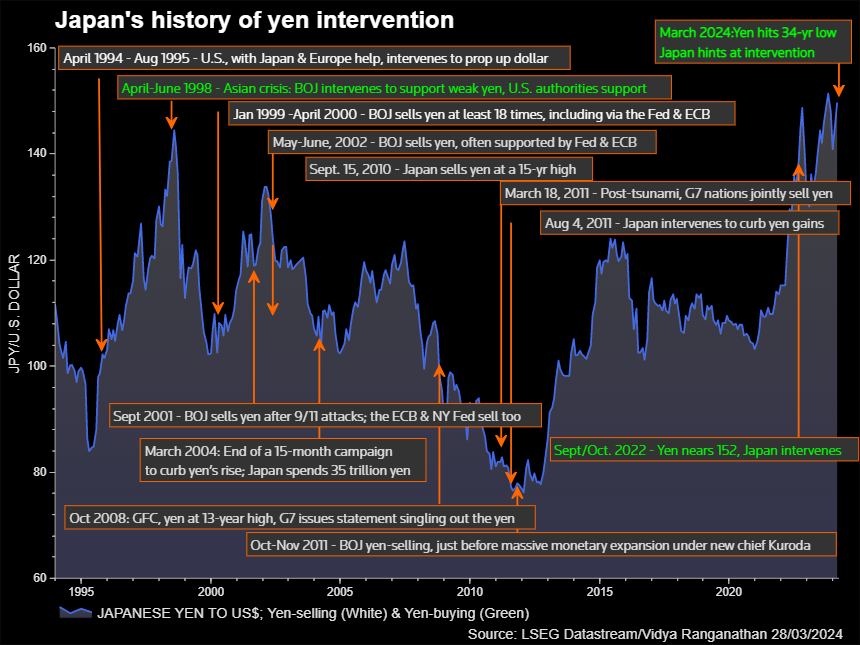

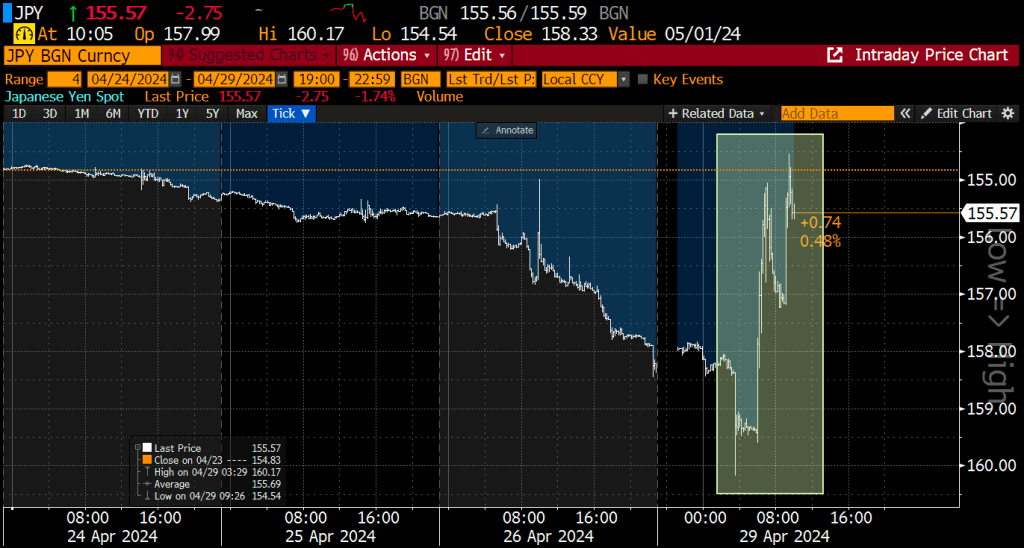

In the time (dis)honored tradition of Haruhiko Kuroda, the former governor of the Bank of Japan, Japan likely conducted its second currency intervention this week, current account figures from the central bank suggest, in another sign of the government’s intensified battle to prop up the yen.

