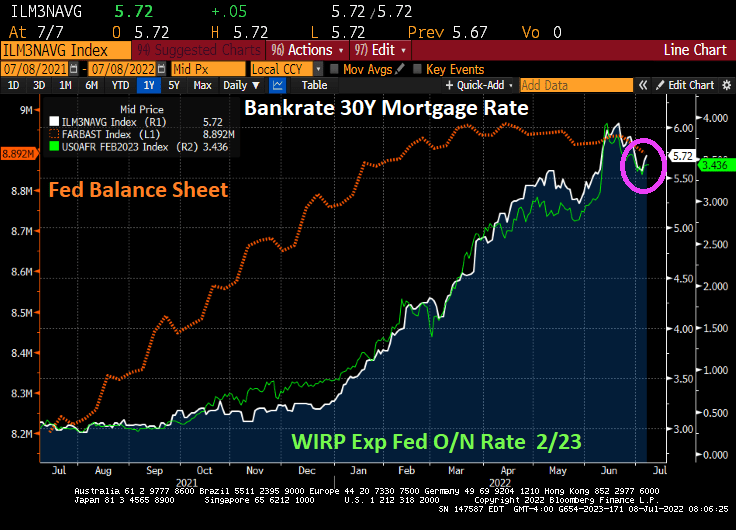

After breaking the 6% barrier back in June 2022, Bankrate’s 30-year mortgage rate has backed-off to 5.28% despite Federal Reserve rate hikes.

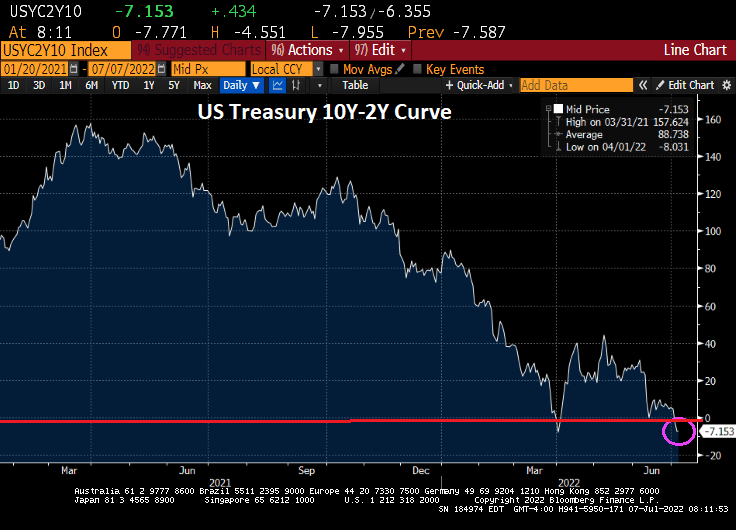

The reason for the decline in the US Treasury 10-year is, amongst other things, a global economic slowdown (partly due to the US and Europe “going green” and cutting the supply of fossil fuel-based energy). Instead of “The Great Reset,” I call it “The Great Economic Suicide.” The 10-year US Treasury yield and Bankrate’s 30-year mortgage rate are declining with declining global GDP.

US inflation, based on June’s Personal Consumption Expenditures (PCE) deflator, rose to its highest level since 1982. The PCE Deflator YoY rose to 6.8% while the core PCE deflator (less food and energy, the two things more households care about) rose to 4.8% YoY in June.

In order to fight inflation, The Federal Reserve is going to have to raise their target rate to … 17.78% based on 6.80% PCE deflator YoY. We are currently at 2.50%.

