The University of Michigan consumer survey results are out and there is good news! Sort of.

The UMich Buying Conditions for Houses rose to 47 in July! That is the good news. The bad news? It was at 142 in the last month before Covid and the economic/school shutdowns.

That is -67% lower than under pre-Covid Trump.

Nothing has been the same since Covid (aka, the Wuhan China Lab virus) where our corrupt politicians and lame street media (aka, government cheerleaders) show no interest in finding out what really happened.

Bitcoin cash is up 21.5% today.

Gold and silver are up today. Too bad I can’t buy nickel coins.

The Walking Dead’s Megan. The honorary symbol of Bidenomics.

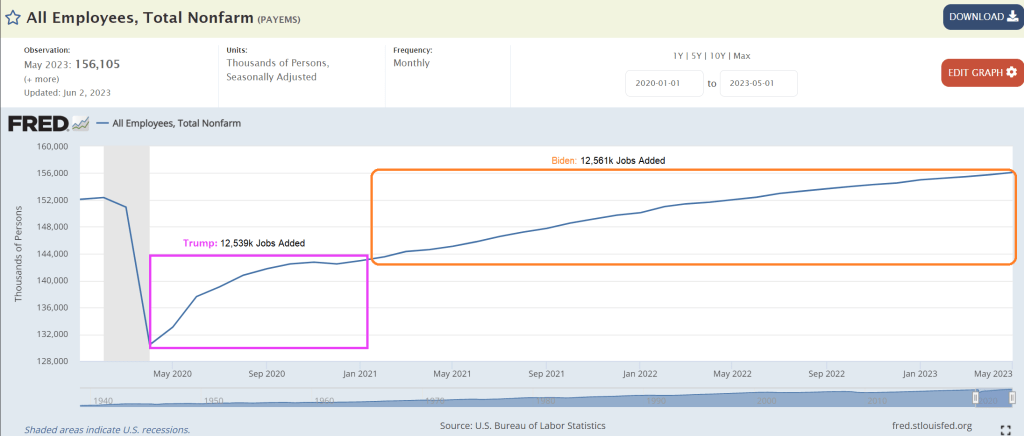

Bidenomics is a great marketing ploy where you have out of control Federal spending and magically decide to reopen the economy and school after Covid and focus only on jobs added after Biden was selected President and ignore the jobs added during Trump.

Real gross domestic income (GDI) is a measure of the incomes earned and the costs incurred in the production of gross domestic product. It’s another way of measuring U.S. economic activity. BEA also publishes the average of real GDP and real GDI.

REAL GDI dropped to -0.8% QoQ for Q1 2023. Kind of looks like Bidenomics is running out of gas.

On Biden’s claims that he created twice as many jobs as any other President, the US economy add 12.53 million jobs after April 2020 (Trump) while Bidenomics created took 2 1/2 years to add 12.56 million jobs.