Tokyo’s latest entry into the market was likely around ¥3.5 trillion ($22.5 billion), based on a comparison of Bank of Japan accounts and money broker forecasts.

The BOJ reported Thursday that its current account will probably fall ¥4.36 trillion due to fiscal factors on the next business day of Tuesday. That compares with the ¥833 billion average forecast by money brokers of what the number would be without intervention.

The figures, released less than a day after the yen jumped sharply during US trading hours, indicate that Japanese authorities made the unusual move of stepping into the market shortly after a Federal Reserve meeting when investors were still digesting the announcement. That would signal the finance ministry is taking an increasingly aggressive stance in what could become a prolonged fight to support the yen.

“With Japanese holidays and US jobs data coming up, it was a very good time for the authorities to tackle speculators,” said Yuya Kikkawa, an economist at Meiji Yasuda Research Institute. “This will have a great impact on the market. I sense a strong determination by the authorities to defend the 160-yen-per-dollar line.”

The latest swing in the yen follows a similarly sudden jump on Monday. Central bank accounts suggested Monday’s move was likely an intervention by Tokyo worth around ¥5.5 trillion, close to the daily record of ¥5.6 trillion set in October 2022.

Ahead of the move late Wednesday in New York and early Thursday in Tokyo, Central Tanshi Co. and Totan Research Co. had forecast a ¥700 billion decline in the BOJ’s current account balance due to fiscal factors including government bond issuance and tax payments. Ueda Yagi Tanshi projected the balance to drop by ¥1.1 trillion.

The calculations based on a comparison of those estimates and the central bank accounts offer only ballpark figures rather than specific amounts. Similar analysis proved accurate in showing that a jump in the yen in jittery markets in October 2023 was not the result of Japan stepping in to buy the currency.

The calculations also estimated the size of intervention on Oct. 21, 2022 at around ¥5.5 trillion, closely matching the actual amount.

An official monthly figure for the size of intervention will come out on May 31. Traders will need to wait until August or later to see daily operation data.

Japan’s top currency official Masato Kanda declined Thursday to comment on whether the finance ministry had intervened two hours earlier in Tokyo, when the yen strengthened sharply against the dollar. Japan’s currency briefly touched 153.04 from around the 157.50 mark.

Kanda oversaw the previous cycle of interventions in 2022. The ministry bought the yen around 30 minutes after the BOJ’s governor press conference ended in September that year. Another round of moves came a month later with back-to-back business day interventions.

The pattern of Japanese officials declining to comment is aimed at keeping market participants in the dark. A lack of immediate clarity may help keep traders more on edge and less willing to bet against the yen even if the ministry hasn’t actually taken action.

“By acting right after the Fed decision and outside of Japan hours, they dished out a warning that they are in a position to intervene 24 hours a day,” said Hirofumi Suzuki, chief FX strategist at Sumitomo Mitsui Banking Corp.

“We are still waiting for US employment figures during the Golden Week holidays and depending on the outcome of that data, there is a risk of further intervention,” he said.