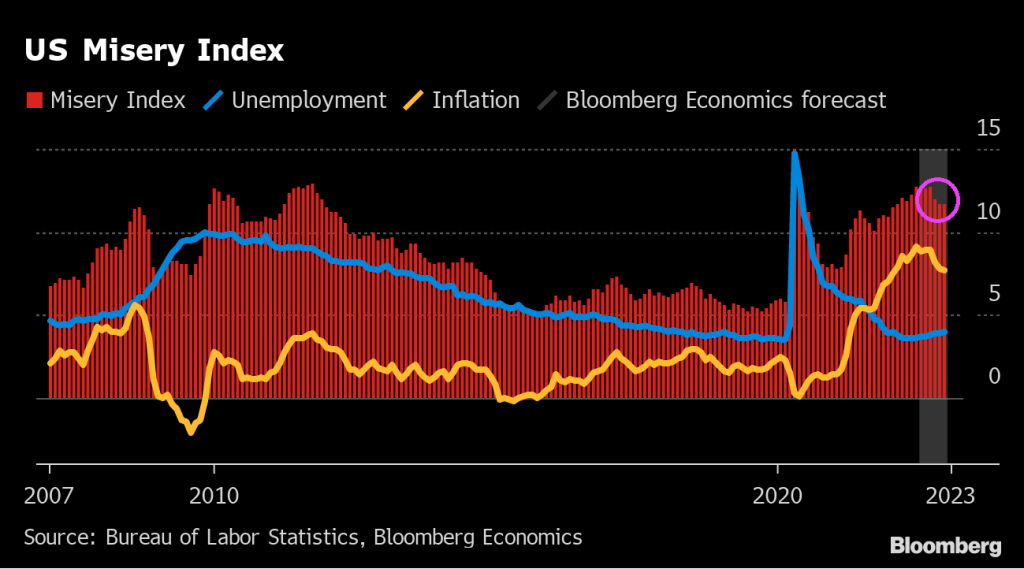

The US Misery Index remains elevated.

Based on the PCE Deflator YoY and U-3 unemployment, the misery index remains elevated compared to before Covid and The Fed’s/Federal government hyper-stimulypto to counter the Covid economic shutdowns. We never fully recovered.

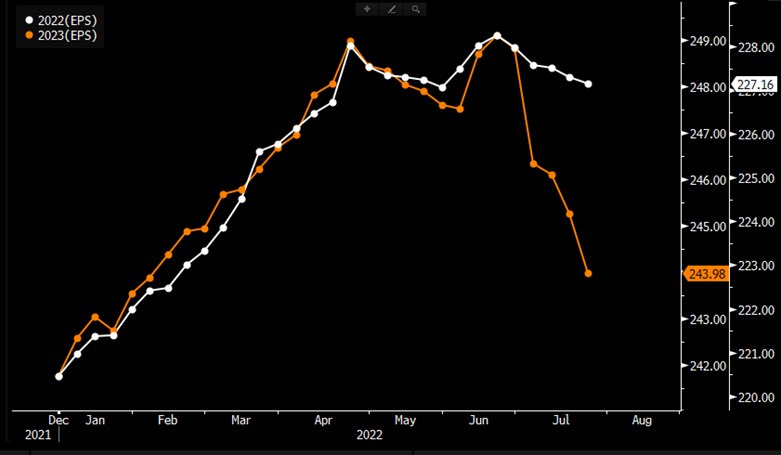

S&P 500 2023 EPS expectations falling off a cliff (orange line).

The US is short on supply of housing for a myriad of reasons (high costs, Not-in-my-backyard (NIMBY) local zoning laws, etc), but The Fed’s cranking up interest rates isn’t helping.

US housing starts, a measure of supply, declined -6.3% YoY in June as The Fed cranked up rates.

1-unit (aka, single family detached) starts dropped -8.05% MoM in June while 5+ unit (aka, multifamily) starts rose 15% MoM.

1-unit permits dropped -8% MoM in June while 5+ unit starts were up 13% MoM.