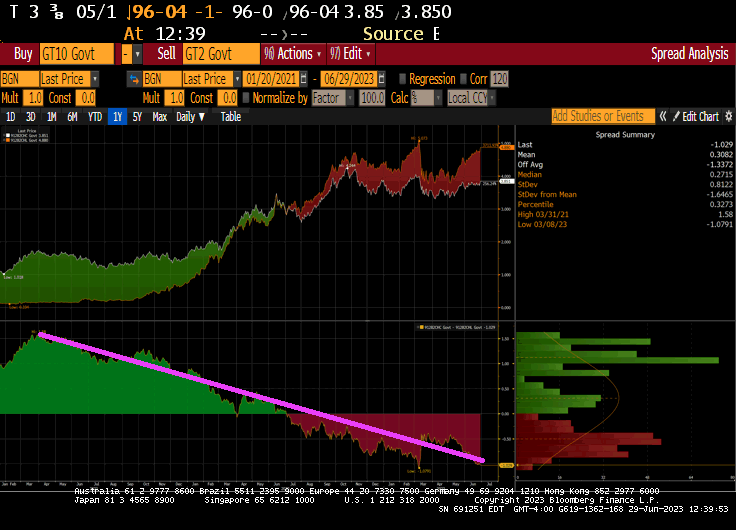

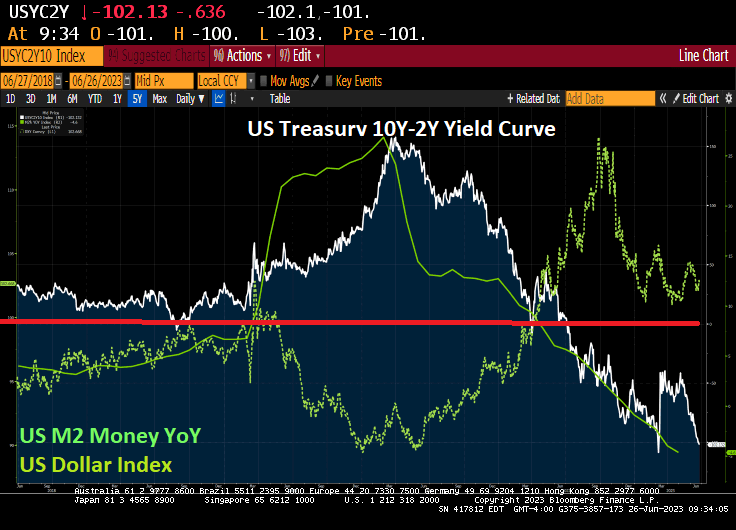

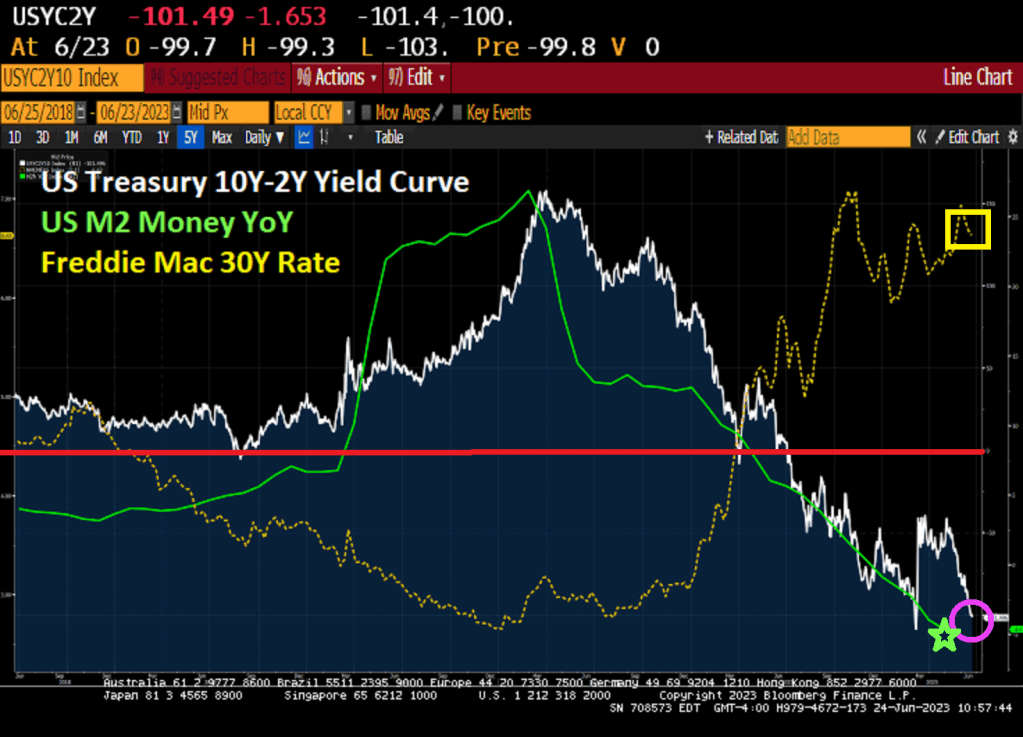

The US Treasury yield curve (10Y-2Y) is now inverted at -103 basis points.

As Fed stimulus wears out, so is the Treasury 10Y-2Y yield curve.

Jay Leno once quipped about the Obama meal. “Order anything you want and hand the bill to the person standing behind you.” Biden, like his boss Obama, is praciticing a similar strategy. Spend like a drunken sailor and just keep borrowing until the whole thing breaks.

The barrage of fresh Treasury bills poised to hit the market over the next few months is merely a prelude of what’s yet to come: a wave of longer-term debt sales that’s seen driving bond yields even higher.

Sales of government notes and bonds are set to begin rising in August, with net new issuance estimated to top $1 trillion in 2023 and nearly double next year to fund a widening deficit. The Treasury is already in the middle of an estimated $1 trillion bump in bills as it seeks to replenish its cash coffers in the wake of the debt-limit deal.

It’s an explosive mix for borrowing costs as debt sales are swelling and the Federal Reserve continues to reduce its balance sheet at a time when traditional buyers of Treasuries overseas are discouraged by currency hedging costs.

“A worsening fiscal profile, amid fairly modest spending cuts, suggests that the upcoming supply deluge will not be limited to T-bills,” wrote Anshul Pradhan, head of US rates strategy at Barclays Plc. “The Treasury will soon need to increase auction sizes meaningfully across the curve. We believe the rates market is too complacent.”

Barclays strategists predict the net rise in coupon-bearing debt from August to year-end will be nearly $600 billion. And that would only ramp up in 2024, they say, with an annual figure of $1.7 trillion. That would be nearly double this year’s expected debt issuance.

Pradhan says he doesn’t think the market appreciates the increase in issuance that’s going to be needed due to wide budget deficits and the fact the Treasury won’t want bills to become a substantial share of the total debt.

