U.S. debt is $33.5 trillion. It’s growing by $1.7 trillion a year, and $1 trillion of that is interest costs.

Interest costs are rising as the overall debt goes up. Then throw in this incredibly reckless military spending in the guise of foreign aid, and you get a society that has completely lost control.

That’s where we are now.

We are in the blowoff stage of a 70-year credit super-cycle.

Those things do not end with a whimper, and they certainly do not end with a soft landing. They end with a bang, and the bang is going to be centered on the currency.

People are going to look at this and say, ‘Do I really want to hold the currency or bonds of a country that is destroying its finances at this trajectory and this scale?’ The answer will be ‘No.’

At that point, it is game over for a deeply indebted economy. We are headed that way fast, and these wars are taking us that way even faster.”

If the Fed keeps raising interest rates, the economy tanks, but you protect the dollar. If you cut interest rates, you spike inflation even more, and the U.S. dollar tanks.

Rubino says in the end, we get a “massive reset,” and the everything bubble explodes.

Rubino says the dollar is going to decline and, at some point, it starts to go into freefall in terms of buying power. Rubino explains,

“If a currency starts to decline in a disorderly way, then you have a massive financial crisis on your hands.

That is definitely where Japan is right now. The U.S. is headed that way fast.

So, once we reach that point, there is no fix.

Then it is only a matter of time that everybody realizes that there is no fix, and they just bail on the whole experiment, and that’s where we are headed.”

Rubino talks about plunging home prices, more trouble coming in the commercial real estate market and why you need gold and silver as core assets during a currency reset.

Riots, already happening in American cities (not to mention looting in New York City, Chicago, San Francisco and Los Angeles), will accelerate if Congress attempts to curtail entitlements (now at $211.65 TRILLION).

Meanwhile, Biden keeps giving away money (student loan forgiveness, electric heat pump mandates, etc.).

Hey, at least Argentina elected AC/DC’s Angus Young as President!

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.