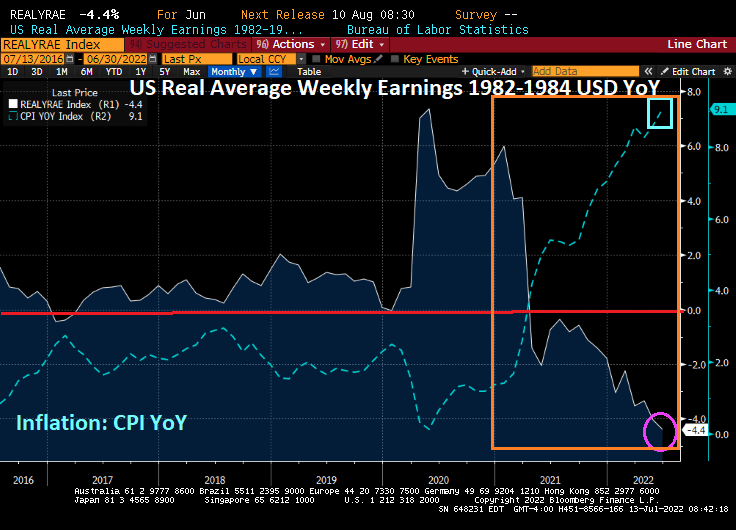

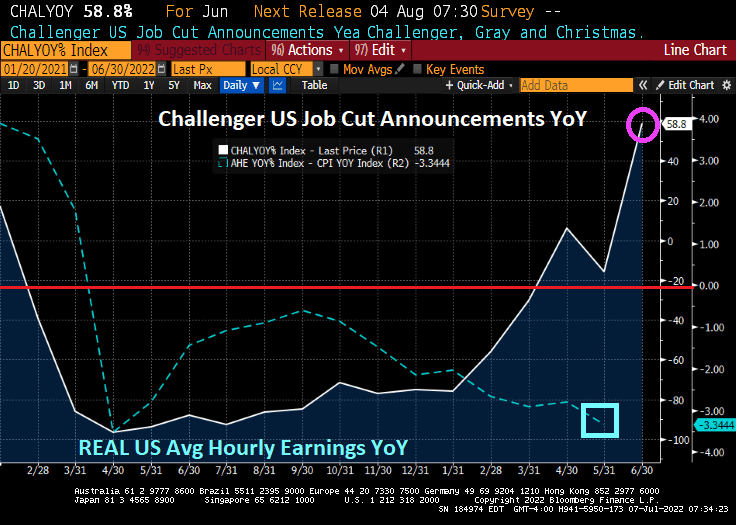

The reason? REAL weekly earnings growth declined -4.4% YoY in June thanks to Bidenflation.

The Federal Reserve isn’t soothing me with their rate hikes.

As The Fed has been raising their target rate and beginning to shrink their balance sheet, we are seeing Q3 Real GDP slipping further down the rabbit hole to -1.5%.

The culprit? Friday’s retail trade, import/export prices and industrial production.

Time for some tequila to soothe me, since The Fed or the Biden Administration won’t help.

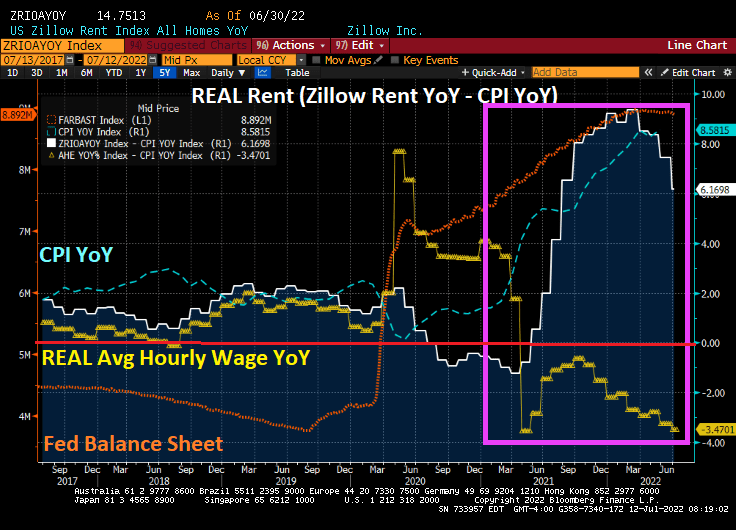

We are all aware that inflation is soaring, since the Covid outbreak in 2020 and the massive overaction by The Federal Reserve and Federal government in terms of stimulus spending and economic lockdowns.