Total net new bill sales are set to bring their share of US debt to about 20%, according to JPMorgan Chase & Co. The issuance would hit a threshold seen by the Treasury Borrowing Advisory Committee as the upper limit for the US to fund deficits at the least possible cost to taxpayers.

Bank of America Corp. says the supply deluge could result in a “demand vacuum” for longer maturity bonds that could push yields higher and tighten financial conditions.

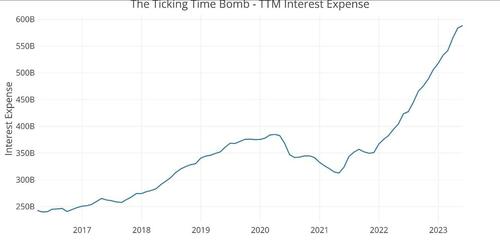

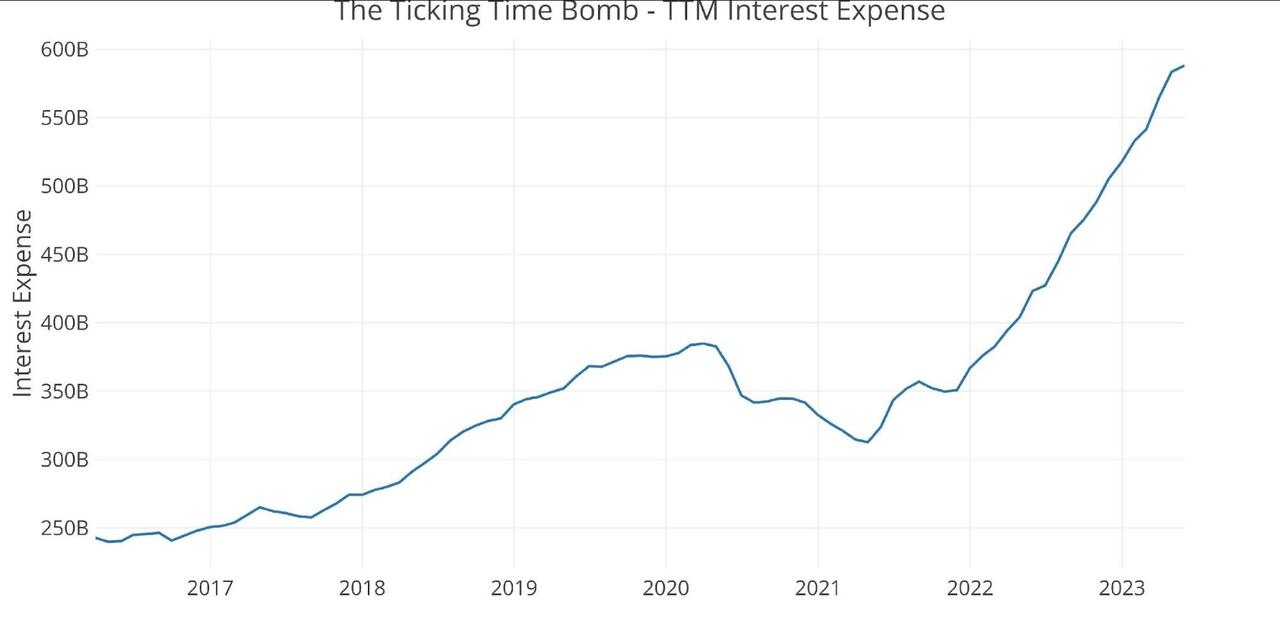

The problem isn’t purely a function of more debt. The bigger issue is that this new debt comes with a much steeper price tag. Interest on the national debt is rising at an alarming clip.

The trailing 12-month (TTM) interest on the debt clocked in at just under $600 billion in May. This was up from $350 billion at the start of 2022, less than 18 months ago. The government has added an extra $250 billion in expenses per year on just debt service.

This is just the beginning of an upward trend. Based on the current interest payments, the Treasury is paying less than 2% interest on the total debt. But a lot of the debt currently on the books was financed at very low rates before the Federal Reserve started its hiking cycle. Every month, some of that super-low-yielding paper matures and has to be replaced by bills, notes and bonds yielding much higher rates. That means interest payments will quickly climb much higher unless rates fall.

Looking at the Treasury sale on June 26 reveals the extent of the problem. The Treasury sold $162 billion in securities, with $120 billion in short-term Treasury bills with high yields.

$58 billion in six-month bills at an investment yield of 5.45%

$62 billion in three-month bills at an investment yield of 5.34%.

$42 billion in two-year notes at a high yield of 4.67%, amid very strong demand. Longer-term yields are still far below short-term yields.

With this flood of Treasury bills, the share of short-term paper underpinning the debt is approaching 20%. That’s considered the upper limit, meaning the Treasury will soon have to turn to issuing longer-term notes and bonds. That means the Treasury will be locking in higher interest rates for the long term.