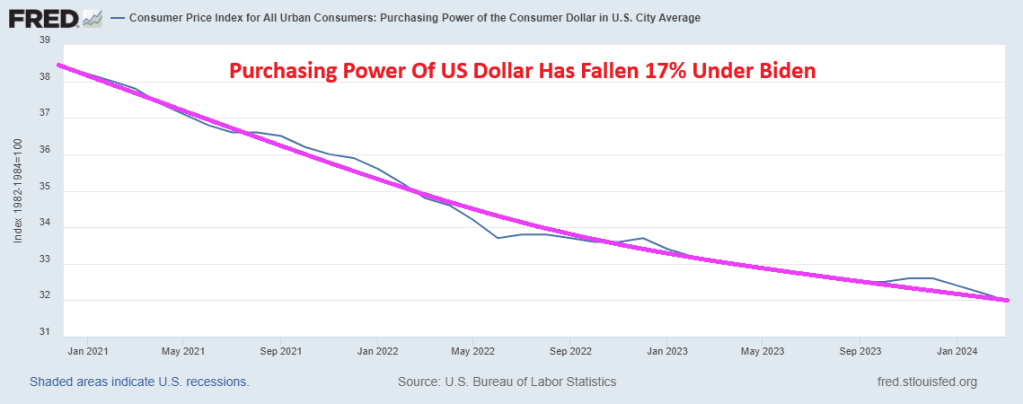

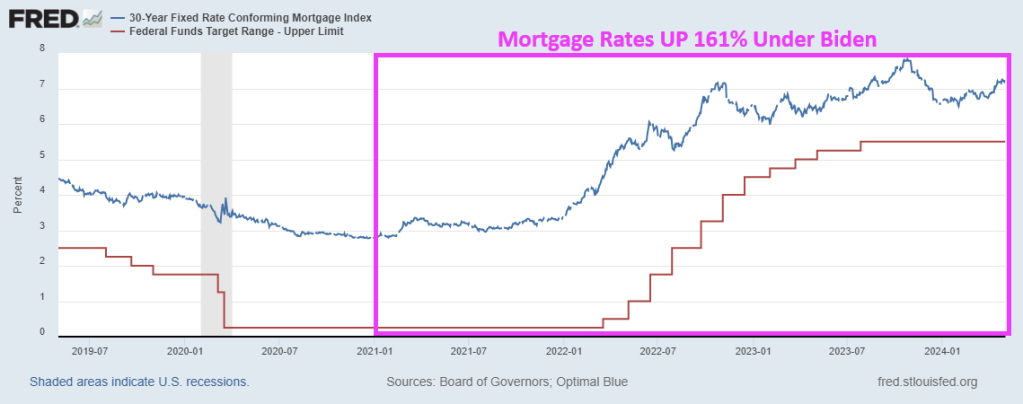

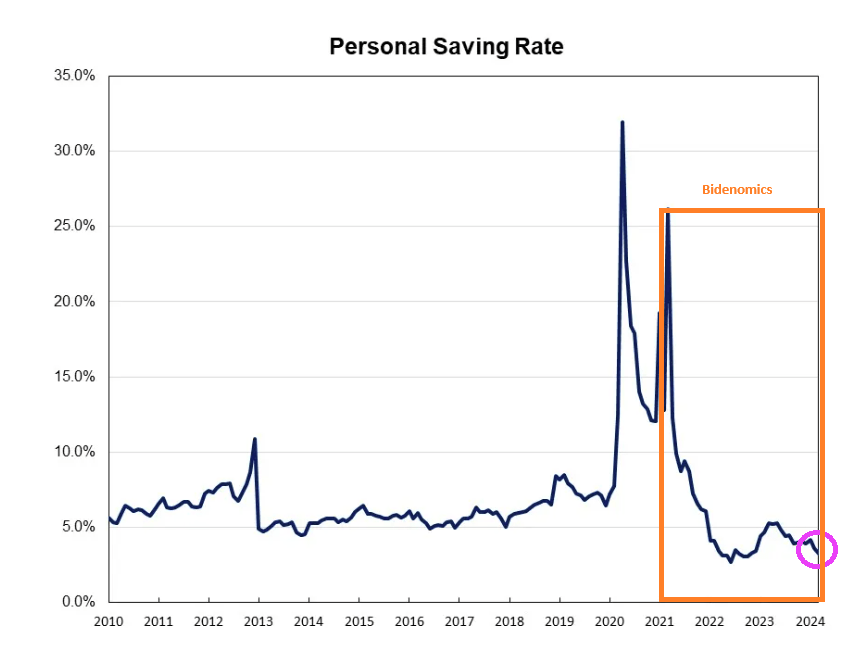

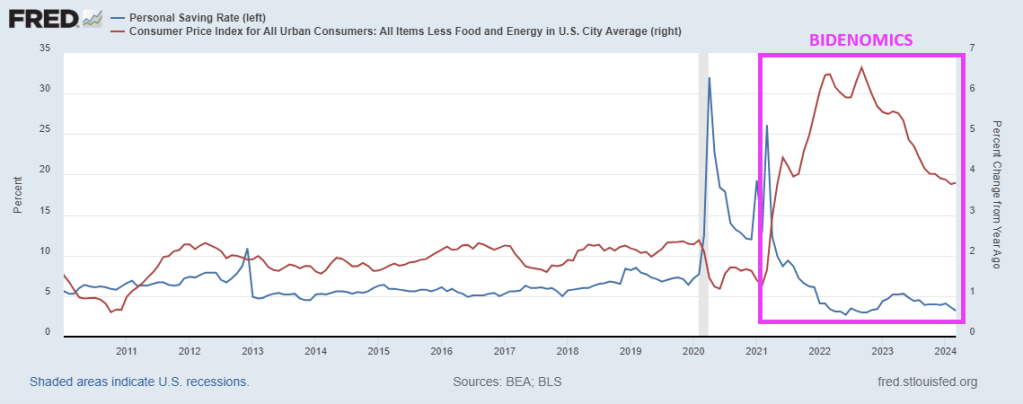