Things were “normal” before Covid in that REAL housing rent (white line) and REAL average hourly earnings YoY (yellow line) moved together. But after Covid shutdowns and Federal stimulus “relief” (orange line), we see that inflation (blue line) took off along with the growth in housing rent. The problem, of course, is that REAL average hourly earnings YoY has been declining. I call this “The Great Divide in housing affordability”.

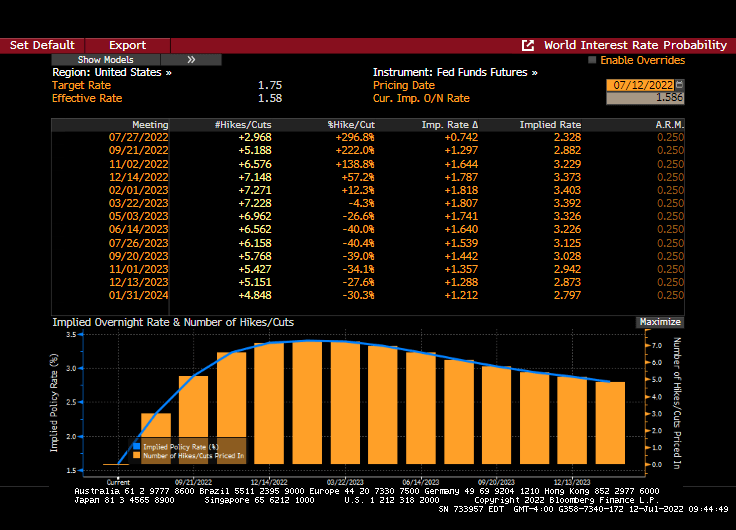

The question, of course, is whether The Federal Reserve will continue their “war on inflation” with a 75 basis point rate increase.

Inflation is at its fastest pace in 40 years, and is expected to increase even higher in tomorrow’s inflation report.

Gasoline prices have been dropping recently, but remain above $4.50 per gallon (regular gas price was $2.40 per gallon on Biden’s inauguration day. And no, it wasn’t the Biden Administration selling nearly 1 million barrels of crude oil from the strategic petroleum reserve to the Chinese government-owned Sinopec that Biden’s son Hunter is an investor (so, The Big Guy aka Joe Biden gets a 10% piece of the action). It is a slowing global economy that is helping to lower gasoline prices.