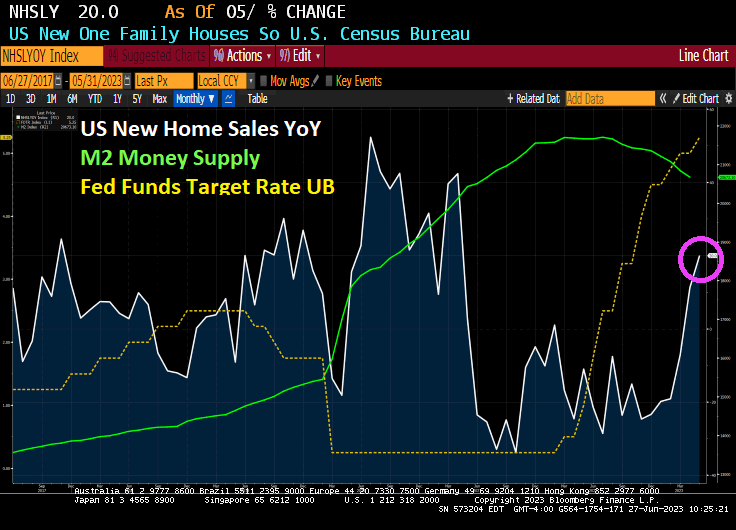

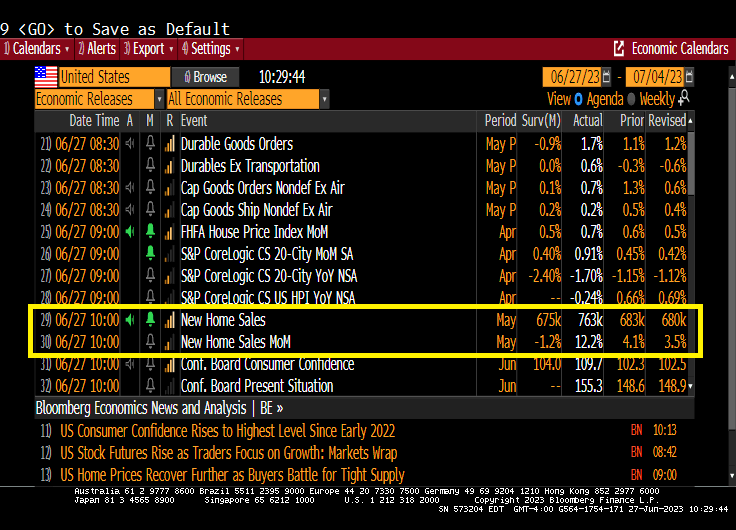

Well its about time that homebuilder started building again! And maybe it was The Fed rate hike pause (and possible rate cuts in the future.

US new home sales rose 20% in May as The Fed pauses rate hikes.

Fed Funds Futures point to one or two more rate hikes, then down she goes!!!

763k new homes were added in May

Remember, there is still a lot of stimulus (M2) sloshing around the economy. Perhaps we can rename all the infrastructure stimulus that is leaking out into the economy “Buttigieg Bucks.” Or “Buty Bucks!”