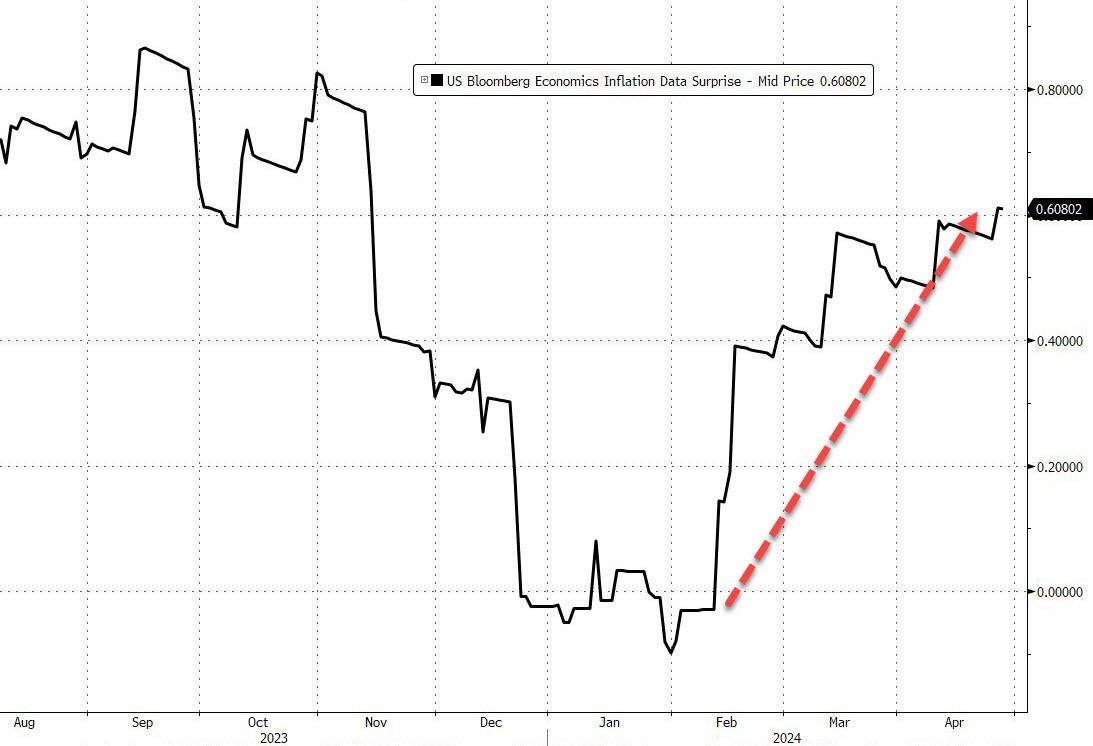

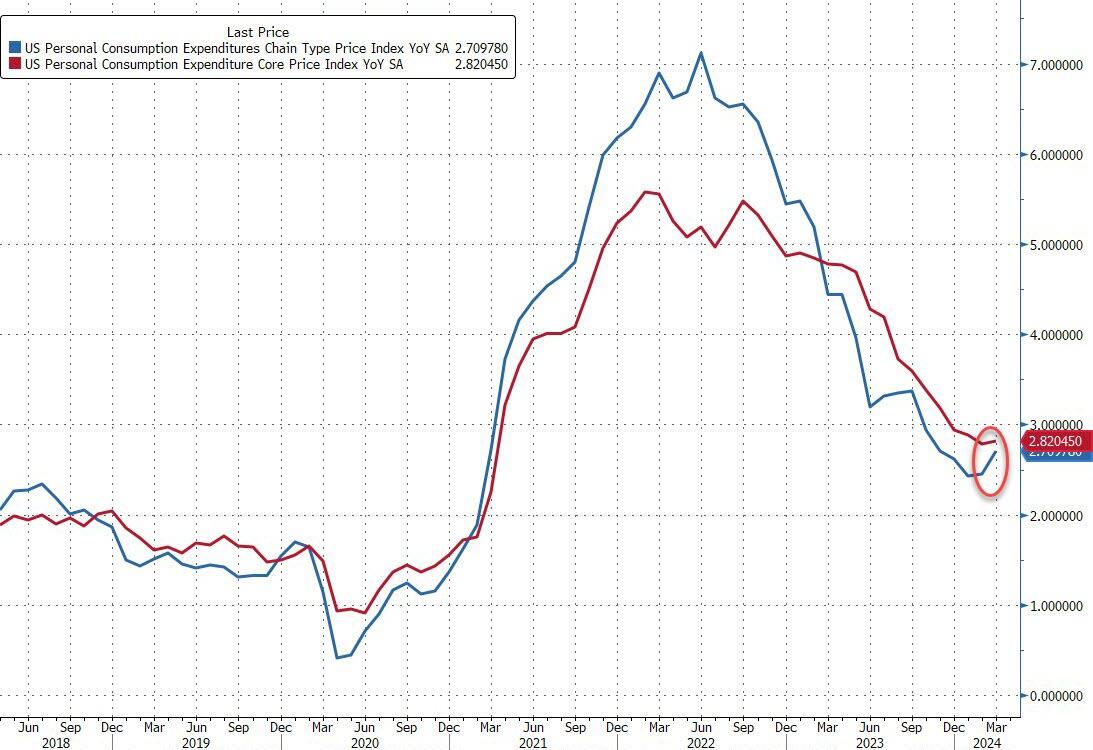

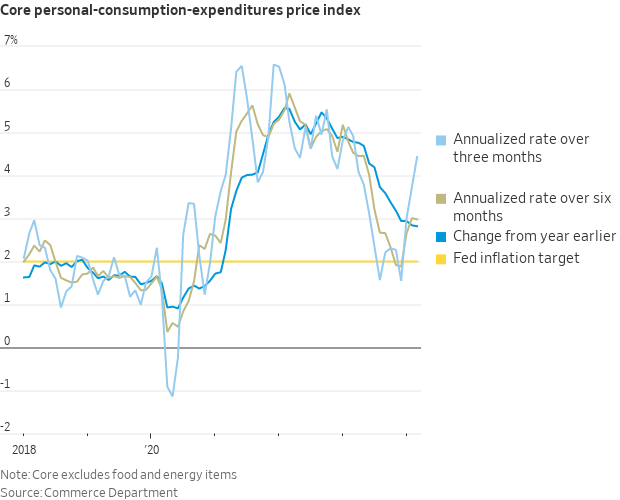

The US is having its own currency problems under Biden with its own bad fiscal and monetary polcies. The Purchasing Power of the US Dollars has fallen 17% under Biden.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.