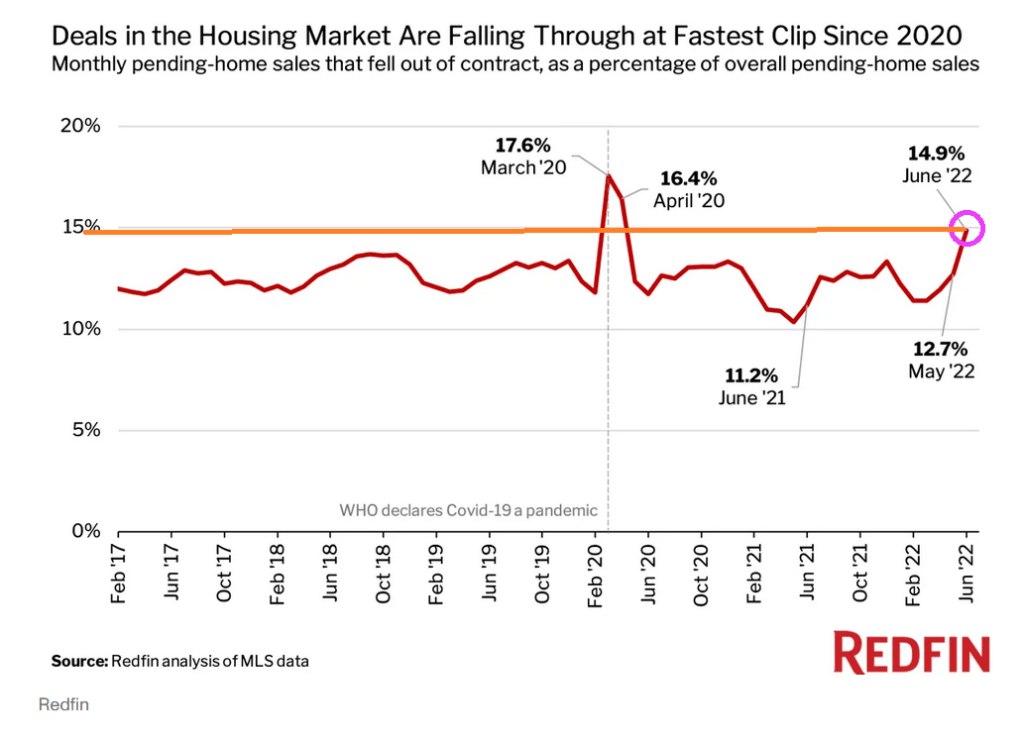

With rising mortgage rates, we are seeing a surge in pending home sales cancellations.

Atlanta Fed’s Raphael Bostic thinks that the US economy is so strong that it can easily handle a 75 basis point increase at the next FOMC meeting. Fortunately, he is not a voting member.