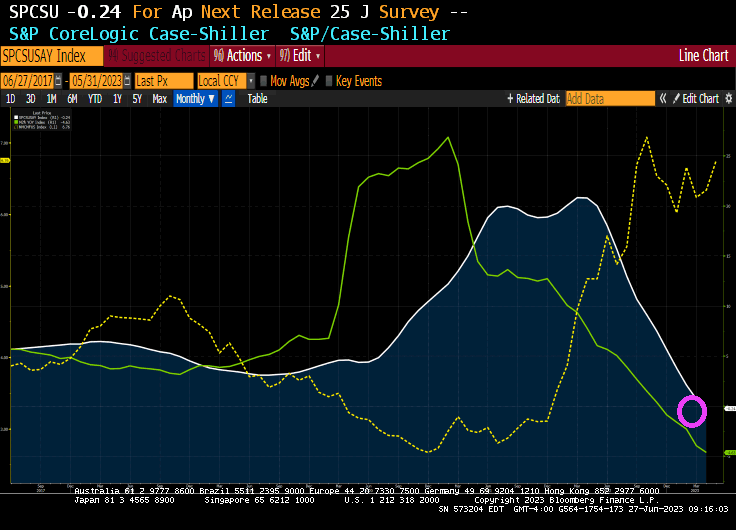

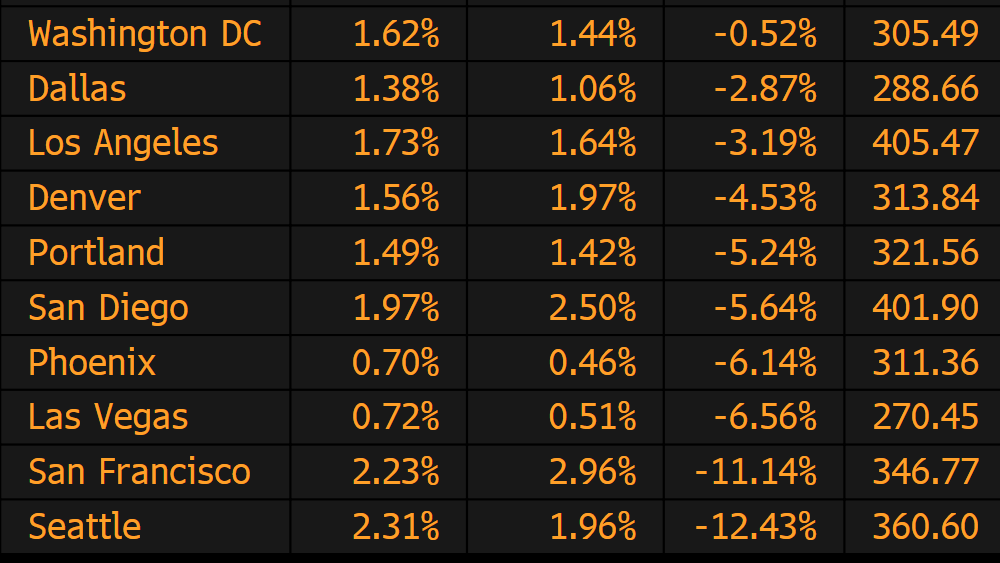

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a -0.2% annual decrease in April, down from a gain of 0.7% in the previous month. The 10-City Composite showed a decrease of -1.2%, down from the -0.7% decrease in the previous month. The 20-City Composite posted a -1.7% year-over-year loss, down from -1.1% in the previous month.

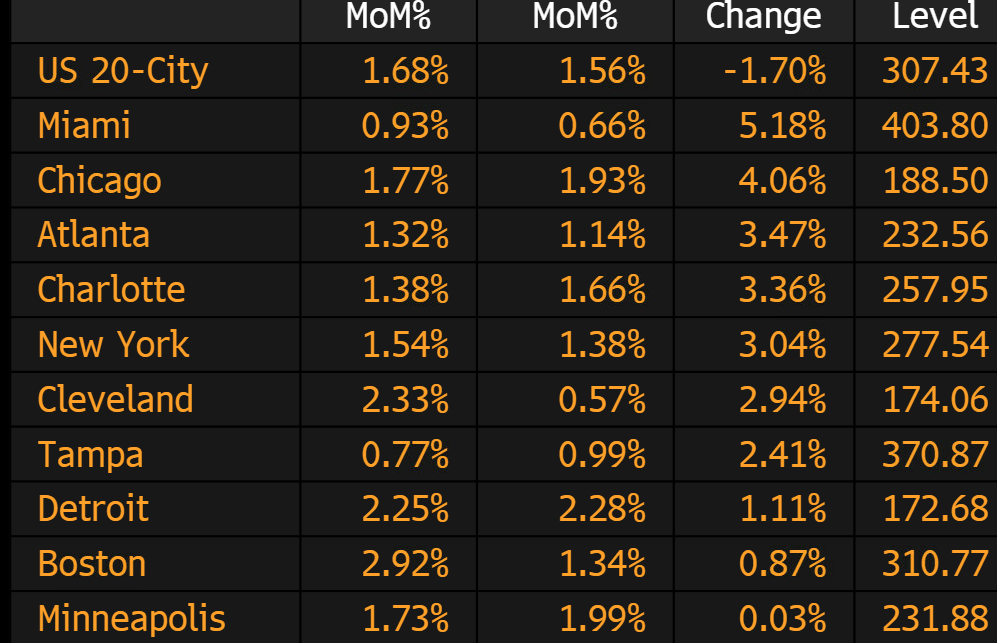

The winners in April? Miami and … Chicago?

The biggest losers in April? Seattle and San Francisco both suffered YoY losses over -11%.

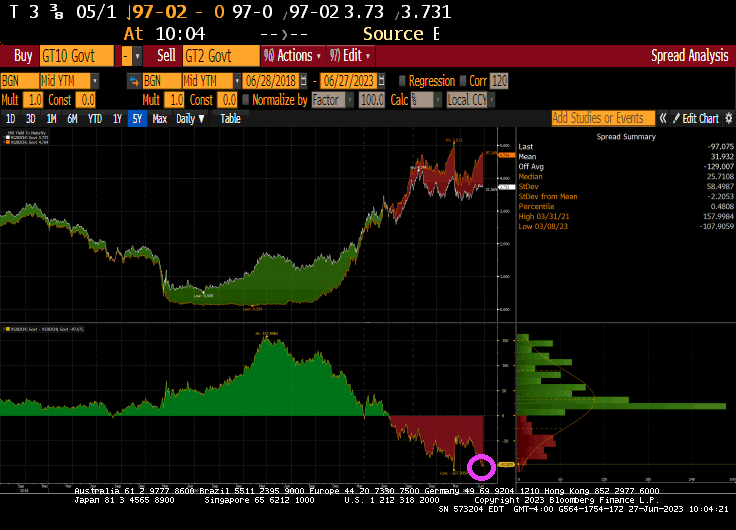

The US Treasury 10Y-2Y yield curve remains steeply inverted at -97 basis points.

Silverado! No, not the Chevy full-size pickup truck, but the precious metal Silver is up over 1% this morning!

The US Treasury 10Y-2Y yield curve remains inverted at -102.7 basis points for the 244th straight day as M2 Money YoY (aka, liquidity) evaporates.

Silver is up over 1% this morning.

Bitcoin Cash is up12.39% this morning.

Speaking of Silverado, a fully loaded new 2023 Chevy Silverado 1500 ZR2 costs around $100,000. Thanks Biden and Powell (BiPow?). Try financing that purchase with auto loan rates soaring!

Yes, the ECB’s own Fabio … Panetta wants to ban any competition to Central Bank printing presses. Of course, like Elizabeth Warren (D-MA) and SEC’s Gary “The Ghoul” Genslar, he wants to protect The Deep State’s monopoly on money printing by banning competition.

According to Fabio Panetta, crypto volatility and aspects of blockchain technology made digital assets only suitable for gambling…

Fabio Panetta, an executive board member of the European Central Bank (ECB), has suggested a dark future for cryptocurrencies, in which digital assets may be used for little more than gambling among investors.

In written remarks for a panel at the Bank for International Settlements Annual Conference on June 23, Panetta said crypto’s perception among investors as a “robust store of value” began to dissipate in late 2021 and into 2022, when the total market capitalization fell by more than $1 trillion. According to the ECB official, the “highly volatile” nature of crypto assets made them suitable for gambling, and should be treated as such by global lawmakers.

“Due to their limitations, cryptos have not developed into a form of finance that is innovative and robust, but have instead morphed into one that is deleterious,” said Panetta.

“The crypto ecosystem is riddled with market failures and negative externalities, and it is bound to experience further market disruptions unless proper regulatory safeguards are put in place.”

He added:

“Policymakers should be wary of supporting an industry that has so far produced no societal benefits and is increasingly trying to integrate into the traditional financial system, both to acquire legitimacy as part of that system and to piggyback on it.”

Panetta claimed the “security, scalability and decentralisation” of crypto transactions was “not achievable,” saying the immutability of blockchains is a negative aspect of the space due to transactions often being unable to be reversed. He cited the collapse of FTX, as well as a recent lawsuit brought by the United States Securities and Exchange Commission again Binance, as “fundamental shortcomings” of the ecosystem.

“Crypto enthusiasts would do well to remember that new technology does not make financial risk disappear,” said the ECB official.

“It is like pressing a balloon on one side: it will change in shape until it pops on the other side. And if the balloon is full of hot air, it may rise for a while but will burst in the end.”

Panetta has previously backed parts of the ECB’s plans for a potential digital euro, currently being researched by the central bank.

He has also proposed banning crypto assets with an “excessive ecological footprint” as part of efforts to address risks to the environment.

Panetta is similar to anti-competition Statists like Senator Elizabeth Warren and SEC’s Gary “The Ghoul” Genslar who don’t want competition for The Fed’s massive printing press.

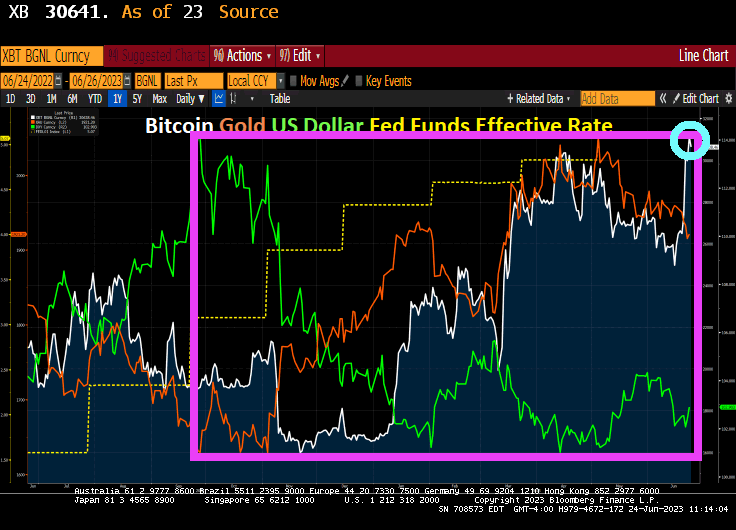

We know that Bitcoin along with Gold and Silver have done well the September 2022 when the US Dollar began to lose value.

Today, we are seeing a slight up-tick in Bitcoin (+0.05%) and Ethereum (+0.60%).