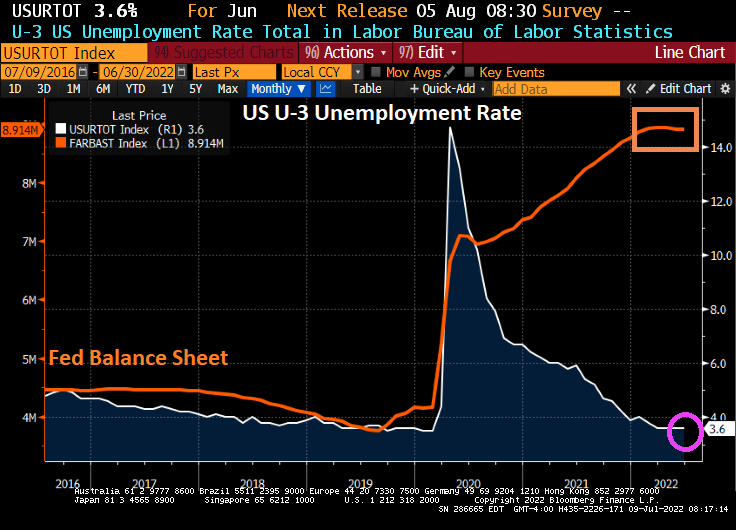

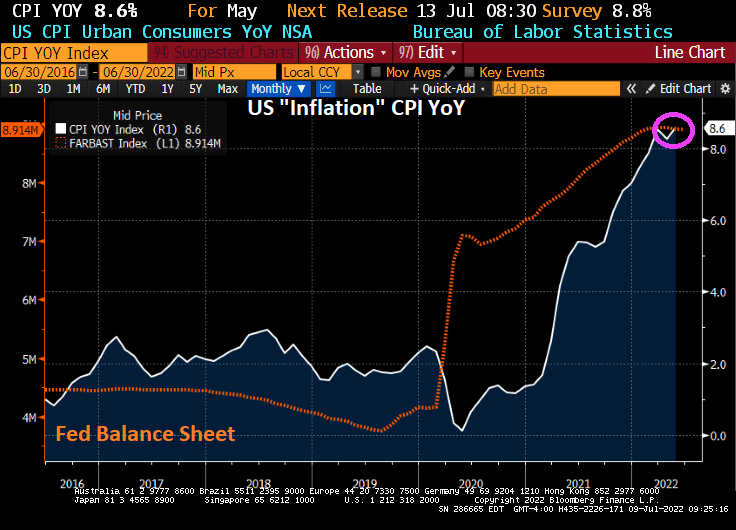

Take the US U-3 unemployment rate. The Biden Administration is proud of the unemployment rate of 3.6%. But if you look at the chart of unemployment relative to The Fed’s balance sheet expansion due to Covid lockdowns, there is still almost $9 trillion of Fed stimulus outstanding.

Of course, the lockdowns were pure economy killers, so opening the economies again led to the unemployment rate falling to 3.6% which is still higher than before the Covid outbreak. But The Federal Reserve has been painfully slow at shrinking its balance sheet, leaving almost $9 trillion in monetary stimulus outstanding.