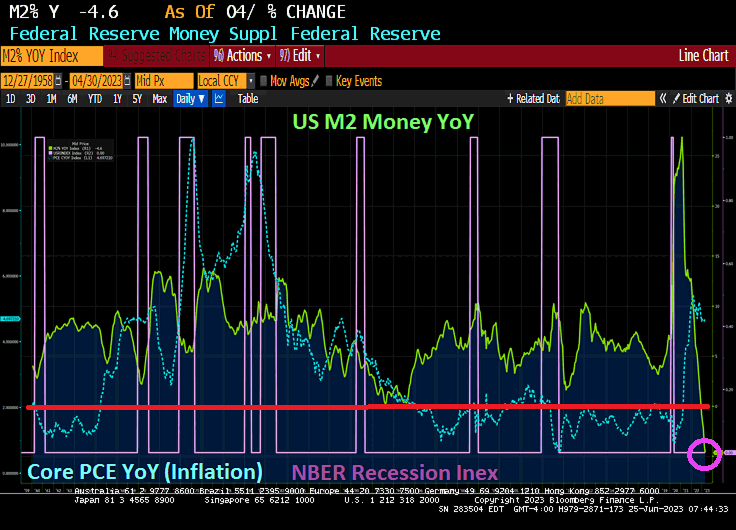

Money supply growth fell again in April from Jerome Powell And The Fed, plummeting further into negative territory after turning negative in November 2022 for the first time in twenty-eight years. April’s drop continues a steep downward trend from the unprecedented highs experienced during much of the past two years.

Yes, The Fed is printing money like it is going out of style! The war on Covid was similar to other wars fought where the US printed boatloads of money to pay for WWI. WWII, Korea and Vietnam wars. And the war against the middle class (known as The Best Depression). Apparently, The Fed is still waging war against the middle class.

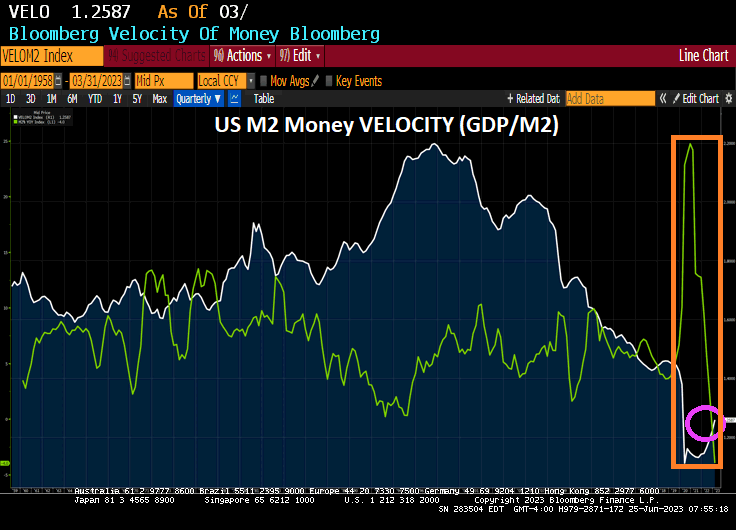

US M2 Money VELOCITY (GDP/M2) is near an all-time low after The Fed went berserk with money printing to combat the Covid economic and school shutdowns.

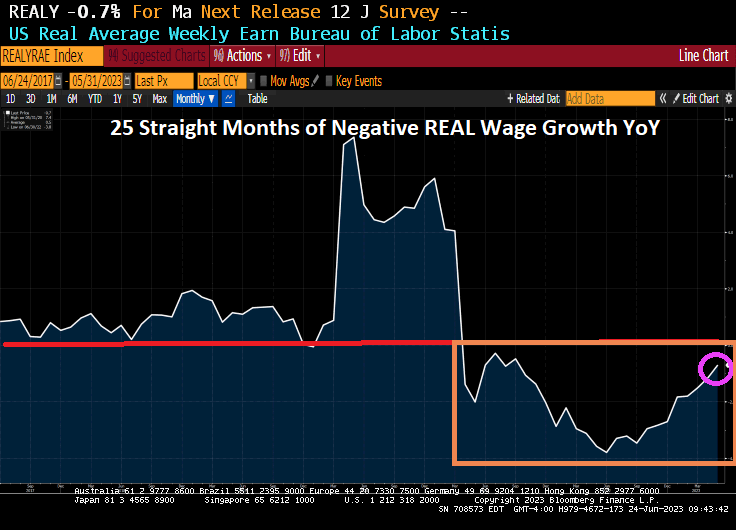

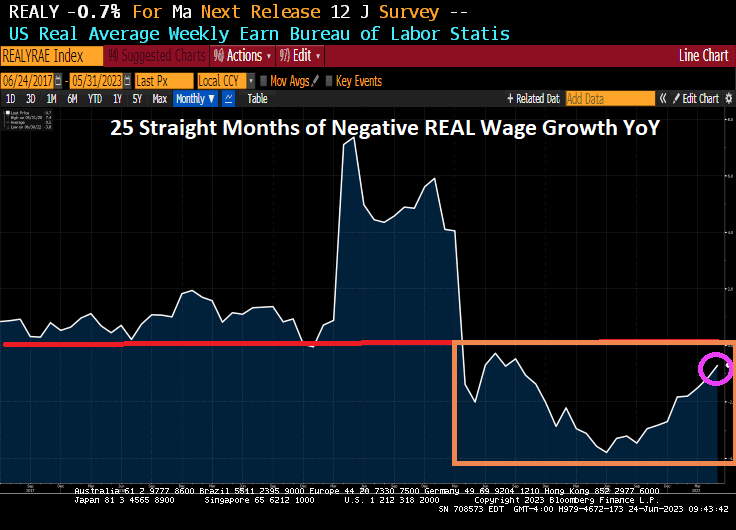

Then with The Fed’s massive monetary expansion and sudden contraction, we have REAL average weekly earnings growth YoY in negative territory for 25 straight months.

The Walking Dead’s Negan, the poster child for The Federal Reserve.

Well, with Jerome Powell And The Fed tightening monetary policy (about half way there!), we have seen competitors to the US Dollar Bitcoin and Gold have soared since September 26, 2022. Bitcoin is up 61%, Gold is up 18% and the US Dollar is down -10%.

Mortgage rates hover around 7% as the US Treasury 10-2Y curve inverts to over -100 basis points with M2 Money growth crashed and burned.

I could have used 3 shades of Joe, but 50 shades of Joe sounds better!

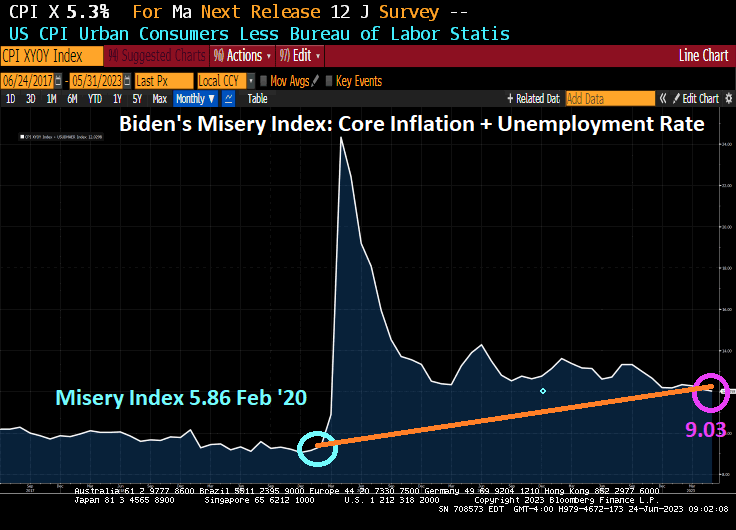

But the fact remains that Americans are far more miserable under Biden than they were under Trump before the Chinese Wuhan Covid virus was unleashed. 9.03 today (Core CPI YoY + U-3 Unemployment) than it was in February 2020 under Trump (5.86). While not twice as bad, inflation is continues to cause serious problems for America’s middle class and low-wage workers.

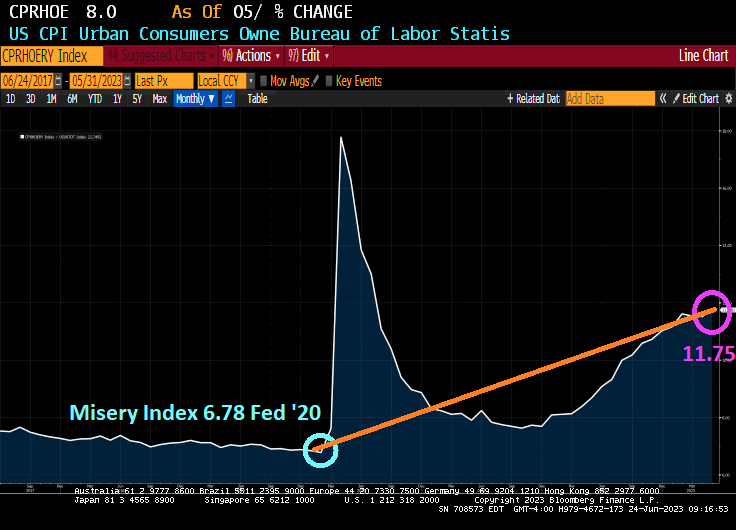

Speaking of the middle class and low wage workers, let’s look at the Renter’s Misery index (CPI Owner’s equivalent rent YoY + Unemployment rate). It was 6.78% in February 2020 under Trump and before Covid struck and is now 11.75% under Inflation Joe.

Speaking of misery, how 25 straight months of negative REAL wage growth? Real weekly wage growth went negative in April 2021, just a few months after Biden was installed as President.

Now, there was winners under Biden. Green energy donors, the big banks, big pharma, big tech, but media … essentially any big donors from big entities got massive payoffs. The middle class and low-wage workers? As Jerry Reid once sang, “They got the coal mine and we got the shaft.”

{kind=link}

{kind=link}

You must be logged in to post a comment.