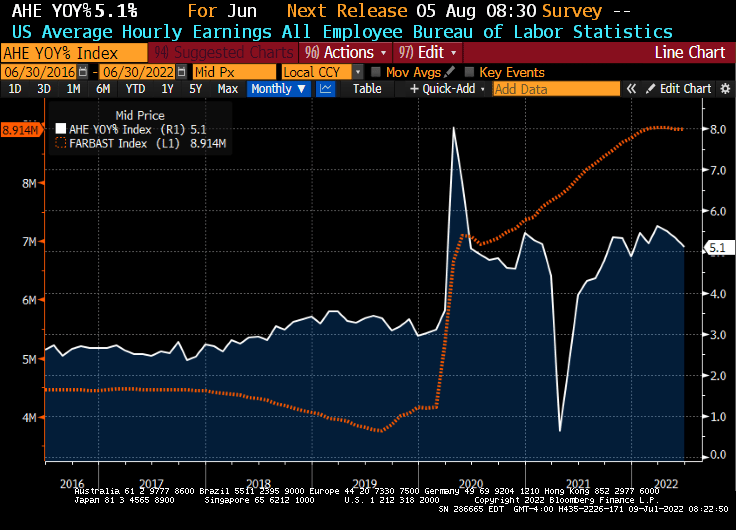

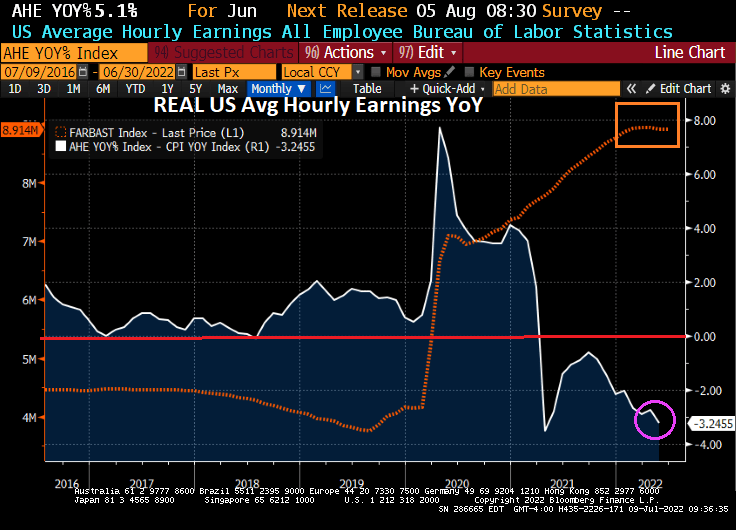

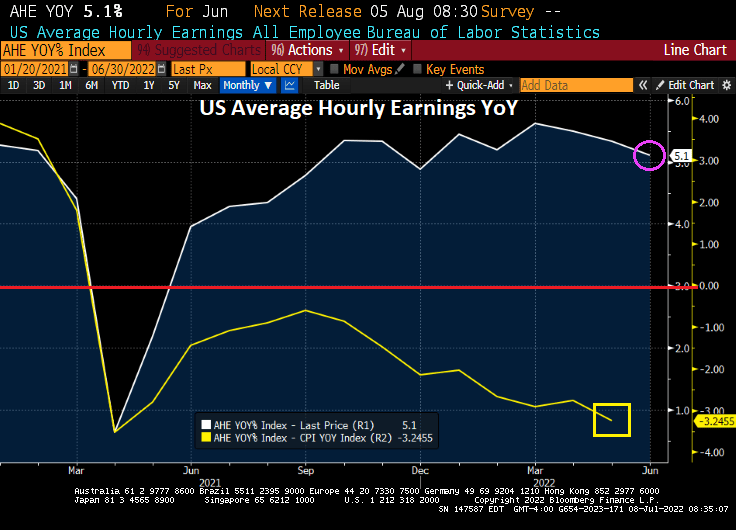

Take average hourly earnings growth. The media is all smiles as US wage growth declined to 5.1%, much higher than pre-Covid.

Then we have inflation, at 40-years highs thanks to massive Fed stimulus (and Federal spending).

And if we deduct inflation from average hourly wage growth, we see REAL wage growth declining at a -3.25% YoY clip.

Lastly, we have the US Dollar. Nothing has been the same since the financial crisis of 2008 and the entrance of The Federal Reserve distorting the economy and prices. Not to mention the US Dollar.

The Fed leaving its monetary stimulus out in force for so long is a major policy error. So what happens when The Fed actually gets serious about withdrawing the monetary stimulus (likely after the midterm elections)?

There is no doubt that the US economy is slowing, thanks in part to The Federal Reserve’s sudden crusade to slow inflation (caused by … The Federal Reserve and Federal spending).

My favorite chart is US Average Hourly Earnings YoY. It peaked in March at 5.6% and has been slowing to 5.1% in June. BUT historically high inflation has caused REAL US Average Hourly Earnings YoY to decline to -3.25%.

The good news? 372k jobs were added in June. The bad news? It was lower than jobs added in May (390k) showing a slowing trend.

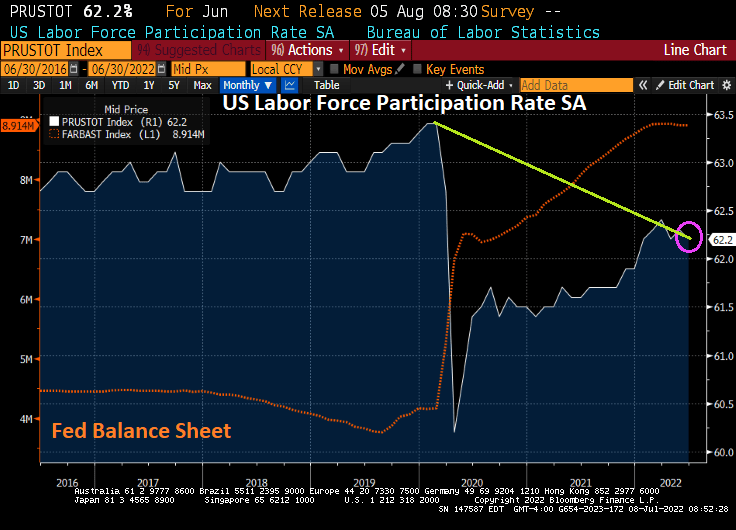

Unemployment remained at 3.6%. Labor force participation fell to 62.2%.

The US labor force participation remains below the pre-Covid levels despite staggering Fed monetary stimulus. But what happens when The Fed’s “Snake Juice” is withdrawn??

Here is a nice summary table.

US 30 year mortgage rates resumed their vertical climb as The Fed continues to tighten their loose monetary policy.

But the jobs report was good enough to lead to the US Treasury 10Y yield to jump 10.3 basis points today.

You must be logged in to post a comment.